ONL - You're The Next REIT Contestant On 'The Price Is Right'

2023-09-03 07:00:00 ET

Summary

- Bob Barker, the late host of The Price Is Right, was part of the greatest generation and had a diverse career in broadcasting.

- Crown Castle, Highwoods Properties, Safehold, Orion Office REIT, and Medical Properties Trust are recommended as attractive REIT investments.

- These REITs offer a margin of safety and potential for price appreciation in the next 12 months.

An American legend passed away this month.

Younger generations – many millennials, Gen Zers, and especially the Alpha bunch of kiddos - might not know the name. In fact, chances are very, very high the latter two don’t.

But Gen X, Boomers, the silent generation, and those of the greatest generation still with us should be very familiar with the late and great Bob Barker of The Price Is Right fame.

At 99 years old when he died, Barker was part of that latter group: the greatest generation. Born on December 12, 1923, he missed World War I by a solid several years. But he would have been intensely aware of World War II.

He even joined the United States Navy Reserve to train as a fighter pilot. And while he didn’t end up serving in combat, I imagine the experience of just being alive back then had an impact on him.

How could it not?

For the record, you’re forgiven if you didn’t know that detail about Barker. It certainly wasn’t what made him a household name. Nor was it the fact that he graduated with a degree in economics – summa cum laude, too.

I’m not sure if he ever officially used it. However, I guess if an economics grad is going to make it big in TV…

The Price Is Right is going to be it.

Come on Down! You’re the Next Contestant on “The Price Is Right!”

Here’s another thing you may or may not know about the now late and always great Bob Barker…

He was not the first host of The Price Is Right . As NBC News wrote in his obituary :

“When producers hired Barker to host The Price Is Right in 1972, they hit the jackpot. The gameshow had faded significantly from its glory days in the late ‘50s and had been punted by two networks before it landed at CBS.

But in Barker, the show found its voice. And it has continued to air a decade and a half after he retired.”

As it also notes, Barker was hardly a newbie at broadcasting. In fact, “Barker landed a job at a radio station in Florida,” presumably shortly after his college graduation. There:

“… it didn’t take long for word of his smooth delivery to travel across the wires. In 1950, he moved to California to start his own radio program, The Bob Barker Show, in Burbank.

“Television producers clearly tuned in, and Barker landed his first game show in 1956, NBC’s Truth or Consequences, a job he would hold for 18 years until it went off the air.”

Incidentally, other sources seem to indicate that he wasn’t the show’s final host. And that he only hosted the show for nine years, not 18.

Perhaps NBC – if it’s in the wrong – was a bit distracted by the fact that it was the original Price Is Right network… a show it eventually let go to CBS, where Bob Barker made it one for the books.

Sorry, NBC. Sometimes you make ‘em. And sometimes, them’s just the breaks.

And the Actual Retail Price Is…

From all accounts, Barker was quite the standout guy, even in a crowded field of TV show talent. Everyone wanted a piece of him, with USA Today adding that :

“Barker narrated the Pillsbury Bake-Off for 16 years and the Tournament of Roses Parade for 19 years. For 22 years, until 1987, Barker served as host of the Miss USA and Miss Universe pageants.”

Then:

“In 1996, Barker made his feature acting debut in Happy Gilmore, in which he made use of his black belt in karate by clobbering Sandler. When moviegoers clamored for more of Barker… he offered a typically cheeky explanation: ‘I refuse to do nude scenes. I don’t want to be just another beautiful body.”

That’s why I said in the beginning that “many millennials” wouldn’t know who he was, not “most millennials.” Because the truth is that, after Happy Gilmore , “vacationing college students competed with housewives and retirees to come down to contestants’ row.”

With so many contestants across so many ages, races, backgrounds, and time overseen by a personality like Bob Barker, it only makes sense that there were memorable moments on the show. Like the one from a 1977 episode, with Barker himself recalling :

“The most talked about single incident in the history of the show was a young lady seated out in the audience in a tube top. And her name was called to be a contestant. And she jumped to her feet. And she began jumping up and down, and out they came. She came on down, and they came on out on CBS.”

I can’t promise you’ll be THAT happy about the following REIT picks and prices I’ve put together in honor of Bob Barker.

But I do think you’ll be pretty pleased nonetheless.

The Price is Right Means a Margin of Safety

As Seth Klarman wrote.

“A market downturn is the true test of an investment philosophy. Securities that have performed well in a strong market are usually those for which investors had the highest expectations. When these expectations are not realized, the securities which typically have no margin of safety, can plummet.”

He added,

“Value investors are not super sophisticated analytical wizards who create and apply intricate computer models to find attractive opportunities or assess underlying value. The hard part is discipline, patience, and judgement.

Investors need discipline to avoid the many unattractive pitches that are thrown, patience, to wait for the right pitch, and judgment to know when it is time to swing.”

Batter up!

Crown Castle ( CCI )

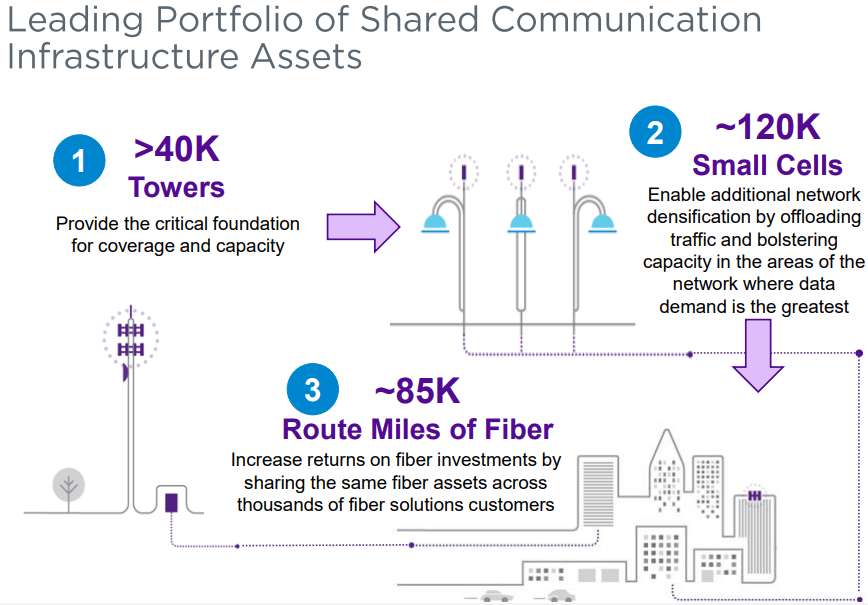

Crown Castle is a cell tower REIT and is the largest provider of shared communications infrastructure in the U.S. Their portfolio consists of more than 40,000 cell towers, roughly 120,000 small cell nodes, and around 85,000 route miles of fiber.

CCI’s assets are critical to a functioning society as their communications infrastructure enables people and businesses to connect to data, technology, and wireless services they routinely depend on. CCI’s core business is providing access to their shared communications infrastructure with long-term contracts that include leases, subleases, licenses, and service agreements.

In addition to generating revenue by leasing space on their communications infrastructure, CCI also provides ancillary services that are primarily related to their tower segment.

They provide site development services which include equipment installation, architectural and engineering, and zoning and permitting services. Crown Castle’s largest tenants are AT&T, T-Mobile, and Verizon Wireless which combined made up approximately 75% of their site rental revenues for the first half of 2023.

{kind=link}

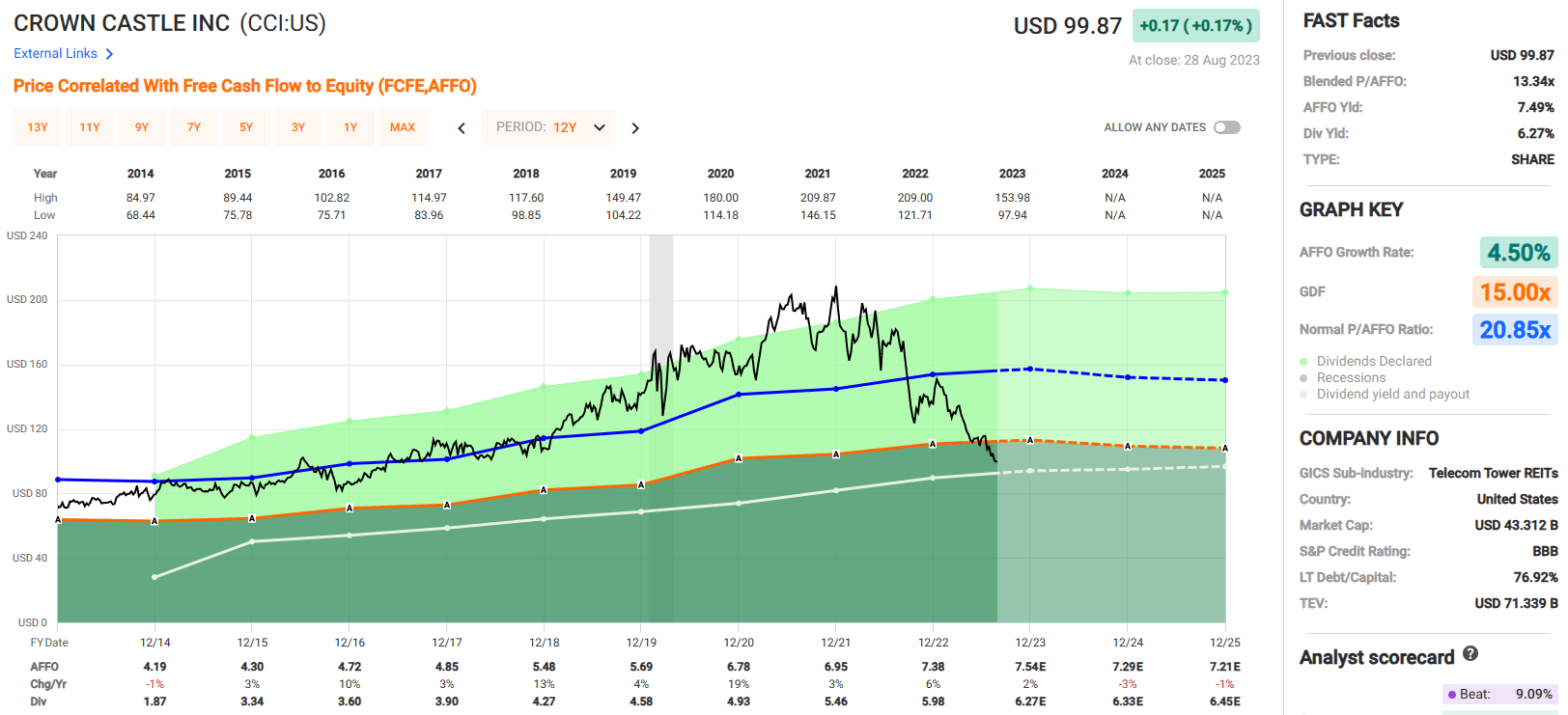

Crown Castle is investment-grade with a BBB credit rating and has sound debt metrics with a net debt to EBITDA of 5.56x and an EBITDA to interest expense ratio of 6.51x.

Their debt is 87% fixed rate and 93% unsecured with a weighted average coupon of 3.8% and a weighted average term to maturity of 7.9 years. Since they converted to a REIT in 2014, CCI has had an average AFFO growth rate of 4.50% and an average dividend growth rate of 17.43%.

Crown Castle pays a 6.27% dividend yield that is well covered with an AFFO payout ratio of 80.96% and currently trades at a P/AFFO of 13.34x which is a significant discount to their normal AFFO multiple of 20.86x.

{kind=link}

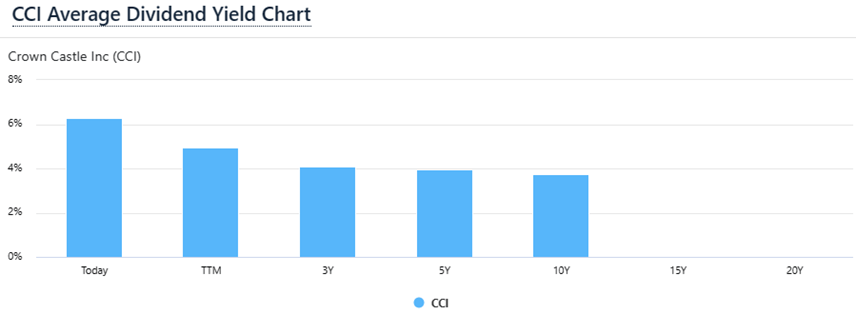

In addition to trading well below their normal AFFO multiple, CCI is trading at a discounted valuation when measured by its dividend yield. CCI’s current yield of 6.27% is well above their historical averages with their dividend yield averaging 3.72% over the last 10 years, 3.94% over the last 5 years, and 4.10% over the last 3 years.

We rate Crown Castle a Strong Buy with a Buy Under target of $170.00 and a Margin of Safety of 40.82%.

{kind=link}

Highwoods Properties ( HIW )

Highwoods Properties is an office REIT based out of Raleigh, North Carolina that develops, acquires, and manages office properties that are primarily located in the Sunbelt region of the U.S.

It’s hard to overstate their focus on the Sunbelt as Highwoods generates 95% of their net operating income (“NOI”) from Sunbelt markets.

Their primary markets are located in the best business districts of Raleigh, Charlotte, Atlanta, Dallas, Nashville, Richmond, Tampa and Orlando and based on NOI their largest three markets are Raleigh at 23.8%, Nashville at 22.1%, and Atlanta at 15.8%.

Based on revenue, HIW’s largest three industries are Finance & Banking which contributes 18.3%, Legal & Accounting Services which contributes 15.9%, and Insurance which contributes 11.6%.

Additionally, their largest three tenants are Bank of America which contributes 3.82%, Asurion which contributes 3.49%, and the Federal Government which contributes 2.66% of their revenue.

As of the end of the second quarter, HIW’s portfolio consisted of 28.5 million rentable square feet (“RSF”) of in-service properties, 1.6 million RSF of properties under development, and development land that has the potential to add approximately 5.2 million RSF of office build out.

As of June 30, 2023, their portfolio had an 88.9% occupancy rate with a weighted average lease term of 6 years.

{kind=link}

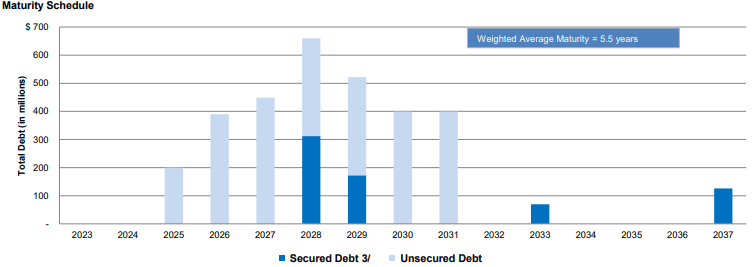

Highwoods is investment grade with a BBB credit rating and has solid debt metrics including a net debt to EBITDAre of 6.0x and an EBITDA to interest expense ratio of 3.97x.

Their debt is 77.0% fixed rate and 78.8% unsecured with a weighted average interest rate of 4.3% and a weighted average term to maturity of 5.5 years. Additionally, they have $747 million in total available liquidity and no debt maturities until the fourth quarter of 2025.

{kind=link}

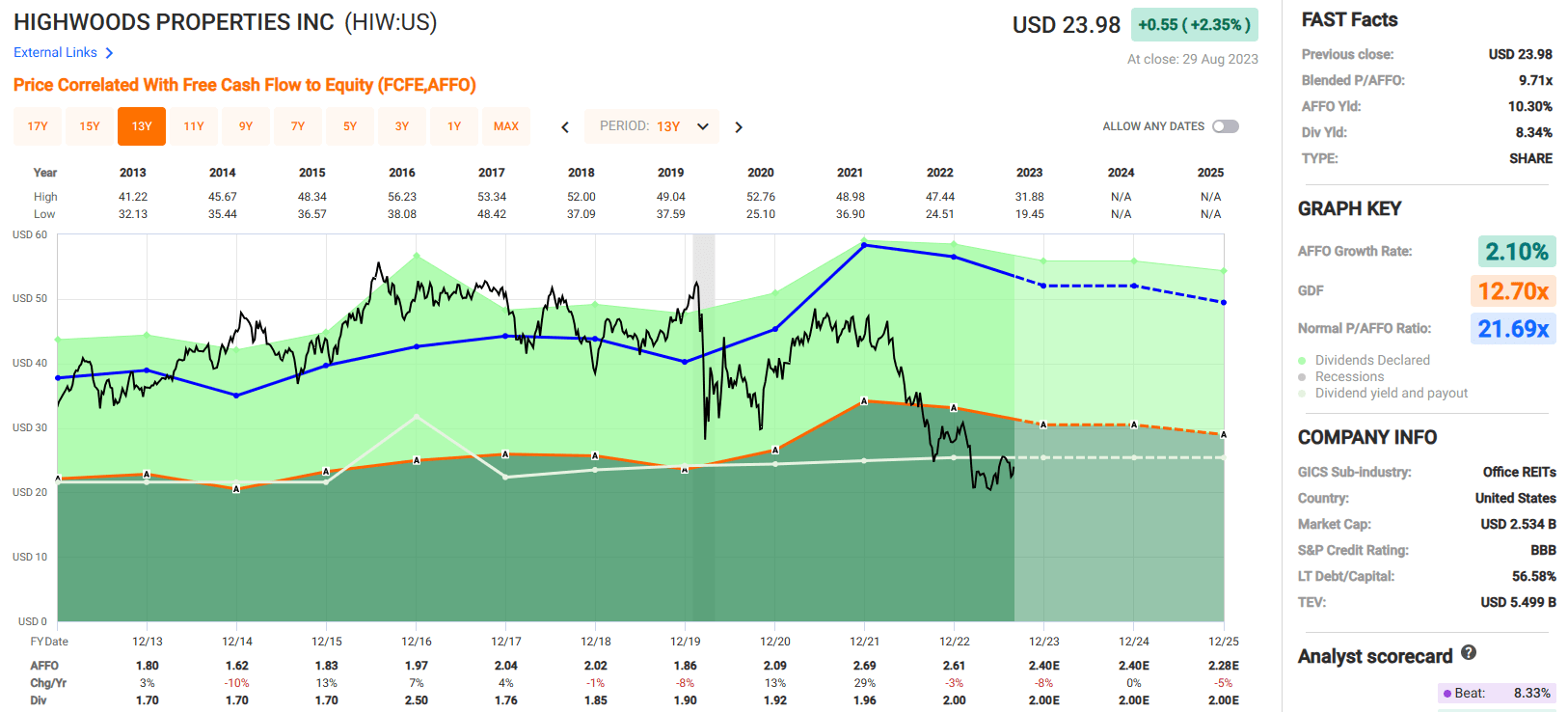

Over the past 10 years, HIW has had an average AFFO growth rate of 2.10% and a compound dividend growth rate of 1.64% They currently pay an 8.34% dividend yield that is well covered with an AFFO payout ratio of 76.74% and the stock is currently trading at a P/AFFO of 9.71x which is a massive discount to their 10-year average AFFO multiple of 21.69x.

{kind=link}

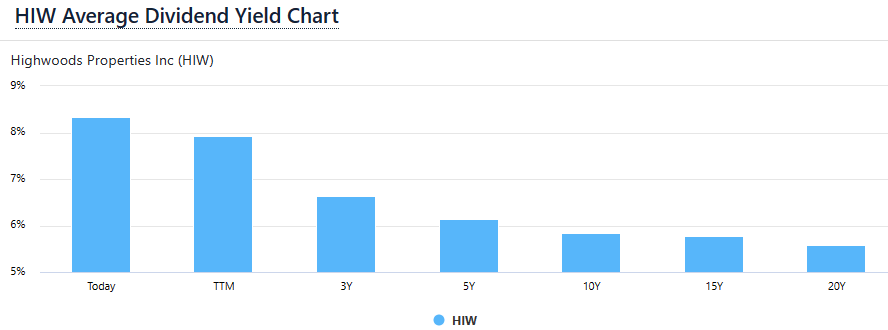

Additionally, the stock is trading almost 40% below its net asset value (“NAV”) with a P/NAV ratio of 0.64x and is also trading at a discount based on its current dividend yield compared to its historical averages with a current yield of 8.34% compared to its 10-year average yield of 5.84%, its 5-year average yield of 6.15%, and its 3-year average yield of 6.63%.

We rate Highwoods Properties a Strong Buy with a Buy Under target of $37.50 and a Margin of Safety of 36.29%.

{kind=link}

Safehold ( SAFE )

Safehold is an internally managed REIT that specializes in ground leases. The company went public in mid-2017 as an externally managed REIT and was the first public company that primarily focused on ground leases.

On August 10, 2022, SAFE and its external manager iStar entered into a merger agreement which was completed on March 31, 2023. The details of the merger are somewhat complicated since it was considered a reverse merger, but essentially the “Old SAFE” merged with and into iStar and ceased to exist.

iStar continued as the surviving company and changed its name to Safehold Inc. As part of the agreement, iStar spun off its legacy assets (non-ground lease properties) and the combined company Safehold Inc. internalized its management.

Ground leases can be described as the ownership of land underlying commercial properties that are leased by the land owner ((SAFE)) to a tenant that owns or operates the property on top of the land.

The leases are long term, typically ranging between 30 and 99 years, and are generally structured as a triple-net lease. Additionally, ground lease agreements typically include provisions that at the end of the lease term or upon default, the land and building revert back to the ground lease landlord ((SAFE)).

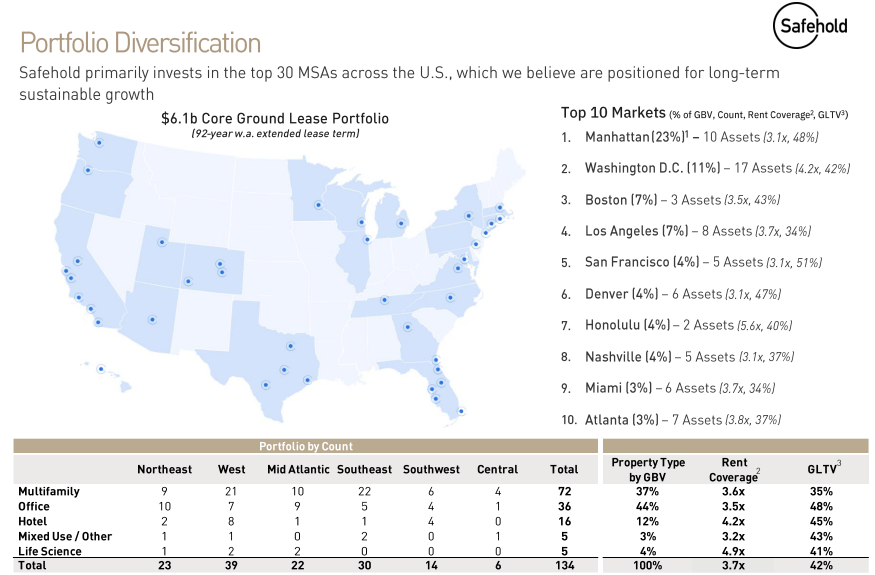

Like most other triple-net leases, SAFE’s ground leases include contractual rent increases either at a fixed rate or CPI based. SAFE’s CPI lookbacks are typically capped between 3.0% and 3.5% and normally start between years 11 and 21 of the lease term. SAFE has a $6.1 billion core ground lease portfolio with a 92 year weighted average extended lease term.

Their land is leased to owners or tenants of multiple property types including multifamily, office, hotel, mixed-use, and life science and their total portfolio has 3.7x rent coverage and a ground lease to value (“GLTV”) of 42%.

{kind=link}

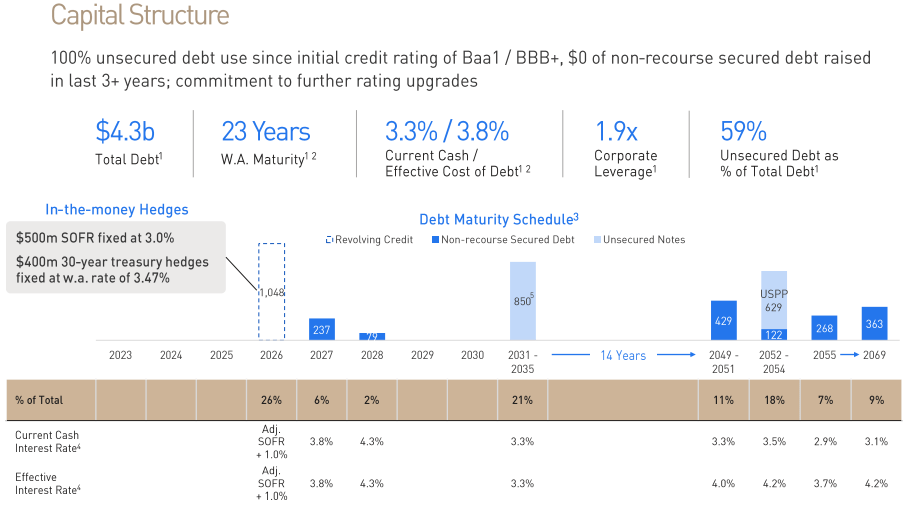

Safehold is investment grade with a Baa1 rating from Moody’s and a BBB+ rating from Fitch. They have a corporate leverage (debt / book equity) ratio of 1.9x and their debt is 59% unsecured with an effective interest rate of 3.8% and a weighted average debt maturity of 23 years. Additionally, SAFE has $816.0 million in liquidity and no debt maturities until 2026.

{kind=link}

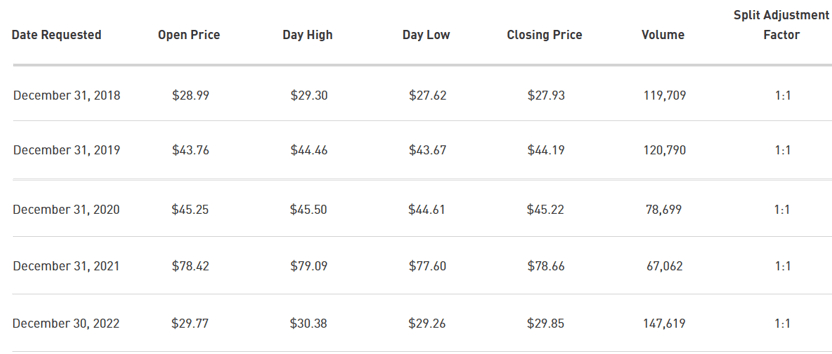

I pulled the information below from the investor relations section of SAFE’s website. I noticed that several financial sites list different information regarding their price, earnings, dividend rate, dividend yield, etc., so I went straight to SAFE’s filings to get a better picture.

For their annual earnings per share (“EPS”) I pulled the 2018 - 2022 info from their Form 10-K’s and for the current column I annualized their second quarter EPS of $0.35. Similarly I annualized their Q2 dividend to get the current annual dividend rate of $0.71 per share.

SAFE IR (compiled and calculated by iREIT)

{kind=link}

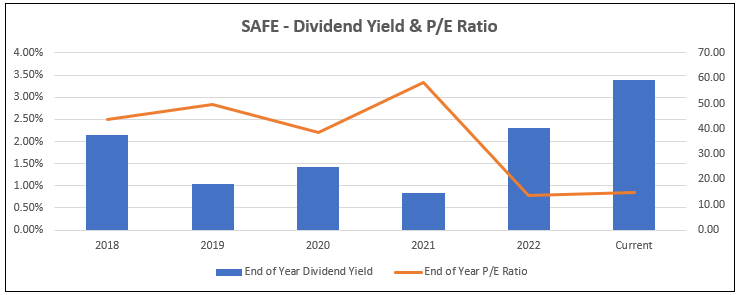

As illustrated below, it is easy to see that SAFE is currently trading at a historically low valuation as it relates to its earnings and dividend yield. SAFE grew its earnings from $0.64 per share in 2018 to $2.21 per share as of the end of 2022, yet its end of year P/E multiple compressed from 43.64x to 13.51x over that time.

Similarly, its current dividend yield is at all-time highs with the stock currently yielding 3.39% verses its end of year dividend yield of 2.15% in 2018 and SAFE is trading at about a 30% discount to its estimated net asset value with P/NAV ratio of 0.71x.

We rate Safehold a Strong Buy with a Buy Under target of $47.00 and a Margin of Safety of 55.40%.

{kind=link}

Orion Office REIT ( ONL )

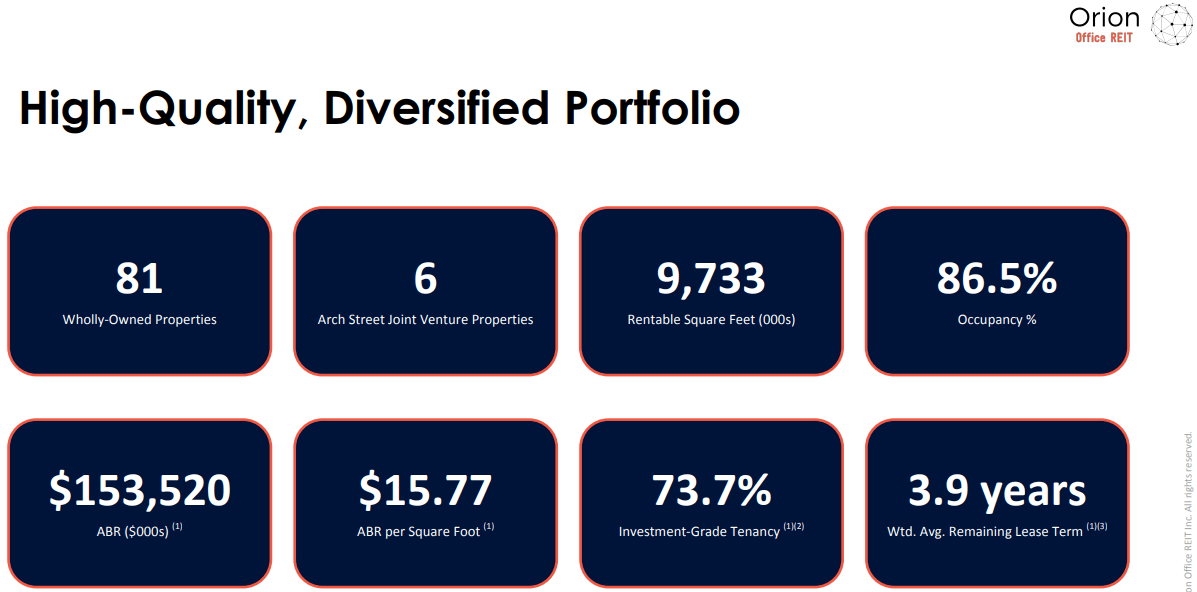

Orion Office REIT was spun-off from Realty Income in late 2021 in connection with the VEREIT merger and its portfolio is primarily made up of the office properties that both companies previously held. ONL is an internally managed REIT that acquires and manages a portfolio of office properties located in suburban markets in the U.S. that are primarily leased to a single tenant on a net lease basis.

ONL writes triple-net, double-net, and modified gross leases with lease terms that are 8 to 12 years on average and include annual rent escalations. Orion Office REIT owns and manages 81 office properties covering approximately 9.5 million leasable square feet that are located in 29 states within the U.S.

Additionally, ONL has a 20% ownership interest in an unconsolidated joint venture (“JV”) with Arch Street Capital Partners, LLC, which consists of 6 properties located in 6 states which covers roughly 1.0 million leasable square feet.

As of the end of the second quarter, ONL’s portfolio had an occupancy rate of 86.5%, with almost 74% of their ABR derived from investment-grade tenants, and a weighted average lease term of 3.9 years.

{kind=link}

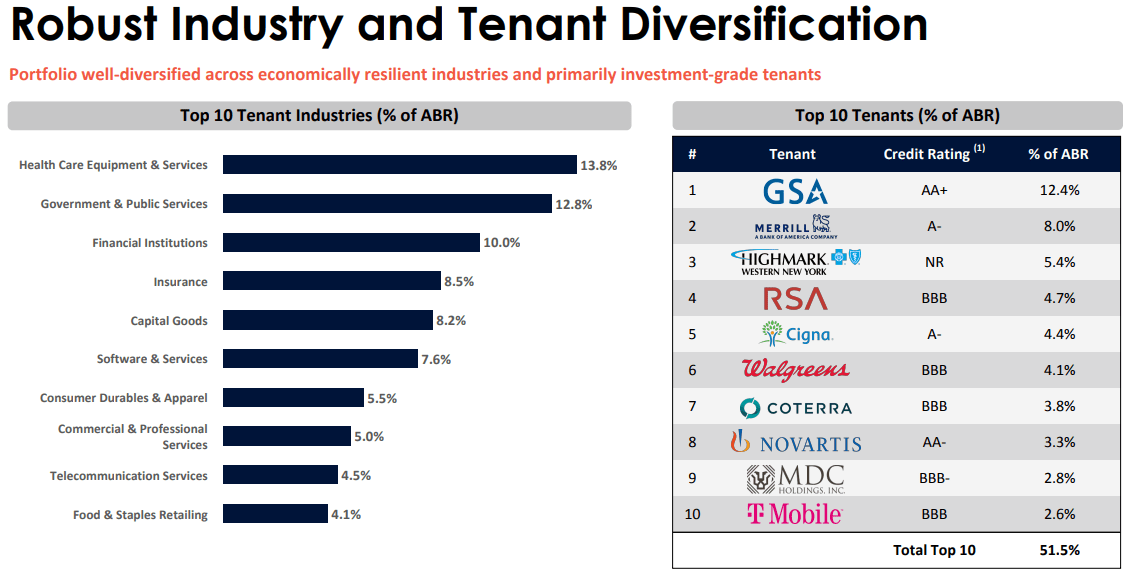

Orion has high-quality tenants listed in their top 10. As a matter of fact, 9 out of their top 10 tenants are investment grade rated. Their top tenant, GSA (General Services Administration), is a government agency that has an AA+ credit rating and contributes 12.4% of their ABR.

Other notable names include Merrill Lynch, Cigna, Walgreens, Novartis, and T-Mobile. They do have a high amount of concentration in their top 10 tenants as they make up over half of their ABR.

{kind=link}

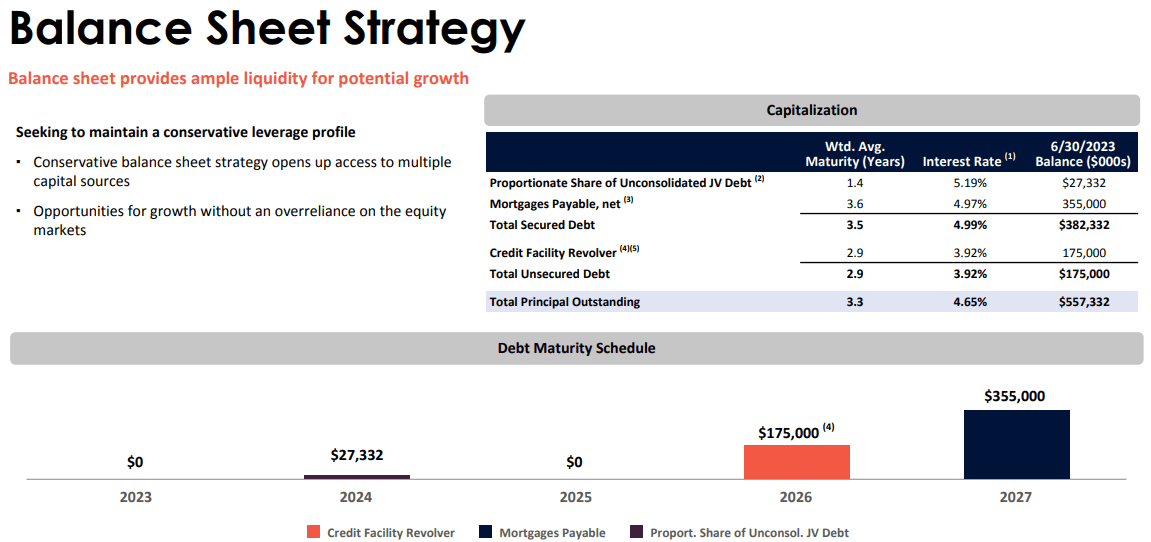

Orion has a strong balance sheet with a net debt to adjusted EBITDA of 3.93x, a long-term debt to capital ratio of 36.51%, and an EBITDA to interest expense ratio of 4.13x. A large portion of their debt consists of mortgages payable and approximately 68.60% of their debt is secured.

However, they have no debt maturities in 2023 and no significant maturities until 2026. Their debt has a weighted average maturity of 3.3 years with an average interest rate of 4.65% and as of June 30, 2023, the company had $292.9 million of liquidity.

{kind=link}

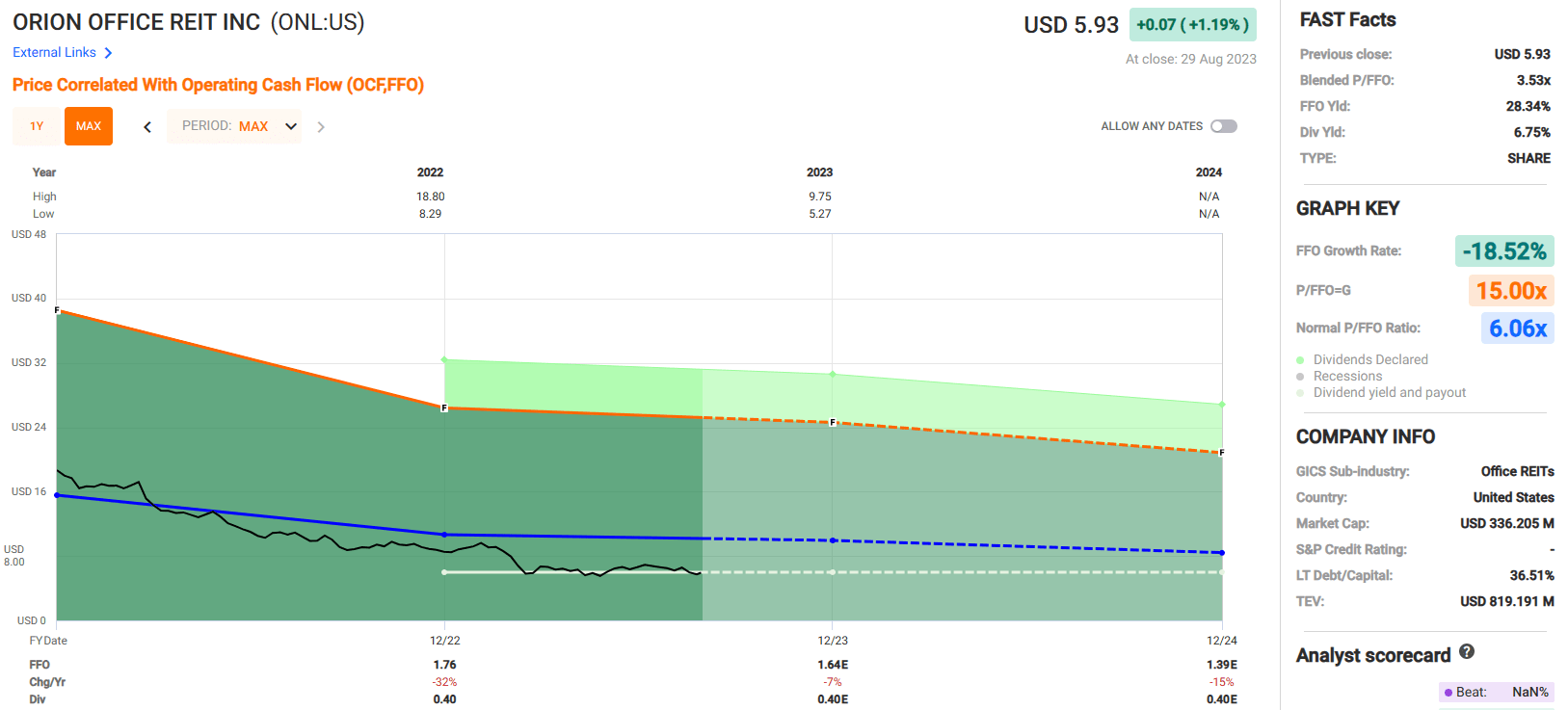

When looking at ONL’s valuation we don’t have a lot of history to judge it on since it only became a stand-alone company at the end of 2021. However, we can see how it compares to its peers in the office sector.

On a relative basis Orion Office REIT has the second lowest P/FFO ratio out of all the office REITs in our coverage and in absolute terms, paying 3.49 times their annual funds from operations is a very attractive valuation for most companies.

FAST Graphs (compiled by IR)

Since Orion’s formation in late 2021 the company has had a blended average negative AFFO growth rate of -18.52%. Keep in mind that they were spun-off right before the office sector meltdown in 2022 as the work from home movement really gained steam.

Analysts expect FFO to fall by -7% in the current year and then by -15% in 2024.

While the office sector has experienced significant headwinds since the pandemic, I believe the concerns over the work-from-home movement along with the negative growth projections have already been priced in with the stock trading at a P/FFO of 3.49x.

ONL pays a 6.83% dividend yield that is very secure with an FFO payout ratio of 22.73% as of the end of 2022. Additionally, they are trading at a significant discount to their estimated net asset value with a P/NAV ratio of 0.46x.

We rate Orion Office REIT a Spec Buy with a Buy Under target of $7.00 and a Margin of Safety of 16.29%.

{kind=link}

Medical Properties Trust ( MPW )

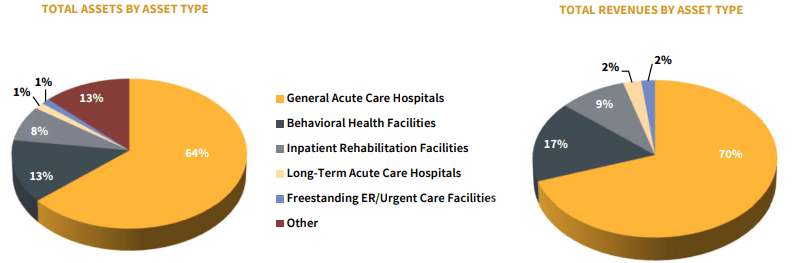

Medical Properties Trust is a healthcare REIT that primarily invests in net-leased hospitals, but also invests in other medical real estate such as behavioral health facilities and post-acute facilities.

As mentioned, the majority of their properties consist of general acute care hospitals which contributed 69.6% of their second quarter revenues, but they also received 16.7% of their Q2 revenues from behavioral health facilities, and 9.3% from inpatient rehabilitation centers.

MPW’s portfolio consists of 444 properties that contain roughly 44,000 licensed beds located in 31 states across the U.S. and international properties located in the United Kingdom, Germany, Switzerland, Spain, Finland, Italy, Colombia, and Portugal.

{kind=link}

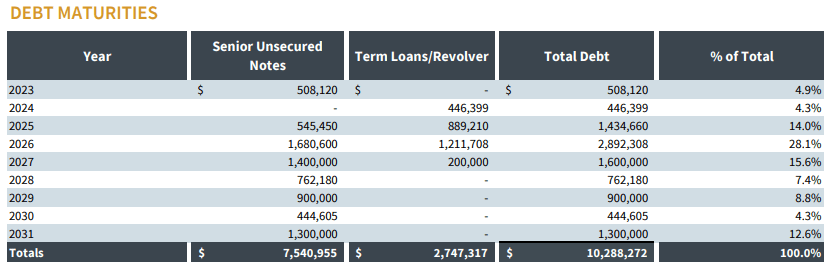

MPW is not investment-grade with a BB credit rating (junk rated) from S&P Global. They have an adjusted net debt to adjusted EBITDAre ratio of 6.8x, a long-term debt to capital ratio of 52.45%, and an adjusted interest coverage ratio of 3.4x.

Their debt is 86% fixed rate with weighted average interest rate of 3.93%, and as of August 4 the company had approximately $800 million in liquidity. Over the past year MPW has placed a large emphasis on reducing their leverage and strengthening their balance sheet.

They have been engaged in asset sales to help accomplish this goal which includes the sale of their Australia hospitals which is expected to be completed by the fourth quarter of this year and their planned sale of 3 Connecticut facilities to Yale which is expected to close before the end of 2023.

In addition to their asset sales, MPW announced on August 21 that it had reduced its quarterly dividend from $0.29 to $0.15 per share, representing a dividend cut of nearly 50%.

{kind=link}

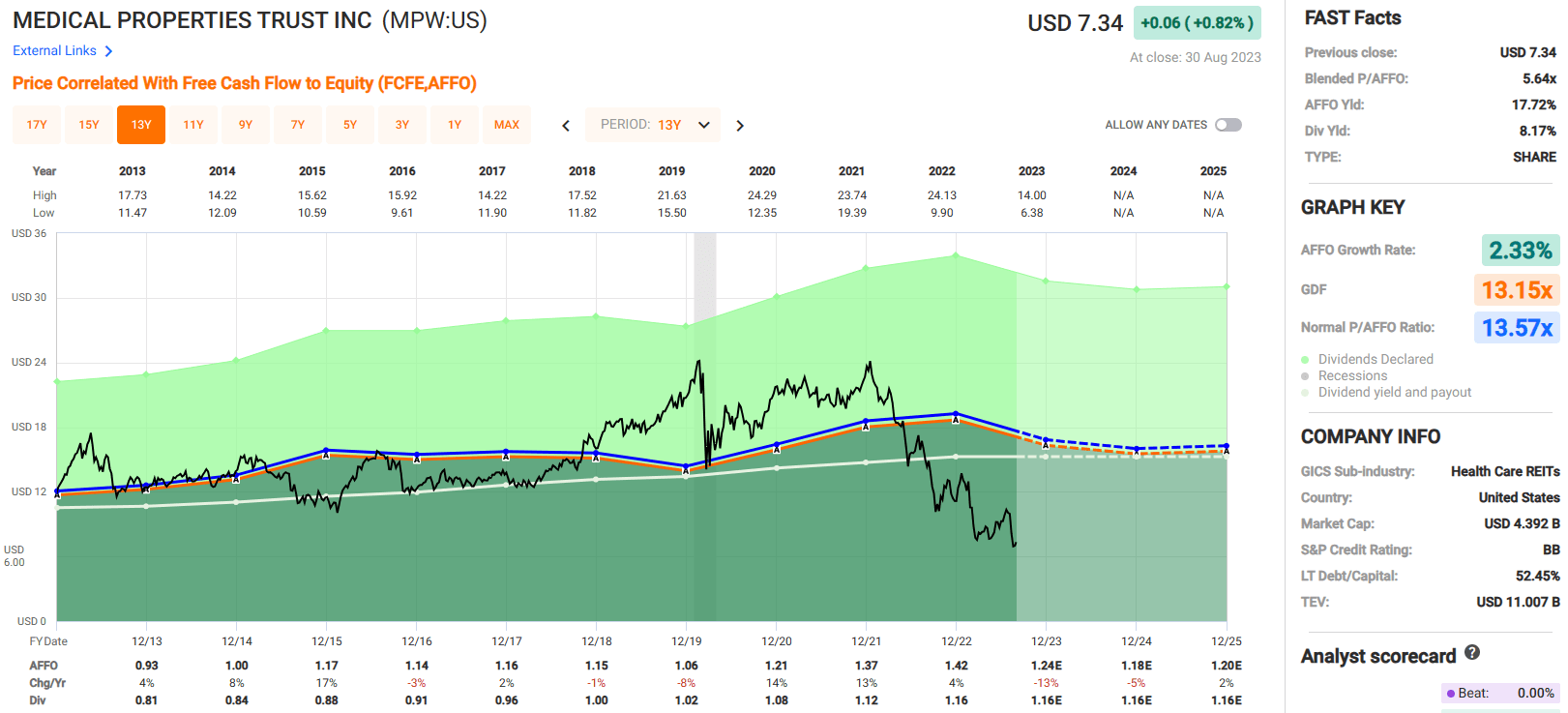

The dividend cut was highly anticipated by the market and did not cause a severe sell-off. Actually, the stock has risen in price since the announcement, going from $7.01 on August 21 to $7.34 as of yesterday’s close.

Even after the cut, the new annualized dividend rate of $0.60 per share still provides a yield of over 8% with a normalized funds from operations (“NFFO”) dividend payout ratio of approximately 40% based on the midpoint of their 2023 NFFO guidance of $1.55 per share.

Currently MPW is trading at a blended P/AFFO ratio of 5.64x which is a significant discount to their 10-year average AFFO multiple of 13.57x. Similarly, the stock is trading at a significant discount to its estimated net asset value with a P/NAV ratio of 0.60x.

We rate Medical Properties Trust a Buy with a Buy Under target of $17.00 and a Margin of Safety of 56.82%.

{kind=link}

In Closing…

In a recent article I highlighted the fact that “with our forecasted Q1-24 investment spreads returning back to 300 basis points or higher, we believe that REITs will become more attractive as investment spreads will widen.”

That’s our thesis and the primary catalyst that should spark an anticipated REIT rally.

In our view, these REITs (referenced in this article) represent an attractive opportunity for price appreciation over the next 12 months. Arguably, these aren’t the safest REITs in terms of quality; however, we believe there’s a significant margin of safety .

Note: Brad Thomas is a Wall Street writer, which means he's not always right with his predictions or recommendations. Since that also applies to his grammar, please excuse any typos you may find. Also, this article is free: Written and distributed only to assist in research while providing a forum for second-level thinking.

For further details see:

You're The Next REIT Contestant On 'The Price Is Right'