YPF - YPF Sociedad Anonima: Ridiculously Undervalued Still Not Buying

- YPF is trading at all-time-lows, like most Argentine stocks.

- Metrics show the company is indeed trading at compelling prices. Vaca Muerta, the world's second-largest shale gas reservoir shows enormous potential.

- Unfortunately, risks, uncertainties, poor decision-making, among other factors, overcome all virtues.

- In this article I explain why I decided not to buy YPF (yet), despite today's depressed prices.

- I also explain what my strategy is in order to gain exposure to Vaca Muerta and other interesting assets YPF can offer, while avoiding YPF's intrinsic risks.

Elevator Pitch

- Hey.

+ Hi.

- Have you ever heard of YPF's stock ( YPF )?

+ Ehm... no, not really. What's that?

- YPF stands for 'Yacimientos Petrolíferos Fiscales'. It's the largest Argentine company in terms of revenue, USD 15 billion a year. It's a leading player in Upstream, Downstream, and Power Generation in the country. It also holds interest in Vaca Muerta, the world's second-largest unconventional gas reservoir with untapped potential probably worth hundreds of billions of dollars.

+ Oh, okay. Wow. That sounds really promising.

- Yeah... no. Don't buy it.

Introduction

Okay, worst elevator pitch ever, but it does summarize our line of thought here. As we will see, YPF's assets are impressive indeed, and its stock certainly is trading at very compelling prices. However, as will be discussed later on, risks and uncertainties are just too high.

Moreover, when we take a look at other Argentine listed companies we find we can very easily put together a stock portfolio with exposure to the most attractive assets YPF can offer us, while at the same time avoiding most of these intrinsic risks and uncertainties.

Company Overlook

YPF is just massive. It's a 100 year-old company and the largest in Argentina in terms of revenue, about USD 15 billion a year.

It's a leading integrated player in the local O&G industry and present in the entire value chain. It has a dominant position in upstream with 35% of the total country's total production (39% in crude oil and 32% in gas) with operations in all productive basins, including Vaca Muerta, a massive shale oil and gas formation with potentially more reserves than the country will ever need.

YPF's dominant upstream position (Company's presentation)

{kind=link}

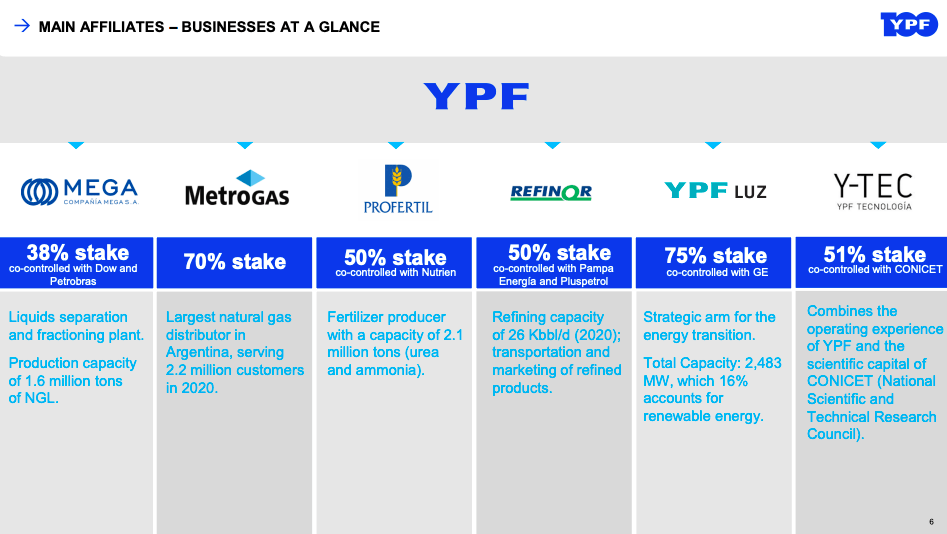

YPF is also a leading player in downstream with a nation-wide downstream distribution network with over 1,600 gas stations, totaling 55% of market share in terms of gasoline and diesel sales. As if that wasn't enough, it also holds a controlling stake in Metrogas, the largest natural gas distributor in Argentina with over 2.2 million customers, and YPF Luz, a key player in power generation with about 2,500 MW of installed capacity.

Here is a glance at YPF's main affiliates.

YPF's main affiliates (Company's presentation)

{kind=link}

Key Metrics

YPF's capital stock is comprised of 393 million shares. At a price per share of about USD 2.9 at the time of writing this article, the company is trading at a market capitalization of around USD 1,100 million.

First, please note that this market cap differs from what most online platforms will show you, reason being that these platforms calculate first the market capitalization in Argentinian Peso ((ARS)) - based on number of shares issued and price per share in the Argentinian stock market - and then convert that to USD using the official FX rate. However, due to strict capital controls currently in place in Argentina, this official FX rate differs significantly from the free market's FX rate known locally as 'Contado Con Liqui', the former sitting at about ARS 135 per USD, while the latter is closer to ARS 300 per USD.

The real market cap is unquestionably USD 1,100 million. There are 393 million shares, each trading at USD 2.9 in the New York Stock Exchange (NYSE), so in theory you would need USD 1,100 million to buy all the shares, or a 100% stake in the company. End of story.

With that out of the way, let's go ahead and take a look at some key metrics.

Company's net debt sits at about USD 5,900 million, therefore YPF's Enterprise Value is USD 7,000 million.

If we take a quick look at 2021's numbers, we find that YPF finished the year with an EBITDA of almost USD 4,000 million, while 2022 will probably end with an EBITDA closer to USD 4,200 million.

This numbers spit out the ridiculously low ratio EV-to-EBITDA of 1.6x. Let's pause here for a second and think about what this means.

If we expect this ratio to converge to something a little more sensible, a ratio of say 4x, we would need an EV of USD 16,800 million. Considering a steady net debt of USD 5,900 million, this would require a market cap of almost USD 11,000 million, almost 10x the current market cap! YPF would comfortably be a ten-bagger.

Now, all these number need a 'little' tweak. You see, we've reached an EV-to-EBITDA ratio of 1.6x by considering an EBITDA of 4,200 million and a net debt of 5,900 million. But these numbers might not represent faithfully the reality of the business. YPF reports its EBITDA mostly by taking first its EBITDA in ARS (all of its revenue is in ARS) and then divide that by the official FX rate. This is not wrong per se, but since the company is unable to access that exchange rate freely due to those capital controls we mentioned earlier, this EBITDA isn't representative of what's really going on. Let's try to make this point clearer with a small exercise.

Imagine you expect to cash out say 12% of the EBITDA via dividends (just taking a random number). YPF should then distribute around USD 500 million, but the company should use the generated ARS and be able to access the official FX rate and buy USD for doing so, but it just can't. With 12% of the EBITDA, it could buy only USD 225 million at the market's FX exchange. So for our purposes we should be better off considering the EBITDA to be USD 1,900 million (i.e. taking EBITDA in ARS and dividing that by the 'Contado con Liqui' rate), and not USD 4,200 million.

On the other hand, the company can access the official exchange rate to pay off its debt (though with some limitations we'll be studying later on). So instead of USD 5,900 of net debt we should be considering USD 2,655 million. This is a fictitious number, not related to the reality of the company, but we do this to make it 'compatible' with other numbers.

So EV/EBITDA is in fact (1,100 + 2,655) / 1,900 = 2x, higher than the 1.6x we originally calculated. Still, arguably a great ratio.

Of course, all this has been an extremely oversimplification and probably not the most elegant way of doing things, maybe even badly enough to offend some analyst (yeah, sorry for that), but that's ok. It will do just fine for our purposes here.

With this ratio in mind, I believe it's safe to say that YPF is indeed undervalued. Especially when we consider the enormous potential Vaca Muerta offers.

But before you jump ahead and buy the stock, let me walk you through the main reasons why I decided not to buy YPF (yet) despite this obvious undervaluation.

1. Gross Debt too High

Let's start by taking a look at YPF's debt situation.

First, the good news. YPF has been improving its debt consistently since 2016.

YPF's net debt evolution since 2015 (Company's presentation)

In fact, in 1Q2022, YPF's net debt is actually lower than shown in the graph above currently, about USD 5,900 million. That's 27% less than 2016's.

In 1Q2022, EBITDA reached about USD 950 million, so the company could reach about 3,800 million of EBITDA a year (I actually believe it will be closer to 4,200 million). That's a Net Debt to EBITDA ratio of just 1.4x (notice we are allowed to do this ratio since both numbers are expressed at the official FX rate, so they are 'compatible'). That's actually really good. So what's the problem?

The main concern here is that in Argentina it's not enough to just have a low Net Debt to EBITDA ratio. You need to have a small amount of debt in nominal terms. Moreover, you want to have your debt maturities well distributed over the years, giving you enough margin of maneuver if things get too complicated (which they often do).

In this market, companies struggle constantly to access USD - there are almost always capital controls in place - and since most of the debt is USD-denominated while revenue is usually in ARS (even for most of exports), then if you can't access - for whatever reason - the FX market to get your hands on some fresh dollars to pay back your debt, then you may find yourself in quite a pickle very quickly. Local companies understand this very well and they keep not only their debt ratios low but also their amount of debt in nominal terms at very low levels (trying at the same time not to lose its tax shield).

Let's go ahead and be a little more precise in this regard. Since early 2020, Argentine companies are required by the Central Bank to refinance at least 60% of debt maturities at a minimum average term of two years, and therefore has only limited access to the official FX market to pay 40% of their debt principal maturing. This presents a constant risk for companies with too much debt maturing in the near term, because it forces them into a constant renegotiation with creditors who may ask for better terms to agree to refinance (therefore increasing cost of debt for companies) or reject refinancing altogether. If not succeeding in this process, companies risk a corporate default. If you want to know more about this regulations, you can find more information in the Central Bank's website here , or more extensively in Communication 'A' 7106 .

Back in 2020, this situation put YPF on the verge of a corporate default, when faced with big debt maturities while its revenue came crumbling down due to covid-19. YPF worked for months trying to reach an agreement with creditors to refinance 60% of that debt principal. In the end, YPF managed to swap 60% of its bonds for new longer ones and avoided the default, but just barely. If interested, you can read more on this here .

So a 1.4x debt ratio looks great, and it is, but it's simply not enough. USD 7,000 million of gross debt is just too high for a company with this zip code.

Let's take a look at YPF's principal debt amortization schedule.

YPF's principal debt amortization (Company's presentation)

Take a look at the graph above. As we can see we have about one billion of debt maturing next year, and another one billion maturing in 2024, followed by almost 1.5 billion in 2025. Remember, companies can't freely access the official FX exchange and are required to refinance 60% the principal debt amortization. This means we will find YPF having to work constantly on refinancing its debt for many years to come. Can we expect a great stock price performance if the market is constantly worried about this? What if it doesn't succeed to do so, or if Argentina's macro deteriorates just a little more to the point the company can't even access that 40% of so desperately needed dollars? What then? In this troubled context, we should be much better off being invested in a company with very low debt, manageable even in the worst-case scenarios.

Let's try to end this item with a positive thought. In regard to YPF's debt situation, I personally believe the worst is already behind us. 2020 was a close call for the company and since then it's been working on improving its debt profile and has succeeded up to some point. But risk is still there and is worth mentioning it. Specially if Argentina keeps on this path, with each day running shorter on dollars having no other option than tightening capital controls even more.

2. Lawsuits: Maxus

YPF is facing two ginormous international lawsuits. First, there's this USD 14 billion lawsuit in the United States. Yes, that is correct. Billion with a B. This lawsuit is for a higher amount than its entire EV or more than eight times its market cap. What on earth is all this about?

In a nutshell, YPF was trying to go global in the late 90's and in 1995 decided to acquire US-based company Maxus Energy Corporation. Maxus was involved in an old conflict over environmental damages caused during the 1950s and 1960s - long before YPF acquired the company - when New Jersey’s Passaic River was polluted with pesticides and other dangerous chemicals. YPF either did not know about this or at least did not fully grasp the magnitude of the conflict. Either way, when realizing the conflict was escalating quickly, YPF allegedly decided to dismantle Maxus and filled it for bankruptcy.

The lawsuit is divided into two parts, the first addressing the environmental damages and the second on Maxus' claims that YPF dismantled the company.

In this lawsuit Maxus claims USD 750 million from YPF plus the transfer of USD 14 billion worth of environmental damages.

3. Another Lawsuit: Expropriation of YPF

On April 16, 2012, former president Cristina Fernandez de Kirchner introduced a bill for the renationalization of YPF, in which the State would buy 51% of the outstanding shares.

The bill was overwhelmingly approved by both houses of Congress, and was signed by the president on May 5. After some dispute with the majority shareholder, Repsol, an agreement was reached on November 27, 2013, whereby the latter would be compensated for a 51% stake in YPF with approximately USD 5 billion in 10-year corporate bonds.

So as of today, YPF is primarily a state-owned company.

According to YPF's bylaw, Argentina should have conducted a public tender offer after gaining control of the company, i.e. a public bid for stockholders to sell their stock. Among these stockholders were Petersen and Eton Park Capital. The public tender offer never happened, violating YPF's bylaw, which resulted in economic damage to these funds.

Litigation finance firm Burford Capital bought the rights from Petersen and Eton to sue Argentina and YPF.

This a lawsuit that can cost up to USD 20,000 million.

Here's a Twitter thread from @SebastianMaril explaining six possible scenarios for this lawsuit. Feel free to translate it to English if needed.

4. YPF is a state-owned company

As we've just discussed, Argentina's State owns 51% of YPF's shares and therefore controls the company. YPF is a state-owned company.

The main consequence of this is that a state-owned company may not have profitability as its number one priority, i.e. it may not necessarily allocate its cash on those investments that will return the most to its shareholders as we normally would expect from a company, but may rather follow a political or a 'common good of the country' agenda.

Maybe it's not the right time to invest in some sector, but will do it anyway because it's 'in the country's best interest'. Or maybe the company enjoys a dominant position in some other sector that may allow it to raise prices and therefore profits (almost) at will but chooses not to simply because it's not in the country's or in the politicians' best interest. Or maybe every four years, when there's a new administration in office, the board of directors is modified and the company swifts priorities, modifying its long-term objectives.

This is exactly what happens with YPF.

As we've seen before, YPF is a dominant player in the downstream sector through its more than 1,600 gas stations, so it could raise prices at will. But this is not the case. On the contrary, this is usually used as a political tool, raising prices behind inflation when needed in a ridiculous attempt to contain inflation numbers (has this ever worked?) or even freezing prices completely for several months when elections are near. This is certainly not in the shareholder's best interest.

I want to give you some concrete examples that show you just how bad politics can affect the company. In February 2019, under Mauricio Macri's administration, YPF signed a 10-year contract with Belgium-based shipowner Exmar for a gas liquefaction barge that would allow the company to export LNG for the first time in the country's history.

A few months later, YPF concluded the first shipment of 25,000 m3 of LNG to Europe. Undoubtedly, a milestone for the company and the country.

In 2020, only 18 months after signing the contract, and now with a new administration in office, this time Peronist Alberto Fernández, YPF decides to terminate that contract. According to different political sources, YPF lost USD 145 million during those 18 months of operation and that's why it should be called off. Regardless of this is true or not, YPF had to compensate Exmar with USD 150 million for the early redemption of the contract. You can read more on this here .

According to those same sources, YPF needed to sell LNG at USD 10 per MBTU or higher to be profitable, and that wasn't happening. Today, only two years later, Argentina imports LNG at a price of USD 40 to 50 per MBTU.

This simple example shows us two things. First, how a change in the political party in power can swift rapidly the objectives of the company and the financial impact that can have. Also, it shows us lack of vision and planification. I mean, calling that contract off only a few months before a commodities boom. Wow.

I can give you literally dozens of these examples, but I'll go ahead with just one more in lieu of briefness.

While I was writing this article, YPF's CEO, Sergio Affronti, resigned his post after only two years in office, due to differences with President of the company, Pablo Gonzalez. Pablo Gonzalez has been President of YPF for just a little over a year now. Before him, Guillermo Nielsen had been President of the company also for just a little over a year.

Question: can a company perform well if its top personnel is constantly being removed and replaced? I don't think so. Or at least we can agree that situation isn't optimal.

5. A (Very) Poor Dividend Policy

If you've read some of my previous articles, you've then come across many local companies probably equally cheap or even cheaper than YPF and with massive dividend policies. Cablevisión Holding ( CVHSY ), for instance, could potentially return up to 30% a year in dividends while also being a ten-bagger, while other covered companies such as Central Puerto ( CEPU ), Loma Negra ( LOMA ) all stand up in the dividends double digits zone.

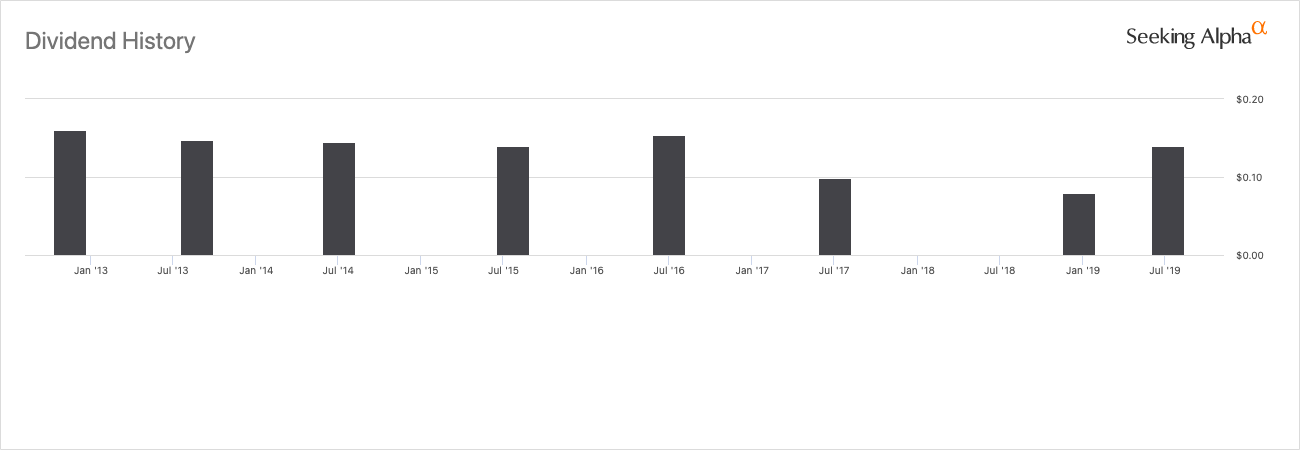

YPF, on the other hand, has a very, very, poor dividend policy. Let's take a look at dividends distributed to shareholders in the last ten years.

YPF dividends in the last ten years ( Seeking Alpha )

{kind=link}

This is an average of about USD 0.11 per share a year, though the company has not distributed dividends since 2019. If we assume this will be the case from here on, then at current prices this would be a 3.4% div yield. This is disappointing considering what other stocks in this very same market can offer. And we reach this div yield considering current all-time lows prices. If we consider instead the stock price when those dividends were paid, we are then talking about a dividend yield of less than 0.5%. And then again, we haven't received dividends in the last three years.

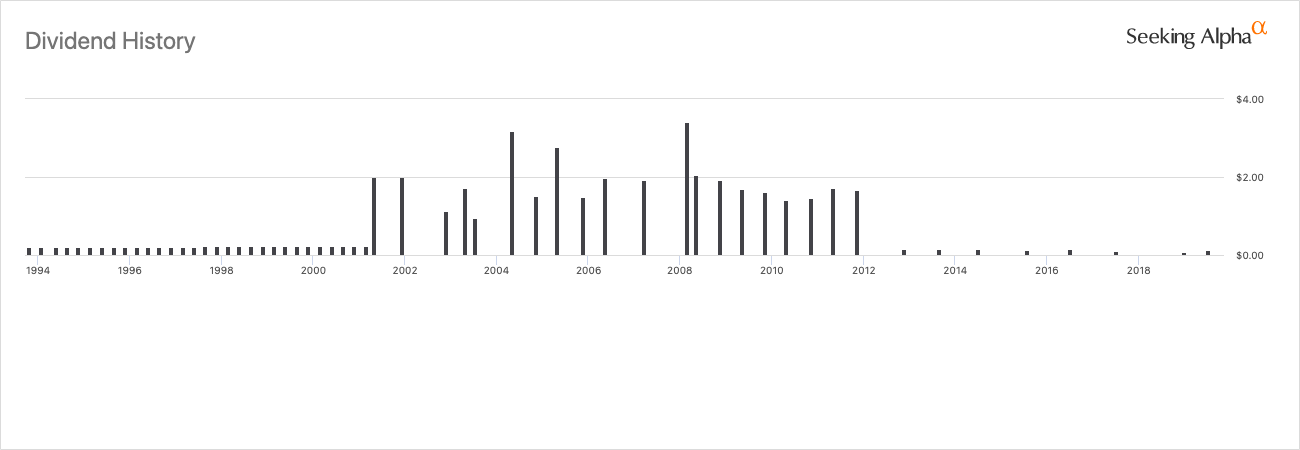

Let's take a look at dividends in the last 30 years.

YPF dividends since 1994 ( Seeking Alpha )

{kind=link}

As can be seen in the graph above, dividends were massive between 2000 and 2012, under Repsol management. In fact, just in 2008 the company distributed almost USD 5.5 per ADR in dividends. That's 170% today's stock price. What the heck happened after 2012? Renationalization happened. Since then, dividends have been even lower than those between 1994 and 2001, when the average dividend was about USD 0.9 per ADR. That would be a 30% div yield at current prices. And we are not even adjusting by inflation here.

This tells us that YPF has been capable of generating tons of cash in the past (and actually is as of today), but that cash has not been going to the shareholder's pockets since 2012, i.e., since Argentinian gov't took over the company. The official explanation is that under control of the State, the company chooses to reinvest basically all of its profit in the business instead of paying back its shareholders. That's fair. It's something that can be done and is done by some of its peer as well. However, that being the case, shareholders should've benefited from a massive increase in the stock's price, something that has not happened. On the contrary, stock is -90% down from its 2012 price. That's not promising at all... We will talk more about the stock performance later on.

Whether we want to admit it or not, truth is that is a common practice for the Argentine gov't to oppose dividend payments, and not just in the energy sector. It does so in other companies where it holds a stake in, specially through state-controlled pension fund Fondo de Garantía de Sustentabilidad.

So unless this policy changes somewhen in the future (which to be honest I don't see happening any time soon), then we can't expect to receive significant dividends from YPF. Logic dictates that we should, since that would benefit the State as well that's so needed of dollars, but at least until now politics overtakes logic in this regard.

Ok, so YPF has a poor dividend policy. No big deal. Other companies choose also not to distribute dividends in cash (Pampa Energía, one of my favorite companies in the local market being one of them). But those companies usually return capital to its shareholders through other means, either by performing aggressive stock buybacks programs or experiencing a great stock price performance, or more typically a combination of both.

6. No Buybacks, Seriously?

Ok, so YPF has a poor dividend policy. But maybe the company is active in the open market doing buybacks which, as we all know, is a more tax-effective way of returning capital to shareholders, increasing the Earnings Per Share which in turn should boost the share price in the long run. At current prices an aggressive stock buyback program is certainly a no-brainer.

Well, turns out YPF has no active stock buyback program whatsoever at the moment. Seriously, why?

In fact, the last time that I recall the company having a buyback program was back in 2020, as a strategy not really aimed at benefiting its shareholders, but as a stock compensation program for its directors.

Of course, there's nothing wrong with a stock compensation program. On the contrary. The idea of such programs is to align both shareholders and director's interests. If the stock price goes up, we all win. Only problem is, that seems not to be working. In fact, YPF's stock has plummeted 90% in the last ten years. Let's take a look at that.

7. Stock Performance

All this wouldn't matter if the stock had performed well in the meantime. I mean, we can be happy with no dividends nor buybacks if the stock just goes up. But this didn't happen. Not even close. Here's YPF stock price in the last 10 years.

YPF's stock performance ( Seeking Alpha )

{kind=link}

Stock is 90% down from its 2012' prices, that's before expropriation. In fact, it's at all-time-lows, even lower than during Argentina's 2001 mega crisis. What's even crazier is that, back then, massive shale reservoir Vaca Muerta was not even on the map.

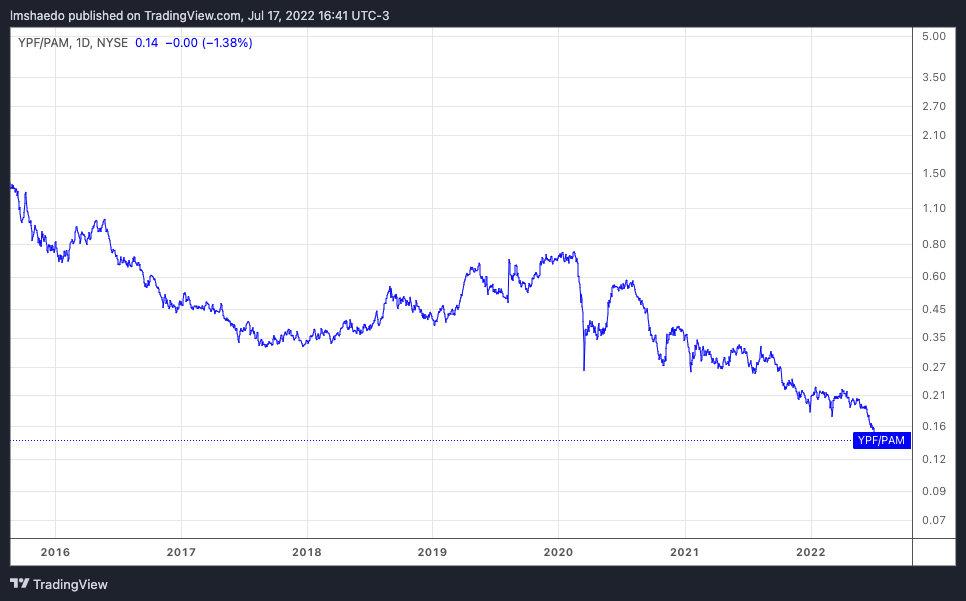

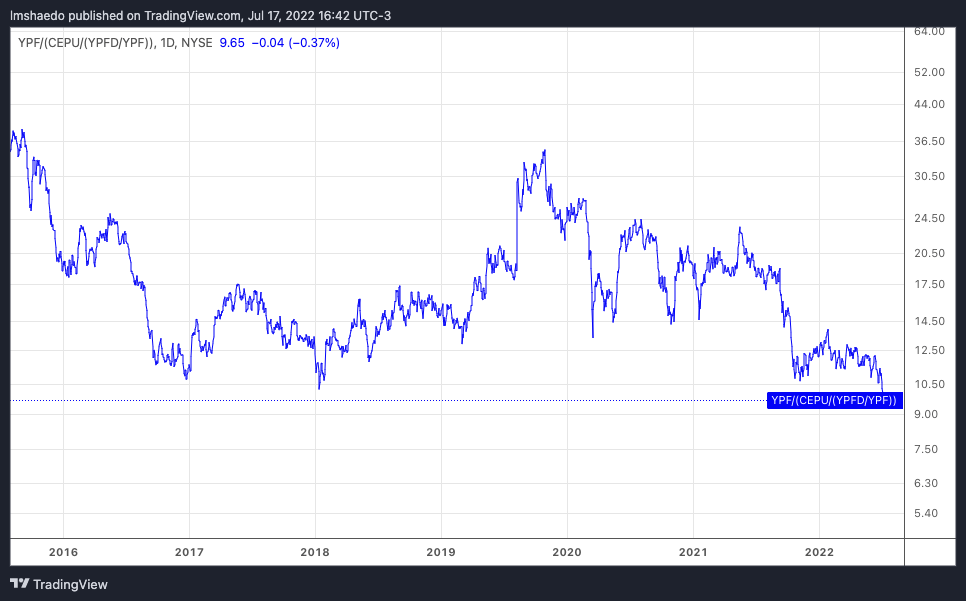

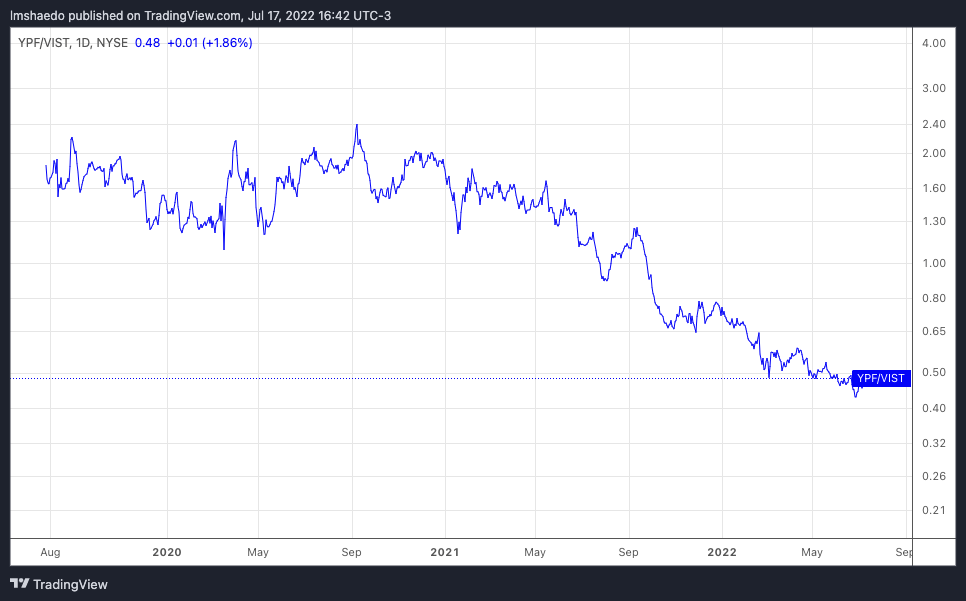

So no dividends, no buybacks, and poor stock performance in the last decade. Well, maybe this last point is not entirely YPF's fault. Maybe it has to do with Argentina's macro, not with the company's actual business. Let's see if this is the case. Let's compare YPF's stock performance against its peers in different sectors, such as Pampa Energía ( PAM ) in Gas, Midstream and Power Generation, Central Puerto in Power Generation and Vista Oil & Gas ( VIST ) in shale oil.

YPF vs PAM ( TradingView ) YPF vs CEPU (TradingView) YPF vs VIST ( TradingView )

{kind=link}

{kind=link}

{kind=link}

Basically, YPF has underperformed against all its peers in the local market.

Based on this graphs, it might be argued that YPF and Central Puerto's performance were (sort of?) similar, but this is actually not the case. Central Puerto distributed hundreds of millions of dollars in dividends during the time shown in the graph. YPF didn't.

Now this very same graphs could be used as a bullish case for YPF. I mean, after all, the company has underperformed its peers. Wouldn't that mean that is could be 'cheaper'? Well not really. Let's take a look at Central Puerto for instance. I've already covered Central Puerto in an article before . Turns out that EV/EBITDA for CEPU was 1x at the time of writing (lower that YPF's), it has a strong dividend policy so we can expect to start collecting double digit dividends in cash soon, an extremely low debt with intentions to lower it down all the way down to zero net debt, and no controlling shareholder., i.e. a company mainly focused in investing and profiting, just the way we like it.

So no, YPF's underperformance doesn't necessarily mean that is lagging against its peers. It means simply that the company has failed in creating value to its shareholders. It means that its decisions are not necessarily based on profiting but on other needs.

Let me be clear about this. There's nothing wrong with this. Really. I understand why a state-owned company makes the decisions it does. Perhaps it truly ends up in a 'better country' sort of situation. But just don't expect me to invest my money there.

Key Takeaways

Based on a quick glance at YPF's key metrics, I believe it's fair to say that YPF is indeed undervalued. Not only that, but the sector seems to be in some sort of inflection point with Vaca Muerta being on the verge of booming (we'll be taking a deeper look into this in following articles). If that's the case, then I believe YPF's stock can be a multi-bagger stock. And for this reasons I'm giving it a 'buy' rating in Seeking Alpha. I truly believe that one can make a profit investing at this crazy low prices.

However, taking a quick glance at Argentina's stock market will reveal that there are in fact bargains all over the place. Even Argentine sovereign bonds seem attractive at current prices (there's a sentence I thought I would never say). So there's really no surprise here. In fact, this is so that I believe one could randomly select some big company's stocks in this market and will do just fine. But we know that that's not enough. Our job as analysts is not to randomly choose stocks and do 'just fine', but to be highly selective, handpicking our stocks in order to achieve the biggest returns possible while also minimizing risks. Is YPF a stock that allows us to achieve that? I think probably not. I think there are better alternatives.

As we've discussed, there are many other companies that are as cheap or even cheaper than YPF is, even within the same sectors. Not only that, but they offer better perspectives on how fast we can make our money back. Some have great dividend policy, others massive stock buybacks plans. All this, without dragging multi-billion international lawsuits on their backs or an always-changing management, or a poor-decision making based on the controlling shareholder's interests.

In effect, say we're interested in gaining exposure to Vaca Muerta, both in the oil and gas business. Well, we could go ahead and buy YPF accepting all its intrinsic risks, or we could instead buy Pampa Energía and Vista Oil & Gas. The former gives us excellent exposure to the gas business while the last one does so to the oil business. Both companies have outstanding management, and creation of value for their shareholders is a number one a priority. And none of them faces international lawsuits. If interested, you can read my article on Pampa Energía . I will be working on an article about Vista soon.

Now say we are interested in the power generation business. Well, Pampa Energía is certainly also a great candidate to gain exposure to the sector, but if we are looking for a pure-play company then that would be Central Puerto. Central Puerto is extremely undervalued as well, and has a strong dividend policy and almost non-existent debt. Ideal for today's market conditions.

There are many other options out there, and I leave as a task for the reader to go ahead and look up for them.

The main conclusion you should be taking from this article is the following. There's really no reason to buy YPF. The best assets YPF can offer can be easily replicated with other better stocks, with less risks, and a higher certainty that we will get our money back. Because sure, YPF can someday become a huge exporter of oil & gas and generate tons of cash. But will that cash be ever used in the shareholder's best interest? Will the company ever distribute dividends? And so, when? And if not, will that cash be invested wisely so as we can have a good stock performance in the future?

Maybe... but I just can't see it yet.

For further details see:

YPF Sociedad Anonima: Ridiculously Undervalued, Still Not Buying