ZGN - Zegna: High-Quality Luxury At A Reasonable Price

2023-11-20 11:10:58 ET

Summary

- Ermenegildo Zegna is an Italian group of luxury companies that benefit from a vertically integrated supply chain and underlying growth.

- The rebranding of Zegna and further reinvesting into Thom Browne offer compelling opportunities for future growth rates, while also containing a higher level of risk than often-cited peers.

- Regarding the upcoming CMD, the company offers an interesting investment opportunity for investors.

Ermenegildo Zegna (ZGN) (in the following referred to as "Zegna") is an Italian-based group of luxury companies built around the Zegna brand under family leadership, currently in its third generation. To expand the company's reach, the family decided to go public in 2021. In retrospect, this proved to be a wise decision given the high demand for luxury goods at the time. Going public also gives us the opportunity to invest in another exciting family luxury business that may offer even higher growth rates than the established French luxury giants.

However, investors have not yet seen the benefits of this opportunity since the IPO, as the share price performance has been negative overall after a rise during the summer. However, compared to the industry, the performance has been fairly stable, allowing investors to enter a position at roughly the same price while the underlying business has continued to perform. In addition, an upcoming Capital Markets Day could boost investor confidence and drive the share price further. Which brings us to the question of whether Zegna is a compelling investment right now.

So let's get started!

Business History

The story of Zegna began in 1910 when founder and namesake Ermenegildo Zegna started his business in Northern Italy with a dream to create the most beautiful and luxurious fabrics in the world. To accomplish this, he specialized in importing the highest quality natural fibers directly from their countries of origin to Italy, in order to export the woven products all over the world.

Ermenegildo Zegna believed that long-term success can only be achieved if industry, people and nature are allowed to prosper in harmony.

[ Born in Oasi ]

Furthermore, this commitment to product quality and regional craftsmanship led the founder to expand what started as a small wool mill in a little Italian village. Under the title "Oasi Zegna", he launched an extensive reforestation project surrounding the mill and several other contributions for the local society. Today, this beautiful natural territory is a great way to tell the story of sustainable and excellent luxury at the Zegna brand, leading all the way to a collection of "Oasi Cashmere".

Oasi Cashmere (Zegna)

I've gone a little further in this case, as Zegna is perhaps less well known to people than the usual names I've already written about here. It also allows us to better understand the origins of the brand and the motivations of the family, and enhance our ability to think about the future of the company.

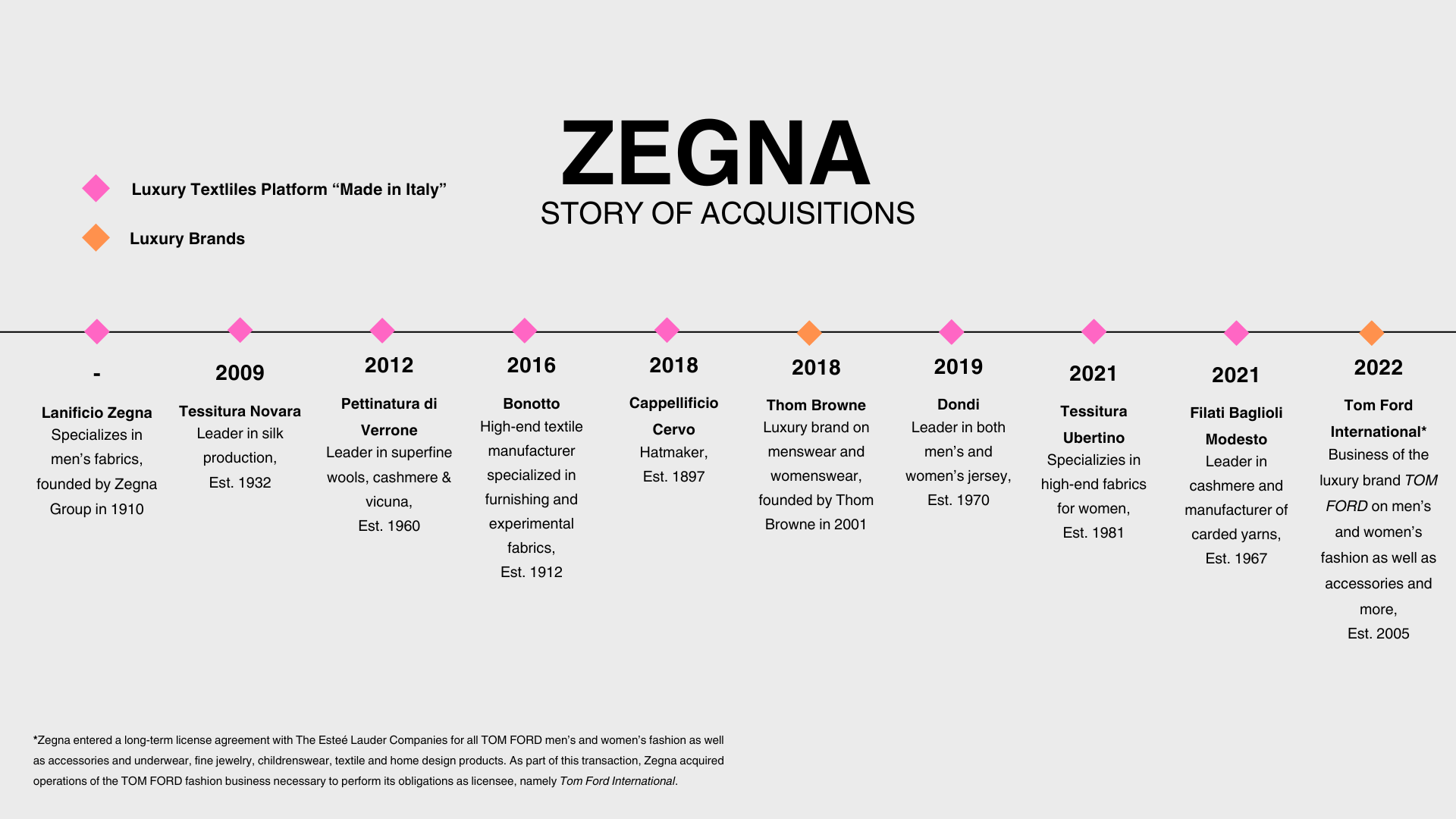

After the next generation had developed the business and expanded geographically and product-wise, Ermenegildo "Gildo" Zegna and Paolo, their sons, initiated a brand extension strategy. This strategy included both organic growth and strategic acquisitions, as well as complete vertical integration of Zegna's supply chain. By acquiring highly specialized, craft-oriented Italian companies, Zegna achieved not only a fully integrated supply chain, but also an attractive contract manufacturer for other luxury fashion brands. But more on that later. First, in order to close the chapter on Zegna's history, I need to comment the other type of acquisitions made in the last 5 years.

In 2018, the company purchased an 85% stake in Thom Browne, a luxury fashion brand based in New York City, for approximately $500 million. The founder and creative director, Thom Browne, retains ownership of the remaining shares. Thom Browne definitely appeals to a younger and less business-oriented clientele than Zegna, which offered the opportunity to reaccelerate the group's growth rates and also to support the relatively small brand with Zegna's manufacturing operations and supply chain network.

The luxury textile platform also enabled the company to finalize the acquisition of Tom Ford's fashion subsidiary in 2022 under a long-term license agreement with Estée Lauder ( EL ). Accordingly, Zegna will manufacture Tom Ford's menswear and womenswear as well as accessories and underwear, fine jewelry, childrenswear, textile and home design products.

Finally, the present structure of Ermenegildo Zegna consists of two fully-owned brands at the helm, backed by a strong manufacturing group and numerous license agreements.

History of Acquisitions (Own Illustration)

{kind=link}

Business Performance

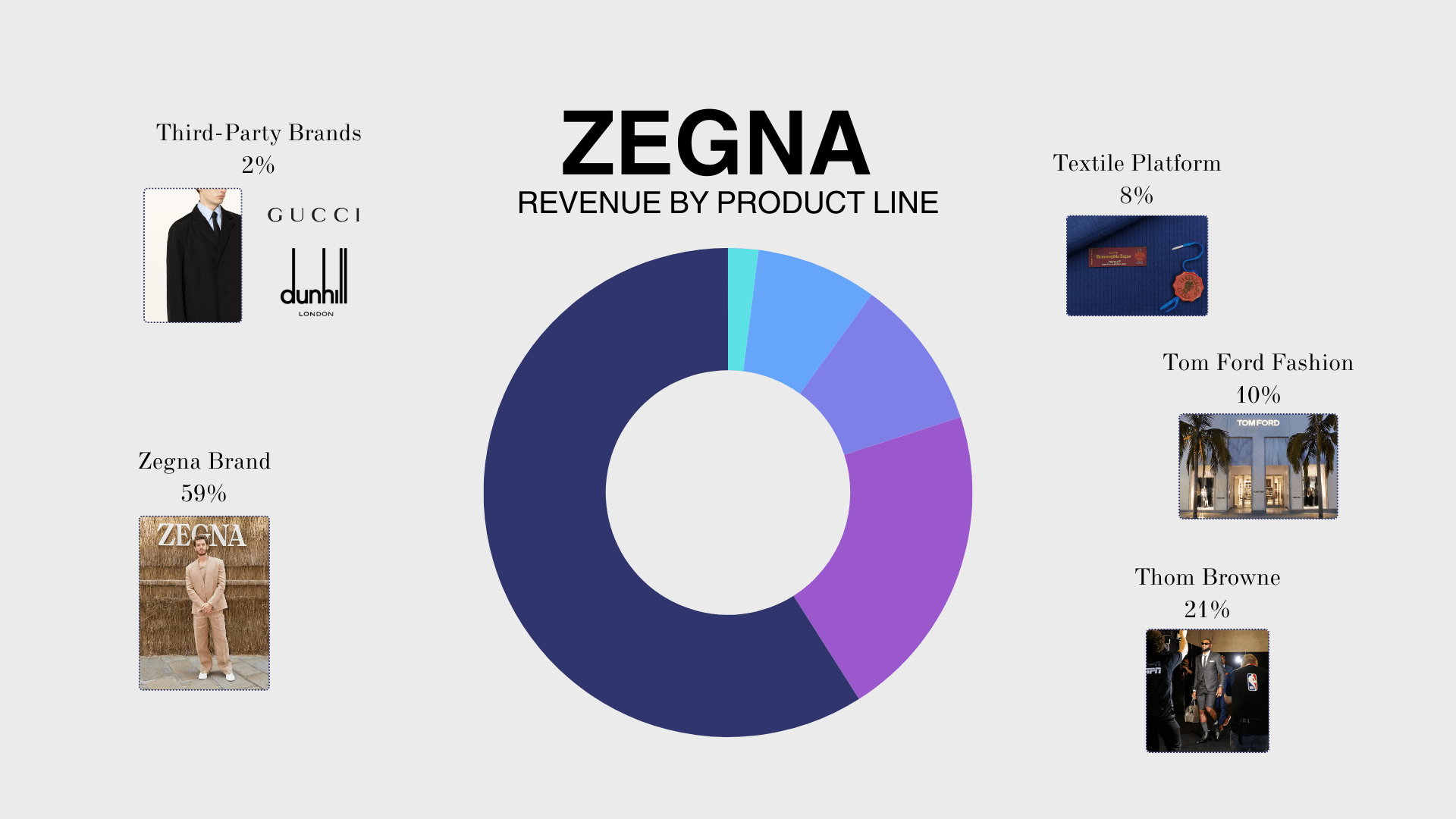

Having introduced the origins and development of the current Zegna Group, we can now explore the company's financials. As presented during the latest quarterly revenue report, Zegna categorizes its sales in the following segments:

- Zegna

- Thom Browne

- Tom Ford Fashion

Revenue by Product Line, Q3/23 (Own Illustration)

{kind=link}

Zegna

The first segment is also by far the largest, accounting for more than 70% of the company's total sales. Most of this is derived from the parent brand Zegna, of course, but it also includes the company's textile platform and third-party offerings, making it the "original" core of the company.

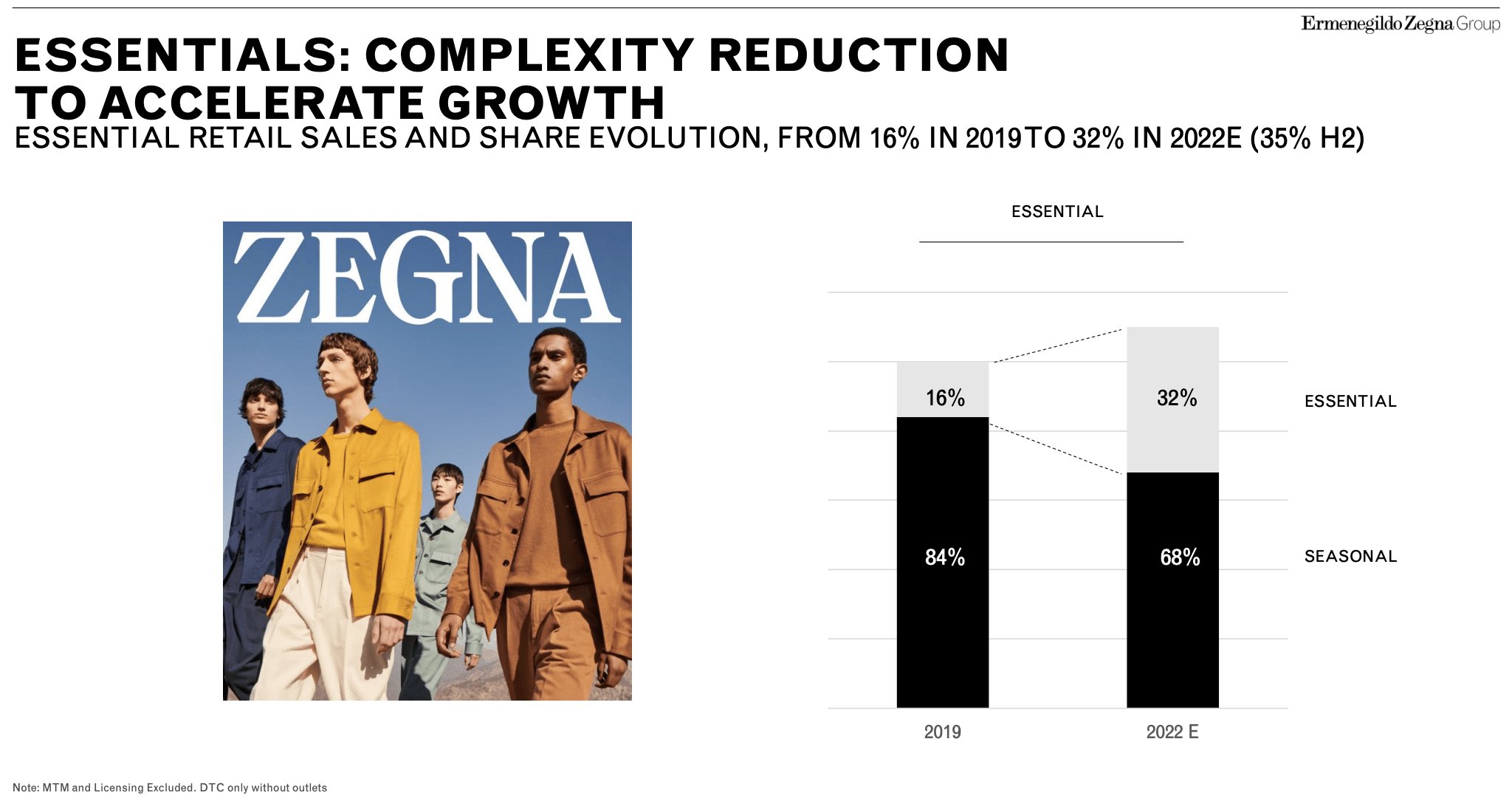

However, we also see a lot of movement here, as the company's flagship brand has undergone quite a rebranding in recent years, from having several sub-brands ( Ermenegildo Zegna, Z Zegna, and Ermenegildo Zegna XXX ) to unifying the entire offering under the ZEGNA brand in 2022. The so-called One Brand strategy should modernize the brand and authentically change the brands' offering from being solely formalwear to including more casual but equally luxurious collections. Luxury leisurewear is the brand's new focus, addressing a younger customer base that is increasingly dressing more casually, a trend that has been accelerated by the pandemic and its impact on the work environment. In addition, these products are less seasonal, allowing for greater efficiency in the brands' store management and potentially higher turnover from a more broadly targeted customer segment. The company's management describes this advantage of the rebranding strategy as follows:

Furthermore, thanks to the One Brand strategy and to the changes in our brand positioning and offering, we are able to develop a more sophisticated merchandising that blends and balances the presence of seasonal products with our Essentials collections which are generally sold across seasons with minimal style changes), which we expect to drive higher sell through. The dynamic management of our DOSs, including the optimization of locations and average square footage, and a data-driven approach to customer relationship management and retail KPIs are important elements of our Retail Excellence strategy.

From my perspective, the new rebranding of Zegna was a necessary move to remain the desirability and general interest of customers, while simultaneously creating new growth potentials and less seasonal sales.

Complexity Reduction in Zegna's Product-Mix (Investor Day 2022)

{kind=link}

However, evaluating this development through numbers is difficult as the company's filings only allow insight into the operating results back until 2019. According to the available data, Zegna faced quiet challenging times as the brands' sales dropped by more than 30% during 2020 and constantly recovered to pre-pandemic levels until 2022, which results in an overall flat revenue growth of 0.14% from 2019-2022.

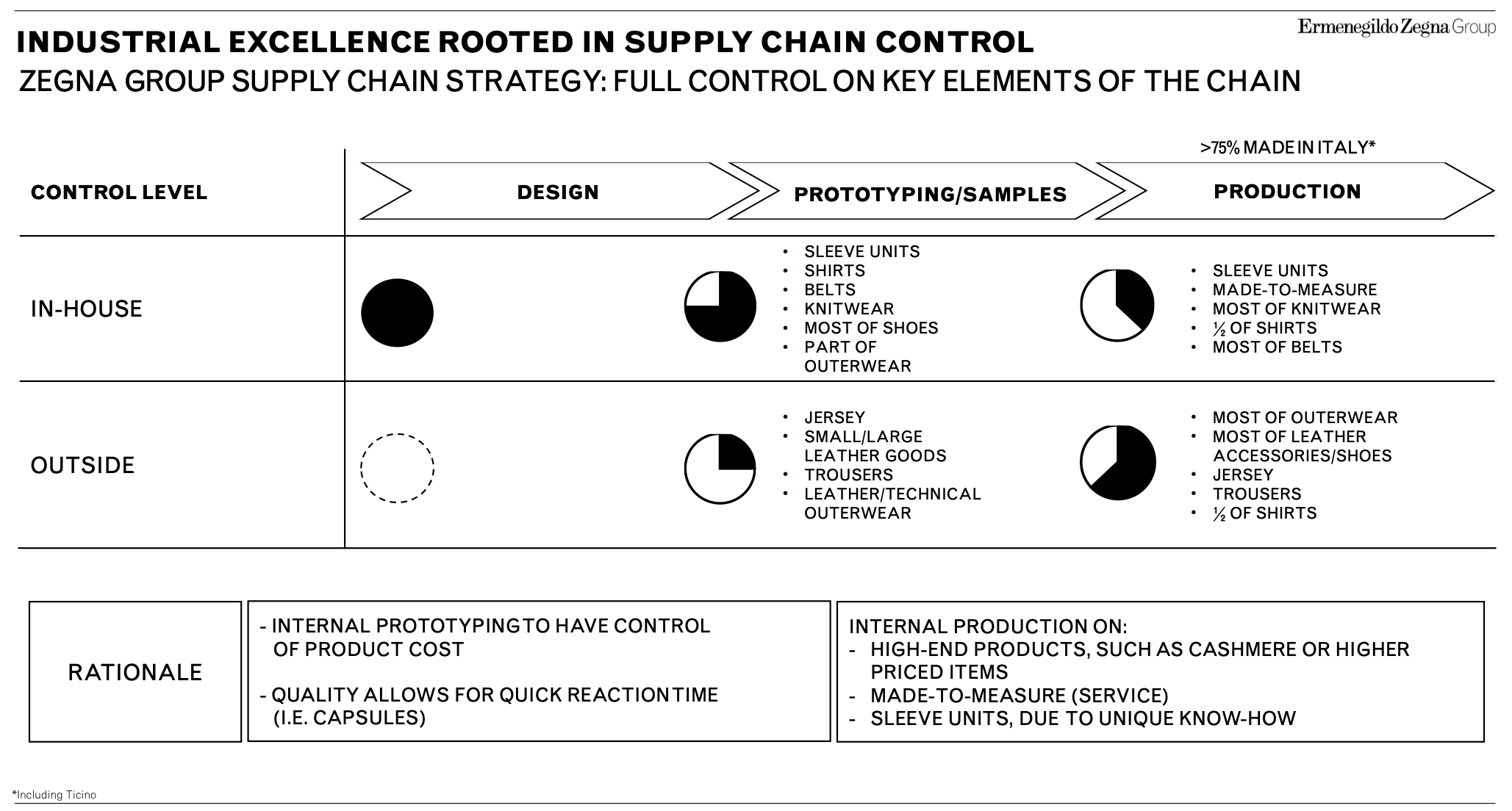

Zegna: Supply Chain (Investor Day 2022)

{kind=link}

But as mentioned earlier, this segment also includes the Italian textile platform and related third-party brand sales. And while all of the small, acquired manufacturing companies are potentially less popular, they're certainly the heart of the parent company, as both Zegna and the acquired brands rely heavily on the high quality craftsmanship ensured by this fully vertically integrated supply chain. From my perspective, they could be the competitive advantage for the company in terms of future acquisitions of smaller independent brands, but also in terms of an authentic way to promote product quality and desirability - the most prominent example being Hermès (which I also discussed in another article ). Having mentioned the French icon, I would say that the dedication to craftsmanship and the traditional "slow factory" model are probably on a par in terms of quality. However, Hermès' combination of exclusivity, product quality and the pricing power of its sought-after bags is more compelling to me in the future than the combination of these factors with Zegna's triple-stitched shoes or superbly crafted suits. Of course, the levels of sales may differ significantly; nevertheless, it is interesting and important to think about a brand's iconic products, which turn out to be the cornerstone of the brand's equity.

But overall, the company appears to have successfully maintained Zegna's appeal through a much-needed modernization. The fully integrated supply chain will additionally assure the high standards of product quality and sustain the brand's perception of sustainability, given the growing interest in local production, long-lasting products and fair compensation among customers.

Thom Browne

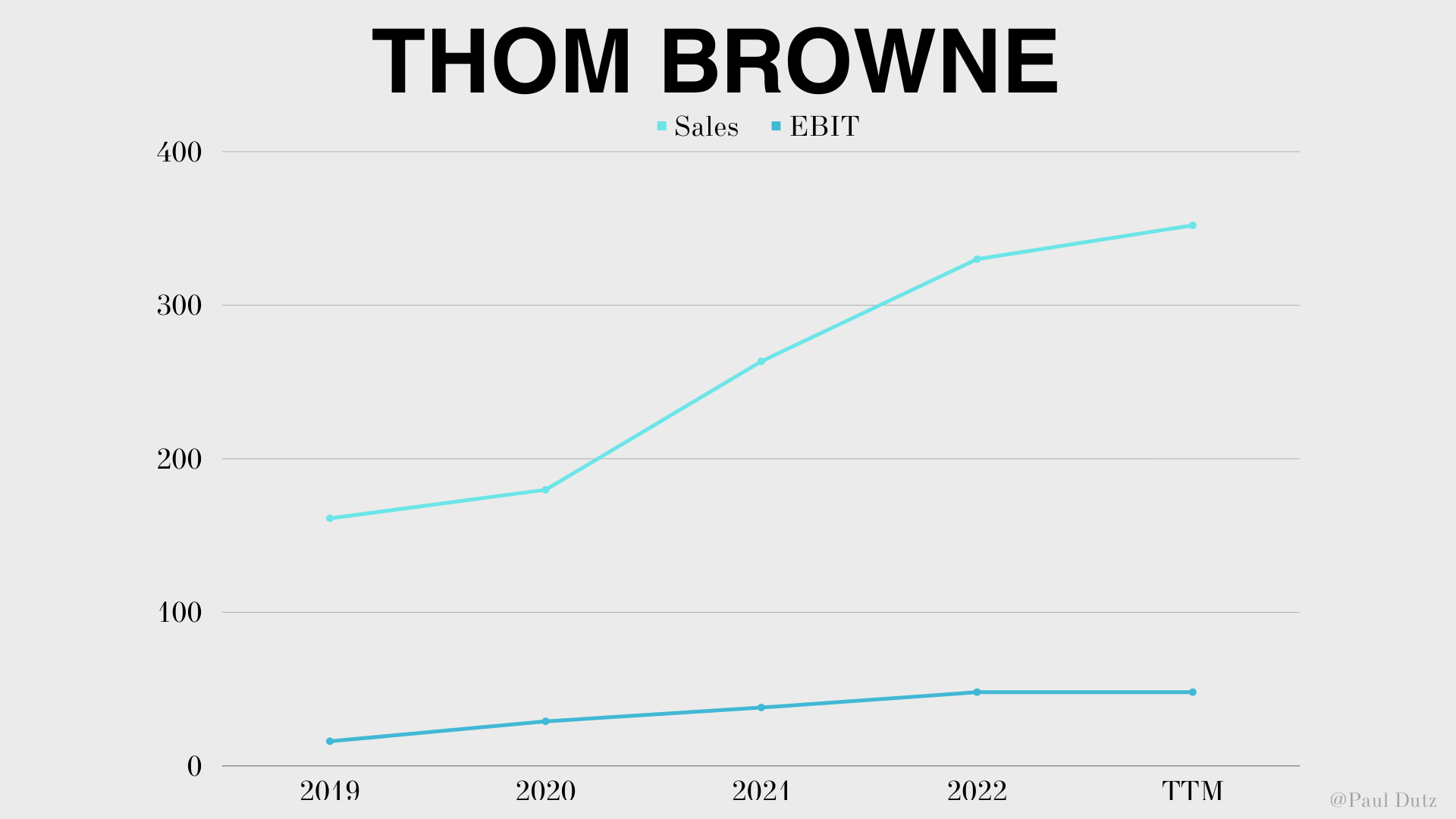

Although my review of the company's core segment left me with mixed feelings, I must admit I was pleasantly surprised by the successful acquisition of Thom Browne. Since 2019, the company has experienced 27% annual growth in sales and a 44% increase in EBIT. However, this only translates to an operating margin of 13.6% on a TTM basis.

Thom Browne, 2019-2022 (Own Illustration)

{kind=link}

Unlike Zegna, Thom Browne initially targeted a younger and more niche clientele, while both focused on menswear. In recent years, however, the brand has gradually added womenswear, presenting a new growth opportunity for the brand in addition to expanding their geographic reach. CEO of Thom Browne, Rodrigo Bazan, commented on the current strategy for Thom Browne during the recent earnings call as follows:

The reason we started to really push women's on 7, almost 8 years ago was just to balance the business to have the brand potential to be both men's and women's overall. [...] It's a very committed clothing client. And we also want to make sure that we continue to have the very loyal client engage with Thom Browne and buy more Thom Browne. And we manage the growth of Thom Browne men's to make sure that we don't lose that original clients, and we mindfully add key clients to the brand. So women's business still is a great opportunity.

Currently, Thom Browne contributes around 20% to the Groups' revenue and could further take share as the momentum continues. In the 9M of 2023, the brand achieved organic growth of 15.7% mostly driven by a strong DTC business that gets further strengthen through the conversion of existing wholesale stores in Korea. And similar to the iconization of products, we can recognize another industry-related pattern here, namely the retailization of the luxury brands' distribution networks.

Overall, there are no indications that Thom Browne's momentum is slowing down in the current market climate, which bodes well for the brand's future outlook. The committed customer base and the significant reinvestment in expansion and retailing strategies create a promising combination moving forward.

Tom Ford

Finally, we can talk about the latest addition to the company's brand portfolio, the Tom Ford fashion segment. As already mentioned, Zegna fully acquired the fashion subsidiary in 2022 and started to present this segment separately in this year's first-half results. Therefore, I can't really delve into the brands' track record, but will show the current status to complete the segment overview.

In the last 6 months, Tom Ford contributed approximately €139 million in sales with an operating margin of around 6%, resulting in a share of 10% of the Group's total sales. During the Capital Markets Day next month we will probably see more details here, but for now we have to stick with what we have.

Overall Thoughts

Now that we've talked about each part of the current Ermenegildo Zegna Group, I'd like to share some overall thoughts. In total, the company has built a group around three individual luxury brands, all of which rely on the excellent product quality provided by the fully integrated platform of Italian textile manufacturers. While each of these brands has an individual and recognizable heritage, we can see a very dynamic strategic evolution in recent years, especially at the key brand Zegna. The rebranding and, in part, repositioning of the brand has created a number of opportunities for the company, but also a number of unknowns in terms of future prospects. However, considering the current market environment for luxury brands in the fashion and leather goods segment, these brands seem to be defending their status remarkably well.

| Sales Growth |

| Zegna (Group) |

| Zegna Brand |

| Thom Browne |

| Brunello Cucinelli |

| Hermès |

| Latest 9M |

| 19.2% |

| 20.6% |

| 10.1% |

| 29% |

| 22% |

| Latest 3M |

| 11.3% |

| 8.0% |

| 5.8% |

| 21% |

| 16% |

Zegna's price point seems to appeal to a similar clientele as Italian peer Brunello Cucinelli ( BCUCF ) and French icon Hermès ( HESAF ), and is more resilient to economic downturns. Gildo Zegna described his current view on the customers as follows:

In terms of resilience, I think that we have seen a good trend by the wealthy buying more luxurious products. That's why we are adding an uber luxury product to our product offer, because I think that for those folks, price is not an issue [...]. And that means that most of the wealthy shopper are attracted by the new Zegna strategy and of our branding.

The brands have shown resilience in recent quarters and management seems confident that double-digit growth rates can be maintained going forward. Similar thoughts arise when we look at Zegna's mid-term guidance. According to this outlook, the company expects to achieve sales of €2 billion and an adjusted EBIT margin of 15% in 2025, which would represent a sales CAGR of around 10%, in line with current expectations. Furthermore, the underlying annual growth rate of the personal luxury goods market can be estimated at approximately 6% going forward. In view of major trends such as product iconization and the growing influence of younger generations, Zegna's strategic shift appears to be highly appropriate and could lead to an increase in market share. However, it should be acknowledged that current profitability lags behind industry peers, and even the targeted 15% is respectable but not exceptional. Similar to Brunello Cucinelli ((BCUCF)), it is clear that sustainable and regional production with fair pay comes at a cost to investors, unlike typical fashion brands that prioritize minimizing production costs. So let's take a look at the cash flow!

Cash Flows

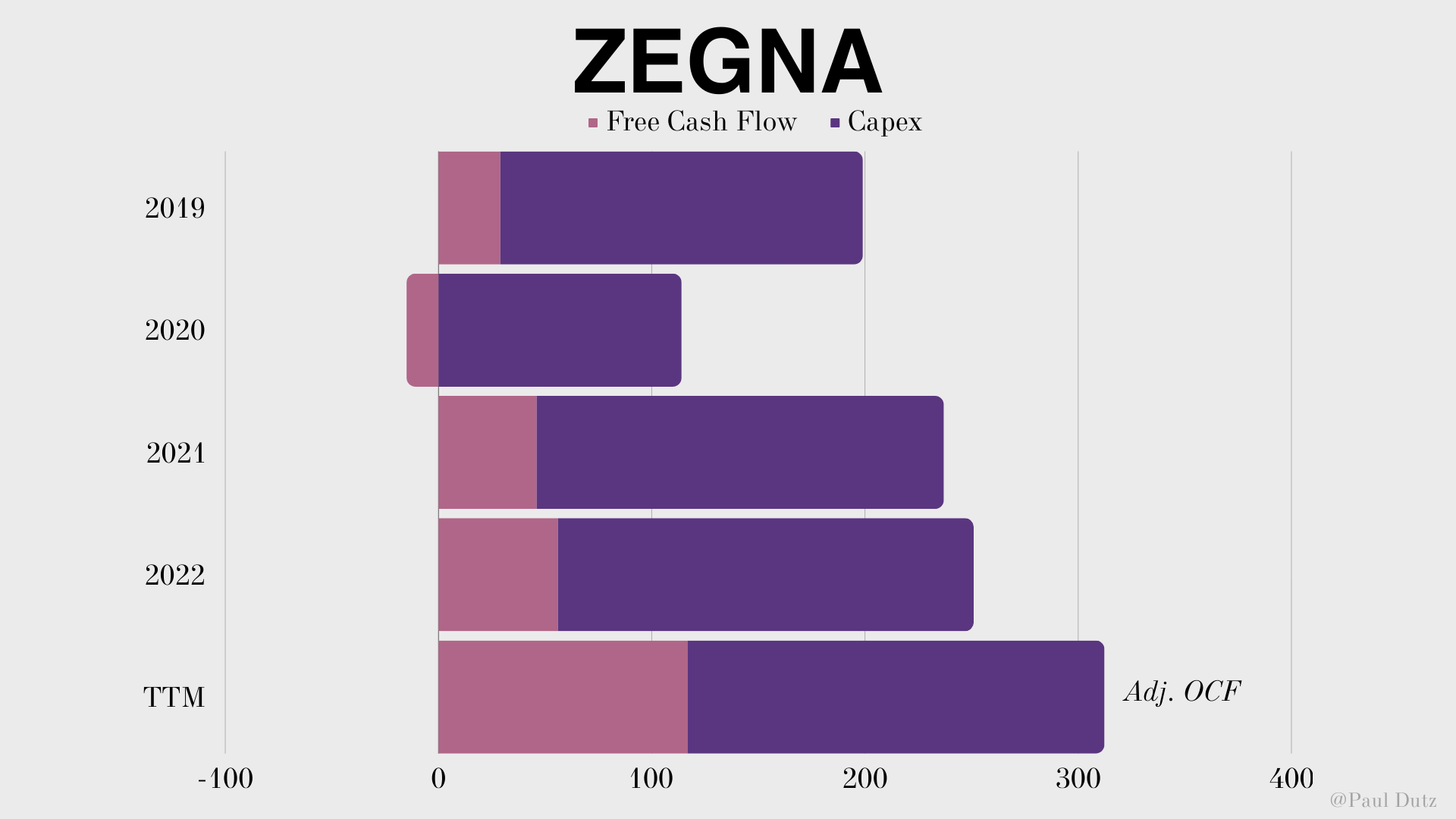

In order to analyze a company's ability to generate cash from operations, I focus primarily on its free cash flow. Despite the usual calculation (OCF - CapEx = FCF), I adjust the operating cash flow for changes in net working capital and subtract the stock-based compensation. Using this approach, I try to get closer to the actual and sustainable cash generation of the business through the perspective of its owners.

For Zegna, the calculation looks like this:

| in € million |

| Operating Cash Flow |

| 225.60 |

| - Stock-based Compensation |

| 0.00 |

| - Changes in Net Working Capital |

| -86.74 |

| = Adjusted Operating Cash Flow |

| 312.34 |

| - Capex |

| 79.30 |

| - Payments on Lease Liabilities |

| 116.13 |

| = Free Cash Flow |

| 116.91 |

During the latest comprehensively reported period, H2/22-H1/23, Zegna was able to convert around 32% of its adjusted EBITDA into free cash flow due to a significant amount of lease payments and capital expenditures during the period. Also, we're missing a historical average for a comparison, because there were too many extraordinary payments to account for. Slowly, we can obtain a more clearer view on the company's ability to generate cash, but it will certainly take a few more years to comprehensively review underlying trends. Therefore, I will add the adjusted operating cash flow in this case to the analysis to obtain a trend.

Overview: Cashflows, 2019-TTM (Own Illustration)

{kind=link}

We can clearly see an improving trend in the company's operating cash flow, which is growing at a CAGR of 8% and 12% until 2022 or TTM, respectively. At the same time, Zegna has been increasing its capex at a slower pace, resulting in a rising FCF margin. If the company continues to achieve this operating leverage, we'll likely see higher margins and better cash conversion in the future. However, I have to admit that the various strategic moves will continue to require reinvestments to build brand equity and maintain high quality, so free cash flow will remain lower.

Valuation

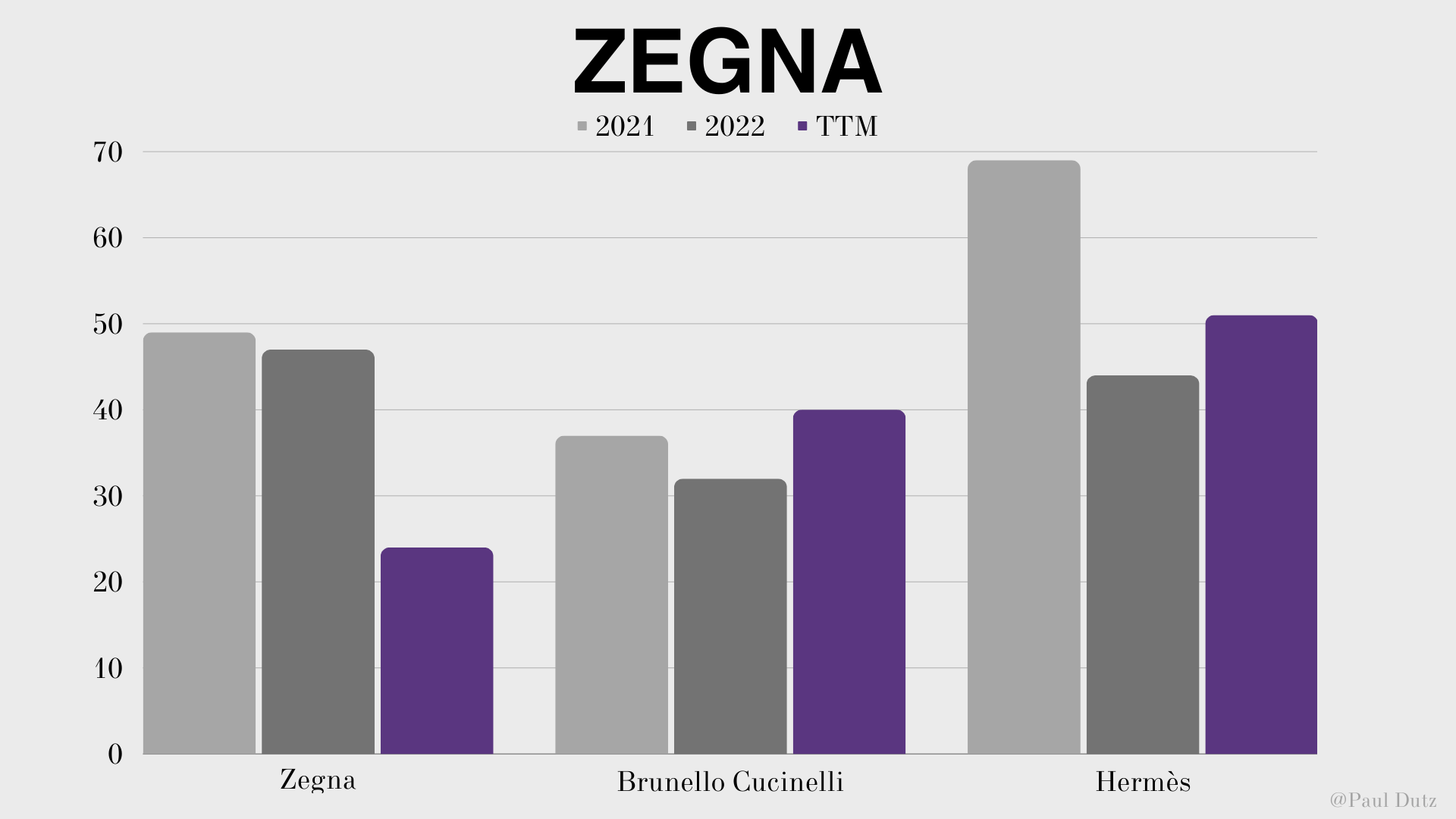

At a share price of $11.62, Zegna is currently valued with a market capitalization of around $2,765 million or €2,527 million, making it a rather small luxury group compared to the often cited peers. Including the company's net debt of around €317 million, we arrive at an enterprise value of €2,844 million, which we'll use to calculate the current multiple.

Based on the company's most recent 12-month cash flow figures, Zegna trades at an EV/FCF multiple of around 24, which seems reasonable given the large amount of growth capex we haven't excluded from the calculation. Interestingly, the current share price is below the IPO price of $11.72 per share, which should be enjoyed cautiously as the number of outstanding shares has been diluted by around 17% in 2022. Nevertheless, we can conclude that Zegna's operating performance has been better than the share price appreciation, leading to the lower multiple.

EV/FCF, 2021-TTM (Own Illustration)

{kind=link}

Compared to other luxury companies that deliver an equivalent level of quality, we can clearly get a discount at the current valuation. Going forward, this could be an opportunity if Zegna continues to deliver double-digit growth with operating leverage that drives margins. However, I find it difficult to evaluate the investment opportunity based on this multiple comparison alone, as we don't have historical averages and also have to price in a higher level of uncertainty for Zegna.

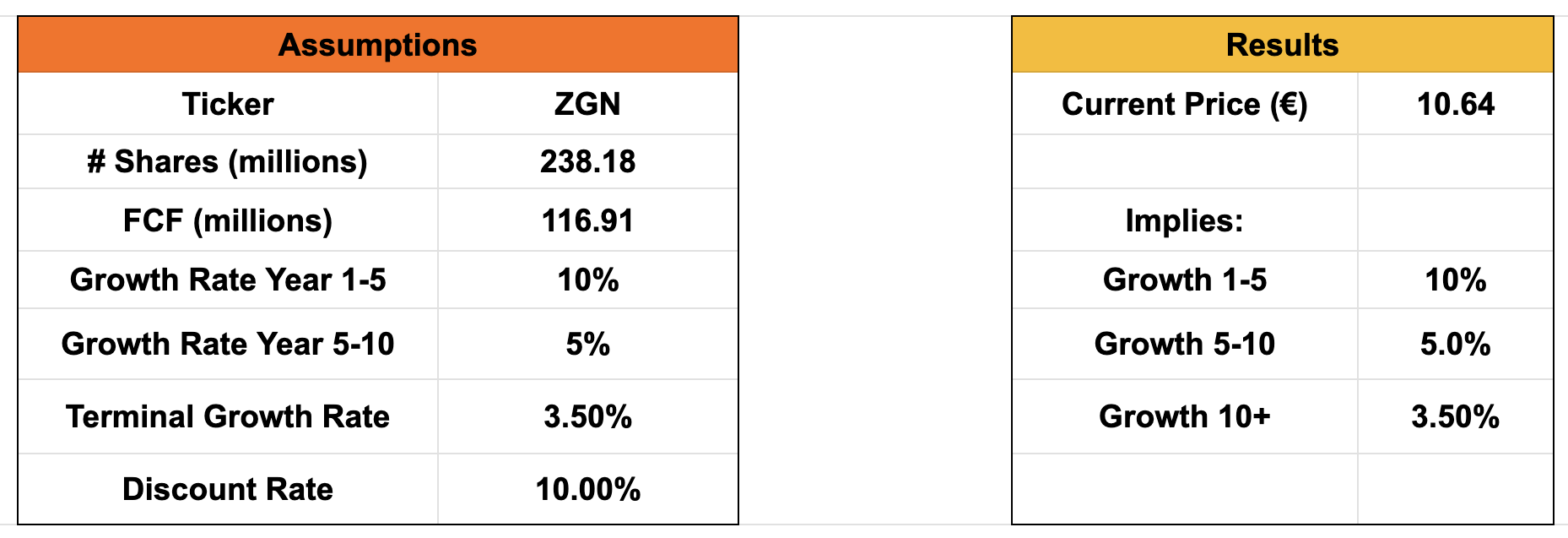

Therefore, I also use an inverse DCF model before closing this valuation segment. Using the FCF we obtained earlier, we derive an interesting result showing that the current share price only implies a growth rate of 10% for the first 5 years and another 5% for the following 5 years. I believe that 10% for the next few years is overly fair in terms of guidance for sales growth and margin expansion. Compared to my article on Hermès , I also lowered the TGR by 1%p to reflect the short track record and higher uncertainty.

{kind=link}

In my view, the model shows interesting upside to the current valuation if Zegna delivers on its mid-term guidance and continues to deliver operating leverage. In addition, investors could be positively surprised by an updated guidance at the CMD in a few weeks or other news that affects the uncertainty discount.

Conclusion

I dedicated a lot of time to this article because I really wanted to do a comprehensive review of the company in order to lay a solid foundation for the results to come. Notably, the company's commitment to quality and fully integrated supply chain distinguish it from other luxury brands, a factor which I felt was important to highlight.

Ermenegildo Zegna is a noteworthy new entry in the luxury space, characterized by strategic M&A and a prosperous opportunity for both organic growth and margin expansion. However, the company is playing several games at once, building the entire group, rebranding the flagship Zegna brand, reinvesting heavily in Thom Browne, and also launching Tom Ford as a standalone division. As a consequence, investors must accept a relatively higher amount of risk regarding the success of each individual outcome. In this respect, the coming CMD represents an opportunity for the company to raise the confidence in the investor sentiment.

In my opinion, Zegna represents an interesting investment opportunity for investors looking for luxury with higher growth potential than the big established names. However, one should be confident in the company's brands and their prospects in order to be patient over the next few quarters while the company's operations develop. Otherwise, I would probably wait until Zegna's quality is reflected in higher margins and a more mature Zegna brand, and the level of uncertainty has shrunk.

For further details see:

Zegna: High-Quality Luxury At A Reasonable Price