YUMC - Yum China: Good Growth Prospects Ahead

2023-04-20 10:39:38 ET

Summary

- Revenue should benefit from pent-up demand, price increases, new product launches, and new store growth.

- Margins should see recovery with the help of price increases, improving productivity, and sales leverage.

- Valuation is lower than historical averages.

Investment Thesis

Yum China Holdings, Inc. ( YUMC ) is expected to benefit from the reopening of the Chinese economy as the Zero-COVID policy is finally being lifted. The pent-up demand for dine-in food services, which was dampened by the pandemic, should help increase guest traffic along with off-premise business, boosting revenue growth. In addition, YUMC's market share gain during the pandemic, price increases, and new store openings are also expected to contribute to sales growth.

On the margins front, sales deleverage, which was the biggest pain point for margins, is expected to ease, helping to recover margins as the year progresses. In addition, price and productivity increases are also expected to contribute to YUMC's margin recovery. Moreover, the company is currently trading below its historical average valuation, and given the growth prospects ahead, the stock is a good buy.

Revenue Analysis and Outlook

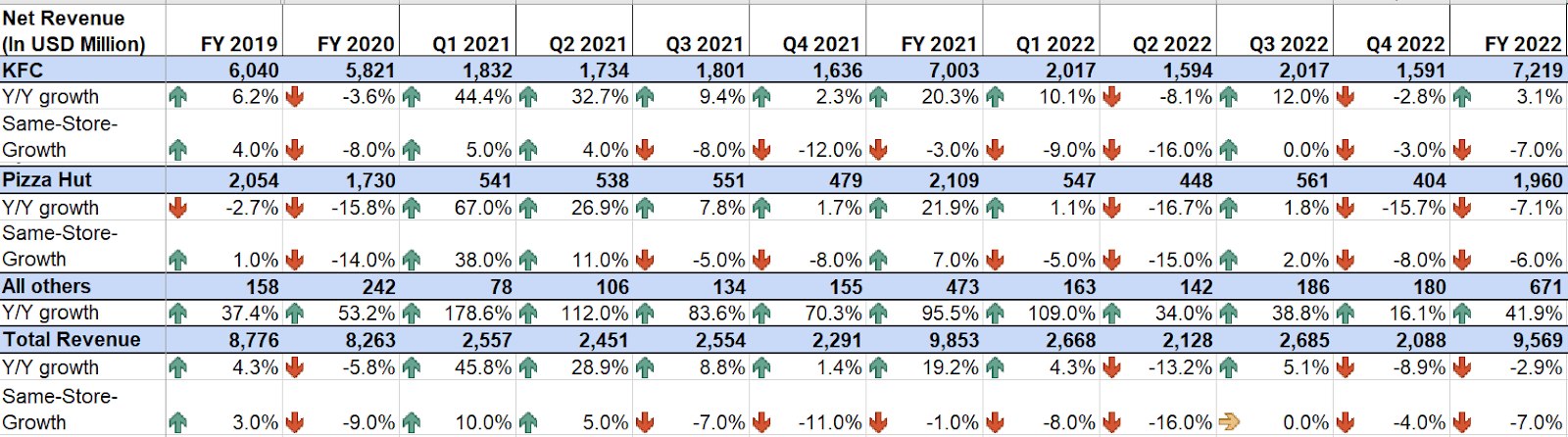

Over the past three years, Yum! China's sales growth has been consistently impacted by travel restrictions and lockdowns due to COVID-19. To counter the disruptions caused by the pandemic, the company focused on its off-premise business and doubled its delivery services from 20% of the sales mix in 2019 to 39% in 2022, which helped it partially offset the decline in dine-in services.

In Q4 2022, while growth through digital and delivery trends continued, a surge in COVID infections in December led to lower comparable transactions (guest traffic) and store closures. Moreover, Yum! China also experienced sales losses due to labor shortages as riders and employees fell sick. However, the higher mix of delivery sales helped increase the average ticket size (delivery sales have a higher ticket size than dine-in sales) and partially offset the lower guest traffic. As a result, same-store sales declined by 4% year-over-year, with reported sales declining by 8.9% year-over-year to $2.08 billion. Excluding the FX impact, sales increased by 2% on a constant currency basis.

YUMC’s Historical Revenue (Company Data, GS Analytics Research)

{kind=link}

Looking ahead, I see YUMC as having good revenue growth potential, driven by Chinese economic reopening and pent-up demand for dine-in services, along with price increases and new unit growth.

Following nationwide closures lasting three years, China's economy is finally reopening, which should lead to a sales uptick for YUMC as mobility restrictions gradually ease. In January, YUMC saw good sales momentum with the relaxation of COVID policies, and during Chinese New Year, same-store sales rose by mid-single digits YoY, indicating strong pent-up demand for dine-in food services. Moreover, the company has gained market share over the past three years as many small players exited the market due to COVID-related challenges. This bodes well for YUMC's sales growth potential.

Furthermore, YUMC plans to implement price increases to protect itself against rising inflation. This along with a higher delivery mix (which has a higher ticket size than dine-in) should boost the company's average ticket size. Accordingly, I expect same-store sales to increase moving forward. Nevertheless, there are concerns about consumer spending due to the uncertain macroeconomic environment and rising inflation. In response, YUMC plans to widen its price range by providing promotions and lower entry points to mitigate the impact of consumer price sensitivity in an inflationary environment. The company has successfully implemented such promotions over the past year, including Crazy Thursday at KFC, which drew a lot of traffic, and the Sunday Buy More Save More offer, which continues to benefit weekend sales. Value offerings through continuous promotional activity should help offset the inflationary headwinds on guest traffic.

Besides promotional activity, YUMC has a history of attracting consumer traffic by introducing new menu items across price points. Despite the pandemic during the last three years, YUMC has launched about 500 new products every year, including regional and national launches, to drive more sales. For instance, KFC's new Juicy whole chicken and Beef Burger generated 5% of KFC's sales mix in Q4 2022, which is almost equal to its original chicken recipe. YUMC continues to introduce new flavors in these categories, such as the Spicy Whole Chicken, which launched during Chinese New Year. I expect these new menu product launches to continue driving guest traffic and supporting sales growth along with promotions.

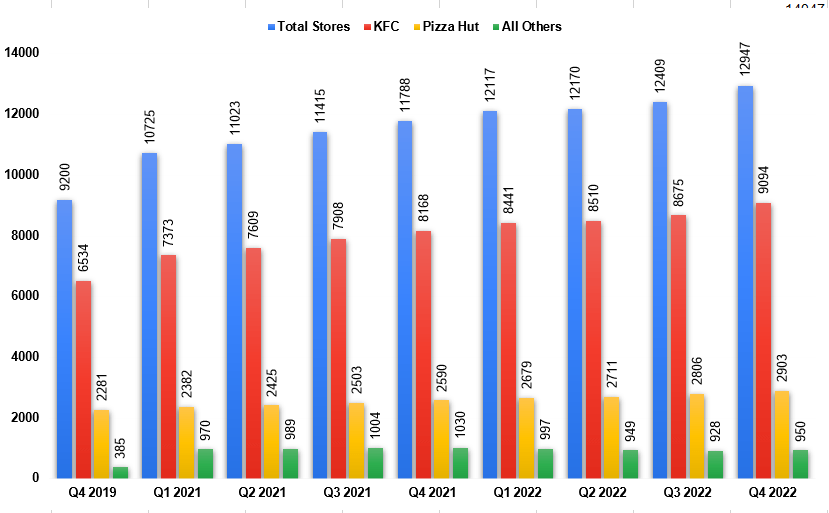

In the long term, YUMC has an attractive growth potential driven by its increasing store footprint. Despite COVID-related challenges, the company has increased new stores by around 40% to 12,947 since Q4 2019. YUMC has expanded new stores in both higher-tier and lower-tier cities, with a focus on filling the gap between stores and increasing the density of stores in higher-tier cities, which is crucial for the delivery business.

YUMC’s Historical Store Count Growth (Company Data, GS Analytics Research)

{kind=link}

While expanding in higher-tier cities can help YUMC fill gaps and increase store density for delivery services, there is also significant opportunity in lower-tier cities where the company can further gain market share. For 2023, YUMC has set a target of opening 1100-1300 net new stores, which represents an 8.5%-10% increase from Q4 2022. Therefore, I believe that YUMC's new store expansion strategy should continue to support its sales growth in the coming years, and overall, I remain optimistic about the company's sales growth prospects moving forward.

Margin Analysis and Outlook

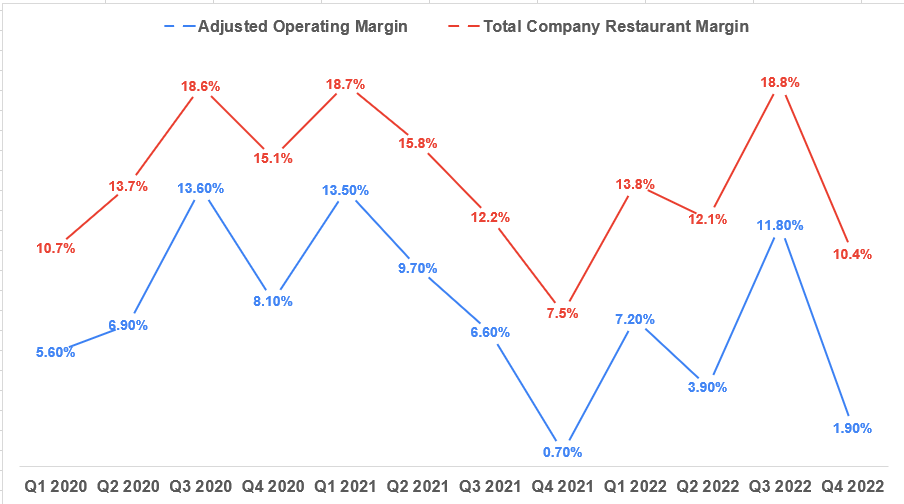

Throughout the pandemic, YUMC’s margins have been negatively impacted by labor wage inflation and sales deleverage as a result of COVID-related disruptions. The impact of sales deleverages was more pronounced in quarters with tighter COVID restrictions.

In Q4 2022, the margins were similarly affected by sales deleverage, but the company was able to offset this through cost savings and labor productivity initiatives. Additionally, a temporary relief fund of $26 million (including $12 million rental relief) from the government and landlords also helped mitigate the impact of sales deleverage. As a result, total company restaurant margins increased by 290 bps YoY to 10.4%, while the adjusted operating margin increased by 120 bps to 1.9%.

YUMC’s Historical Restaurant Margin and Adjusted Operating Margin (Company Data, GS Analytics Research)

{kind=link}

Looking forward, I believe YUMC should be able to achieve margin growth. The biggest factor negatively impacting margins over the past three years has been sales deleverage, but thanks to the Chinese economic reopening, this pain should gradually ease, and help YUMC recover its margins as we progress further into the year.

Additionally, YUMC has been focused on improving labor productivity and unit economics over the last couple of years, by enhancing its supply chain network with advanced technologies. For example, the use of IoT (Internet of Things) and AI enables real-time supply chain monitoring of frozen raw food products. This system monitors the temperature of products in transit, including all refrigerated trucks delivering to stores at any given time, as well as cold storage facilities. All detected exceptions are sent via GPS network to YUMC's digital call center, where the company contacts the relevant driver or operator to resolve the issue and reduce wastage. YUMC is also utilizing technologies such as truck docking station management and automated storage to improve operational efficiencies at its logistics centers. It is also rolling out a smart order system at KFC, which uses AI to more accurately predict demand and recommend a food preparation plan to minimize stockouts and wastage, as well as reduce waiting time for customers. Therefore, I expect these technology investments to continue improving productivity and help YUMC recover margins.

Furthermore, the company is planning to increase its prices to offset the inflationary commodity and labor pressure, which should support margin recovery moving forward. So, I am optimistic about YUMC’s margin growth prospects in the coming years.

Valuation and Conclusion

Yum China is currently trading at a forward P/E ratio of 32.18x based on the FY23 consensus EPS estimate of $1.97 , and a 26.60x based on the FY24 consensus EPS estimate of $2.38. This is lower than its 5-year historical average forward P/E of 34.23x . YUMC has strong growth prospects, thanks to the lifting of the zero-COVID policy. Revenue is expected to benefit from market share gains during the pandemic, pent-up demand for dine-in food service, price increases, new product launches, and promotional activities. Margins are also expected to resume their recovery as the impact of sales deleverages ease. The long-term Chinese growth story is also attractive. While, in the last few years, the company’s results have been impacted by COVID-related restrictions in China, I believe the company should post a good recovery over the coming years. Hence I have a buy rating on the stock.

For further details see:

Yum China: Good Growth Prospects Ahead