PUMSY - Zalando: Unbelievably Pricey

Summary

- The German online retailer Zalando has seen a fast price rise over the last quarter. Its financials have shown some improvement too, but that doesn't appear to justify its P/E.

- The P/E is at vertigo-inducing 2,852x, driven more by its fast-shrinking earnings than its performance. With the company not entirely sure of future profits, a correction looks due.

- This is especially so as 2023 is expected to be recessionary for Europe, particularly for its key DACH market.

Since the last time I wrote on Zalando (ZLDSF) in October 2022, the company's price-to-earnings (P/E) ratio has gone from what I then called "eye-popping" at 276x to completely unfathomable. It's now at, wait for this, 2,852x . Yes, that's four digits, you read that right. With multiples like these, it would be expected that ZLDSF would be in free fall. It isn't. Far from it, in fact. Since the time of writing last, it's actually up by almost 45%.

This begs the question - What explains this? And importantly, is there anything about the company that indicates that it can sustain this upward momentum?

Some improvement in financials...

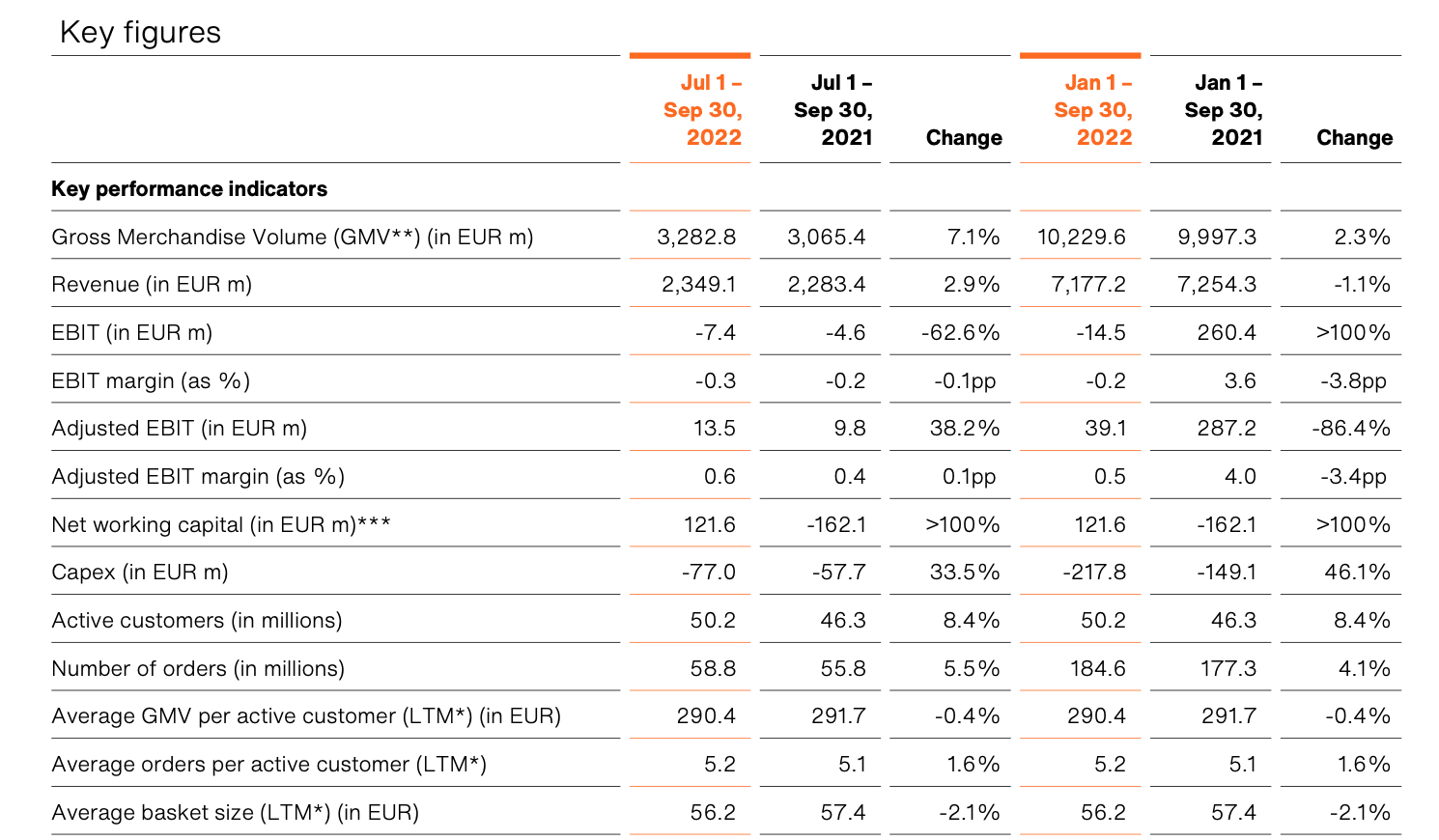

Let's get to the first question. In November, the company released its third-quarter results . Which showed some turnaround in performance. In the second quarter (Q2 2022, April-June, 2022), it reported a 4% year-on-year (YoY) drop in revenue. For the first half of the year (H1 2022), its performance was weak too, with a fall in revenue of 2.9%. But come the third quarter (Q3 2022) and its sales rose again. At 2.9%, it wasn't a substantial increase, but it was an increase nevertheless.

{kind=link}

It incurred operating losses for both the first nine months of the year and in Q3 2022. However, its adjusted operating profit grew significantly by almost 38%. This is because the number excludes the impact of items like share-based payments and acquisition-related payments. As a background, Zalando acquired Berlin-based Highsnobiety , a fashion news and e-commerce platform, earlier last year. The financials of the acquisition are undisclosed, but going by the company's latest income statement, a guess can be made.

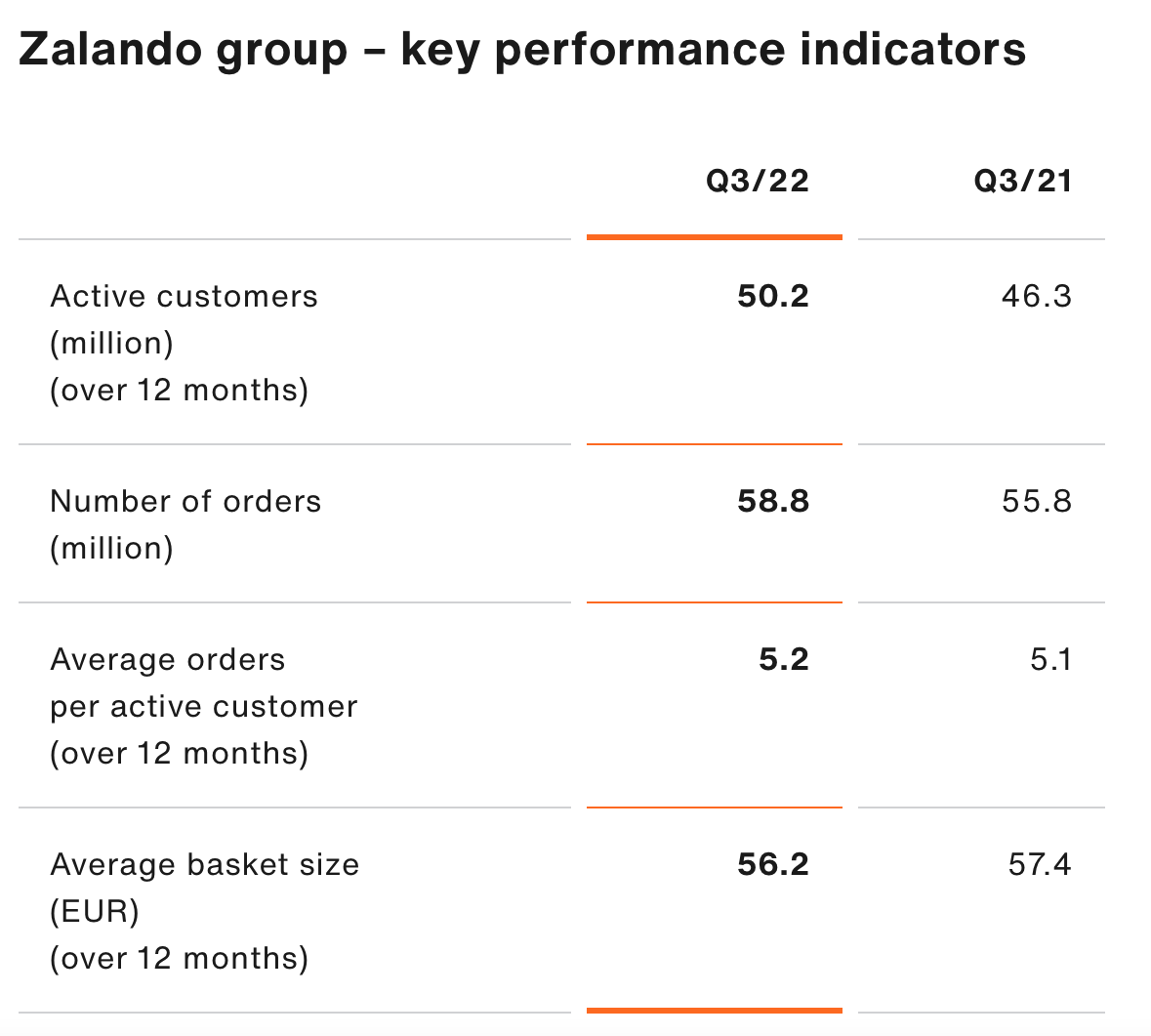

The company also reported a rise in the number of active customers, which surpassed 50 million for the first time in the quarter. Other metrics like the number of orders and average orders per active customer also rose, though the average basket size declined, as is understandable in the inflationary environment we face (see chart below).

{kind=link}

Zalando also remains relatively upbeat about its 2022 full-year performance, with expected revenue growth of 0-3%. Considering that for the first nine months, its revenue has declined by 1.1%, it clearly expects Q4 2022 to have seen positive revenue growth. It does, however, say that it expects revenue to come in at the lower end of the range.

…but that doesn't match the price rise

This is a definite improvement over its last results, but I'm not sure if it's enough to justify the price rise. It has reported negative net earnings for the first three quarters of 2022, and its earnings per share are just about positive. If they had turned positive in Q3, as I had pointed out the last time, the P/E would have looked more reasonable. But it has instead become even harder to digest now.

It's true that its price is still lower than it was during the highs of early 2020. But then its trailing twelve months [TTM] income is significantly lower than it was then too. Another way to look at Zalando is to consider its price-to-sales (P/S) ratio. After all, its TTM revenues are 58% higher than they were at the end of 2019. From this perspective, it looks a bit more reasonable at 1.1x, which isn't much higher than 0.9x for the consumer discretionary sector. But I can think of more than one consumer discretionary stock or ADR that's growing way faster and is still trading at reasonable valuations.

A case in point is Puma ( OTCPK:PMMAF ), which I just covered . It's growing fast, reporting profits and has a P/S that's exactly the same as Zalando. And even that is a cautious buy according to me, going by the two pressures of sustained high inflation and a recessionary environment expected in 2023.

Risks ahead

To be fair, Zalando has done a good job of keeping costs down. For Q3 2022, for instance, its cost of sales is up by just 2.4% and the number is even lower for the nine months at sub-2%. If inflation starts declining meaningfully in the next few months, its numbers could look better.

But the recession does remain a huge risk. The DACH markets, which comprise Germany, Austria and Switzerland, make up 39% of its revenues and saw a small decline in Q3 2022. The rest of Europe did better, with a 3.1% revenue growth, but it doesn't seem enough. Germany, the biggest European economy, is expected to enter a recession this year, which could be a drag on Zalando.

What next?

In light of this, the sharp run-up in price is even harder to reconcile. There could be positive effects from the acquisition of Highsnobiety down the line, but it remains to be seen how much of a contribution that makes. It's also possible that it returns to profits as it continues to reduce costs. It also makes a reassuring statement in its quarterly release statement that "Zalando continues to be laser-focused on protecting profitability.". To this extent, it has undertaken initiatives like minimum delivery size, or else the customer pays a delivery fee, making below-minimum size orders profitable now.

Looking at the company in totality, though, I am tending towards a Sell on it now. Its price run-up would have earned a nice stash for anyone who bought it when it was in the dumps. But holding on to it, for now, is risky. If it hadn't risen this fast, it would still be a Hold.

It's hard to see it as sustaining its current multiples at a time when it isn't exactly confident of how the future will work out. Its CFO, Sandra Dembeck says, "With consumer confidence at new lows and ongoing inflation, it was a prudent decision to start early with decisive action and measures to support profitability…". In other words, it's possible that profits will continue to suffer. I haven't bought the stock, and as of now, I would steer clear of it. It's better to wait for a real improvement in its financials, which matches its long-term performance, or for its price to decline from its current levels.

For further details see:

Zalando: Unbelievably Pricey