VNO - You Say Vornado I Say Vornado

Summary

- Vornado is one of the Office REITs with the highest upside we consider relevant at this time here at iREIT on Alpha.

- Vornado is a very strong NYC-based office REIT with a great platform and portfolio, and there are key arguments for why we may see a reversal here.

- While speculative, we like Vornado here, and consider it a speculative "BUY." Learn why here.

This article is coproduced with Wolf Report.

In this article, we'll take a closer look at one of our more speculative office REIT plays - Vornado Realty Trust ( VNO ).

While speculative plays are not everyone's cup of tea, we try to make sure that even our speculative plays are, in the end, qualitative enough for you to trust.

Let me show you exactly why this is.

Vornado Realty - New York offices at a steep discount

At its heart, Vornado is an NYC-focused office real estate investment trust ("REIT") with significantly qualitative assets in its portfolio. NYC hasn't exactly seen the most favorable of developments over the past 3 years.

First COVID-19, then people leaving, then companies leaving. All of this has left investors with questions such as if the Office REIT model is still even still workable.

At iREIT on Alpha, we believe this to be the case.

VNO IR

The argument for office REITs is usually that the company's operating area is qualitative, with good demographical development and good forecasts. This makes it difficult when a REIT is exposed to only one geography.

The city may still have a decent labor pool and forecasts for economic growth isn't horrendous, but it's definitely been somewhat tarnished from what it offered back in 2019 before COVID-19 came.

This company is used to being undervalued - so much so that management mentions it in investment material as one of the reasons to invest in VNO - the deep discount to NAV.

This upside is aside from its experienced management team, its attractive overall yield, its at least decent balance sheet, and it being one of the few ways to invest in growing Manhattan... the company mix isn't just office either - just most of it.

VNO IR

It's also important to mention that VNO is diversifying away exactly from its significant office focus , looking for multifamily developments, soundstages, casinos, and retail, which brings a positive component to an otherwise office-heavy NOI mix.

The company has delivered significant progress on its non-office portfolio, including more than a half-dozen residential developments in various NYC areas and Northern Virginia. The soundstages and gaming licenses just add more variety to things here - and also remember, VNO is growing its retail exposure as well.

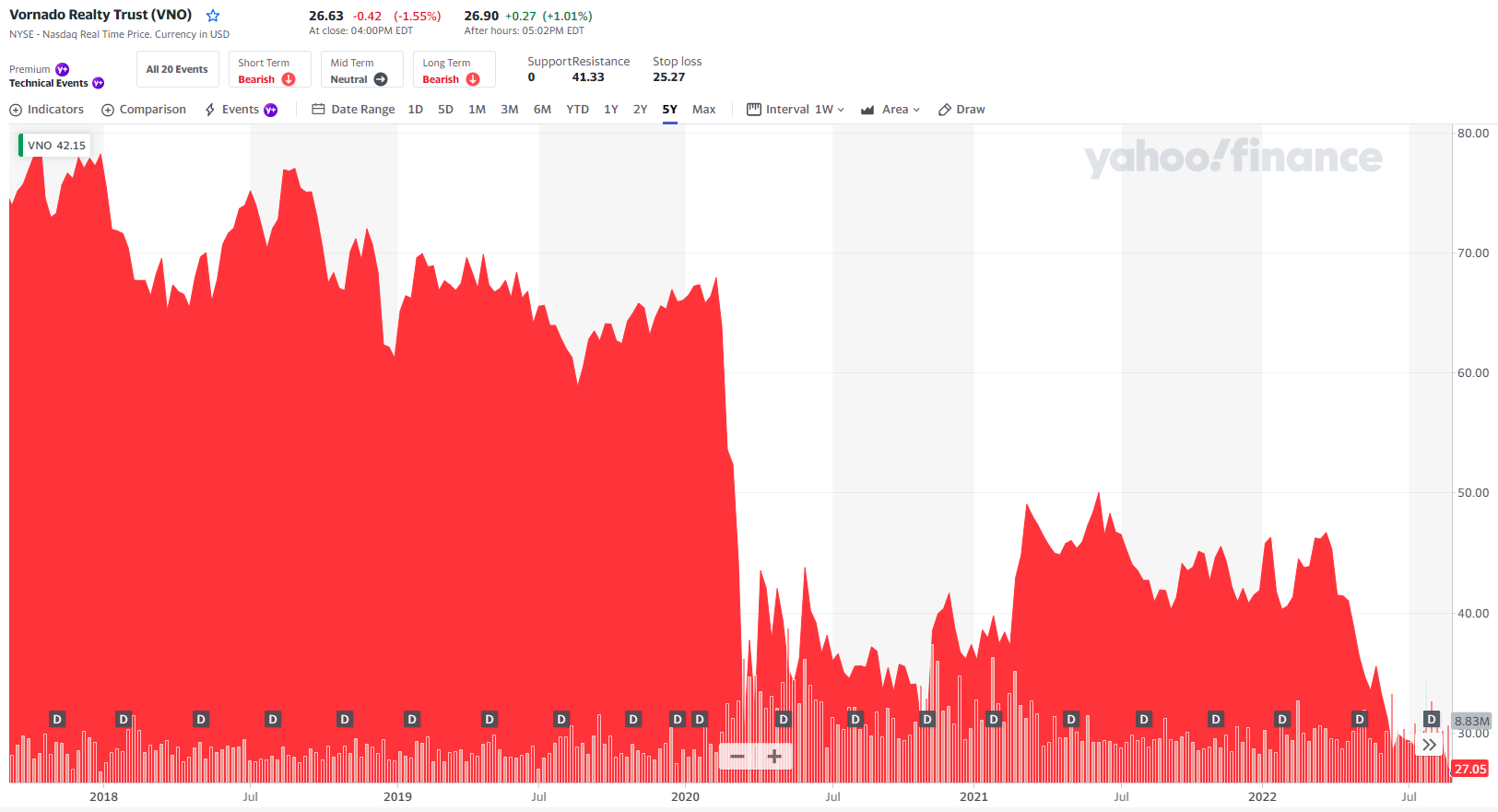

The share price action on Vornado since COVID-19 became serious has been insane . The company is literally down more than 60% since COVID-19 began - and this is despite some fairly good results from the company over time.

{kind=link}

This drop has been despite the facts that:

- The company has retained investment-grade credit at BBB-

- The company did not cut its dividend, and currently yields 7.59% , well-covered on an FFO/AFFO basis

- The company is expected to generate upside this year on an FFO basis

VNO may not be in a position to deliver massive amounts of growth - that is not what we are arguing here. We are arguing that the portfolio is good enough to continue to deliver decent returns here, even on the basis of just yield.

VNO IR

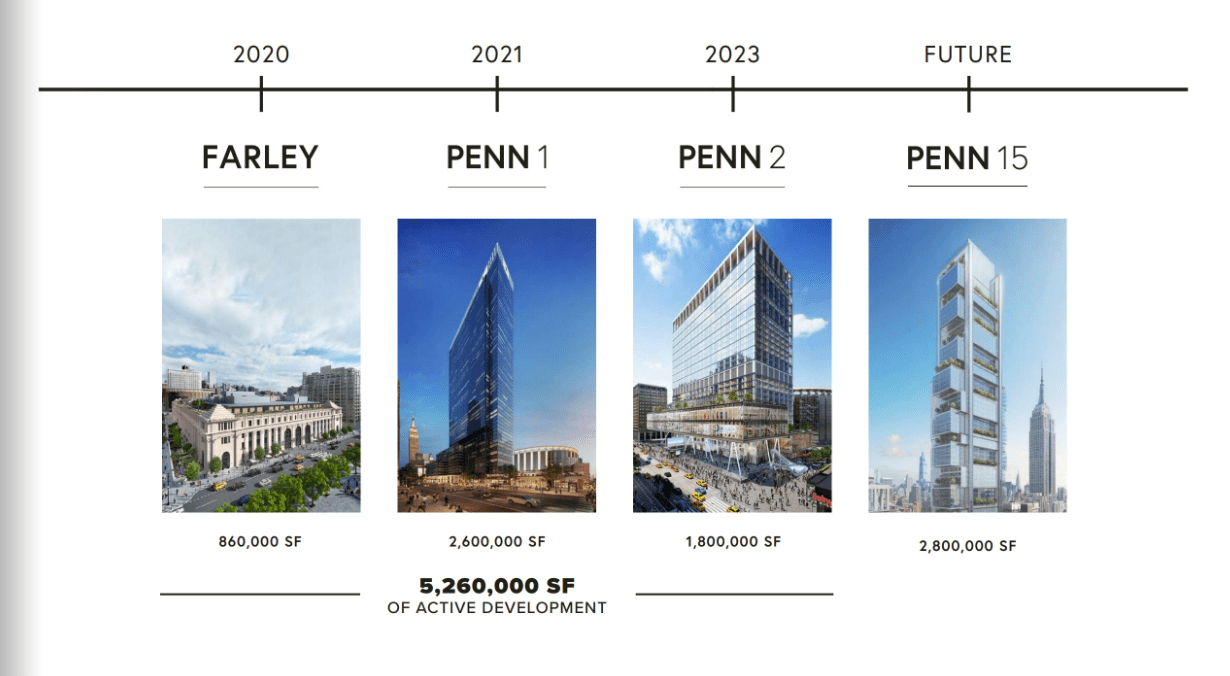

Among the most-priced assets the company owns is the Penn District geography that surrounds the New York Penn station. There are investors and analysts that believe that at the current valuation, the company's interests in these areas could even be spun off as a separate entity at a very attractive valuation.

{kind=link}

The recent earnings reported by the company came in significantly better than the market expected, with actual occupancy and leasing metrics completely on track. Yes, the company saw negative interest rate effects, and yes, the company did see some adversarial development from its overall exposure to variable-rate debt. But, aside from this, there were no new negatives to consider.

The shares bounced off this news initially but quickly lost steam.

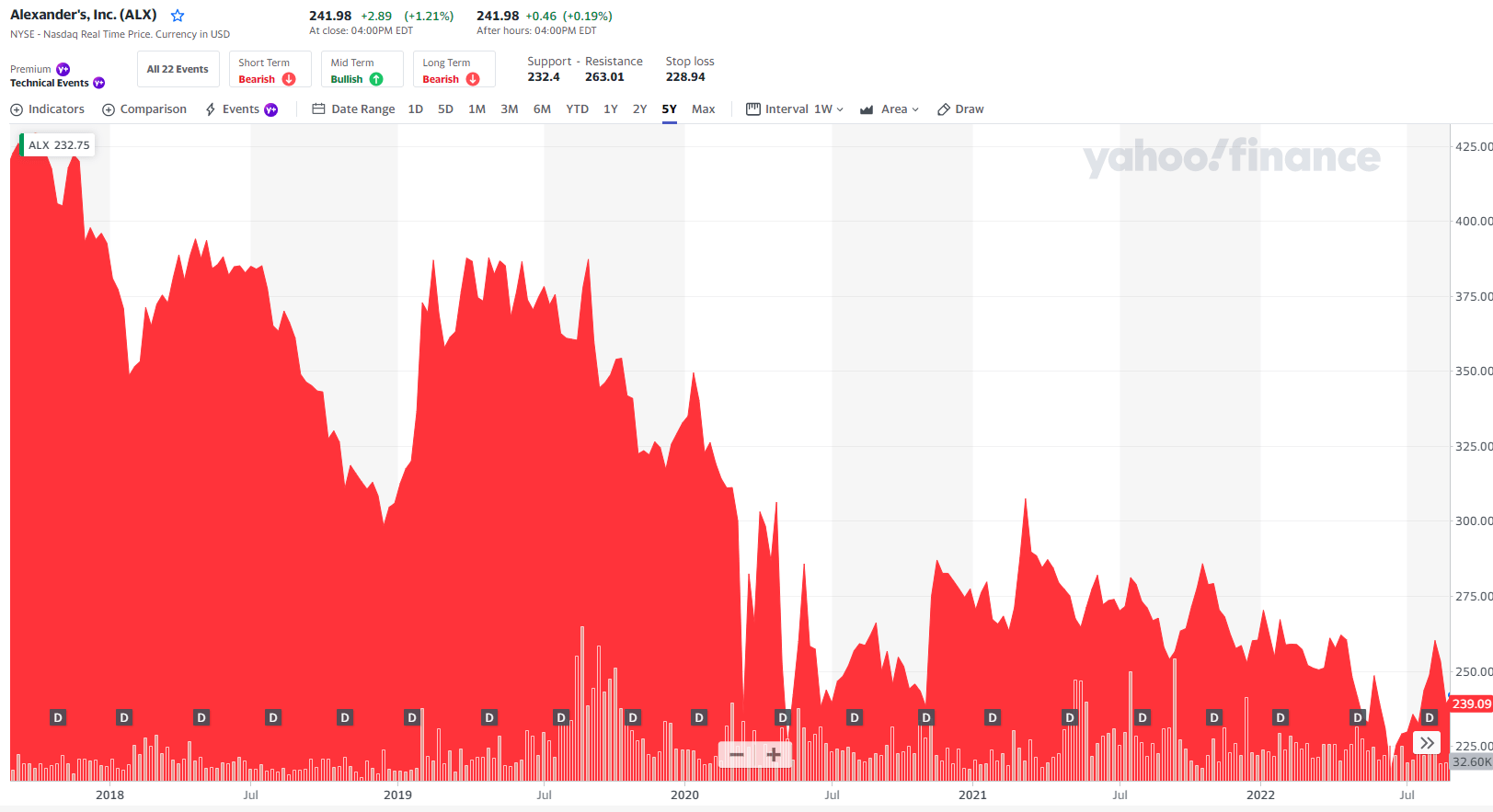

The company has a very close relationship with another player - Alexander's ( ALX ) - which was recently approached by activist investors to overhaul their business.

ALX in turn is 30% owned by VNO. These ideas of spin-offs and potential changes in VNO's portfolio are not pulled from the air, but from tangible actual relationships between these two businesses.

{kind=link}

Any deal made here if it included spinning off existing Penn assets would likely come to the advantage to current VNO shareholders given the value of Penn District assets and their valuation, it being the largest connected submarket in NYC and home to the busiest transportation hub in all of North America.

Such appeal does not come without attraction from developers and investors, and indeed, the company's focus on the Penn district is the talk of most analysts here.

The city (Economic Development Agency) even approved a fairly recent general plan for the district, which would turn the district into a new city centerpiece.

This is obviously a grossly oversimplified view, as the complexities in such a project or revitalization are massive where funding and the money is concerned for the infrastructure pieces of such a project.

We can conclude that any large portion in a Penn district revitalization is risky - hence also why we view the company as speculative. However, this in no way takes away anything that the company actually, currently has - namely some of the most attractive office assets in NYC.

While we can view the Penn assets as a potential catalyst for an upward direction, my focus is on the safety and dividend coverage of its legacy assets. FFO (funds from operations) for 2Q22 is up 22% YoY, and overall business development was solid - however, the company makes an allowance for the next quarter and 4Q22 to be lower than expected due to interest rate pressures and ongoing inflation, as well as ongoing non-cash charges for ground leases.

Still, much like analysts, VNO expects to be up YoY. The current situation for the Penn projects can be said to be "ongoing," with things carefully moving forward.

However, the argument I make for VNO is not based on its development projects - this is a massive bonus, but we can't really forecast how long it will take or what troubles it might encounter. As of right now, Penn is actually a bit of a drawback in terms of accounting that burdens the company's results with charges.

Instead, take a look at how the market is currently looking at the company, despite excellent trends in new leases in both office and retail - essentially ignoring the fact that the company is printing cash.

VNO Stock - Valuation, and Upside

Because this is the real argument when it comes to Vornado - you can buy quality at what is essentially dirt-valuation.

Vornado currently trades at a blended P/FFO of 9.2x . This is significantly below its historical range, with a 5-year average of around 15x. The Penn-plan volatility does justify some amount of discounting here - there's no doubt about that.

iREIT

But the degree of undervaluation here is not congruent with the actual risk of the legacy assets that the company has under its belt. FFO is not expected to materially decline for the coming years.

FAST Graphs

This sort of imbalance is what I typically look for when investing in real estate.

We're talking about an attractive REIT at below 10x P/E valuation, with a yield over 7.6% that's currently well-covered.

iREIT

Business areas are performing, in part at pre-pandemic levels. This recovery is what we are looking for when looking at companies like this. Company-wide same-store cash NOI is up nearly double-digits YoY, and the overall office business is actually up and positive here.

Occupancy for the portfolio is low. Lower in fact, than any other office REIT I've previously written about - especially in retail.

The NYC retail store occupancy is around 1% above 75% - but this is due to the company's projects, including Farleys. There are light points and upsides as well, showing increased leasing activity from the finance sector.

The same trends that dominate other office REITs are visible for Vornado - meaning that higher-quality buildings continue to show a premium here in terms of leasing activity. Older commodity products and spaces are showing significantly higher vacancies.

However, the company considers trends and demand to be strong. Vornado's management and team abilities have resulted in leasing 5M sq ft of Office space at WA leases of 12.4 years at impressive rates in 2022. The company managed 21 leasing transactions during 2Q22.

Again, the overall trends are not bad, yet the market is treating this company as though it was externally managed and poor overall quality.

Let's make this clear.

The conservative upside for Vornado here is no less than 22% in 3 years here - and that is expecting a lower 9x P/FFO than we have today. Let me repeat that - even if the company drops further, you'll still get 22% based on current forecast expectations, and this is at an FFO growth rate of 2.5%.

Any sort of reversal or normalization, which could come due to Penn, or leasing normalization (though most likely Penn), would result in an upside of no less than 91.17% in 3 years, or 31.5%+ annually based on a 15x P/FFO.

Now, it might be a bit too optimistic, expect an NYC office/retail REIT to get back up to 15x P/FFO in that timeframe given variable rate debt exposure and inflation, but it's a possibility if this turns out positive.

FAST Graphs

All in all, I believe the like RoR range for VNO for the next few years to be at least 20% over a period of 4 years , and likely higher than this. I understand why the company is viewed as speculative, and perhaps even a somewhat troubled investment.

However, at these levels, the upsides are compelling.

VNO already beat its cash retail guidance and raised its guidance for 2022. We continue to believe in outperformance based on continued additions from more retail, and the eventual additions from Penn assets, weighed up in the meantime (and in a dividend-coverage manner) by the company's legacy assets.

In the absolute upside scenario, we view the company as having a likely PT of above $40/share - but even in the case of a downside scenario, this REIT should still be worth at least $25/share.

S&P Global gives the company a range of exactly around that - $20/share on the low side and $45/share on the high side. The average PT is $32.5/share, giving the company a potential upside based on analyst expectations of 16.6%, with a current price/NAV of less than 0.5x. This share price target is down from a $45/share average in less than 6 months based on some of these mentioned risks.

This isn't a company for everyone . Vornado is a speculative "BUY" - but if you're willing to take on a bit of risk here, you have a high upside to look forward to, potentially.

Our positive PT for Vornado is $45/share - implying an upside of 38% here. Even if we're more positive on the company here, and consider it a spec buy, there's still a lot of quality to be had - and you can consider the lower PT as well.

Anyway you really slice it, this REIT has a lot of upside going forward, and at over 7% yield, VNO has a real potential of delivering inflation protection based solely on the basis of the dividend, which is well-covered.

Thesis

We like Vornado for a few reasons - but if you've read this far, then the reasons should become clear to you.

Even with the risks considered, we're now at a level where no matter what happens (within reason), VNO actually has a bit of an upside to offer. This might not be everyone's idea of a safe investment in the current situation - nor is it, really.

This is a "Speculative BUY" - and on the basis of current circumstances, the more risk-tolerant investor can make a good upside here.

Now, let me ask you, Vornado or Vornado?

For further details see:

You Say Vornado, I Say Vornado