YUMC - Yum China: Appealing Growth Prospects And Reasonably Priced

2023-09-07 01:41:48 ET

Summary

- Yum China Holdings has good revenue and margin growth prospects due to economic reopening and pent-up demand for dine-in services.

- The company's revenue growth is supported by attractive offers, promotional activities, delivery and digital channels, and new unit expansion.

- Yum China stock is trading at a discount to historical averages, making it an attractive investment opportunity.

Investment Thesis

Yum China Holdings, Inc. ( YUMC ) has good revenue and margin growth prospects ahead. The company’s revenue growth should benefit from a gradual increase in mobility due to economic reopening after a three-year-long lockdown. This should unleash the pent-up demand for dine-in services, and increase guest traffic. Further, an increase in attractive offers and promotional activities, strength in the delivery and digital channels, and new unit expansion should also support the sales growth moving forward.

On the margins front, the company should benefit from improving sales leverage, increasing productivity, and efficiency gains in the restaurants. In addition to encouraging growth prospects, the valuation is also attractive with the stock trading at a discount to the historical averages. Hence, I have a buy rating on the stock.

Revenue Analysis and Outlook

In my previous article , I talked about the company’s growth prospects ahead given the economic reopening of China, post a three-year-long lockdown. The company has reported its first and second-quarter earnings of 2023 since then and posted good results. However, the stock price corrected post my previous article in line with the broader market correction, despite good results. I believe the recent stock correction has made the stock an even better buy given improving fundamentals.

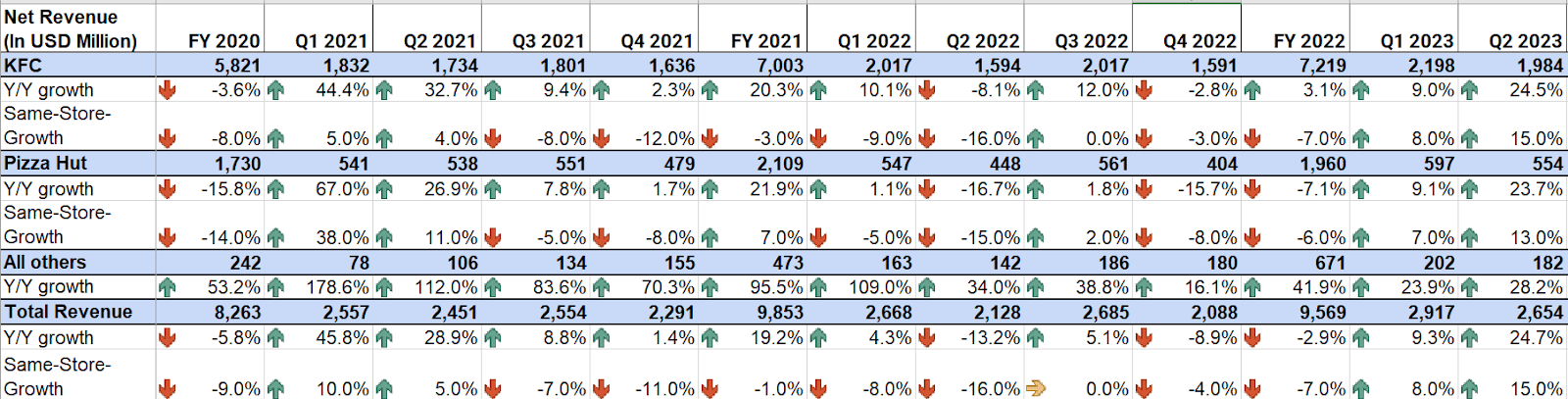

In the last quarter, the company saw recovering sales growth due to the reopening of the economy, which supported pent-up demand for dine-in food services. In addition, the company also saw a good contribution from higher transactions due to the company’s promotions and value offerings along with the pent-up demand. New restaurant openings also benefited the sales growth. This resulted in a 24.7% YoY increase in total sales to $2.6 billion. Excluding a 6 percentage point impact from unfavorable foreign currency, sales grew by 32% YoY. This good revenue growth reflected a 15% YoY same-store sales and the remaining contribution from new restaurant development. The easy comparisons from the previous year’s quarter due to temporary restaurant closures as a result of COVID-19 also helped.

YUMC’s Historical Revenue (Company Data, GS Analytics Research)

{kind=link}

Looking forward, I believe the company should be able to recover its revenue growth further as it continues to benefit from economic reopening and easing of mobility restrictions. Further, the growth should be aided by an increase in value offers and promotions, strength in delivery and digital channels, and new unit development.

China is witnessing a gradual reopening of its economy and a return to normalcy after the three-year-long lockdowns and restrictions on mobility. As the economy continues to adapt to the post-pandemic routine, mobility should further increase and restaurant traffic at the company’s restaurants should be boosted due to pent-up demand. The post-pandemic world is seeing a significant surge in pent-up demand for dine-in services. After enduring lockdowns and restrictions, people are eager to return to the social and culinary experiences that restaurants offer. Whether it's celebrating missed occasions, or simply enjoying the convenience of dining out, consumers are flocking to restaurants in search of a sense of normalcy. This resurgence in demand is a promising sign for the food service industry. So, the pent-up desire for dine-in services should support the industry's recovery in a post-pandemic world and also help YUMC’s sales growth moving forward.

Furthermore, the company is also focused on increasing its guest traffic. For this purpose, the company has been increasing value offerings to help the consumer deal with inflation while enjoying the long-waited experience of dine-in post-pandemic. The company has expanded its pricing options by introducing promotions and lowering entry-level costs. In the past year, KFC effectively rolled out appealing promotions, such as KFC's Crazy Thursday, which has been helping drive 50% more sales than other weekdays, and the ongoing Sunday Buy More Save More deal at KFC, which is boosting weekend sales. For Pizza Hut, Scream Wednesday where the company offers different meal choices from pizza, steak, rice, and pasta to appetizers at an attractive price of US$3 to US$5, is helping increase guest traffic.

These efforts resulted in a 21 percentage point increase in transactions in KFC and a 27 percentage point increase at Pizza Hut in the second quarter of 2023, helping the same-store sales growth. The company plans to further accelerate these value and promotional offers moving ahead as well in order to capture the pent-up demand while supporting consumers during inflationary times. So, I expect these increases in promotions should continue to help the same-store sales growth moving forward.

Moreover, during the pandemic, the company saw a good surge in online delivery channels which helped in partially offsetting the temporary dine-in closures. Now as the dine-in services have resumed, delivery and digital channel sales growth are normalising. However, despite normalization, it is still well above the pre-pandemic and at very healthy levels. In the second quarter of 2023, delivery sales grew by 25% YoY at KFC and by 9% YoY at Pizza Hut on a constant currency basis. The company is working with third-party online platforms to expand its reach, for example, prepaid discount vouchers and geographically specific deals, which are helping attract new members and have increased the spending of existing customers.

Further, digital sales including delivery, mobile orders, and kiosk orders, accounted for approximately 90% of KFC and Pizza Hut's Company sales in the second quarter of 2023, with 66% of member sales, up 400 bps YoY. This was a result of growing loyalty program membership which exceeded 445 million members, up 15.6% YoY. To further recruit and engage members, YUMC is introducing interesting member-exclusive perks to customers, such as app-exclusive new product presales and lucky draws utilizing member points. So, I expect delivery and digital channels to keep fueling the overall sales growth despite their growth rate normalization.

Lastly, the company is also well poised to expand its sales growth with the help of new unit development. Over the recent years, the company has been focusing on opportunities to expand its reach and increase market share, and it has accelerated the net unit development. The company saw an 11.8% YoY increase in the second quarter of 2023 with a 3.2% sequential increase to a total unit count of 13,602.

YUMC’s Historical Store Count Growth (Company Data, GS Analytics Research)

This increase in unit development has helped the company increase its market share and, as post-pandemic normalcy returns, this strong growth in restaurant footprint should help the sales growth. The company plans to keep the pace of new unit development constant moving forward as well with a goal to open ~445 to 645 net new stores in the second half of 2023 to reach the target of 1100 to 1300 net new unit development for the current year.

Moreover, the company is expanding its footprint both in top-tier cities as well as low-tier cities which is helping attract consumers across geographies and income brackets. While it is helping the company gain good traction and pent-up demand, the company is also focused on expanding in different geographies by utilizing different channels such as universities, hospitals, and high-speed railway service stations. It is also diversifying its store formats by opening up smaller format stores focused on takeaway and delivery which requires less investment and has a good payback of 2 years. These stores are helping in boosting off-premise sales and also increase market share. Further, these also include pop-up stores and food trucks which help attract traffic by increasing customer convenience and store accessibility. The company plans to open more of these store formats for holidays and festivals, which should help add incremental guest traffic. So, I expect the company to accelerate its top-line growth through new unit development in the coming years.

Hence, I remain optimistic about the company’s sales growth prospects ahead.

Margin Analysis and Outlook

In the second quarter of 2023, the company’s margins saw favourability from commodity and wage costs due to volume leverage. In addition, price increases also helped the company’s margins. Moreover, cost-savings and productivity improvements also supported the margin growth in the quarter. This resulted in a 400 bps YoY increase in total company-owned restaurant-level margins to 16.1%. On a consolidated basis, the adjusted operating margin increased by 590 bps YoY to 9.8%.

YUMC’s Historical Company-Owned Restaurant Margin and Adjusted Operating Margin (Company Data, GS Analytics Research)

Looking forward, I believe the company should be able to deliver margin growth. One of the biggest margin drivers for any company is sales leverage and, over the past three years, YUMC saw headwinds from sales deleverage due to declining sales. Now, that sales growth is recovering, the company is able to drive sales leverage. So, I expect as the sales continue to recover, sales leverage should help in delivering margin growth moving forward in the year.

Moreover, the company is also seeing benefits from productivity and efficiency initiatives accelerating. The company is enhancing its supply chain network with advanced technologies in order to improve store economics. Those initiatives have helped the company save costs through supply chain efficiencies and increasing labor productivity. The company has also taken steps to boost operational efficiencies within its restaurants. These efforts include utilizing digitization to allow store management teams to work across multiple stores. AI-driven systems implemented in these initiatives have streamlined administrative tasks, freeing up Restaurant General Managers (RGMs) from repetitive duties. So, by further integrating its store management system, the company has improved the visibility into store operations and in turn, supporting RGMs in more effectively managing multiple stores while maintaining operational standards. These initiatives should unlock further cost savings and improve productivity.

Moreover, as discussed in the revenue analysis, the company has accelerated its new unit development, and these new store openings are equipped with all these productivity measures and enhanced digital infrastructure. This has meaningfully improved the per-store economics of new stores as compared to the stores in the pre-pandemic era. Around 40% of YUMC’s current stores have opened after 2019, and presently, the company is opening an average of one new store every five hours. This expanding portfolio of stores is well-positioned to operate efficiently in the changing market landscape due to the company's efficiency initiatives. Therefore, as the company continues to add new units, the associated improvements in efficiency and cost structure should continue to boost margins in the long run. Hence, I remain optimistic about the company’s margin growth prospects ahead.

Valuation and Conclusion

Yum China is currently trading at a forward P/E ratio of 24.66x based on the FY23 consensus EPS estimate of $2.18, and 20.72x based on the FY24 consensus EPS estimate of $2.59. This is at a discount to its 5-year historical average forward P/E of 34.40x. Post my previous article, the stock price saw a correction largely due to broader market correction and also due to some concerns around lower consumer spending in an inflationary environment.

However, I am not worried about the company’s growth prospects ahead, as the company is well poised to benefit from a gradual return to normalcy and further increase in mobility moving forward. The pent-up demand for dine-in services, increasing promotional activities, strength in delivery and digital channels, new unit development, sales leverage, and improved store economics should support the company’s growth prospects ahead. This should offset any weakness arising from macroeconomic uncertainty and, hence, I believe the recent correction has made the stock even more attractive in terms of valuation. So, I am continuing to have a buy rating on the stock. I am also looking forward to hearing management updates on the company’s long-term growth plans in the upcoming Investor Day on 14th September 2023, which I believe should further improve the investment community's understanding of the company’s long-term prospects and act as a catalyst for the stock.

For further details see:

Yum China: Appealing Growth Prospects And Reasonably Priced