YUMC - Yum China Holdings: Positive About Strategies Put In Place

2023-11-03 17:15:00 ET

Summary

- Yum China Holdings, Inc. reported 8.5% revenue growth, with 4% SSSG for KFC and 2% SSSG for Pizza Hut.

- Management is implementing strategies to combat softer consumer sentiment.

- Despite some areas of concern, such as declining restaurant margin, the management's response and favorable commodity prices support YUMC's growth outlook.

Summary

Following my coverage of Yum China Holdings, Inc. ( YUMC ), I recommended a buy rating as YUMC continues to show positive performance in SSS and margin recovery. This post is to provide an update on my thoughts on the business and stock. I reiterate my buy rating for YUMC, as I am positive about the strategies that management has put in place.

Investment thesis

YUMC reported 3Q23 total revenue of $2.914 billion. On a year-over-year basis, total revenue increased 8.5% thanks to 8.4% growth in the KFC brand and 6.8% growth in the Pizza Hut brand. For KFC, the brand saw same-store sales growth [SSSG] of 4%, and for Pizza Hut, the brand saw 2% SSSG. For profits, the restaurant margin declined to 17% vs. 1H23's 18.3% and 3Q22's 18.7%. The decline in restaurant-level margin was mainly due to higher-than-expected food and paper costs. This led to a group operating profit of $323 million and margins of 11.1%, a decline of 70 basis points compared to 3Q22. However, I would note that the group's operating profit experienced a lapping of $30 million in temporary relief related to COVID, contributing 1.12% of sales in 3Q22. As such, if we were to adjust for this, the like-for-like comparison would be 11.1% (3Q23 operating profit margin) vs. 10.65% (3Q23 11.77% - 1.12% = 10.65%), a ~46bps improvement.

While the results might seem a little weak from a headline perspective, revenue growth slowed to 8.4% vs. 24.7% in 2Q23 and 9.3% in 1Q23; group operating profit margin declined. I remain optimistic about YUMC's business and growth outlook.

For revenue growth, management mentioned that they noticed softer consumer sentiment in late September and early October and that consumers are still being cautious in their spending, as shown by a slight slowdown in sales of premium products. To combat these, they have responded by expanding the price range across the board, including higher-end options for those looking to splurge as well as more affordable options for value buyers. In my opinion, this should help capture and retain more consumers on the YUMC platform, as there is a relevant price point for everyone. One example of such a strategy is that YUMC is penetrating the below-RMB50 price point for pizzas and single-person meals. I see this as the right strategic move, as YUMC currently only has a single-digit percentage of Pizza Hut's revenue coming from pizzas priced under RMB50 and has an average party size of over 2. Aside from the Pizza Hut example, for KFC, management strategy is to add product offerings. YUMC has been successful, as can be seen from its successful launch of whole chicken and beef burger categories, which have collectively exceeded 6% of KFC's sales mix, higher than the classic original recipe chicken (which has been on the market for over 3 decades). This gives comfort that YUMC understands its market really well and is able to navigate the changing consumer environment to position itself.

For operating profit margin, aside from the like-for-like comparison issue that I addressed earlier, I expect margins to remain stable as commodity prices were favorable in 3Q23, with inflation of poultry netted out by cost deflation of other proteins, including pork and beef. The remaining concern is wage inflation, which has escalated from a low single-digit percentage in 1H23 to a mid-single-digit percentage in 3Q23, but management is expecting this to stay at a mid-single-digit percentage in 4Q23. That is to say, we should not see an increase in headwinds in the near term.

And we also faced higher poultry prices in the quarter. This was partially offset by more favorable prices for commodities, including beef and cooking oil, as well as full utilization of chicken. 3Q23 earnings results call

On another note, with regard to competition, I give merit to the team from Tastien for garnering quite a bit of momentum. However, this is not to say that YUMC has fallen behind and cannot catch up. YUMC already has a strategy in place to combat this competitive pressure by launching their own Chinese-style burger at a competitive price in three provinces, mainly in the T2 cities, and so far, management is seeing positive feedback.

All in all, I'd say that 3Q23 performance was good, and management has rolled out key strategies that I believe will help support YUMC's growth and market position.

Valuation

Own calculation

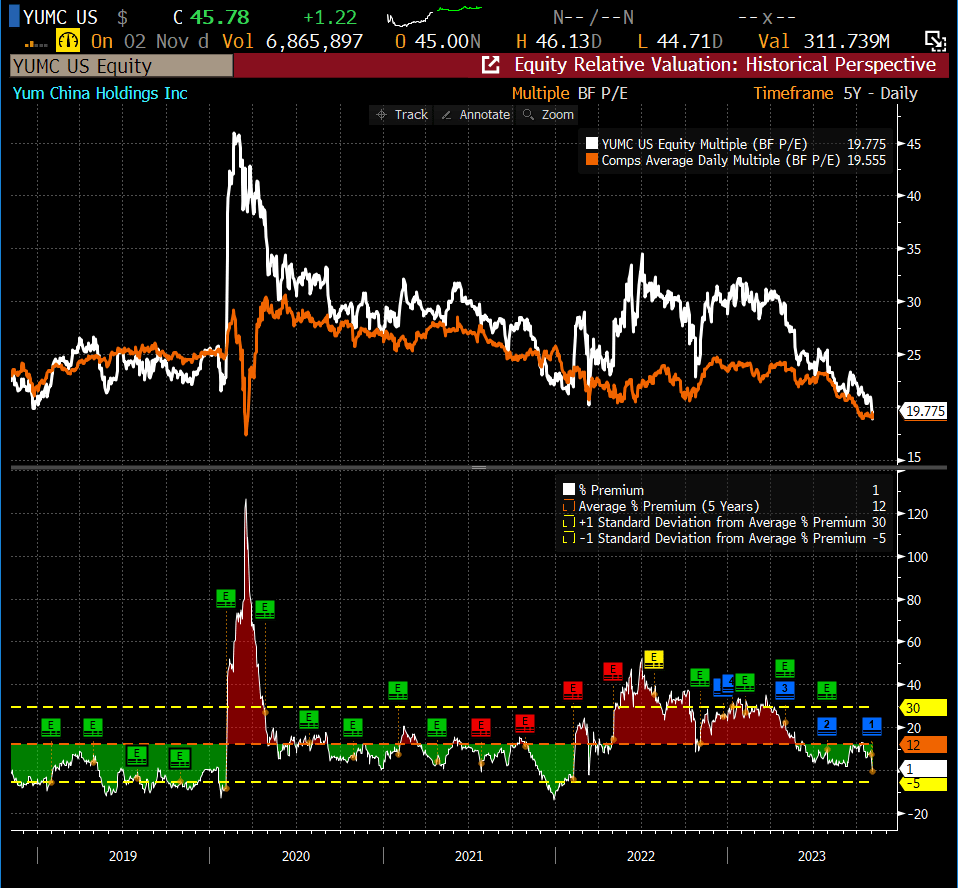

I believe the fair value for YUMC based on my model is $60. Following up from the previous model, I remain confident that YUMC can continue to grow; however, I am tapering my expectations for FY23 given the 3Q23 performance and also the management commentary regarding consumer sentiments. I did not change my assumptions for FY24 and FY25, as I believe the strategies in place should work. I have also revised my net income margin expectations down by 50 basis points from FY23 to FY25, given the wage inflation situation. For valuation, YUMC's peer group has traded down by almost three full multiple turns since I gave an update, and this has dragged down the stock performance on YUMC. In my opinion, this is a near-term issue, as the market might have downgraded this basket of peers altogether. YUMC deserves to trade at a premium, as I mentioned previously. The business has a faster growth outlook than peers' averages of mid-to-high single-digit growth and no debt (YUMC is the only one in a net cash position). Hence, I continue to assume YUMC to trade at 2x above peers, which is the average premium that it has received over the last 5 years (12% * 20x forward p/e = ~22x).

{kind=link}

Risk

As management mentioned, the risk is a further slowdown in consumer sentiment. While strategies are in place to reduce this impact and potentially capture share (as consumers trade down), a steep reduction in out-of-home food spending could negate all these positive measures.

Conclusion

I maintain my buy rating on YUMC due to the strategies implemented by the management team. While the latest financial results showed some areas of concern, such as a decline in restaurant margin and a softer demand trend, I remain optimistic about YUMC's business and growth outlook.

The management's response to the challenges, including expanding the price range and introducing new product offerings, seems well-suited to capture a wider consumer base and address the weak consumer sentiment. Despite wage inflation, commodity prices have been favorable, which should help stabilize operating profit margins in the near term.

For further details see:

Yum China Holdings: Positive About Strategies Put In Place