ZLDSF - Zalando Continues To Execute But The Economic Environment Is Problematic

- Zalando continues to execute on transforming its business.

- Zalando is cheap according to its own targets.

- But the state of the European economy is problematic.

While Zalando's ( ZLDSF ) (ZLNDY) stock price has declined significantly due to the inflationary environment, a recession and other economic factors; the company continues to execute well on its long-term vision. The market seems too focused on short-term margin contraction from its wholesale business. Zalando is undergoing a transformation that will create significant long-term value.

I already discussed Zalando in my previous article. A short summary: Zalando is a European fashion platform and very popular in particularly Western Europe. The company has until now grown significantly by operating as a wholesale business: but it is now transforming into a platform/partner led business. A big reason for its success is that the company from its inception had an incredibly flexible return policy.

Results

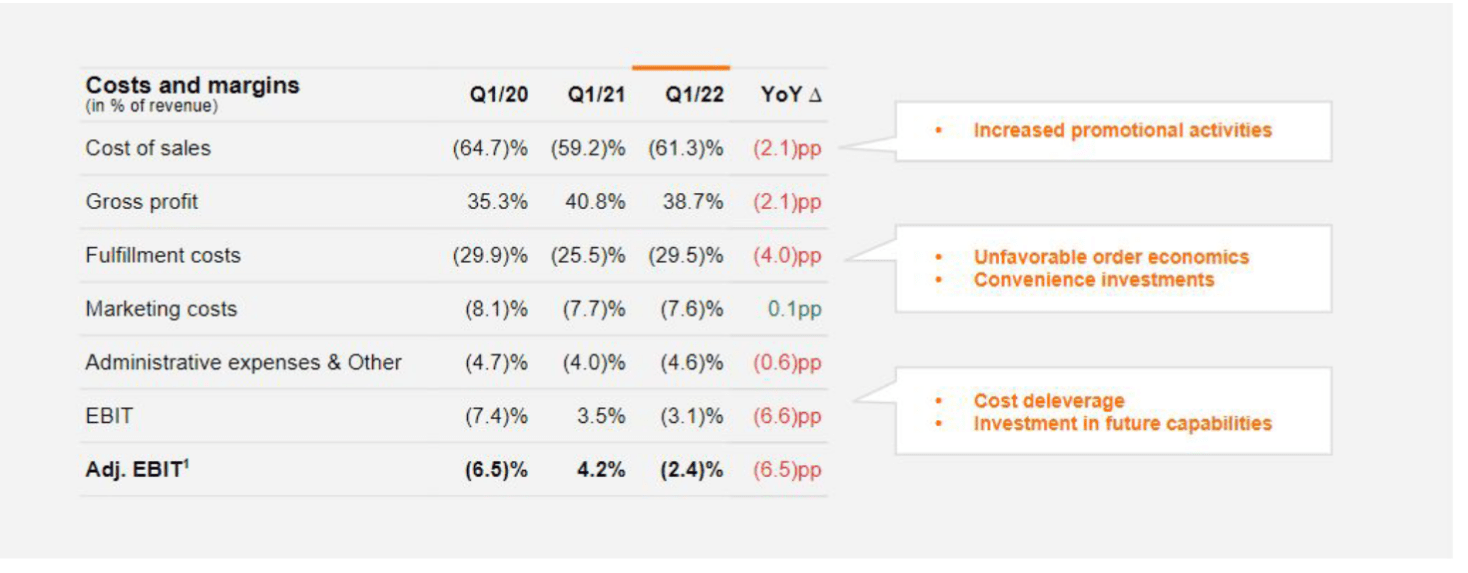

In Q2 2022 the company experienced 0% YoY gross merchandise volume growth, which is not terrible considering the harsh economic environment. As Zalando is targeting a 20% CAGR in the coming years it is possible that Zalando will not achieve those targets, but the huge growth from the last couple of years can help compensate. Simultaneously the company's adjusted EBIT margin fell from 6.7% to 3%. This justifies the expectation that the profitability of 2022 is set to fall significantly compared to 2021. A big portion of this decrease in profitability is driven by increased fulfilment costs which of course is highly related to the inflationary environment and worker shortage. Zalando management believes it can return to compensate for inflationary impacts by the end of the year but other trends like lower utilization are not offsettable.

{kind=link}

The positives

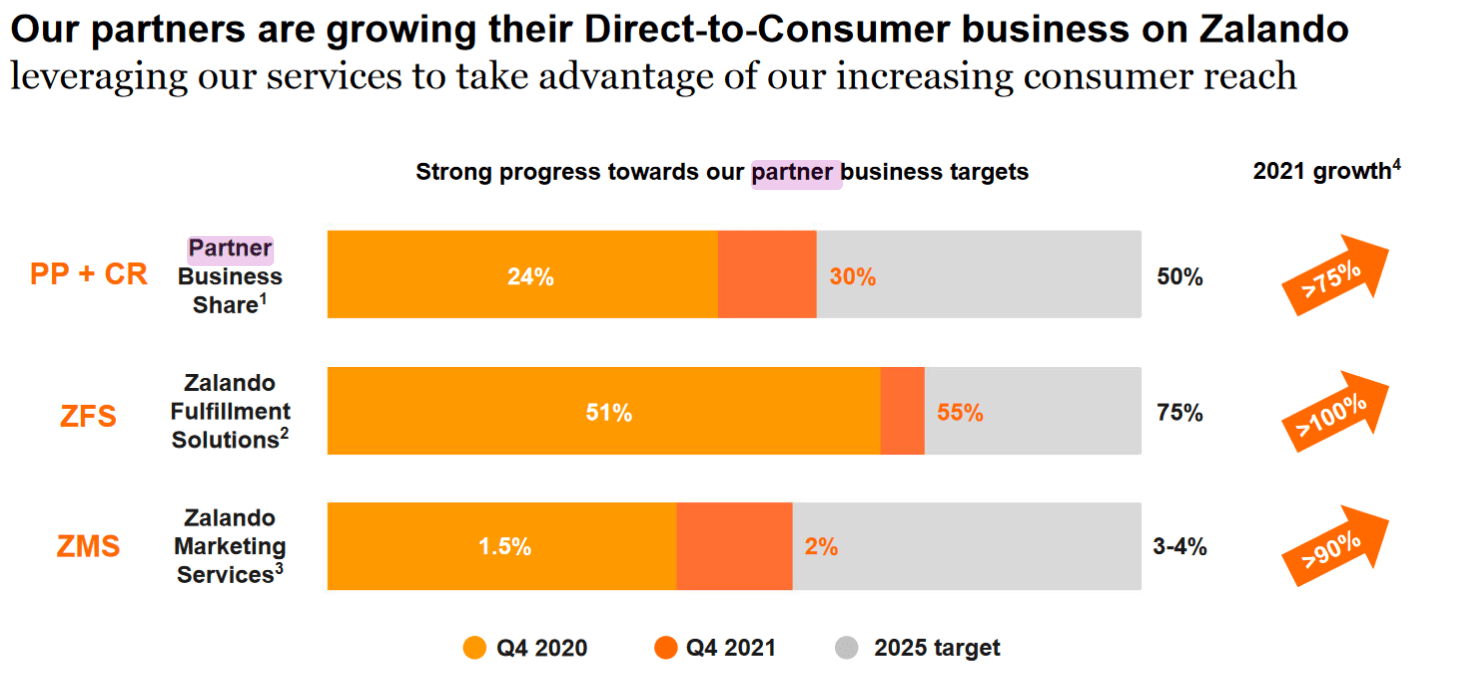

Zalando is transforming into a true platform-based company providing partners with different services like fulfillment and marketing. The current contraction in profitability shows that Zalando is investing its resources in the right areas. The partner business continuously outgrows wholesale while the former is also significantly more profitable. In Q2 2022, the Zalando marketing services grew revenue by 40% YoY while gross merchandise value was flat. Last year in 2021, Zalando's partner services also experienced significantly higher growth rates. Zalando can provide these services at a great price point to its partners due to network effects while simultaneously achieving high returns on invested capital.

{kind=link}

It is also interesting to note that active customers has increased by 11% YoY in Q2 2022. It is clear that Zalando is executing well to achieve its long term goals.

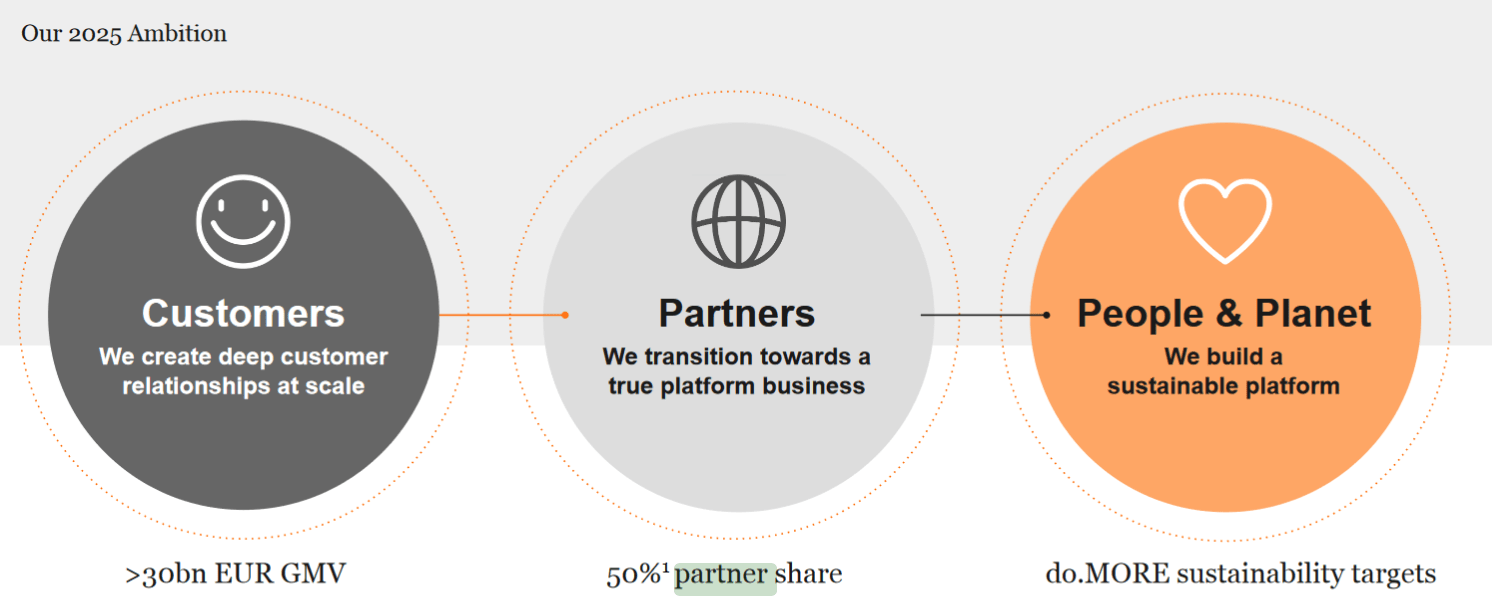

By 2025 Zalando wants to reach €30 billion in gross merchandise value with a 50% partner share. For the partner business Zalando targets an adjusted EBIT margin of 20-25% while the wholesale targets are 6-8%. When doing the math it is clear that the targeted adjusted EBIT amounts to €4.4 billion - which is probably at least €3 billion in real EBIT. It is good to note that the current adjusted EBIT margin is just 5.8% showing that Zalando has a long way to go to achieve its margin goals.

Still, at those targets with an enterprise value of €8.05 billion the EV/EBIT ratio is a meager 2.7. So either these targets are absolutely wrong or the stock is significantly undervalued.

{kind=link}

The problem

The problem is the economic environment in Zalando's markets. Zalando operates in many different countries on the European continent. With interest rates on the rise, a high probability for a recession on the European continent and decreasing e-commerce retail share of total retail sales; everything seems to be turned against Zalando. While Zalando has €1.6 billion in cash and €700 million in receivables, the balance sheet also has €1.7 billion in inventory and €2.3 billion in trade payables. This is the problem with Zalando's wholesale business, when the economy turns sour you are left with an inventory with value that one can question. Zalando has a healthy balance sheet for now but it is clear there's some risk involved if we are going into a deep recession.

Takeaway

Zalando is an interesting stock with a management that is executing well but is negatively impacted by the economic environment. With chances of a European recession being too high it is plausible Zalando will struggle to achieve its profitability goals in the coming years which is not a good sign for the stock.

For further details see:

Zalando Continues To Execute But The Economic Environment Is Problematic