ZLDSF - Zalando: Still Waiting For A Better Entry Price

2023-03-20 05:10:46 ET

Summary

- Zalando reported solid Q4 results, comfortably topping consensus estimates with regard to both sales and earnings.

- With financial discipline and profitability becoming more and more of a priority, the e-commerce giant has guided for a solid 2023 outlook.

- Zalando is slowly but surely transitioning from a high-growth company with a focus on topline expansion to a mature business focused on profitability.

- Although I slightly raise my EPS expectations through 2025 to account for stronger profitability, I estimate close to 20% downside risk based on a EUR 31.78/share target price.

Thesis

Quite some time passed since I have last covered Zalando ( OTCPK:ZLDSF ) ( OTCPK:ZLNDY ), and argued that investors should wait for a 'dip' opportunity to buy stock of the German fashion e-retailer. However, since my argument was made, Zalando has not dipped, but slightly increases (up about 10%). Thus, even though Zalando has delivered better than expected FY 2022 results , ZLDSF's valuation expansion has kept pace with the fundamentals, leaving little room for an attractive risk/ reward repricing trade.

According to my valuation model, I continue to see the valuation risk slightly skewed to the downside (about 20% overvaluation). And thus, I reiterate a "Hold" recommendation.

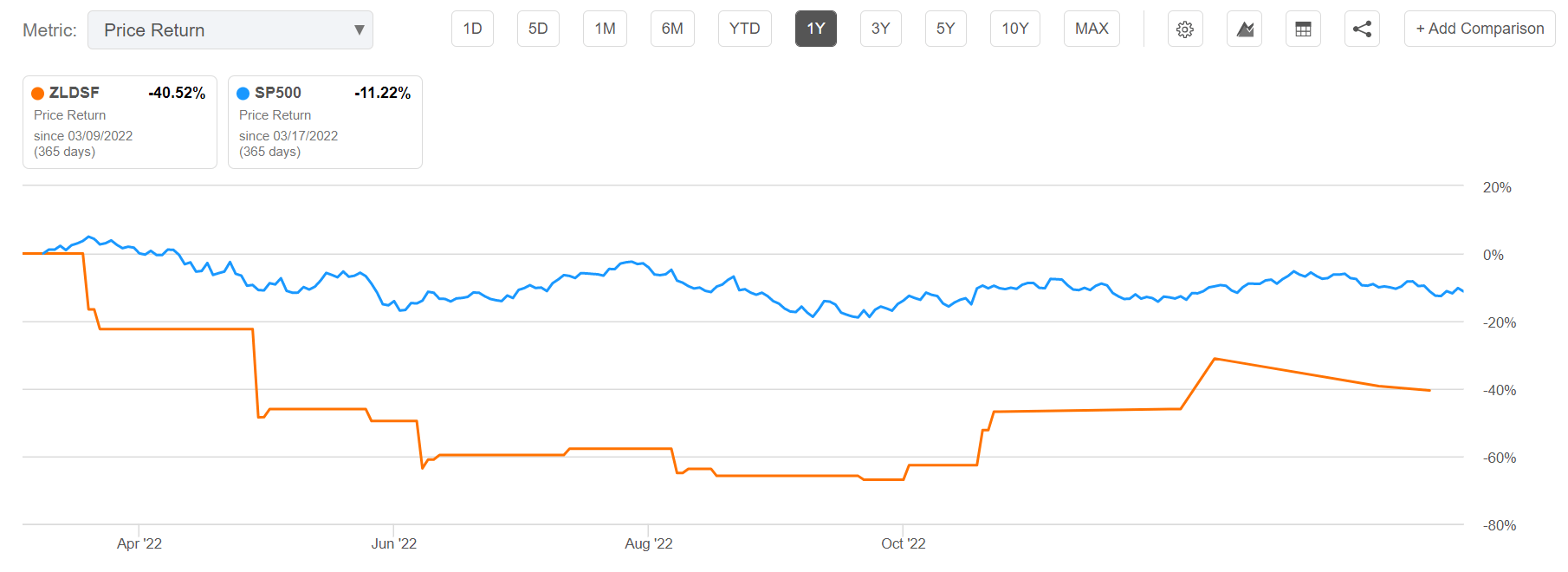

For reference, Zalando stock is down approximately 40% for the past twelve months, as compared to a loss of about 11% for the S&P 500 ( SPY ).

{kind=link}

Zalando Beats FY 2022 Earnings Estimates

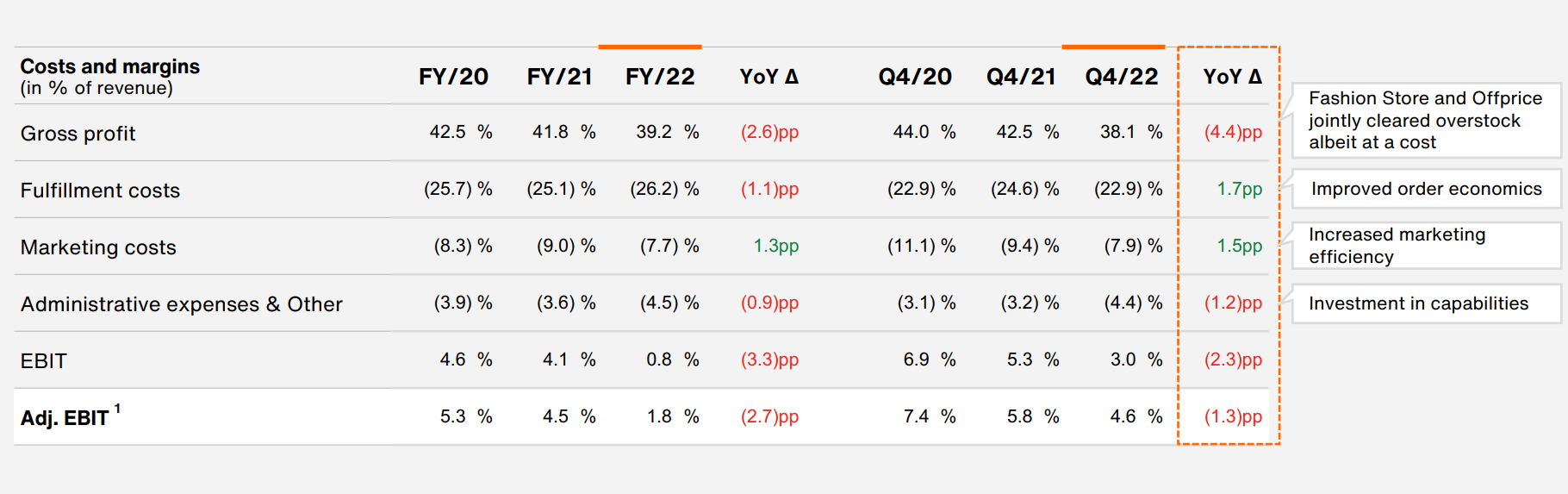

Zalando reported solid Q4 results, comfortably topping consensus estimates with regards to both sales and earnings. During the period from September to end of December, Zalando generated group revenues of about EUR 3.2 billion, an increase of close to 2% as compared to the same year prior, and about EUR 30 million above analyst consensus estimates (according to data collected by Bloomberg). The e-commerce giant's gross merchandise volume increased by about 5%, to EUR 4.6 billion as of December 2022, and the number of active customers grew by about 6%, to over 51 million respectively.

Although Zalando's topline metrics expanded nicely in Q4 2022, profitability growth failed to keep pace: Zalando's gross profit margin in Q4 FY 2022 versus Q4 FY 2021 contracted by approximately 440 basispoints, to 38.1%. And as a consequence, despite an improvement in operating cost efficiency, Zalando's adjusted Q4 FY 2022 EBIT fell to EUR 146 million, down nearly 20% year over year. However, profitability came in better than expected, as analysts estimated EBIT closer to EUR 100 million.

{kind=link}

Zalando management is well aware that profitability remains a key consideration for investors. With that frame of reference, Chief Financial Officer Sandra Dembeck said in a statement that:

the challenges of 2022 demanded us to be laser-focused on profitable growth

...and added that:

[management] acted quickly and decisively with measures that improved margins such as the introduction of minimum order values

Furthermore, only recently (late February 2022), Zalando has voiced plans to cut 'several hundred' jobs, arguing that some parts of the organization have expanded too aggressively and too quickly. While management has not yet given further insights on the job cuts, I expect cuts could match the '10% of workforce' reference that many high-growth companies have communicated in the past few months. (Zalando had about 17,000 employees as of December 2022)

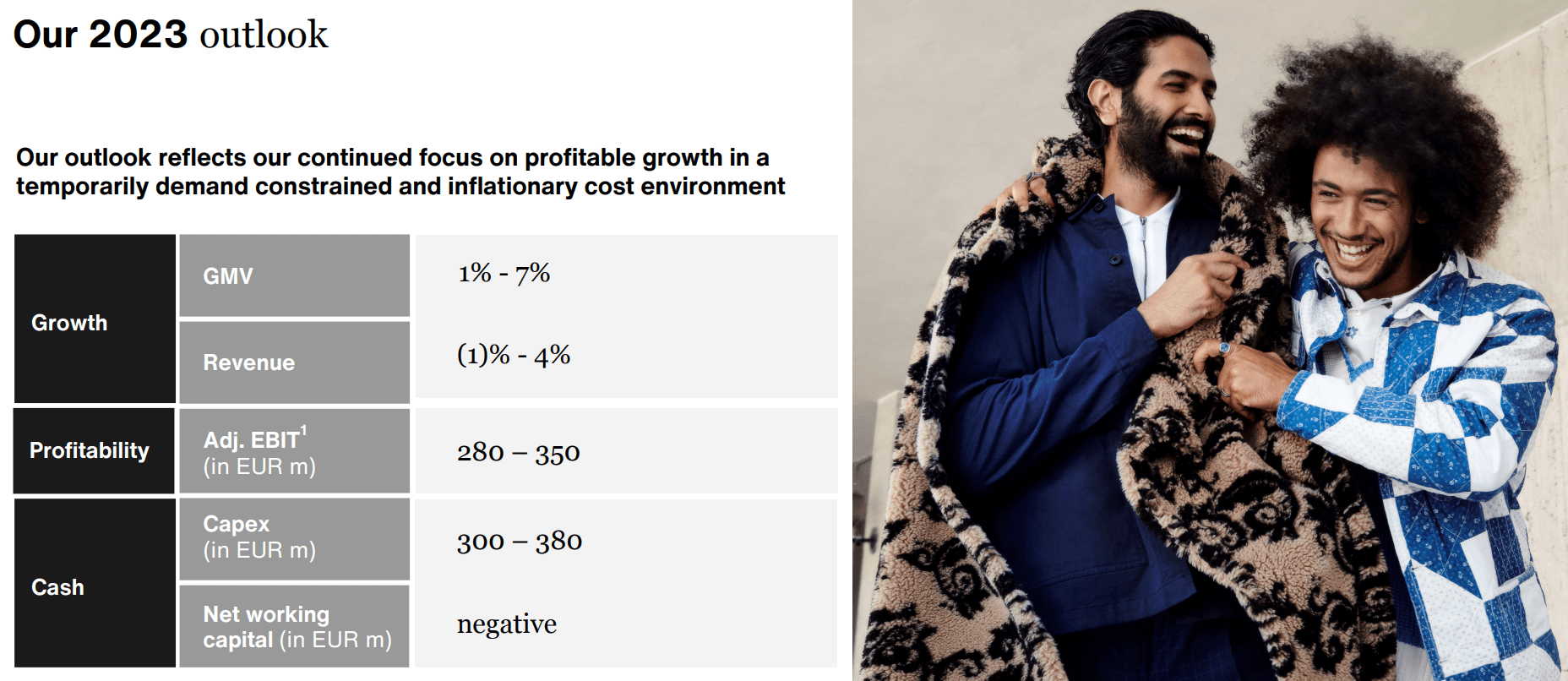

With financial discipline and profitability becoming more and more of a priority, Zalando has guided for a solid 2023 outlook. According to the latest management estimates, FY 2023 gross merchandise volume could grow by anywhere between 1% - 7%, with a consequential revenue expansion of (1)% and 4%.

{kind=link}

Valuation Update

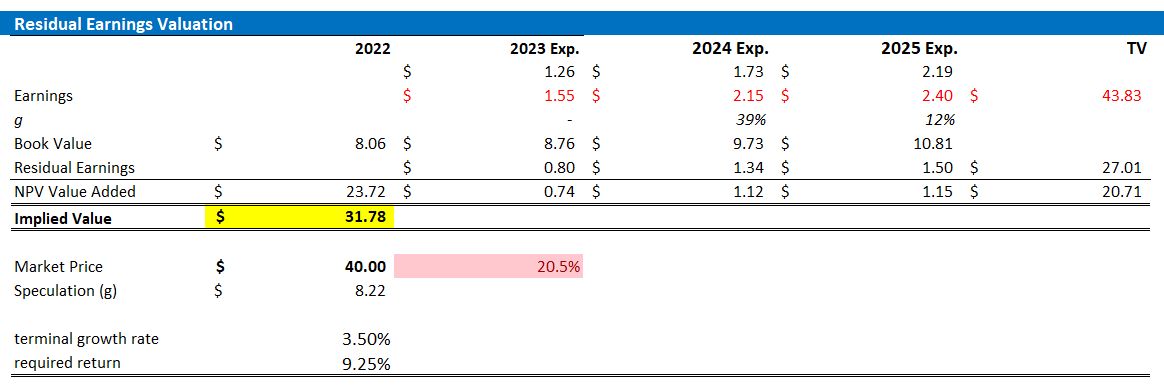

As Zalando will likely continue to focus on operating discipline and profitability expansion, I update my EPS expectations for the e-retailer through 2025. I estimate that Zalando's EPS in 2023 will likely expand to somewhere between $1.5 and $1.6 (estimate also reflects management guidance). Moreover, I also raise my EPS expectations for 2024 and 2025, to $2.15 and $2.4 respectively.

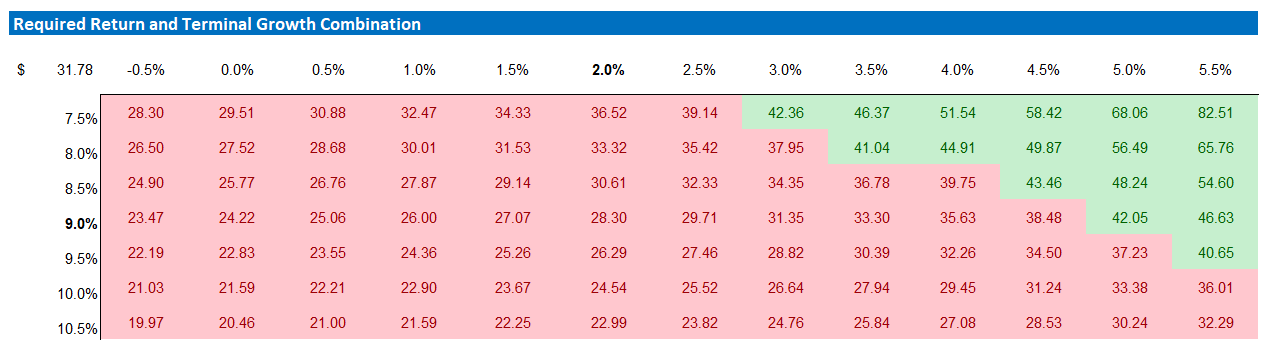

I continue to anchor on a 3.5% terminal growth rate (one percentage point higher than estimated nominal global GDP growth), but I raise my cost of equity requirement by 75 basis points, to 9.25% (to reflect structurally higher risk premia for equity investments across the world).

Given the EPS updates as highlighted below, I now calculate a fair implied share price of $31.78.

Author's EPS Estimates; Author's Calculation

{kind=link}

Below is also the updated sensitivity table.

Author's EPS Estimates; Author's Calculation

{kind=link}

Risks

As I see it, there has been no major risk-updated since I have last covered Zalando stock. Thus, I would like to highlight what I have written before:

Investors in Zalando should note the following downside risks: First, macro-economic challenges including supply-chain issues, rising real yields and inflation negatively affect Zalando's business operation. Second, the probability that Europe will see a recession sometime in the next weeks is elevated. That said, if consumer sentiment decreases considerably, Zalando's topline sales will reflect the slowdown. Third, the fashion market, especially in Europe, is highly competitive. There are many online shops competing for the same customer-base and increased competition may pressure Zalando's margins and market shares. Forth, overconfidence and overexpansion might be a potential risk for successful growth companies such as Zalando. If the company starts to seek growth in relatively unknown international markets, the expansion may turn out unsuccessful and/or more costly than expected.

Conclusion

As management guidance for 2023 indicates, Zalando is slowly but surely transitioning from a high-growth company with focus on topline expansion to a mature business focused on profitability. While I see potential for Zalando to cut costs, I would appreciate more transparency--or results--with regards to how Zalando management expects to justify the firm's rich valuation (x27 FWD EV/EBIT ). For the conservative investor, Zalando shares look overvalued. Although I slightly raise my EPS expectations through 2025 to account for stronger profitability, I estimate close to 20% downside risk based on a EUR 31.78/share target price. I reiterate a HOLD recommendation for ZLDSF stock.

For further details see:

Zalando: Still Waiting For A Better Entry Price