YUMC - Yum China Holdings: Reiterate Long As SSS Continues To Show Strength

2023-08-10 07:10:17 ET

Summary

- YUMC continues to show signs of recovery with strong SSS growth for KFC and Pizza Hut.

- Government stimulus measures to boost consumer confidence unlikely to show up in YUMC's numbers in the near-term.

- Despite short-term margin pressures, YUMC's strategic initiatives should improve long-term margin profile.

Summary

Following my coverage on Yum China Holdings (YUMC), which I recommended a buy rating due to my expectation that YUMC will see improvements in operating performance as SSS showed signs of recovery in the previous quarter. This post is to provide an update on my thoughts on the business and stock. I continue to recommend a buy rating for YUMC as the stock's valuation continues to be below its intrinsic value. As YUMC continues to show strength in SSS and recovers margin, I believe the market will reflect the value that I expect YUMC to trade at.

Investment thesis

KFC's SSS grew by 15% year over year in 2Q23, while Pizza Hut's grew by 13%. As of 2Q23, both of these brands had reached 10% and 6% of their 2019 levels, respectively. After hearing the management's comments, I'm optimistic that SSS will continue its recovery momentum. During the holiday season, YUMC saw a significant uptick in SSS, especially at its transportation hub stores. Even more promisingly, T2 cities' tourist attraction stores have fully recovered to pre-COVID levels. In the wake of the holidays in May, consumer demand for YUMC slowed significantly. However, the company was able to regain its footing in June, when consumer sentiment improved and new records were set for the number of daily transactions processed (8.5 million on Children's Day). The success of the latter strategy gives me confidence in the efficacy of YUMC's advertising and marketing strategies.

Management is still wary of a full SSS recovery in 2H23, but they expect the recent government consumption stimulus measures to boost consumer confidence in the long run. However, in my view of the Chinese economy, shoppers are still hesitant to make purchases (i.e., consumer sentiment is unchanged ). Therefore, stimulus's effects are unlikely to become apparent anytime soon. To combat this, the company's management is broadening the company's price range in order to attract a wider range of potential customers and improve the company's value proposition by offering more competitive pricing on better products. Even though small restaurant operators are returning to the market (as mentioned by management during the call), I believe YUMC is in a very favorable position to defend itself. YUMC's value-focused offerings (which do well in the current consumer demand climate), nimble supply chain (lower COGS than sub-scale peers and better operational support for its stores), and robust digital capability (to take advantage of the new demand paradigm - delivery and in-store efficiency improvements) are its main sources of competitive advantage. With the groundwork in place, YUMC should be able to make quick and effective changes to its market position and product offerings in order to boost revenue.

While SSS should drive positive topline action, I expect pressure on the margin in 2H23 due to a couple of factors. First, management believes that chicken prices will continue to rise in 3Q23. Secondly, inflation in wages, which is expected to run in the low to mid-single digits. Last but not least, YUMC's $30 million one-time relief in 2Q22 makes 3Q22's margin comparison more difficult. Nonetheless, I do not believe these problems are structural and will have an impact on YUMC's long-term margin profile. Never forget that YUMC is proceeding with its plans to fully digitize its operations (storefront, etc.), optimize store space (smaller stores), and refine its cost structure via preferable least terms. All of these are actions that will increase the long-term profitability of the business.

Valuation

Own calculation

I believe the fair value for YUMC based on my model is $77.96. My model assumptions mirror my previous update. I continue to expect higher growth in FY23 as YUMC experiences recovery growth back to pre-COVID levels. Management's near-term focus on driving sales should also benefit 2H23 and FY24. Margin expectations remain the same as well, and I see them continuing to improve as management restructures its cost base, digitalizes the portfolio, and improves operating efficiencies.

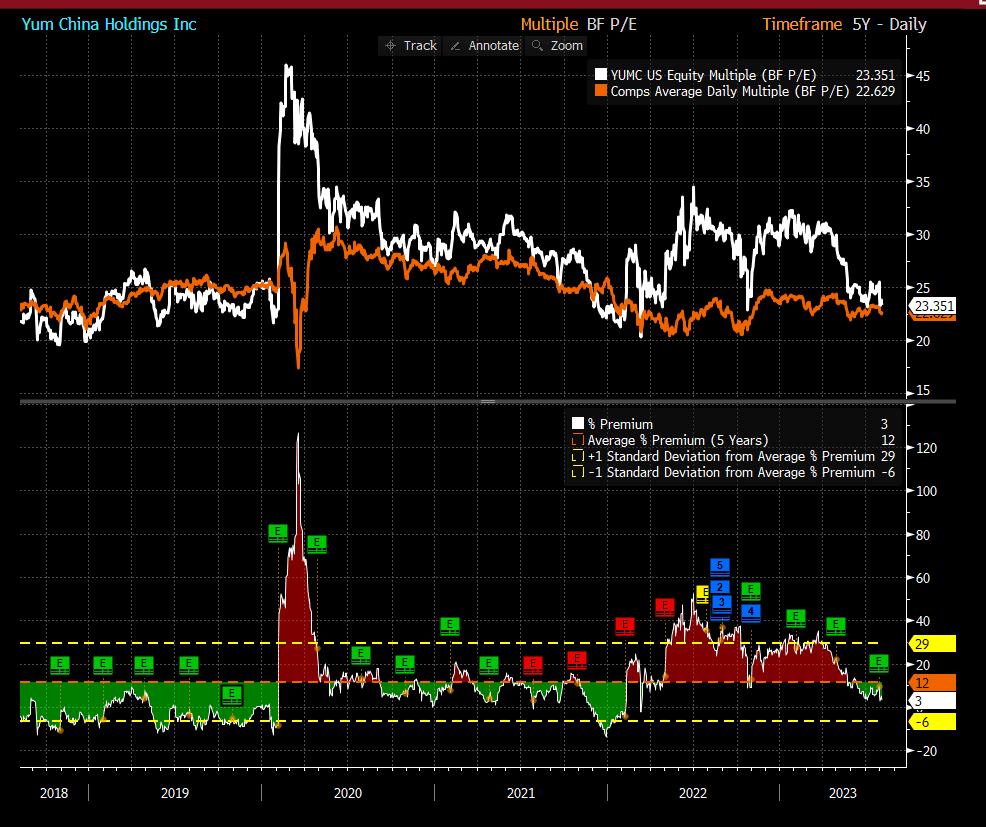

Peers include Domino's Pizza, Yum! Brands, Restaurant Brands, McDonald's, Starbucks, Wendy's, and Jack In The Box. The median forward PE multiple peers are trading at is 24x, the expected 1Y growth rate is 9%, and the leverage multiple is 5x net debt-to-EBITDA. YUMC is trading at 23x forward PE today, which I think is not justified as the company is expected to grow faster (17% vs. 9%) and is in a net cash position. As such, I modeled a slight premium to where the peers are trading, which is also the average that YUMC has traded at over the past 10 years.

{kind=link}

Risk

Delivery platforms may offer substantial discounts to customers in order to increase their user bases and significantly broaden and subsidize consumer choice, thereby taking market share away from YUMC.

Conclusion

YUMC remains a compelling investment opportunity. The consistent growth in SSS indicates a resilient market presence. While challenges like rising chicken prices and wage inflation may impact short-term margins, YUMC's strategic initiatives, including digital transformation and cost optimization, position it well for sustained profitability. Considering YUMC's faster growth and net cash position compared to peers, its current valuation appears conservative.

For further details see:

Yum China Holdings: Reiterate Long As SSS Continues To Show Strength