ZGN - Zegna: Walking Through 2024 With Success And Style

2024-01-02 00:32:32 ET

Summary

- Zegna's current undervaluation and under-following made the Italian company my pick for the year 2024.

- During the recent Capital Markets Day, the company demonstrated a promising vision and financial target for Tom Ford Fashion.

- Zegna's top-line will benefit from ongoing demand for "quiet luxury" and high-quality products, while operating leverage reinforces margin expansion.

- Zegna is trading at a 50% discount to other absolute luxury companies, and could narrow this gap throughout the next year.

Ermenegildo Zegna ( ZGN ) (in the following "Zegna") is a fast-growing luxury platform built on the Zegna brand and currently in the hands of the third generation of the founding family. With its origins in the beautiful "Oasi Zegna", the company has created a luxury textile platform through various acquisitions of specialized workshops that preserve the quality of the "Made in Italy" label. While operating results in 2023 were promising, shareholders weren't rewarded with outperformance. The main reason for the market's discount was the higher level of uncertainty as a result of Zegna's short track record and the newly established acquisition of Tom Ford Fashion. However, the recent CMD has brought light into the darkness by providing a comprehensive strategy and mid-term targets for each brand. Combined with the remaining valuation gap, I see a great opportunity for investors next year, making it my top pick for 2024. Let's take a closer look at my reasons.

Investment Thesis

Zegna has successfully created a group around three luxury brands, all of which rely on the excellent product quality provided by the fully integrated platform of Italian textile manufacturers. Based on the solid foundation of the finest Italian garments, the company has restructured the Zegna brand over the last years, making it more appealing and desirable in the modern world of iconic products and comfortable yet elegant ready-to-wear apparel. Due to the successful transition, the brand is able to benefit significantly from the recent "quiet luxury" trend, while the simplification and elevation of the brand also enhances its margin potential. In addition, the group owns the unique luxury tailor, Thom Browne, that is becoming increasingly popular among the fashion industry, while simultaneously enjoying impressive loyalty from existing customers. Lastly, the luxury group was supplemented by the fashion business of the iconic Tom Ford under a licensee agreement with Estée Lauder.

Overall, the group has achieved excellent results since its listing in 2021, in particular by exceeding its own financial targets. The passion of CEO Gildo Zegna has led to a successful business combination, on which the company can build to expand and increase profitability. Looking ahead to 2024, I expect company's perception to benefit from the differentiating industry environment, promising operating results, and reduced uncertainty around Tom Ford's prospects. As a result, Zegna could be re-rated by the market, thereby narrowing the valuation discount to company's absolute luxury peers.

Luxury Goods: Increasing Duality Benefits Absolute Luxury

The global personal luxury goods market achieved record results and double-digit growth in 2022 as a consequence of the rebounding demand and filled budgets. According to Bain & Company , it can be expected that around 95% of brands experienced positive growth during this time, underlining the old wisdom "a rising tide lifts all boats", therefore making in-depth analysis seem pointless. However, due to the fact that the luxury market is a resilient but not fast-growing industry, it was to anticipate that the extraordinary demand will normalize soon. During 2023, we have experienced the beginning of this normalization as particularly "aspirational" consumers increasingly face exhausted budgets and inflated cost of living. Accordingly, Bain noted that only 65-70% of brands are expected to grow positively in 2023, stating:

This is a defining moment for brands, and the winners will separate themselves through resilience, relevance, and renewal —the basics of the new value-centered luxury equation.

And we were clearly able to see the results already come in quiet differently among the "luxury category" investors were hyped about. These differences depend on the resilience of the luxury brands, which correlates in particular with the degree of exclusivity and rarity. Brands that massively increased their penetration in the last years, especially to sell the demand of "aspirational" customers, are now experiencing the hardest fall. Zegna, due to its wealthy and loyal customer base, however, will likely stay optimistic looking forward, as they're less sensitive to inflated cost of living and the recent price increases. In the case of the Zegna brand, the company declared that the top customer segment, classified as spending at least €50,000 during a year, has grown by over 60% since 2022, leading to only 5% of the brands' total costumers that contribute 40% of revenue. Importantly, Zegna is benefitting from a high customer retention rate of 89% of this cohort, which is building a promising fundament for the next year. Furthermore, Zegna has successfully modernized the brand through simplification and the focus on iconic product lines. As a consequence, new customers of the brand are on average 7 years younger than the existing customer base and also spends 58% more on a global basis. The combination of both should strengthen the company's resilience and furthermore, its perception in the market.

China: Zegna Perfectly Positioned to Increase Market Share

Additionally, when thinking about the global luxury market in 2024, an important growth factor will be the continuous comeback of the Asian customer segment, particularly the domestic demand and Chinese tourists. The overall economy in Asia-Pacific is contributing around 43% of Zegna's overall revenues, while solely China accounts for almost one third. During the last quarter, the results in China unperformed most of the other geographies for Zegna, however, it will surely be a key for future growth. Therefore, it was reasonable to address this market in particular during the latest Capital Markets Day. Especially, the Zegna brand and Thom Browne are currently expanding in this region by initiating events in order to raise brand awareness and engagement. With success - the Zegna brand has achieved the highest results in a report on WeChat users' perception of popularity and engagement regarding luxury brands during the last quarter. Compared to last year, Zegna more than doubled its engagement rate and also increased the popularity of the brand by more than 50%. And also Thom Browne is seeing a promising opportunity in this market that will be particularly fueled by the brands' clienteling app, which will be rolled out in China and South Korea during the start of 2024.

Tom Ford: Promising Strategy to Drive Results and Reduce Uncertainty

During my latest article on Zegna, I argued that the missing strategic and financial outlook on the newest contributor Tom Ford will add uncertainty to the company's perception among investors, especially under the current market environment. To this regard, I was satisfied by the recent CMD, during which the company was quiet enthusiastically presenting their vision for Tom Ford, started by Gildo Zegna stating the following:

The brand [Tom Ford] is significant bigger than the business. This is the incredible part. And there are ample opportunities to leverage the group's synergies to fuel its growth and make it, I'd like to be bold, one of the 10 largest luxury brands in fashion, in the long term. Long term, don't ask me how many years. But we have the possibility, because the brand is so powerful.

Of course, this is quiet ambitious, but from my perspective it's an important statement to clarify the passion and ambition of the company's management for the future. It also gives the brand a vision to strive, which was also filled with color by the newly appointed CEO of Tom Ford, Lelio Gavazza. For me very important, he mentioned that the brand's development will be done step by step in a sustainable and "healthy" way, which directly reminds us of Brunello Cucinelli and his motivation of a "right growth". Given that Tom Ford will focus on the high-end luxury segment, it will be important to maintain the exclusivity of the brand and not overexpose it through rushed retail expansion. On the other hand, this means that Tom Ford will not be a surprisingly strong contributor to the company's results next year, especially due to initial investments that will likely wipe out the brand's profitability. However, given that the current contribution of 10% isn't significant, I would argue that the positive effect of developing the brand and communicating the strategy will more than offset the initial operational weakness. In addition, at the recent event, a medium-term outlook for Tom Ford was presented, which expects a top-line CAGR of 10%, which I believe is an appropriate target given the ambition to develop the brand sustainably. Furthermore, as these are just early rationales for the business, I would argue that investors could also be pleasantly surprised in 2024 if the brand's traction is more visible than expected.

Zegna: Strong Operational Performance Reinforces the Revaluation

Having discussed several facets of the group that could drive the stock performance in 2024, I want to additionally share my thoughts on the overall company. As a consequence of the ongoing "quiet luxury" trend and the refocusing of customers to buy "less but better" luxury goods in 2023, Zegna is expecting a revenue growth of 25% for this fiscal year, resulting in around €1.8 billion. These results are already ahead of the company's outlook to achieve €2 billion in revenue by 2025 (even excl. Tom Ford Fashion), which was initiated during the beginning of the year. Nevertheless, these exceptional results were driven by outstanding demand in an industry that has already started to normalize, therefore also reducing the pace for growth at Zegna going forward. As a consequence, Zegna presented a medium-term outlook for the company, expecting a revenue CAGR of 10%, contributed by the development of the brands, particularly through leveraging the Direct-to-Consumer distribution, price increases and continuous expansion and elevation of the brand's collections.

A key metric to monitor a company's success in growing its business profitably and efficiently is revenue per square foot. Interestingly, the company has almost achieved its own target for 2025 to improve this metric by 50%, which will further strengthen the quality of management and potentially the perception of the company going forward. In terms of profitability, these measures should provide an operating leverage that expands the overall margin. Accordingly, Zegna expects its adjusted EBIT to grow at a CAGR of 20% over the medium term, reaching 15% (excluding Tom Ford Fashion) by 2025. All in all, the combination of margin expansion, top-line growth and the continued reduction of brand development uncertainties is a promising mix for next year and beyond.

Risks

Going into 2024 with several opportunities, as described above, Zegna will potentially face different challenges that would be a risk for the future stock performance. Generally, there is the ongoing normalization of demand in the global luxury market that could impact Zegna's customers more significantly than anticipated. This could be the consequence of a higher-than-expected reluctance by wealthy clients that are critically important for the company's results. However, according to the most recent industry research, I would share the optimism of Zegna given the company's positioning and missing of a large aspirational, and more sensitive customer segment. Further, Zegna will likely show excellent results driven by the continuously high demand for "quiet luxury" and high-quality products.

That being said, another risk would be that Zegna is not able to continue the brands' developments as successfully, while particularly Tom Ford Fashion contributes the highest uncertainty. Given the company's track record of profitably integrating Thom Browne and the promising transition of the Zegna brand, I would argue that this risk is rather unlikely to unfold materially. However, the integration and development of Tom Ford Fashion, especially, will require significant investments in the next years, which will need to be monitored.

Overall, these risks are reflecting the challenges that Zegna will face, while continuously growing the business. Given the company's success in doing so, and the underlying strength that is a consequence of the passionate management and the excellent textile platform, I remain confident that Zegna will turn these factors into positive going into 2024.

Valuation

Nevertheless, I already stated at the beginning that another significant part of the investment thesis relies on the current valuation of the company. At a share price of $11.57, at the time writing this article, Zegna is currently valued with a market capitalization of around $2,755 million or €2,492 million, making it a rather small luxury group compared to the often cited peers.

However, a comparison among absolute luxury companies shows that Zegna still receives a significant discount of more than 50% from the market. I would argue that the ongoing development of the company's portfolio and its current outperformance of the broader luxury market should reinforce the perception of the company as a resilient luxury player and thus narrow the valuation gap.

Surely, Zegna's brands are unlikely to achieve a similarly iconic and "unbeatable" status as Hermès, however, they are likely to grow constantly in the future, while fully benefitting from the resilience of absolute luxury.

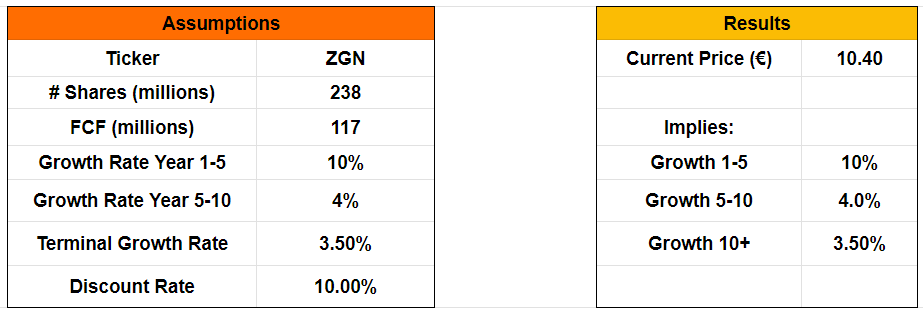

In order to proof the current undervaluation of the company, I also used an inverse DCF model. Using the most recent FCF of €117 million ((TTM)), we derive an interesting result showing that the current share price only implies a growth rate of 10% for the first 5 years and another 4% for the following 5 years. I believe that 10% for the next few years is overly fair as it represents the company's guidance for the medium-term. I also used a rather conservative terminal growth rate given the higher uncertainty compared to the cited peers in the absolute luxury segment.

{kind=link}

In my view, the model shows an interesting upside to the current valuation if Zegna delivers on its mid-term guidance and continues to deliver operating leverage. In this case, the company should outperform as the current multiple as recognizes upside potential.

Conclusion

Looking ahead to 2024, I think Zegna ( ZGN ) is a very interesting opportunity for investors to benefit from the resilience of the industry and several catalysts that could potentially drive outperformance during the year. At the recent Capital Markets Day, Gildo Zegna's passionate vision for the Group as a whole and for each of its brands, and how the company intends to execute it, was clearly demonstrated. However, I also discussed the challenges that Zegna will have to face in order to deliver shareholder returns in the coming year. And with that, I wish you all the best for the coming year and, of course, the best returns!

For further details see:

Zegna: Walking Through 2024 With Success And Style