AGESF - You Should Buy Ageas For Its 6.8% Dividend

Summary

- The company offers a 6.8% yield that is safe and growing.

- It gives investors exposure to high-growth Asian markets.

- The biggest headwind is nearly gone as the Fortis settlement for almost all claimants has closed.

- Ageas is a potential good buy right now while it is 12% undervalued.

- I have initiated a buy rating on Ageas here.

Editor's note: Seeking Alpha is proud to welcome Dividend Investing Mindset as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

The current downward trend in the stock price of Ageas (AGESY)(AGESF) presents a buying opportunity for the long-term dividend investor. The company is currently trading below its historical P/B ratio and has a current dividend yield that is above the five-year average yield. The Asian markets will provide the needed growth for years to come. The company's updated dividend policy combined with an improving Solvency II ratio makes me currently consider Ageas a buy.

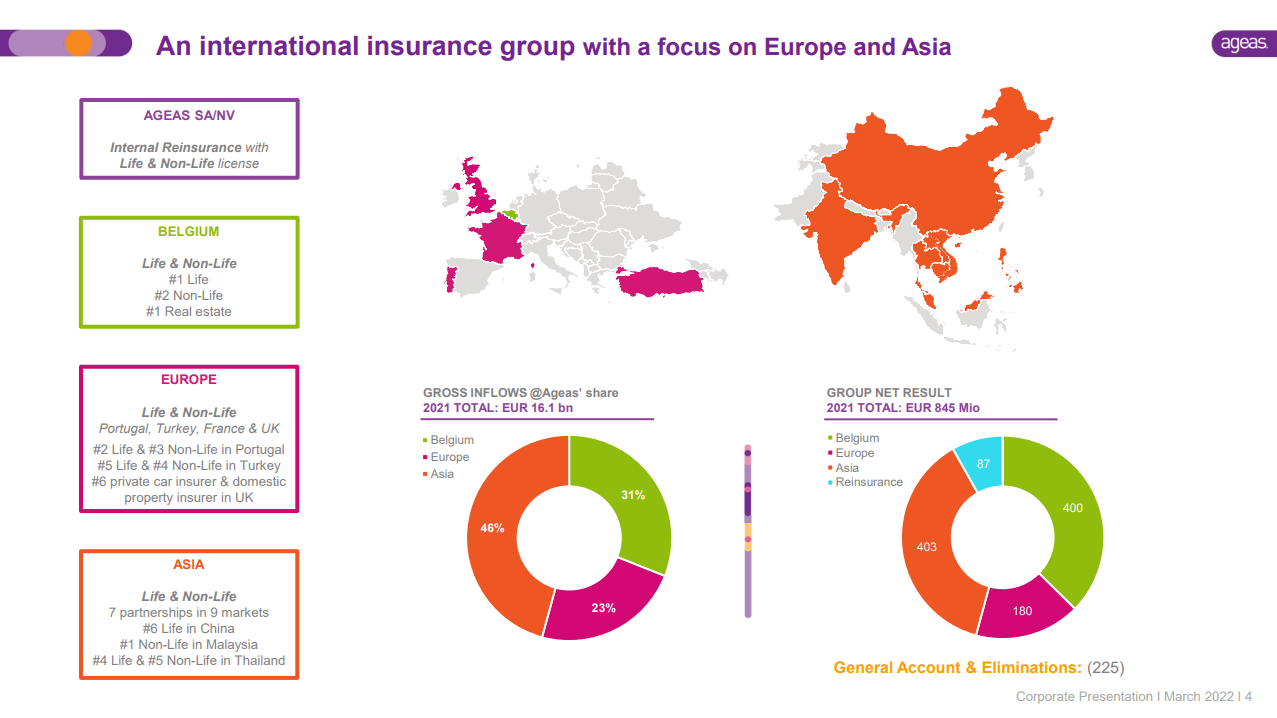

Company Overview

Ageas is Belgian insurance company. It is the market leader in Belgium and active in 14 other countries. The main focus is life insurance (~70%), but it also provides non-life insurance (~30%).

Here's a quick look at the company:

Group Overview (Company presentation)

{kind=link}

As you can see in the chart below, it has been a rather eventful couple of years for Ageas. Let me quickly explain what happened during this time period. The stock price more than halved during the COVID-19 crash. The stock price was able to slowly recover over the next 15 months as more and more investors gained back confidence. In July 2021, Belgium was hit by unprecedented floods, which put pressure on the stock price again as investors feared a heavy impact from the floods. It only took a couple of months before sentiment started to change as the risks of flooding were minimized by reinsurance. It didn't take long before negative sentiment from rising interest rates, the Russia-Ukraine war, and a possible recession put the stock price in a downward trend again.

Dividend Safety and Growth

The dividend policy that applies for most European insurance companies depends on the Solvency II ratio. In general, the higher the ratio the better. Ageas is currently targeting a Solvency II ratio of at least 175% in its "Impact24" strategic plan:

Under Solvency II, capital requirements are determined on the basis of a 99.5% value-at-risk measure over one year, meaning that enough capital must be held to cover the market-consistent losses that may occur over the next year with a confidence level of 99.5%, resulting from changes in market values of assets held by insurers.

For FY2021, the group's Solvency II ratio was 197%. And in the first half of 2022 the ratio improved to 221%. The group also presented an improved dividend policy, with a progressive dividend between 1.5B EUR and 1.8B EUR (cumulative).

A Solvency II ratio of 175% means Ageas is able to stick to its dividend policy. The dividend policy applies as long as the ratio is above 157%. Here's a look at the Solvency II ratio over time:

| Year |

| 2016 |

| 2017 |

| 2018 |

| 2019 |

| 2020 |

| 2021 |

| 2022 1H |

| Best case (1.8B EUR) |

| 2.75 EUR |

| 3.22 EUR |

| 3.76 EUR |

| 9.73 EUR |

| Avg Case (1.65B EUR) |

| 2.75 EUR |

| 2.98 EUR |

| 3.26 EUR |

| 8.99 EUR |

| Worst case (1.5B EUR) |

| 2.75 EUR |

| 2.75 EUR |

| 2.75 EUR |

| 8.25 EUR |

In the best case, investors can expect up to 17% dividend growth per year. In the average case, they can expect up to 8% dividend growth per year. In the worst case, the dividend would remain flat, but stable, as outlined in the dividend policy.

Given this information and Ageas' own prediction of EPS growth of 5%-7%, I believe investors can expect 6%-8% dividend growth until at least 2024. This is in line with the average case I presented in the above table.

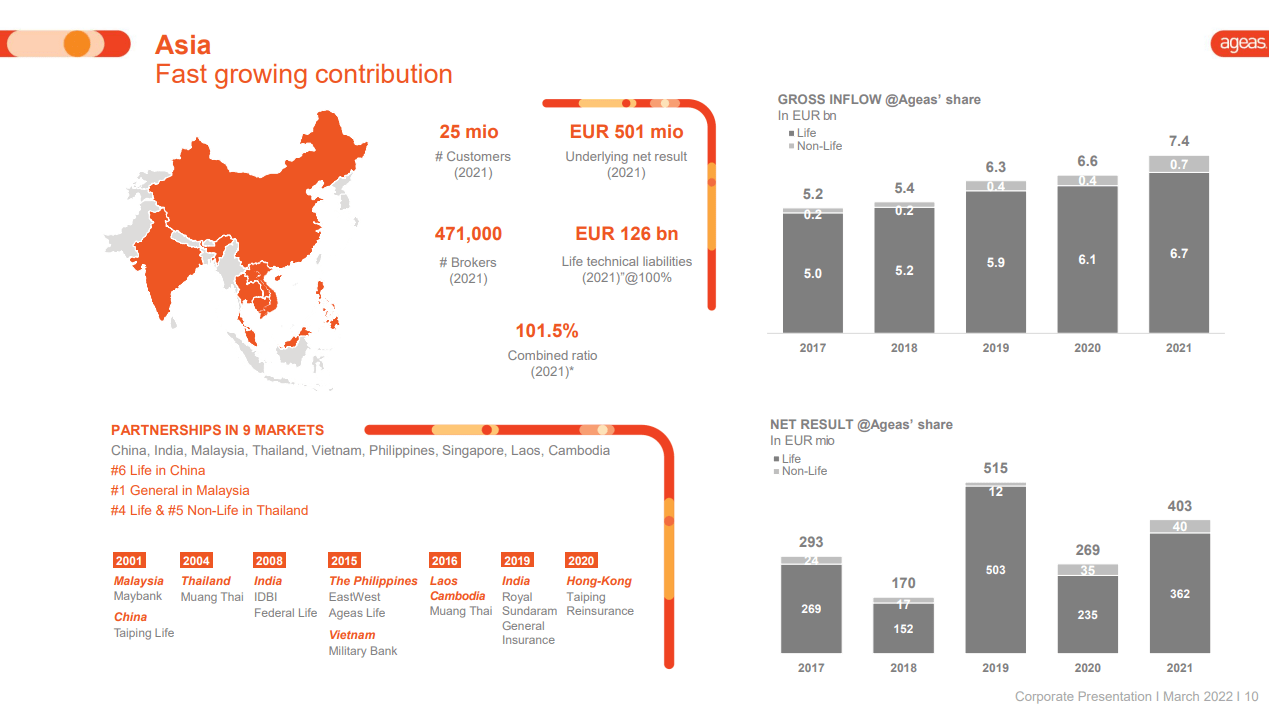

Growth

Let's take a closer look at where Ageas get its growth from. Ageas is active in both stable and high-growth markets. Europe falls into the stable and low-growth segment. On the other hand, Asia falls into the high growth but less stable/reliable segment. This is an advantage for the investor in Ageas. While they can expect stable and reliable returns from Europe, they can also expect growth from Asia.

Asian markets (Company Presentation)

{kind=link}

Ageas expects the Asian share of the net result to increase to ~50%. To fuel this growth in Asian markets, it is relying on its stable/core European markets. While the Asian markets are growing, Ageas is still looking to enter a new core European market. This will be done in order to maintain the balance between the stable and growth markets.

End of the Fortis Settlement

One of the biggest headwinds for Ageas has been the Fortis settlement, where they had to provide 1.3 billion EUR for claims from duped Fortis shareholders. The accelerated closing of the settlement allows Ageas to once again 100% focus on their insurance business.

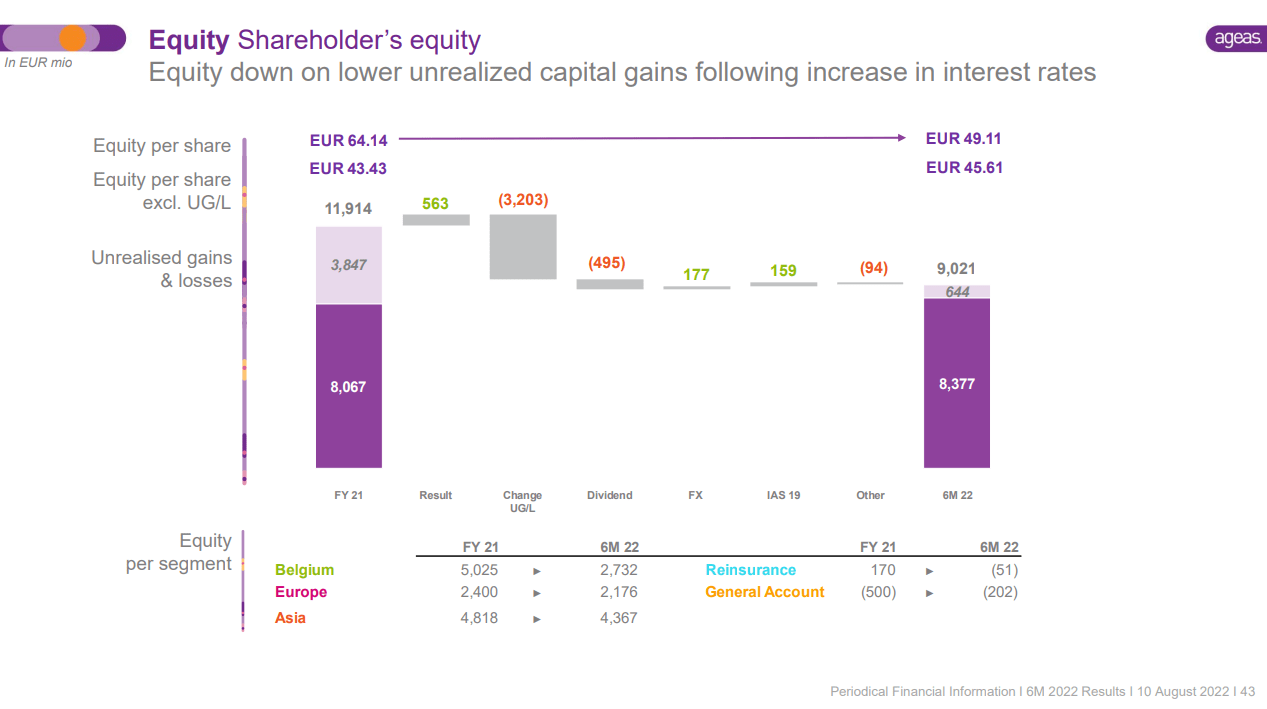

Rising Interest Rates

Rising interest rates are great for life insurers like Ageas as they will further boost earnings and solvency ratio. This in turn will help make the dividend policy better. However, this comes at the cost of lowering the value of the fixed-income portfolio.

As you can see below, the unrealized gains/losses took a big hit between FY 2021 and 6M 2022. But the good news here is that the equity per share excluding these did rise further.

Shareholders equity (Company presentation)

{kind=link}

Undervalued

I'll show you why I think Ageas is currently undervalued based on three different metrics. The metrics I will use are:

- tangible book value

- earnings

- dividend yield

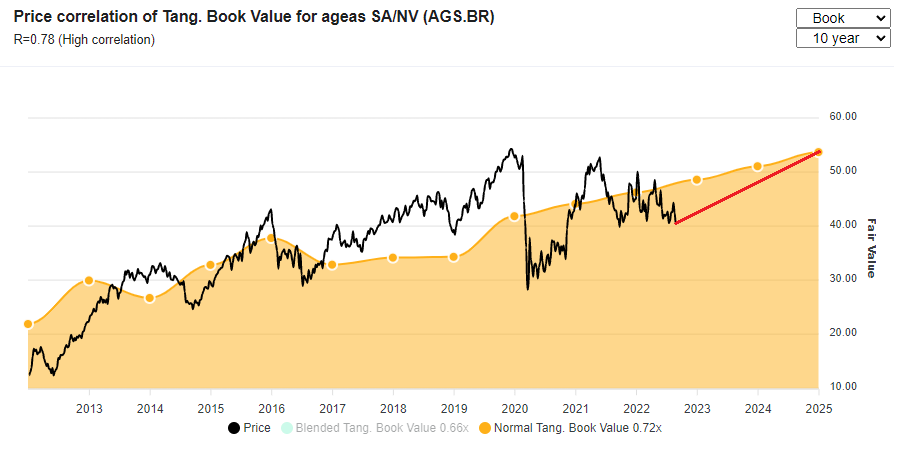

Tangible Book Value Multiple

Price correlation with tangible book value chart (Author's own software)

{kind=link}

Currently, Ageas is trading at a tangible book value multiple of 0.62x, while they normally traded at an average multiple of 0.72x over the last 10 years. This represents a discount of 12% to implied fair value. If the tangible book value keeps growing by the 10-year average growth of ~5.3%, this would imply a fair value stock price of 53.69 EUR by the beginning of 2025. If Ageas reverts back to its fair value by 2025, this would imply a capital gain of 13.29 EUR/share or a CAGR 12.84% (excluding dividends).

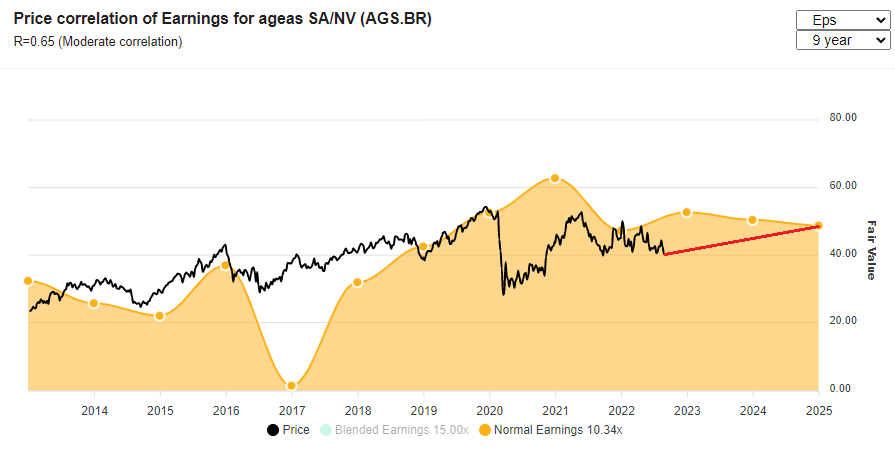

Price-Earnings Multiple

Price correlation with earnings chart (Author's own software)

{kind=link}

Currently, Ageas is trading at a P/E multiple of 8.84x. It normally traded at an average multiple of 10.34x over the last nine years. If the EPS keeps growing by the nine-year average growth of ~4.13%, this would imply a fair value stock price of 48.74 EUR by the beginning of 2025. If Ageas reverts back to its fair value by 2025, this would imply a capital gain of 8.34 EUR/share or a CAGR 8.30% (excluding dividends).

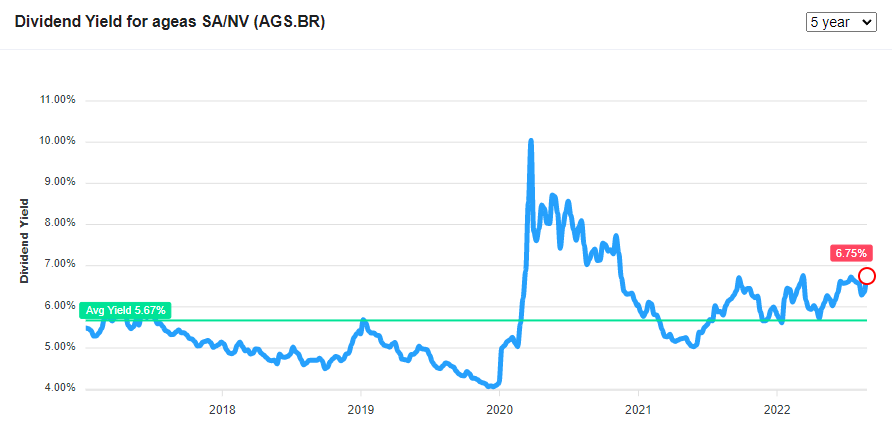

Dividend Yield

The current dividend yield of Ageas is ~19% above its five-year average. According to the Dividend Yield Theory , dividend yields tend to revert back to the mean. I will now calculate what the current share price would be if Ageas does indeed revert back to the five-year mean.

Calculation: 2.75 EUR / 5.67% = 48.50 EUR

This would imply a fair value share price of 48.50 EUR.

5-year dividend yield chart (Author's own software)

{kind=link}

Dividend Discount Model

For the DDM, I used the following inputs:

- dividend growth of 4%/year

- terminal dividend yield of 5.67%

- margin of safety of 10%

Putting these numbers in the DDM calculator gets you a buying price of 43.97 EUR. After applying a 10% margin of safety, the current suggested buying price for Ageas is 39.97 EUR. This is slightly below the current share price of 40.40 EUR.

Dividend discount model (Author's own software)

Internal Rate of Return

I also calculated the IRR of an investment in Ageas for the next 10 years. In order to get my exit share price, I projected out the EPS, dividend and tangible book value over 10 years at their current growth rate. I gave all of these future share prices an equal weighting.

2031 projected share price based on earnings, dividend and book value (Author's own software)

For the IRR calculation I will assume an exit price of €77.11 in 10 years, and an initial investment price of €40.40. For the cash flow, I used a dividend that grows at 4%/year. The result of the IRR calculation is 14.91%. This is above what I would expect for Ageas given its current risk/reward proposition.

IRR Calculation (Author's own software)

This also happens to be above the expected IRR for its closest peers.

| Company |

| IRR |

| Ageas |

| 14.91% |

| NN Group ( NNGRY ) |

| 12.52% |

| Legal & General ( LGGNY ) |

| 13.29% |

| Allianz ( ALIZY ) |

| 12.61% |

If you read this article in the future, here is the IRR at different initial investment prices:

Distribution table of IRR (Author's own software)

Risks

Despite all of this, there are some risks to consider. Low liquidity could be an issue when trying to buy/sell the shares. The company has a rather low trading volume; on Euronext Brussels, the average trading volume is only ~300k shares per day. And the over-the-counter shares only have an average trading volume of ~16k.

Rising interest rates are expected to further decrease the value of Ageas' fixed income portfolio. The Fortis settlement has been closed for almost all claimants (290k), and there are fewer than 80 files pending. But these could still pose a risk.

External disasters like the recent floods in Belgium are becoming more and more common, so these could have a significant impact on the business as well. The main growth driver of Ageas is heavily exposed to emerging markets (China, Singapore, and Thailand); because of this, Ageas is exposed to the political, economic, and currency risks of these countries.

Conclusion

Dividend investors should take a look at Ageas while it is undervalued. Please keep in mind that Ageas is based in Belgium, where the standard dividend withholding tax rate is 30%.

With an IRR of 14.91% and a suggested buying price slightly below 40 EUR based on the DDM calculation, I consider Ageas to be undervalued currently. The current share price of 40.40 EUR is also well below the net equity per share (excluding unrealized gains and losses) of 45.61 EUR.

The company's three-year strategic plan favors income investors as it will boost its dividend even further in favor of share buybacks. The Solvency II ratio is improving and well above the minimum level needed to support the dividend policy. The dividend is safe and well covered by upstream cash from subsidiaries.

Rising interest rates is great for life insurers like Ageas. They will further boost earnings and solvency, but at the cost of lowering the value of the fixed-income portfolio.

Expanding into a new, stable market could provide the group with more diversification and another source of stable earnings and dividends. This in turn will strengthen the dividend even more. There's also continued growth from Asian markets, as they are expected to become ~50% of the group's net result.

Given all of this, I am initiating a buy rating on Ageas and plan on adding to my position below 40 EUR.

For further details see:

You Should Buy Ageas For Its 6.8% Dividend