ZLDSF - Zalando: Dominating The Fashion Industry

2023-09-05 22:19:07 ET

Summary

- Zalando has a substantial position in the European e-commerce retail industry, with a high-quality platform and an unrivaled suite of products.

- The company is facing near-term headwinds but is expected to see margin appreciation and growth returning in the medium term.

- The company has an active customer base of over 50m, driving consistent demand for products and a position from which to grow further.

- Zalando's peers are struggling far more, potentially suggesting market share growth despite the declining revenue.

- Zalando's valuation has declined significantly, now reflecting a smaller growth rate. We believe there is upside at this share price.

Investment thesis

Our current investment thesis is:

- Zalando has developed a monopolistic-like position in the e-commerce retail industry within Europe, with a high-quality platform, relationships with the leading global brands, an active customer base in excess of 50m, and scope for low double-digit growth once economic conditions improve. While its competitions struggle heavily, Zalando is ticking along far better.

- The business is facing near-term headwinds but we believe these will subside, allowing the business to see margin appreciation and growth returning.

- The company is attractively valued when compared to its historical averaging, implying the forecast growth and margin improvement has be re-rated to a more reasonable level.

Company description

Zalando SE ( ZLNDY ) is Europe's leading online fashion platform, headquartered in Berlin, Germany. It offers a wide range of fashion and lifestyle products, including clothing, footwear, accessories, and beauty products, from various international and local brands.

Share price

Zalando's share price has disappointed, having rallied post-pandemic to over 240% gains. This underperformance is due to a change in investor sentiment, with the outlook of the business changing negatively.

Financial analysis

Zalando financials (Capital IQ)

{kind=link}

Presented above is Zalando's financial performance for the last decade.

Revenue & Commercial Factors

Zalando's revenue has grown at an impressive rate in the last 10 years, with a CAGR of 20%. During this period, growth has fallen below 20% once, in 2022, with this continuing into LTM.

Business Model

Zalando's business model is based on a two-sided platform approach. It connects customers with fashion brands and retailers, providing them with a digital marketplace to showcase and sell their products. The company operates both an online fashion store and a partner program, where brands can access Zalando's customer base and logistics network.

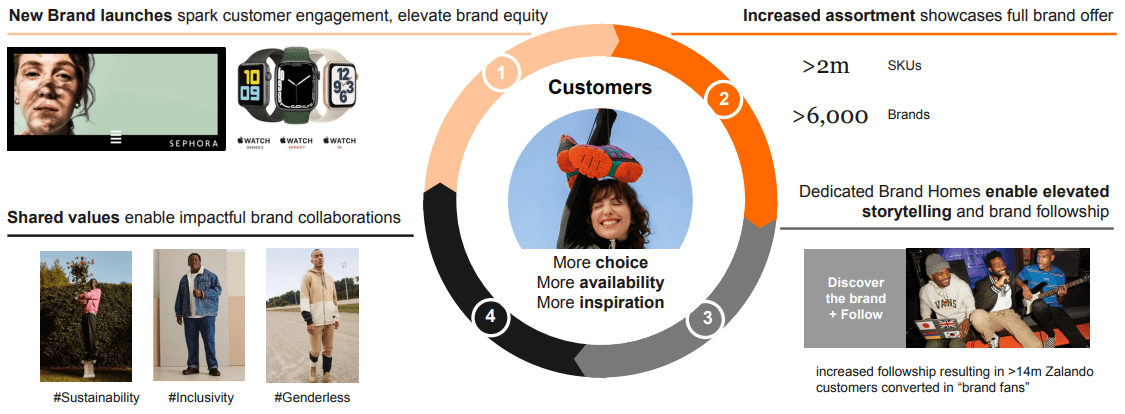

A key selling point for the business is Zalando's extensive product assortment, which sets it apart from many other e-commerce platforms. Zalando offers products from a broad range of brands, from affordable to high-end, catering to various customer segments and product categories. The company currently boasts over 2m SKUs and 6000+ brands, with regular new releases. The value proposition for an e-commerce retailer relative to the wider market is choice and convenience, with convenience being the more homogenized characteristic among peers.

{kind=link}

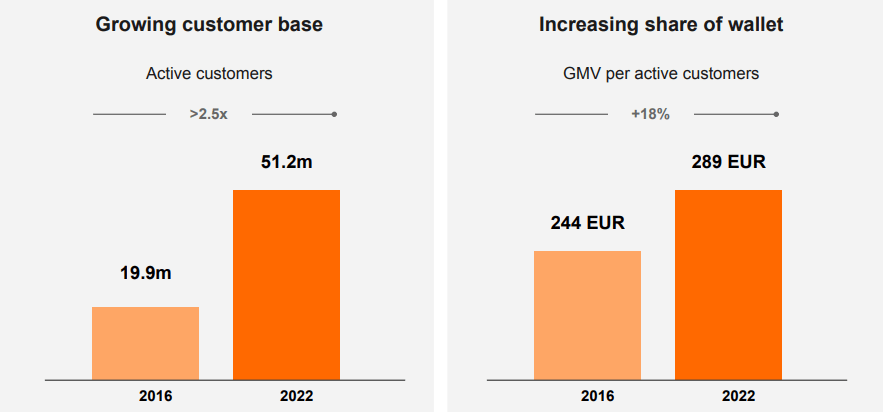

Zalando places a strong emphasis on providing an excellent customer experience, having invested heavily in its website and app. Its platform provides personalized product recommendations based on user behavior and preferences, provides a seamless purchasing experience, and offers enhanced benefits such as 100 days returns and free delivery. This customer-centric focus has helped build customer loyalty and encourages repeat purchases. The number of active customers reached 51.2m in 2022, an impressive growth trajectory. GMV growth per active customer has been less impressive but when considered in conjunction with active customers, it is strong.

{kind=link}

A particular characteristic of Zalando's platform we like is its curation of outfits. The business is rare in that it places a heavy emphasis on displaying outfits with easy access to every component. This encourages consumers to purchase beyond just the piece they are looking for. Further, many consumers are shopping around for products without necessarily knowing what they are looking for. Being able to search for "Streetwear" allows consumers to narrow down their search across products.

Zalando collaborates with fashion brands and designers to offer exclusive collections and limited-edition items. Zalando's impressive access to consumers affords the business a luxury position, allowing it to bargain for these collections that will inevitably drive traffic to its platform through hype. The Highsnobiety collaboration (a business they have acquired a majority stake in) contributed to over 7.1m impressions, with a 3x click-through rate.

Zalando x Highsnobiety (Zalando)

Operationally, Zalando employs a hybrid inventory model, where it maintains its own inventory on-premise while also partnering with various brands that use Zalando's platform for distribution. This combination allows the company to offer a broader product range (a critical success factor) without bearing the full costs and risks associated with holding vast inventories. This keeps the company's operations leaner than its peers. Again, this advantage is only afforded to Zalando due to its size, as no one wants to hold inventory voluntarily.

Zalando's growth has been fueled by its expansion into new markets. The company began in Germany and then gradually expanded into other European countries, benefiting from similar cultures and market conditions. Zalando is now the largest business in Europe by far, giving it a springboard to further expand if deemed possible.

Market share (Zalando)

Zalando faces competition from various online fashion retailers, both regionally and globally. Key competitors include ASOS plc ( ASOMF ), Amazon Fashion ( AMZN ), boohoo group plc ( BHHOF ), H & M ( HNNMY ), Inditex ( IDEXY ), TJX ( TJX ), Farfetch ( FTCH ), and Foot Locker ( FL ). Our view is that Zalando is performing extremely well relative to this peer group.

Its key competitive advantages over the industry are its product choice, high-quality platform, active customer base, and brand relationships. This affords the business a good barriers to entry in an industry where it is incredibly difficult to develop.

Economic & External Consideration

Current economic conditions are defined by high inflation and elevated interest rates. Europe in particular has been hit hard by this, with its dependency on Russian oil biting heavily. This has impacted the company in the following ways:

- Consumer Spending. The combination of these two factors is deteriorating consumers' finances, discouraging discretionary spending while finances are focused on living costs. This has hit Zalando hard, with FY22 growth grinding to a halt and this continuing into the LTM period (-2.5% growth in Q2'23). Despite discounting activities, the business has been unable to stem the decline.

- Input Costs. Rising inflation is also impacting the company operationally, with a rise in logistics costs. GPM has declined to 39%, illustrating a combination of this and greater discounting.

We expect conditions to remain difficult in the coming 6-12 months, as inflation continues its slow decline. This suggests Zalando faces a difficult period ahead, although its peers are suffering far more, just see the situation over at ASOS. Net, Zalando could exit this bear period with greater market share.

Margins

Zalando has low margins, reflecting its position as a middleman responsible for driving sales. During the historical period, its margins have lacked material improvement despite growth in scale, a disappointing development in our view.

The business has a strong GPM at 39%, suggesting the scope for operating cost leverage is high, yet this has not been the case. This implies the cost of acquiring customers is not something it can materially reduce.

Once economic conditions improve, we believe the business can normalize at a 5-7% EBITDA-M level, although likely closer to the lower end.

Balance sheet & Cash Flows

Zalando's inventory turnover remains below its pre-pandemic level, suggesting operational weakness in response to the changing demand conditions currently. We expect inventory to unwind during the year, allowing for an improvement in cash flow. This could mean greater discounting activities to move this stock, however, leading to further margin erosion.

Industry analysis

Apparel Retail (Seeking Alpha)

{kind=link}

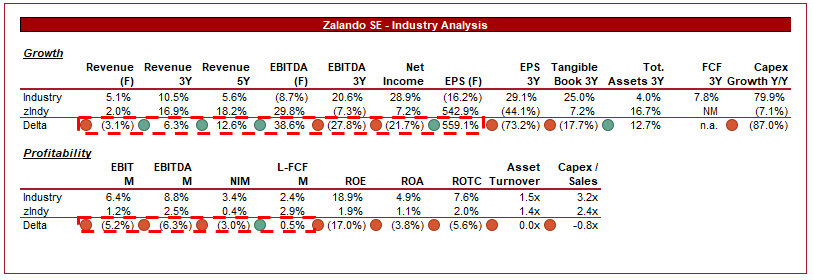

Presented above is a comparison of Zalando's growth and profitability to the average of its industry, as defined by Seeking Alpha (34 companies).

Zalando's performance is good in our view. Its growth outperforms the market, reflecting its focus on growth thus far, allowing for scale. Slightly unusually, growth is expected to match the industry on a forward basis (When excl. a single outlier), implying it is overly exposed to the slowdown. Margins are the company's area of weakness, although the gap at a FCF level is surprisingly good.

If Zalando can achieve the margin improvement we expect in the coming years, the business will be well-placed to warrant a premium valuation.

Valuation

{kind=link}

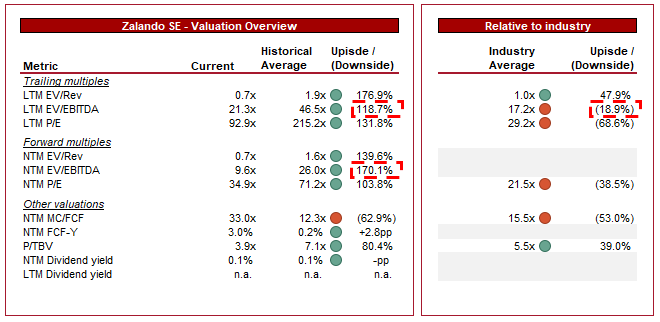

Zalando is currently trading at 21x LTM EBITDA and 10x NTM EBITDA. This is a discount to its historical average.

A discount to the company's historical average is undoubtedly warranted. The company was expected to continue its strong growth trajectory, alongside achieving margin improvement, neither of which has occurred. On an NTM basis, we believe the valuation reflects a substantially slower growth and margin trajectory, with an NTM FCF yield of 3% representing an attractive entry point.

Zalando's valuation relative to its peers looks messy. This is due to significant disruption in the industry, with valuations all over the place. We do not place too much stock in this metric currently.

Based on the historical analysis, we believe Zalando is within range of being attractively priced, although its share price may struggle in the near term.

Final thoughts

Zalando is a quality business. The retail industry needs a premier e-commerce offering that brings together the leading brands in the affordable-to-high-end segment. Zalando is just that business for Europe. It has a dominant position and thus scope for growth in line with the industry (although better in the medium-term), and should see some margin improvement from this.

Current economic conditions are battering the business, but also its peers. Zalando is positioned well to navigate this, and is doing so far better than ASOS and Boohoo.

Zalando is undervalued in our view, with an NTM EBITDA multiple of 10x while still having scope for double-digit growth once conditions improve. While its FCF yield is a good entry and economic conditions remain difficult, we do not consider it above a soft buy. We believe investors could do well slowly accumulating a position in this stock over a 12 month period.

For further details see:

Zalando: Dominating The Fashion Industry