CMCSA - Your New Year's Resolution For 2023: Invest $10000 In These 10 Stocks

Summary

- In this article, I review the stocks of ten world-class companies that I either have in my portfolio or am in the process of building a position in.

- I point out the specifics of the companies' business models, discuss their profitability and balance sheet quality, and evaluate their dividend growth record and future prospects.

- In addition, I review a hypothetical example of an investor starting his investment journey in 2023.

- I compare several scenarios that illustrate the importance of a high savings rate and why I believe owning a range of current high-yield stocks alongside lower-yielding stocks with higher growth rates is the optimal strategy.

Introduction

As the year draws to a close, I like to sit back for a moment, review the year, and think about New Year's resolutions, including my investment goals. Since government-sponsored plans are, in my opinion, an increasingly risky bet on a prosperous retirement, I think it is extremely important to set up an alternative plan. For myself, I have chosen a dividend growth strategy, as I outlined in an article in March of 2022 . For all the benefits this strategy brings, it requires commitment and a long-term mindset. Dividend growth investing is not a get-rich-quick strategy. Therefore, I think it is worth making a New Year's resolution to help maintain that mindset.

In what follows, I briefly review the stocks of ten world-class companies that I either have in my portfolio or am in the process of building a position in. I point out the specifics of these companies' business models, discuss their profitability and balance sheet quality, but most importantly, I evaluate their dividend growth record and future prospects. In the last section of this article, I review a hypothetical example of an investor starting his investment journey in 2023. I compare several scenarios that illustrate the importance of a high savings rate and why I believe owning a range of current high-yield stocks alongside lower-yielding stocks with higher growth rates is the optimal strategy.

The Procter & Gamble Company ( PG )

I first covered Procter & Gamble in a comparative analysis with European competitor Unilever ( UL ) in October 2022. PG is one of my core holdings as it meets several criteria that I consider important for a solid long-term investment. The company owns a number of leading brands and sells everyday items with low-dollar price tags. It is diversified globally, so it combines growth opportunities in higher-risk emerging markets with reliable returns in developed markets. It is a less aggressive bet on emerging market growth than, say, Colgate Palmolive ( CL ) or Unilever.

Much has improved at P&G since activist investor Nelson Peltz became involved in 2017. The company is now generating strong growth in free cash flow ((FCF)) and excess return on invested capital ((ROIC)) in the high single digits, meaning it is generating value for shareholders above its estimated cost of capital. P&G's balance sheet is pristine, with a current interest coverage ratio of approximately 30 times FCF, normalized for working capital movements and stock-based compensation. If P&G hypothetically suspended its dividend and share repurchases, it could repay all of its outstanding debt with just over two years of FCF. Because of the robustness and reliability of its earnings and cash flows, P&G can operate with negative working capital. Companies with consistently negative working capital, asset-lean business models, and reliable earnings typically outperform the broader market - I consider the "new" (i.e., post-2018) P&G to be one such example, joining the ranks of other world-class companies such as The Coca-Cola Company ( KO ) and PepsiCo ( PEP ), as I discussed in my detailed analysis from mid-November.

P&G has proven resilient during the pandemic and has also taken the current high inflation in stride. As a result, P&G is - unsurprisingly - anything but cheap at $150. I added to my position when the stock plunged along with the broader market in October, but the current price tag is not really inspiring as it translates to a price-to-earnings (P/E) ratio of about 26, a current FCF yield of less than 4%, and an enterprise value (EV) to EBTIDA ratio of 20. P&G is also expensive relative to historical multiples. From a dividend investor's perspective, the current yield of 2.4% does not compare favorably to the five-year average of 2.6%.

However, as an income-oriented investor, I appreciate management's shareholder-friendly stance, which is underscored by long-term average dividend growth of 6% to 7% per year and regular share repurchases that significantly outpace dilution from exercised stock awards. For example, over the past nine years, the company has reduced the number of shares outstanding by 14% (net of new shares issued), boosting earnings and cash flow per share by 16%.

Looking ahead to 2023, I want to increase my position in P&G while acknowledging the company's high valuation, so I've come up with a compromise. I am willing to add to my position at $120 or less, which translates to a P/E ratio of 20 and an FCF yield of nearly 5%, but in the event the stock does not fall to that level, I plan to increase my position by 5% in the fourth quarter of 2023, regardless of the price level. I have adopted such a strategy for world-class companies that rarely go on sale. In 2022, I was fortunate to be able to take advantage of the opportunity in October, so I do not plan to buy any more shares this year.

Visa Inc. ( V )

I only started a position in payments technology company Visa this year because I always found it too expensive. Therefore, I believe the stock serves as an interesting case study as part of a New Year's resolution to "force myself" to invest a fixed amount of money in ten companies.

Visa operates a transaction processing network for purposes such as authorization, clearing and settlement. The company is probably best known for its credit, prepaid and debit cards. Despite being a long-established leader in a mature industry, the company can still grow at staggering rates. Of course, the payments industry is evolving rapidly, but I think Visa, like Mastercard ( MA ), has proven its ability to adapt and evolve. With the proliferation of digital payments, which Visa is leading the way in, I think it is a pretty safe bet.

I particularly value the network effect and asset-lean business model of these major payment service providers. It is therefore hardly surprising that Visa's operating and normalized FCF margins are very high, at around 66% and 46%, respectively. The asset-lean business model is also the main reason for the mouth-watering excess ROIC in the 20%+ range, which gives the company a significant advantage over smaller competitors. At the same time, the company is able to operate without much leverage - Visa could pay off all of its debt in less than two years if it suspended its dividend and share buybacks. Speaking of which, Visa bought back 19% of its outstanding shares over the last nine years, boosting earnings per share by 23%. Given that Visa stock is rarely cheap, the return on investment probably was not the best, but the reduced number of shares outstanding certainly helped keep dividend cost in check, increasing the room for future dividend increases. Visa's current yield of 0.9% is uninspiring for an income-oriented investor, but I think it is incorrect to view Visa as a dividend stock. Nevertheless, if the company maintains its current long-term dividend growth rate of 18% per year, investors who buy Visa today would see a 2% yield on cost after just four years and more than 6% after 11 years.

Mr. Market has clearly understood that Visa is a world-class company and is valuing it accordingly. With a P/E of nearly 30, an FCF yield of 3.1%, and an EV/EBITDA multiple of 22, the stock is anything but cheap. However, when comparing this data to average multiples over the past five years, the stock appears reasonably valued, although it is important to remember that these valuations are the result of an extremely strong bull market. My position in Visa is still very small, so I will be a little more aggressive in 2023 than what I plan for P&G, in part because I think Visa's growth prospects are much better. I am comfortable buying at a price of about $180, which represents a 20% discount to investor services firm Morningstar's fair value estimate. However, I still consider Visa a reasonably solid buy at $200. Since my position is still very small (0.2% of my portfolio), I will at least triple my position in 2023. If the stock falls to $180 or less, I expect to increase my position to 1.0% of the total portfolio value.

Bristol-Myers Squibb Company ( BMY )

At a late stage in the business cycle, stocks of major pharmaceutical and biotechnology companies tend to perform quite well. I started looking into Bristol Myers Squibb, which I believe has similarities to AbbVie ( ABBV ), in the fourth quarter of 2021 and began building a position at that time. I have published several analyses of the company in the past, most recently comparing it to Gilead Sciences ( GILD ).

The company made a bold move in 2019 when it acquired Celgene to bolster its current portfolio and drug pipeline. Fast-forward three years, the debt-laden acquisition has gone quite well and Bristol has evolved into a reliable cash flow machine with a management team that delivers on its commitments. With operating and FCF margins of over 60% and over 40%, respectively, BMY's profitability is very solid indeed, and the company has delivered excellent excess ROIC of over 15% in recent years, which is a great performance given the bold acquisition. Debt levels are well under control thanks to strong free cash flow and a manageable maturity profile (Figure 1 in my first article on the company).

Sales of Revlimid, a cancer drug about to lose exclusivity ((LOE)), are declining as expected, but are still strong. Other key cash flow generators include Eliquis, an anticoagulant that BMY co-markets with Pfizer ( PFE ), and Opdivo, a novel checkpoint inhibitor for the treatment of various cancers. The company has a robust pipeline and should be able to more than offset declining sales due to LOEs, but of course faces strong competition, such as from Merck ( MRK ) with its blockbuster cancer therapy Keytruda. Recognizing that patent cliffs are a natural phenomenon and that big wins are far from always guaranteed, I own a broad range of Big Pharma companies. I make sure to build my positions at compelling valuations, so I consider myself fortunate to have started buying BMY in late 2021 when the company was trading in the sub-$60 range.

However, I do not think the stock is overvalued even at the current level of over $70. The current starting dividend yield of 3.2% is not particularly high for a mature pharmaceutical company, but I consider it acceptable compared to its five-year average yield of 3.0%. At an 8% cost of equity, Bristol Myers would only need to maintain its current free cash flow to justify the stock's valuation. With a price-to-earnings ratio below 10 and an FCF yield above 8%, the stock may not be your typical deep-value pick, but that is to be expected given the much-reduced uncertainty since 2019.

My position currently accounts for about 1% of my portfolio value, and I am gradually adding to it during times of weakness to bring it up to about 1.2% to 1.5%. An important factor in my investment thesis in BMY is the fact that since the acquisition of Celgene - a company that did not pay a dividend itself - management has placed a higher priority on dividends. BMY's three-year CAGR of 8% is pretty solid, in my opinion, and there is plenty of room for growth given the payout ratio of less than 40% of normalized free cash flow.

Altria Group, Inc. ( MO )

Altria does not need much introduction, as it is the major U.S pure play tobacco company. I have written about the company several times in the past - first in 2018 when I compared it to the other Big Tobacco companies. It may be hard to believe, but tobacco stocks were quite overvalued between 2014 and 2017, but the FDA's 2017 announcement of a possible ban on menthol cigarettes gradually brought valuations back in line with reality. Altria's focus on the U.S. market since its spinoff of Philip Morris International ( PM ) in 2008 and missteps by management as the company attempted to diversify its operations away from the combustibles business (e.g., through investments in JUUL and Cronos Group ) further pressured the stock price.

As a result, the quality of Altria's balance sheet has suffered, but it can be argued that because of strong free cash flow, the increased debt burden is not a problem (see my recent discussion of Altria's maturity profile). Its operating and FCF margin are currently 67% and 40%, respectively. Given the company's low capital intensity - Altria typically spends between $200 million and $300 million on capital expenditures and generates about $8 billion in FCF - the company's excess ROIC is also extremely solid at about 20%.

While I am very optimistic about the company's profitability and manageable debt level, I am also aware of the risks associated with investing in the tobacco sector, especially when it comes to a US-only company like Altria. Finally, it is important to remember that the company's core product is in decline and Altria must compensate for declining volumes by regularly raising prices. I own quite a few tobacco stocks in my portfolio, and my position in Altria currently represents about 2% of my total portfolio value. As a result, I only add to my position on rare occasions, but the current valuation (P/E below 10, FCF yield above 9%, EV/EBITDA multiple of 9) is really compelling. As an income investor, the high yield of currently 8.2% is another plus, but overly generous dividend increases as in the past (8% to 9% CAGR) should not be expected given the continued decline in cigarette volumes, likely increasingly higher taxes and other headwinds.

PepsiCo, Inc.

PepsiCo, the owner of world-class brands such as Pepsi-Cola, Gatorade, Tropicana, SodaStream, Mountain Dew, Lays, Doritos, Cheetos and Quaker, defied the bear market in 2022 with flying colors. The company has great pricing power and continues to post solid growth in what certainly are far from easy times.

A gross margin of 50% or more is certainly very solid for a consumer staples company. Given PepsiCo's relatively solid operating margin of around 16% and moderate asset base, its return on invested capital is typically much higher than its weighted average cost of capital. However, due to relatively weak cash flow conversion, PepsiCo's CROIC is only slightly higher than the Capital Asset Pricing Model ((CAPM)) derived cost of equity. PepsiCo's business model differs significantly from that of its competitor, The Coca-Cola Company (see my recent comparative analysis ), but both companies generally operate with negative working capital, which is one reason for what is in principle very solid profitability (see above).

What bothers me most about PepsiCo is its debt. In addition to acquisitions, the company regularly engages in share buybacks. Over the past nine years, it has reduced its shares outstanding by about 12% (net of stock options exercised), which has certainly helped earnings per share growth. If PepsiCo were to suspend its dividend and stock buybacks, it would take more than six years to pay off all of its debt. Of course, a company of PepsiCo's caliber can certainly handle that kind of debt, but I still think it is important to keep an eye on the balance sheet, in part because cash flow profitability is relatively weak.

While this may sound overly negative, I still think PepsiCo is in principle a great company because of its world-class brands. I have a relatively modest position of PEP in the portfolio, which I plan to grow over time. However, as a value investor, the current high valuation keeps me from adding to my position. With a P/E ratio of over 26, an EV/EBITDA multiple of 18, and an FCF yield of only 2.5%, I find it really hard to buy shares of the company. Finally, the stock seems overvalued even from a dividend yield perspective (currently 2.5%). Therefore, I follow the same strategy as with Procter & Gamble. I am forcing myself to add at least 5% to my position in the fourth quarter of 2023 if an opportunity ($140, P/E of 20, FCF yield of 3%+) does not present itself sooner.

T. Rowe Price Group, Inc. ( TROW )

T. Rowe Price runs a wonderfully asset-lean business. It is an active fund manager with more than $1.4 trillion in assets under management, with diversified operations around the world but, of course, a focus on the United States. I have covered the company several times in the past, and just recently compared its performance since the COVID 19 pandemic with that of its competitor Franklin Resources ( BEN ). As a result of the 2022 bear market (asset managers are basically a leveraged long bet on the stock market), shares have lost more than 50% of their value since the exuberant all-time high in late 2021. In addition, the valuations of active managers like TROW and BEN are being hurt by the secular trend toward passive investing. While their stocks certainly deserve a valuation discount due to this aspect, I still believe they are not obsolete business models. In particular, I appreciate TROW's emphasis on retirement products, but at the same time, the company is suffering from withdrawals due to increasing baby boomers' retirements.

All in all, I think TROW is nevertheless well positioned and has handled difficult situations in the past with flying colors. For example, the company increased its dividend during the Great Financial Crisis, and its current payout ratio is still well below 50% of free cash flow. Partly due to its asset-lean business model (operating and FCF margins of around 40%, excess ROIC of around 10%), it has no financial debt on its balance sheet. Therefore, the company has a lot of capacity to diversify into asset classes with typically better retention of client funds such as alternative investments through acquisitions. For example, TROW acquired Oak Hill Advisors in late 2021.

TROW is one of the smaller positions in my portfolio due to the uncertainties associated with its business model. It currently makes up less than 1% of my portfolio value, and I currently only add small amounts because I do not really want the position to get much larger than 1%. That said, I think the current valuation is compelling (P/E of 14, EV/EBITDA of 9, FCF yield of 10%). With a dividend yield of 4.4% and a long-term average dividend growth rate of 15%, the company certainly qualifies as a dividend growth stock. Nevertheless, somewhat slower dividend growth should be expected in the future due to the undeniable challenges.

The Home Depot, Inc. ( HD )

The pandemic has been a major tailwind for home improvement giant Home Depot. Moreover, the company's excellent management has so far handled the ensuing supply chain challenges and inflationary pressures very well. If there is anything to criticize, it is the fact that management appears to be committed to share buybacks regardless of stock valuation. HD's balance sheet quality has suffered, but debt is still quite manageable (see my recent analysis ). HD's weighted average interest rate was about 3.4% at the end of fiscal 2021, and the company would need about four years (assuming stable free cash flow) to pay off all of its outstanding debt if it suspended share buybacks and dividends.

I am not usually a big fan of middle man's businesses, but HD is an exception to the rule because of its prime position alongside Lowe's ( LOW ) and solid profitability. Operating and free cash flow margins of 15% and 10%, respectively, confirm the company's excellent position. Excess ROIC is also very high at around 20%, confirming HD's wide economic moat. The company's management is extremely shareholder-friendly and has increased the dividend at a CAGR of 19% over the past nine years. Dividend growth has slowed in recent years, but is still very solid at over 10% (three-year average). Share repurchases reduced the number of diluted shares outstanding by an astounding 30% over the last nine years, boosting earnings per share by over 40%.

I recognize that a recession will hurt the company's earnings, and its current valuation (P/E of 19, EV/EBTIDA multiple of 15, FCF yield of 4%) is still somewhat high for a retailer. As a result, my position in HD is still very modest at only about 0.8% of portfolio value. Since I am a big fan of HD's business in general and management in particular, I would like to increase my position in 2023. I feel comfortable buying HD at around $270, so I am taking the same approach I did with PepsiCo and Procter & Gamble. If the stock drops to $270 or below, I will increase my position to 1%. Otherwise, I will increase my position by at least 5% during 2023, regardless of the stock's valuation.

Raytheon Technologies Corporation ( RTX )

I first covered diversified defense and aerospace company Raytheon Technologies in early October 2022. I compared the company, which was only formed in 2020 from a merger of Raytheon Company and United Technologies, to Lockheed Martin ( LMT ) and explained why I have both companies in my own portfolio. I view LMT as a largely non-cyclical bet on the U.S. defense budget (and probably most of the Western world), while I view RTX as a more cyclical aerospace company that is benefiting from a resurgence in air travel but has the added diversification of a defense contractor. I particularly appreciate RTX's focus on service-related revenues and its top-tier position through Pratt & Whitney, which manufactures world-leading aircraft engines used in Lockheed's F-35 fighter jet and the Airbus A320neo, for example (GTF Advantage).

Since my article, RTX's stock price is up about 17%, which is a pity considering I am still in the process of building my position. I think the stock is a solid buy in the low- to mid-$80s, so it is understandable that I am not a fan of the price increase, in part because nothing has fundamentally changed for the company. Of course, Raytheon is benefiting greatly from the war in Ukraine, but I think the expected increase in sales of the Patriot missile defense system and F-35 engines is already priced into the stock and investors are increasingly disregarding a potential negative impact from an impending recession and the ongoing supply chain issues.

Profitability-wise, Raytheon Technologies is still somewhat enigmatic. I believe that the merger with United Technology and the subsequent spin-off of Otis Worldwide ( OTIS ) and Carrier Global ( CARR ) have helped the company focus, which should obviously benefit profitability in the long run. Raytheon is not really a positive example from a debt standpoint either (current notional debt repayment period of six years and interest coverage of six times FCF before interest), but the now dampened volatility of cash flows due to its diversification as a defense contractor make the situation rather unproblematic.

My position in RTX represents about 0.6% of my portfolio value, and I would like to increase it to at least 0.7% in 2023, or 1.0% if valuation move a bit more in line with fundamentals.

Comcast Corporation ( CMCSA )

CMCSA is a global media and technology company with three main businesses: Comcast Cable, NBCUniversal and Sky. The company is well diversified, but the cable business is the cash cow and at the same time the main reason for the company's attractive valuation. Growth expectations are rather muted, which is understandable due to increasing competition and "cord cutting," but I think this phenomenon is currently overrated by market participants. Of course, the company offers a largely commoditized product, but it operates in a consolidated industry with high barriers to entry. The capital-intensive nature of Comcast's business can be viewed as both a positive and a negative.

Comcast's business is surprisingly profitable - given its high capital intensity - with operating and free cash flow margins of around 20% and 10%, respectively. Of course, the substantial asset base and goodwill due to the acquisitions of NBCUniversal in 2011 and 2013 and Sky in 2018 result in a rather weak excess ROIC, and a cash return on invested capital that is often even below the CAPM-derived cost of equity. The company's debt pile is huge, but manageable given its reliable cash flows with a notional repayment period of seven to eight years. Its maturity profile is very comfortable, with an average maturity of around 18 years, so Comcast will not suffer from near-term debt service challenges.

Comcast, in particular due to fear of accelerating cord-cutting, is rather cheap. Of course, these fears are not unfounded, and continued inflation could exacerbate the trend. However, with a P/E ratio of under 10, an EV/EBITDA multiple of 7.5, and a free cash flow yield of 7% to 8%, I think the risks are well-reflected in the valuation. With a dividend yield of 3.1%, the stock is a welcome income generator in a market that I think could move sideways for an extended period. Comcast's management is shareholder-friendly and has increased the dividend at a CAGR of 12% over the past nine years. Growth has slowed in recent years, but still significantly outpaces also current higher inflation rates. Because of the risks, I do not want my position in CMCSA to exceed 1% of portfolio value. Therefore, I am only adding on weaknesses, with the intention to fill the remaining 0.25% over the course of 2023.

Microsoft Corporation ( MSFT )

As a value investor, I focus on companies with strong current cash flows and avoid stocks with valuations that are largely the product of expected future growth. Microsoft has benefited greatly from the pandemic and the trend toward remote work. The company puts a lot of emphasis on service-related revenue, stabilizing its cash flows. The ecosystem built over the years has resulted in world-class profitability. Operating margin and normalized free cash flow margin are approximately 40% and 25%, respectively, and due to the asset-lean business model, excess ROIC is extremely high at over 30%, confirming the wide economic moat. Similar to other technology companies, Microsoft's leverage is not really worth mentioning, and the company should actually benefit from rising interest rates thanks to its solid cash position.

Evidently, a company like Microsoft belongs to a diversified portfolio. However, it should not necessarily be seen as a dividend stock, as the starting yield is rather low, currently only 1.1%. Like Visa, I see Microsoft as a "growth engine" in my portfolio. Given its low payout ratio and exceptional profitability, a continuation of long-term dividend growth of around 10% per year seems a reasonable assumption, which translates into a yield on cost of 2.6% after ten years and over 4% after 15 years.

Due to the significant overvaluation in 2021, I have refrained from opening a position so far. Now that technology stocks have let off considerable steam, I think Microsoft is at least worth considering. However, with a P/E of 25, an EV/EBITDA multiple of 18, and an FCF yield of less than 3%, the stock is far from cheap. Moreover, I would be very cautious not to extrapolate current earnings growth into the future, as I explained in my recent analysis of Alphabet's ( GOOG , GOOGL ) cash flow. However, comparing Microsoft's valuation to that of mature staples companies like Procter & Gamble and PepsiCo (see above), things do not look so bad. Microsoft's growth prospects remain solid, and the undeniable network effect in its business makes it a reasonable investment at its current valuation, so I believe. I do not own any shares of the company yet, but plan to open a position very soon.

A Look At The Past And A Few Thoughts About The Future Of This Portfolio

Assuming that a hypothetical investor had invested $1,000 in each of these stocks ten years ago, he would have significantly outperformed the S&P 500, assuming dividends were reinvested. While an investment in the S&P 500 yielded a CAGR of 13.5%, or an ending balance of nearly $40,000, the model portfolio of these ten stocks would have grown at a CAGR of 15.6% to an ending balance of $48,400. In addition, risk-averse investors would likely have appreciated the lower volatility of the portfolio (maximum drawdown of 19% compared to 24% for the S&P 500).

Of course, the past is not necessarily indicative of future returns. However, I believe the companies listed above have staying power and, more importantly, solid pricing power. They all operate businesses with wide economic moats, and they should be able to continue to grow their distributions to shareholders at a significant rate. As a result, investors should be able to increase their purchasing power over time. The ten companies listed above have increased their dividends by an average of 12.4% per year over the past decade, assuming an equally weighted portfolio. Going forward, it seems reasonable to expect somewhat more modest dividend growth rates, especially for companies with challenges like T. Rowe Price or with de facto dying business models like Altria.

A portfolio like the one I have presented above - which is broadly similar to my own portfolio in terms of sector allocation and weighting - should allow an investor to live off dividend income at some point in the future. Consider the following example of an investor who starts with an investment of $10,000 in the ten companies listed above.

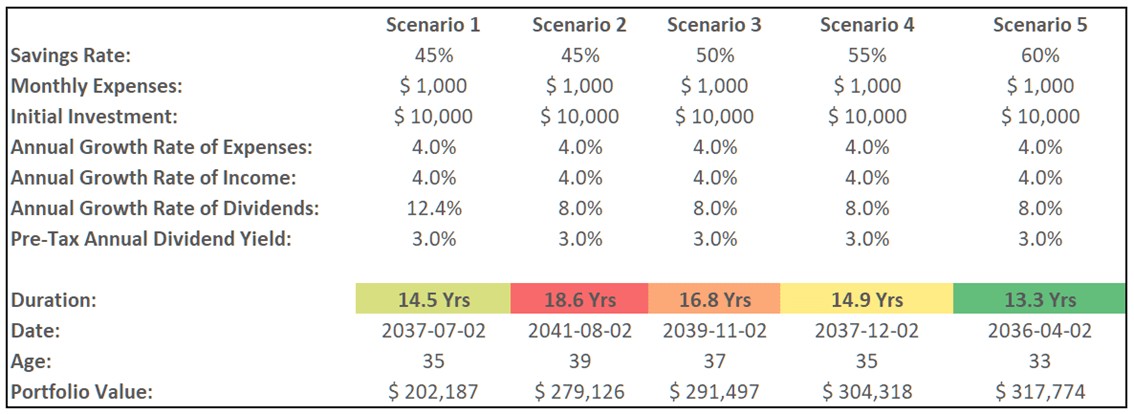

Suppose the investor has living expenses of a hypothetical $1,000 per month and can invest $833 each month, i.e., a savings rate of 45%. His living expenses and income grow at 4% per year, but the dividend income from his ten investments grows at a CAGR of 12.4% (see above). Assuming a weighted average portfolio yield of 3.0%, the investor would need to stick with his or her plan for just under 15 years to become financially independent, i.e., the income generated by dividends exceeds living expenses. Assuming a somewhat more modest dividend growth rate of 8% per year, thereby taking into account the aforementioned headwinds, it would take about 18.6 years for the investor to be able to support themselves on dividends. However, if our hypothetical investor makes another New Year's resolution to increase his savings rate from 45% to 50%, retirement would be almost 2 years closer. At a savings rate of 55%, retirement would be reached after just 15 years, and at a savings rate of 60%, the period would be shortened to just over 13 years (Figure 1).

{kind=link}

I realize that such savings rates are not easy to achieve, especially for families or individuals living in areas with a higher cost of living. Of course, this is just a hypothetical example to illustrate the power of dividend growth and a high savings rate. Every little bit helps, and increasing the savings rate while investing in a diversified portfolio of top-rated companies definitely brings the dream of early retirement closer to reality. Of course, more risk-tolerant investors can focus on higher-yielding stocks with lower dividend growth rates, but I believe my strategy is more universally applicable due to the dependability of the companies, their moderate dividend payouts and because it does not require regular maintenance. Finally, choosing a dividend growth strategy instead of a capital appreciation-focused strategy is more universally applicable, in my opinion, because retirement income is largely decoupled from stock market performance.

Thank you very much for taking the time to read my article.

If you want to learn even more about my research process and what stocks I like, please stay tuned because I am launching a subscription marketplace service with Seeking Alpha in the near future and the first wave of subscribers will get a lifetime discount.

More details coming soon, so please keep following and reading my work.

For further details see:

Your New Year's Resolution For 2023: Invest $10,000 In These 10 Stocks