HON - Zebra: Post Mortem Of Why My Investment Thesis Broke (Rating Downgrade)

2023-10-07 11:00:51 ET

Summary

- I was invested into Zebra Technologies for over a year but recently sold at a 5% loss at $306 per share.

- I made a couple of mistakes, most notably ignoring the cyclicality of the business.

- Fundamentals deteriorated quickly, but the company remains a good business.

- At its current valuation, it is not unreasonably priced.

As some of you may know, Zebra Technologies (ZBRA) has been a part of my personal portfolio for over a year. Still, in my recent efforts to concentrate my portfolio on my best ideas, I decided to sell out of the company on July 10th at $306 per share or a 5% loss. In this article, I'll reflect on my mistakes in analyzing Zebra and what I expect from the company in the future. While I sold the company, I still want to follow it as it is a high-quality company. It is always challenging to admit mistakes, but being open about them is a vital part of investing.

This is not my first Post Mortem; check out my others and what I learned from them:

- Teladoc (TDOC) Post Mortem

- Adobe (ADBE) Post Mortem

My initial thesis

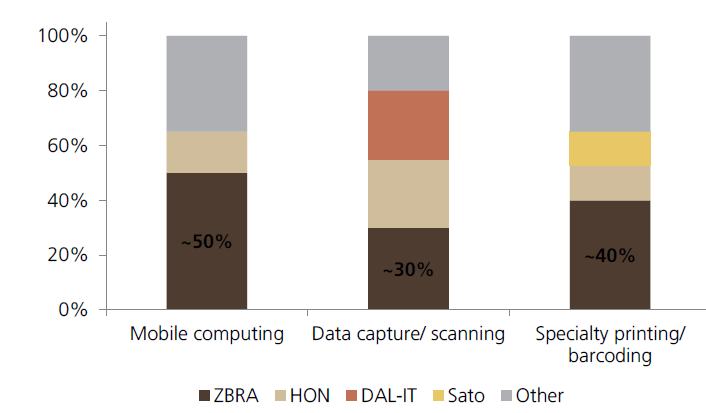

I first covered Zebra Technologies on Seeking Alpha in May 2022 and bought my first shares around the same time. I was drawn to the stock by a good long-term tailwind from the warehouse automation and machine vision markets. These are growth opportunities for Zebra. Furthermore, they have a fantastic market share in mobile computing, data capture/scanning and specialty printing/barcoding, with Honeywell (HON) being the leading competitor.

{kind=link}

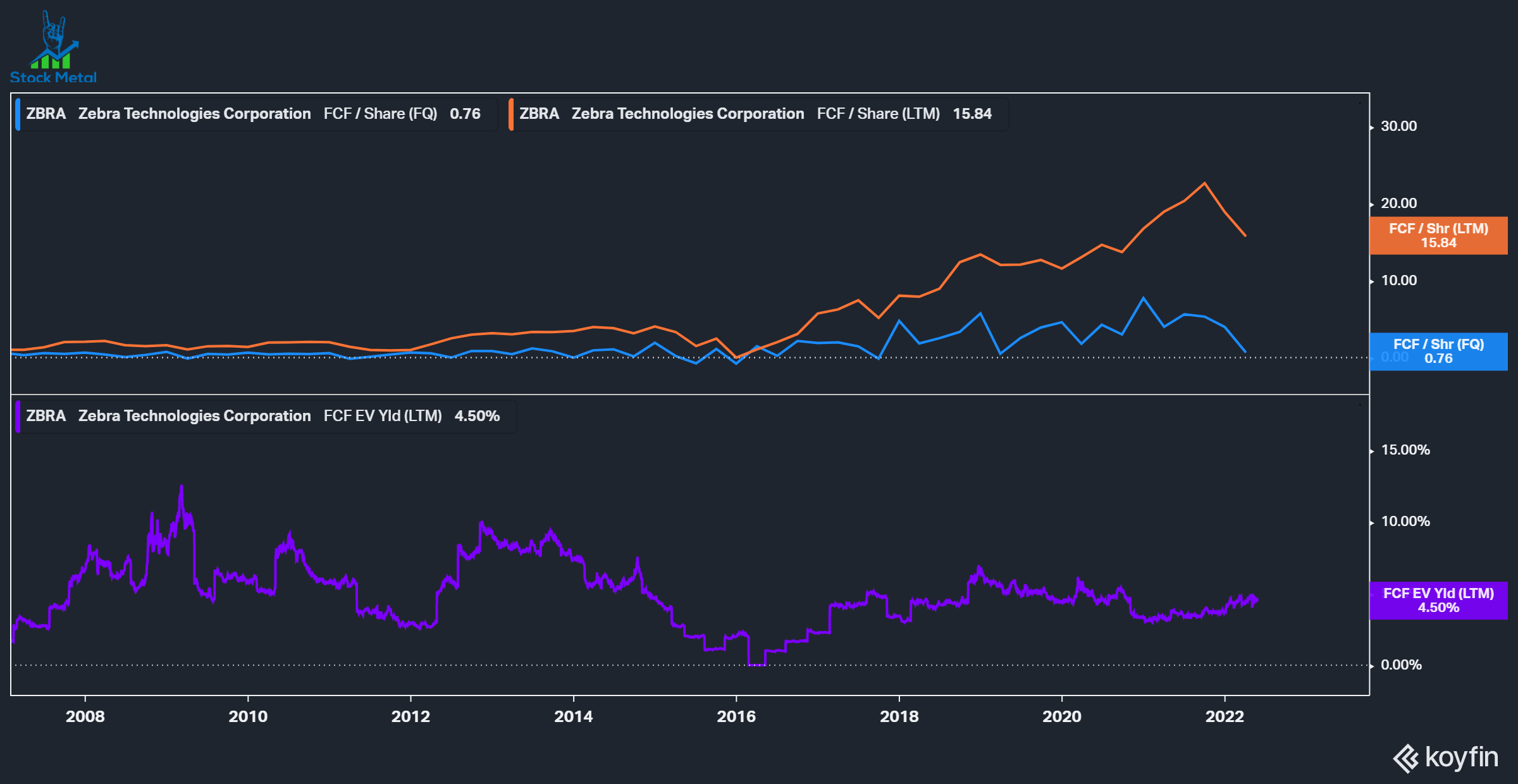

I was drawn to the excellent development of Free cash flows, but even back in 2022, we could see that Zebra was past its peak. Margins were broadly consistent, but the capital allocation looked very good: Priority in internal investments or acquisitions meeting internal hurdle rates to increase the product portfolio, with a 1.5-2.5 times leverage and opportunistic share buybacks. Returns on Capital were at 15%, a good value. The stock traded at 15 times forward earnings and a 4.5% FCF yield, while I expected FCF growth to continue at a teens rate. In hindsight , that was way too optimistic and didn't consider the associated risks.

{kind=link}

Where it went wrong

Cyclicality

In my whole write-up and personal notes, I did not mention the cyclicality of being heavily exposed to retail and industrial customers. Over the last decade, we saw a good economic environment and Zebra grew well, but in 2022, fundamentals started to deteriorate. Zebra primarily sells to distributors, with three main distributors accounting for 50% of sales. This leaves them very vulnerable to destocking after inventory was rushed during the pandemic.

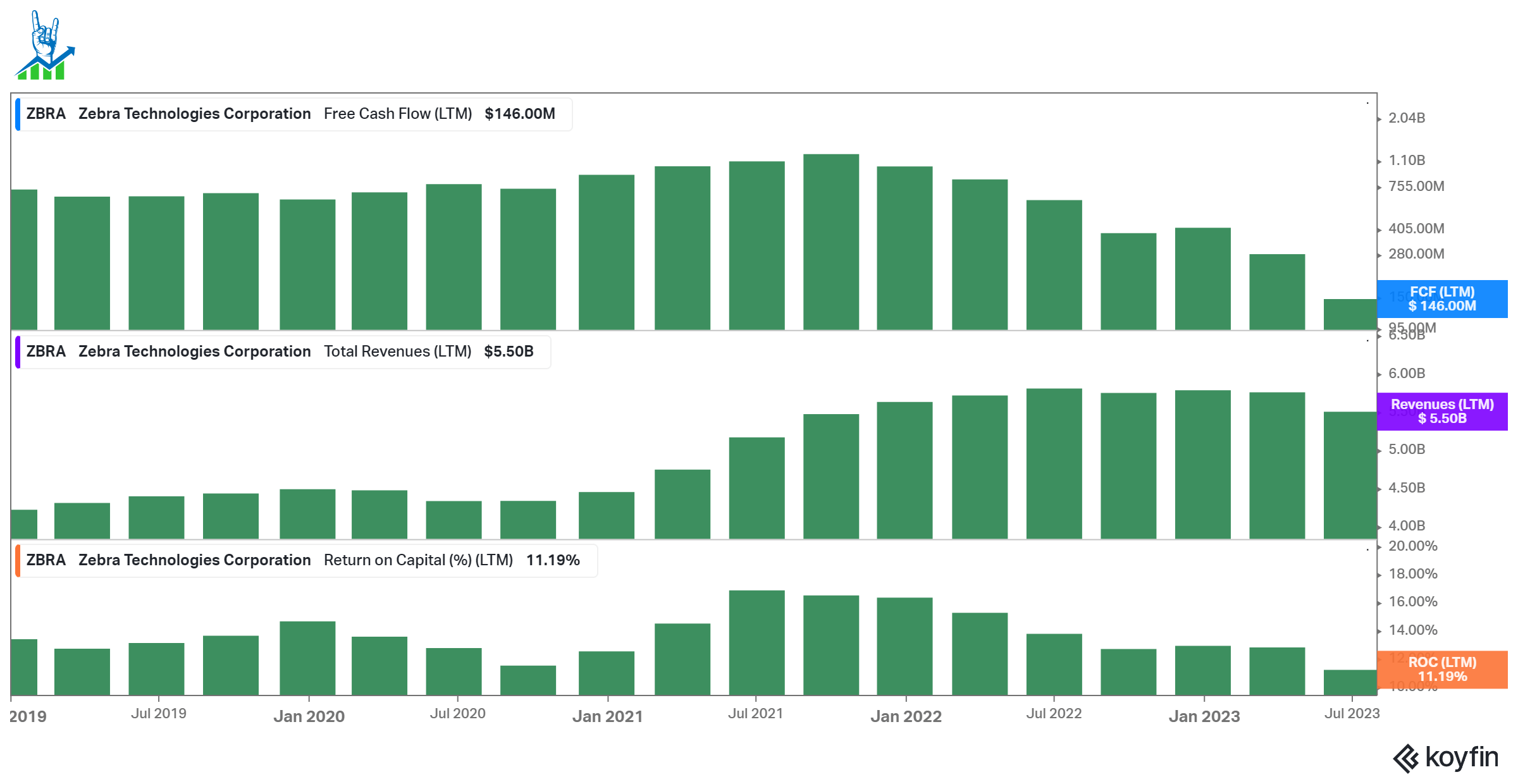

We can see that free cash flow did not grow but deteriorated quickly. This was primarily attributable to increasing inventory levels, the settlement payments to Honeywell and other working capital changes. However, even after adjusting those, we saw adjusted cash flows plummet to $450 million for the last twelve months. EBIT and gross profit margins stayed consistent with a slight deterioration so that the bull case could be a return to historic cash conversion.

{kind=link}

Improving revenue quality

My bull thesis included the continuous transition from hardware sales to services and software sales. This would counteract cyclicality and make revenues more stable and predictable. While customers might delay buying new devices, they wouldn't stop using the existing ones so quickly. Zebra has more software engineers than hardware engineers, which I liked, but hardware sales account for 79% of revenue. While the sales mix continued to shift, it was not meaningful enough to counteract the cyclical nature of the business. Instead, I decided to put my money into Napco Security ( NSSC ), a company with a similar strategy of improving software sales. Sadly, I added to Napco before it plummeted to an accounting issue . At Napco, recurring sales are growing rapidly and are expected to reach 50% of revenue in the next few years.

Lack of M&A information

Zebra has been quite aggressive with M&A over the last decade, but they hardly share information about the acquisitions' progress. The company only reports in two segments: EVM (Enterprise Visibility and Mobility) and AIT (Asset Intelligence & Tracking). These provide little information and make it hard to see if expensive acquisitions like Matrox work out. I would prefer that investor relations be more transparent with investors, especially as fundamentals deteriorate.

Zebra acquisition history (Aggregated by the author with data from Zebra IR)

Increasing debt

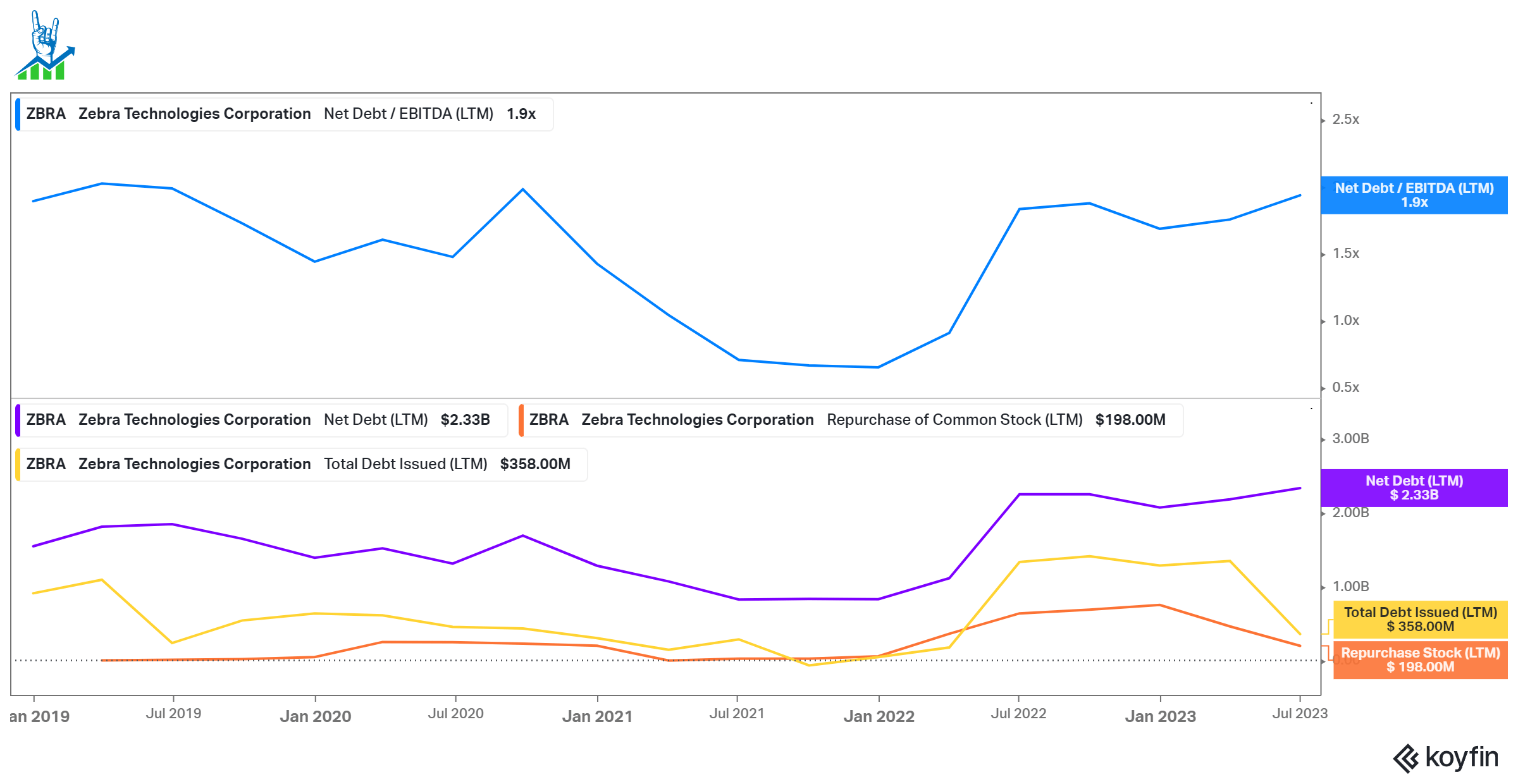

Due to the weakness in cash flows, Zebra had to lever the balance sheet with over a billion in debt taken on since I started my position. The leverage level is still okay at 1.9x, but the company needs to start generating cash flows again to manage it. Much of the borrowed money went into buybacks, which did not go well, while fundamentals deteriorated faster than management expected.

{kind=link}

Deteriorating outlook

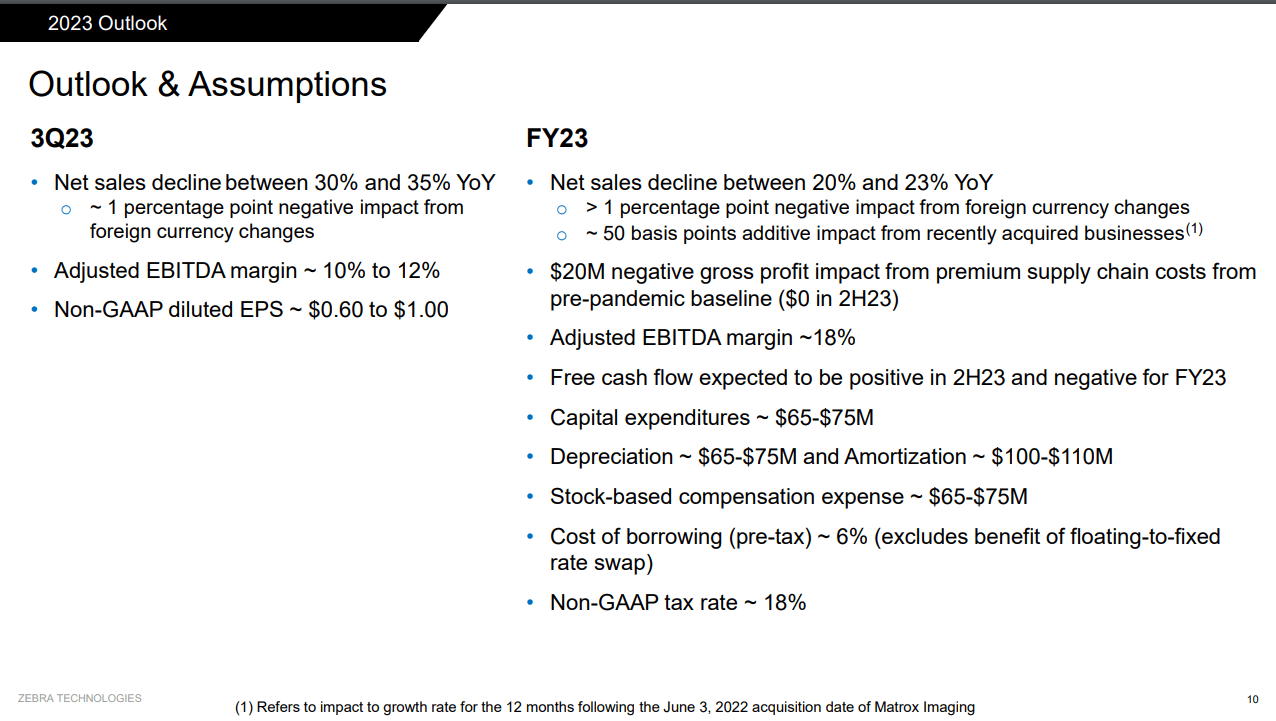

The FY23 outlook for Zebra deteriorated rapidly over recent quarters. In Q4 2022, Zebra guided for FY23 with net sales between -3 and +1% and a 22-23% AEBITDA margin with $650 million in Free Cash Flows for the year. Below, we can see the updated outlook after two quarters. Sales outlook completely collapsed to a 20-23% decline, AEBITDA margin is expected to be 400-500 bps lower and Free cash flow is expected to be negative for the full year. This shows how rapidly and violently fundamentals deteriorated and how bad the cyclicality hit Zebra.

{kind=link}

Valuation is alright

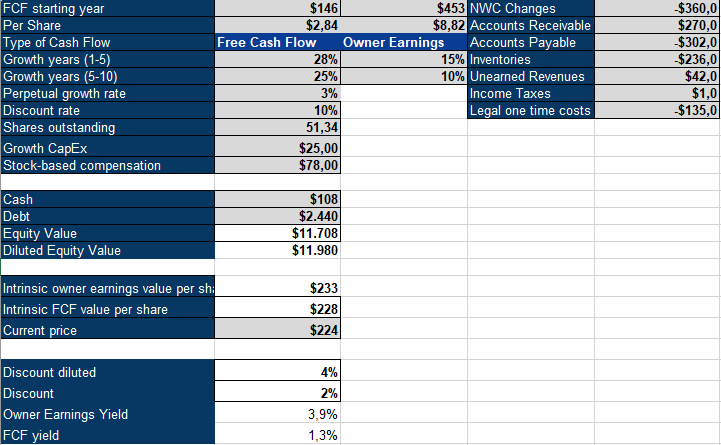

To value Zebra, I'll use an inverse DCF model. I adjusted FCF with net working capital changes and added the settlement payments. This leaves us at $453 million in owner earnings. Zebra would have to grow Owner earnings by 15% over the next five years, followed by 10% the following five years. This does not seem unrealistic if the macro is in their favor again and distributors return to stocking their inventories. I recently started to increase my discount rate on cyclical companies to account for the added risk; I started my investment in Zebra at a 10% discount rate, so I'll keep it for this valuation, but keep in mind that one could be more conservative and use a higher discount rate. I will continue to follow the company from a distance and see how it manages to turn around the fundamentals. I learned a lot from my investment in Zebra and managed to get out with only a 5% loss. I will rate Zebra a hold because it remains a good business.

{kind=link}

For further details see:

Zebra: Post Mortem Of Why My Investment Thesis Broke (Rating Downgrade)