MATX - ZIM Integrated Shipping: Q3 Results May Miss Again (Rating Downgrade)

2023-11-12 08:22:04 ET

Summary

- ZIM Integrated Shipping Services Ltd is set to report its Q3 FY2023 earnings, trading near its all-time lows.

- I've decided to update my coverage in advance as ZIM's direct competitors have already reported on the third quarter. Read on.

- Matson was the only company in the sample that made relatively positive comments. But I expect ZIM to follow the actions of Maersk and Hapag-Lloyd.

- If we look at the actual performance of the peers and take Wall Street's expectations as the missing final observation for ZIM, we will see that the downward revisions ZIM has experienced in recent months may not be enough.

- I continue to hold ZIM and follow the dollar cost averaging, but as I have no concrete evidence that things should change in the near future, I classify my earnings preview article as "Hold".

Intro

Q3 FY2023 season is in full swing and shipping companies are no exception. One of the most intriguing companies for income-seeking investors is ZIM Integrated Shipping Services Ltd. ( ZIM ). It's due to report on November 15, 2023 , and is trading near its all-time lows after the reversal of the containership cycle became obvious to the market, and those who had hoped for ZIM's dividends until the last minute started to get rid of their positions.

I've decided to update my coverage in advance as ZIM's direct competitor, A.P. Møller - Mærsk A/S ( AMKBY ), has already reported on the third quarter. The same is true about Hapag-Lloyd ( HPGLY ) and Matson ( MATX ). In the past, the peers' results have predicted ZIM's, so I thought you might find my ZIM's earnings preview analysis interesting.

Peers Predict Another Ugly Quarter For ZIM

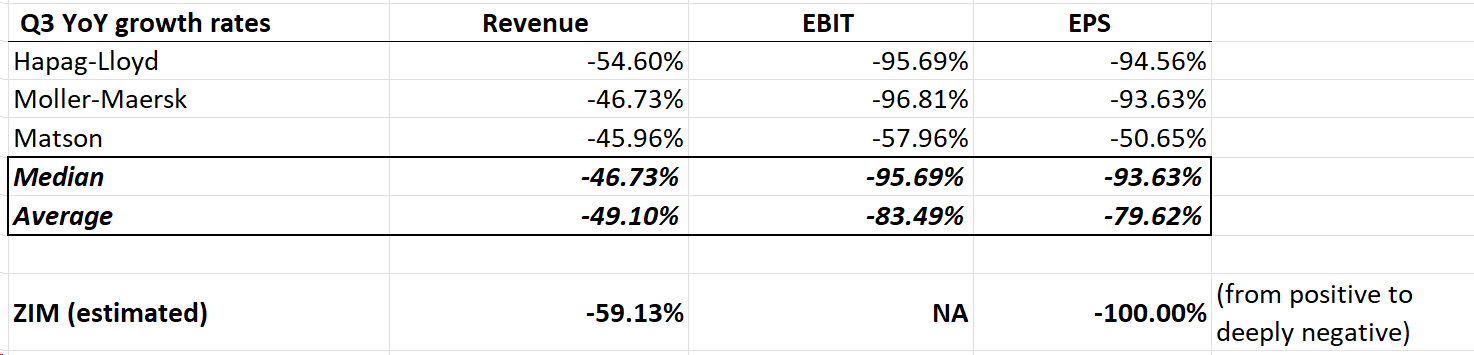

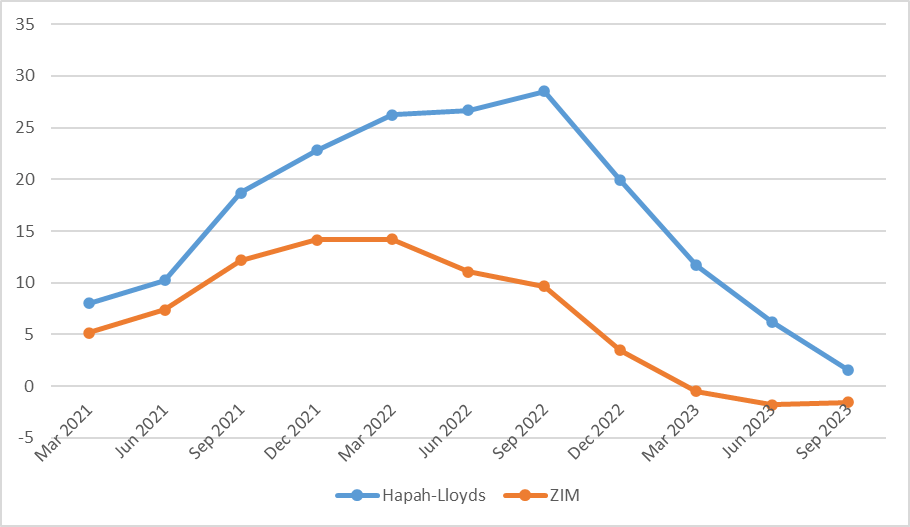

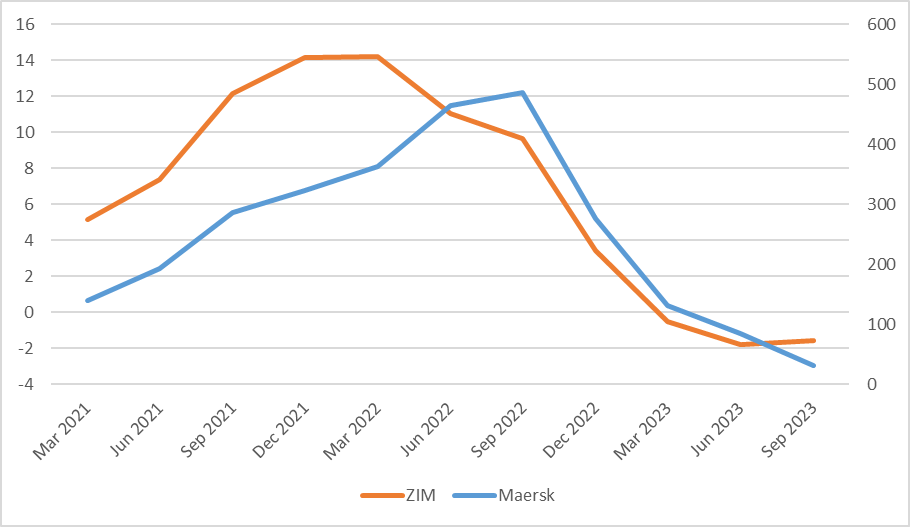

All of ZIM's competitors reported their quarterly results with a colossal drop in sales and shrunken EPS figures as a result of the normalization of global supply chains and falling freight rates. Hapag Lloyd's earnings call , for example, revealed that the company's Q3 results had come under increasing pressure due to falling rates despite increased volumes. The company faced pressure on spot rates on many trade lanes, necessitating initiatives to reduce costs.

Maersk had to make the same move , including a hiring freeze, reduced non-necessary expenses, and the cutting of 6,500 jobs. Maersk's efforts are now intensified , aiming to decrease the workforce by another 3,500 positions. The firm's focus shifts towards protecting margins, and CapEx guidance is cut to ~$8 billion for 2022-2023 and $8-9 billion for 2023-2024.

Matson proved to be the only company in the sample that made relatively positive comments . For example, MATX forecasts that EBIT in Q4 FY2023 will be above the level of Q1 2023, while others cut their guided ranges. The company acknowledges the impact of economic conditions on U.S. consumers but highlights resilience in its business segments. The market has apparently allowed MATX to outperform its competitors over the past month for this reason:

Anyway, the overall tone we hear during earnings calls reflects the challenges faced in the shipping industry, with a focus on adapting to market realities, cost reduction, and preparing for an uncertain trading environment. If we summarize the results of the companies in a single table, these challenges become as clear as possible:

{kind=link}

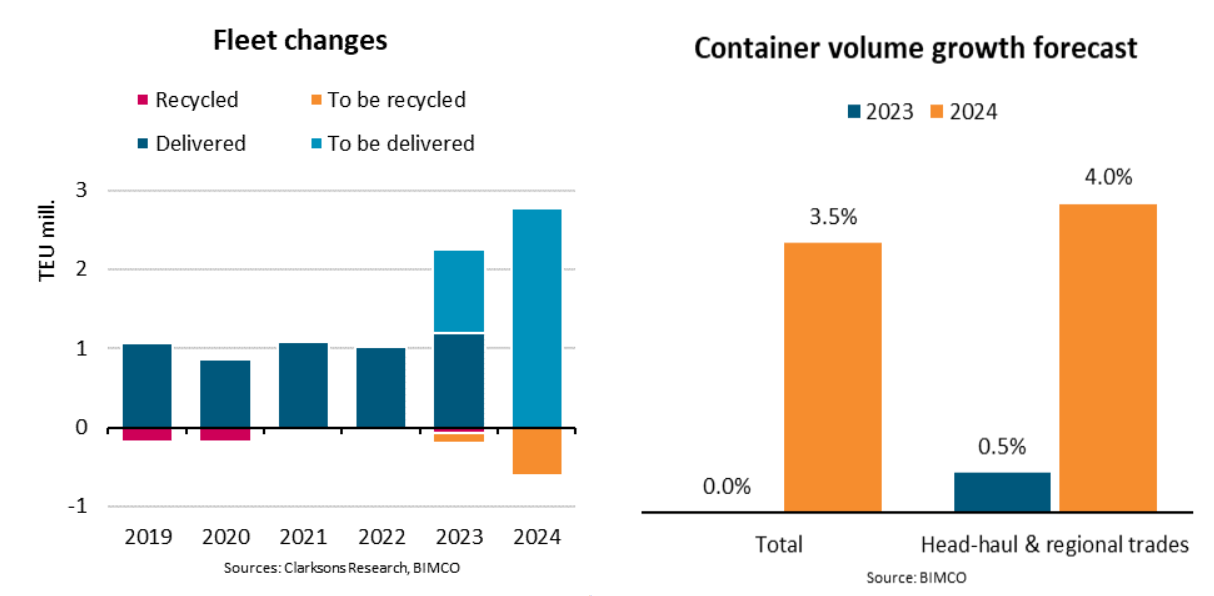

The high orderbook has become a much-discussed topic in the industry. The CEO of Hapag Lloyd stated that looking ahead to 2023 and 2024, there are concerns that the supply growth could exceed the growth in demand. As BIMCO noted in its recent outlook [ September 2023 ], the capacity of ship deliveries is expected to reach new records in both 2023 and 2024, reaching 2.3 and 2.7 million TEU respectively. The analysts also forecast that global container volumes will grow by between -0.5% and 0.5% in 2023, and by between 3.0% and 4.0% in 2024:

{kind=link}

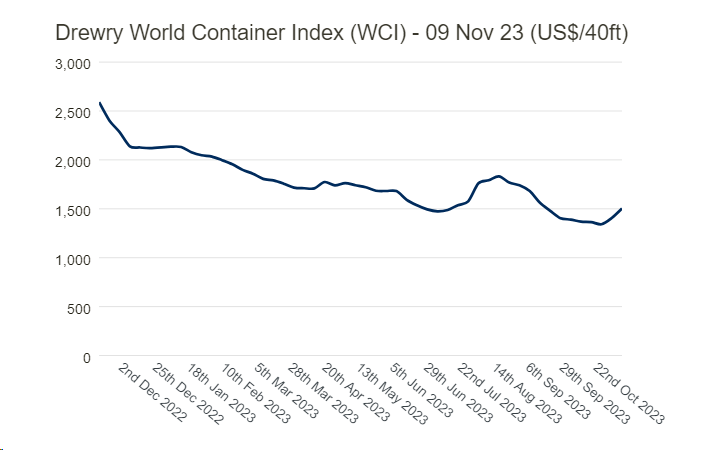

An increase in the supply of ships on the market has a negative impact on rates. Although the Drewry's World Container Index rose by 9% last week, it is still in a strong downward trend.

{kind=link}

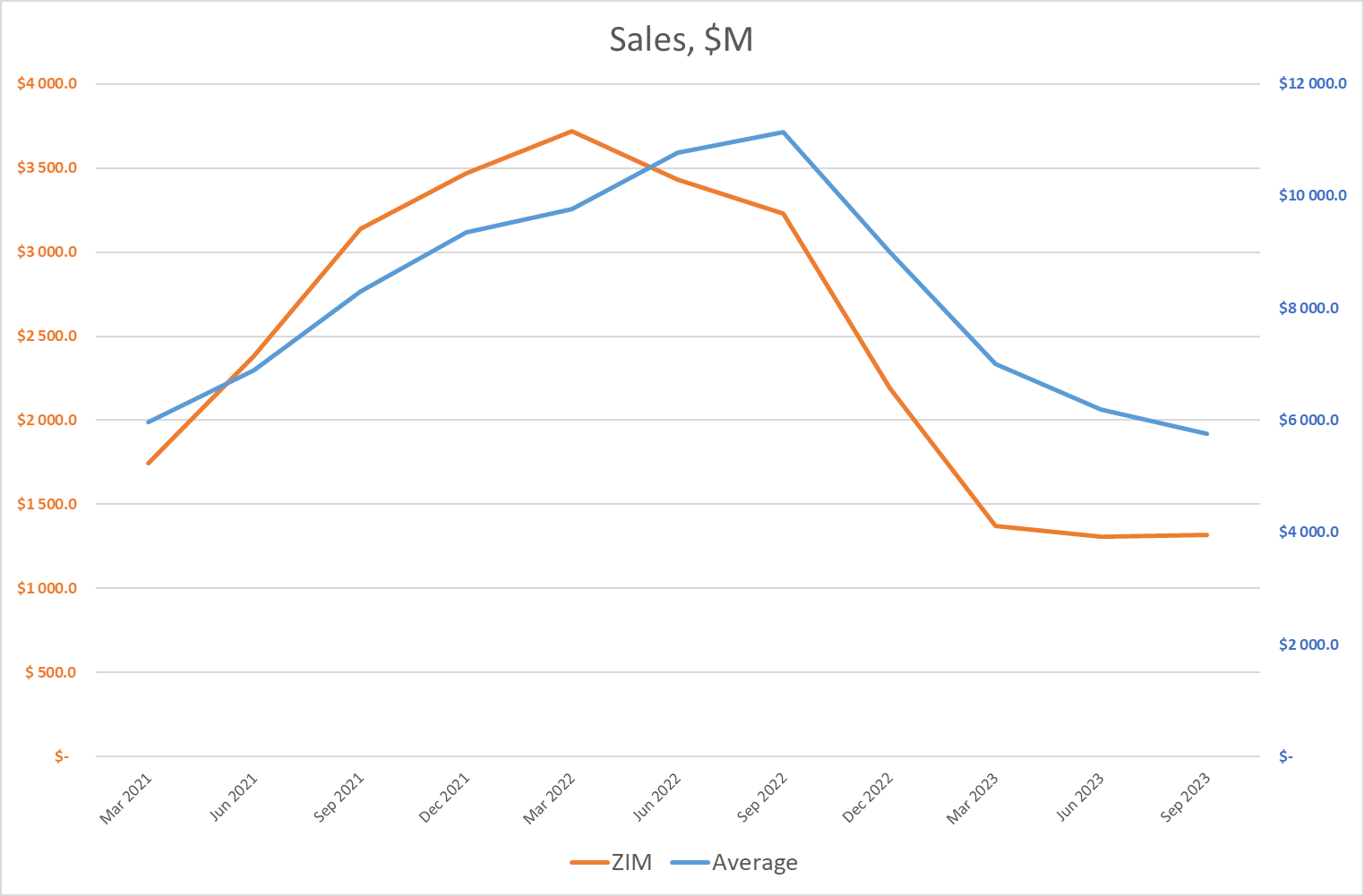

If we try to forecast how likely it is that ZIM will beat Q3 guidance, there is not much good to report for the bulls. The last two quarters have been unprofitable for ZIM in terms of EPS, while all other companies, although declining, still remained profitable. If we look at the actual performance of the peers and take Wall Street's expectations as the missing final observation for ZIM, we will see that the downward revisions ZIM has experienced in recent months may not be enough.

{kind=link}

{kind=link}

{kind=link}

The severity of Hapag-Lloyd and Maersk's Q3 FY2023 revenue/EPS declines does not match what the market expects from ZIM in a couple of days (not in the company's favor).

The market's reaction to the company's results will also depend heavily on management's guidance for the fourth quarter and beyond. From what I've seen from Hapag-Lloyd and Maersk, I don't think ZIM will come up with anything as promising as MATX. If you look at the call transcripts of past earnings , you'll see that ZIM's management usually follows what Maersk or Hapag says.

But I Keep Holding

Despite the rather gloomy medium-term outlook, I continue to follow the principle of dollar cost averaging, which I have repeatedly mentioned in my last articles on the company. I regularly buy equal amounts of ZIM shares, which continue to fall and increase my paper loss. But I won't be selling for the next 5-10 years, so in some ways I actually want ZIM to fall even further. I hope this will be the case after the Q3 release.

I hear many people say that ZIM has more cash on its balance sheet than its capitalization. And that is true today if we take the data for Q2:

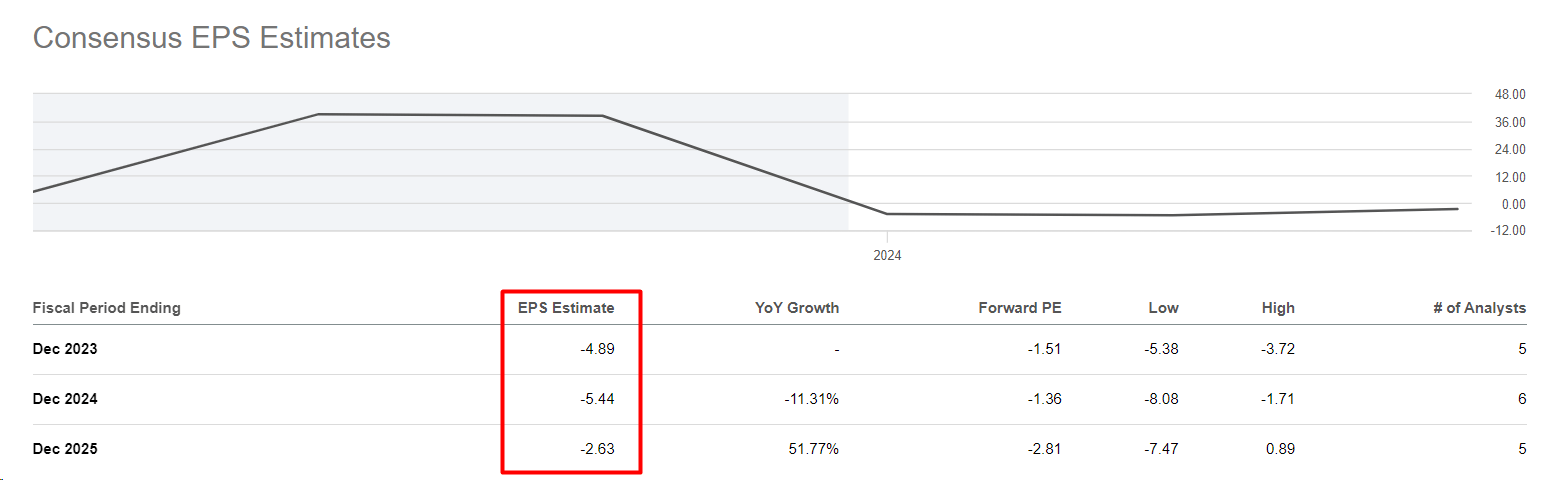

The company is severely undervalued by the market, but Wall Street is looking to the future where the company will most likely use up that money to sustain its operations, as it is expected to have at least 3 more unprofitable years ahead:

{kind=link}

The cycle is like a pendulum. If the company succeeds in overcoming this cycle's downward move, its shares should theoretically recover very quickly in the next upward movement. No one knows when this upward movement will come, but I want to continue to build my position in ZIM because I believe in this inevitable course of events.

But since I have no concrete evidence that things should turn around in the near future, I'm classifying my earnings preview article as a "Hold" without advising you to buy ZIM before the report. Please do your own due diligence. Always.

Good luck with your investments!

For further details see:

ZIM Integrated Shipping: Q3 Results May Miss Again (Rating Downgrade)