HOLX - Zimmer Biomet: Profit Growth Superb Q1 Knee Growth But Further Evidence Needed

2023-05-03 13:06:59 ET

Summary

- Zimmer Biomet posted a strong set of Q1 numbers at the top-and-bottom lines.

- The stock trades at a premium to peers, but has the fundamentals to back this up.

- There is room to grow for ZBH in my opinion and it has plenty of ways in which to deploy growth capital.

- Net-net, I reiterate buy with a $150 price target.

Investment summary

Investors are showing demand for Zimmer Biomet Holdings, Inc. (NYSE: ZBH) , after a solid set of Q1 FY'23 results , and there are legs in the old med-tech workhorse just yet. Since my last coverage in November, the company has gained a 15% bid. ZBH still has numerous supply-chain and manufacturing challenges to work through this year, so it won't be a normal period for the company, as stated by management last earnings call. But it will be a good year for robotics in orthopediatric surgery. This should benefit ZBH greatly, but it leaves many burning questions that must be satisfied.

Fig. 1

Data: Author's previous ZBH publication

{kind=link}

The drift towards robotics to perform surgery is a trend that's been in situ for some years now. Since the pandemic, labor costs have been front of shelf for hospital executives, and tight money has ring-fenced a lot of capital spending growth towards orthopedics. Still, GlobalData found the global robotic accessories market grew 500bps YoY from FY'21-22, and authors from Strategic Market Research project 20.75% geometric growth of the surgical robotics into 2030. Contrary evidence from GlobalData estimates 10% CAGR into 2030.

It is without question that ZBH's Rosa knee platform can benefit immensely from these growth percentages. The years of innovation and successful profit growth means this orthopedics colossus has claim to >50% of the global partial knee market. Add to that, the company grew its U.S. knees segment 18.1% YoY, 15% globally, to a combined total of $762mm in Q1 FY'23. I'd point out this is well above the knee market's growth rate, and that ZBH is priced accordingly as well. At 14.6x forward EBITDA and 2.4x book value, it better be more than just size we are paying for here. Net-net, I reiterate ZBH as a buy, looking to a $150 valuation.

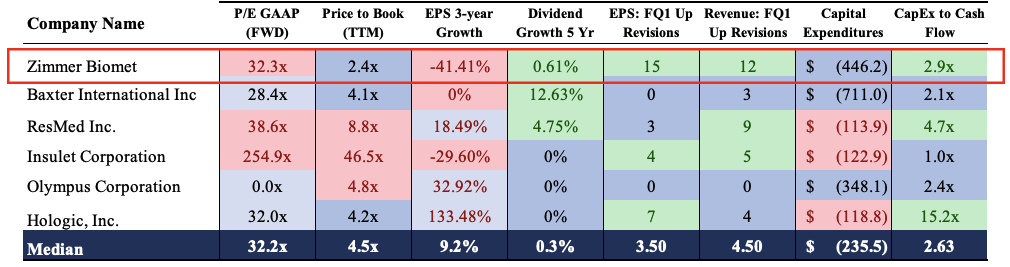

Market has ZBH priced to perform

For those observant investors, it is noteworthy to see where the market has placed ZBH relative to peers. ZBH is a name I have covered extensively with analysis back to 2020, and I believe ZBH could be at a turning point with the latest set of quarterly numbers. Using the list of comps seen in Figure 2, ZBH neither stands out or completely falls behind. Reminder, this isn't a group that's done overly well these past 12-months. Both Hologic ( HOLX ) and ZBH lead the way here with price returns and fundamentals. I recently rated HOLX a buy with a recent note by the way, you can see it here. I'd also add in Stryker Corporation ( SYK ) for comparisons here as well, although not shown in the graphics.

A few observations of note:

- ZBH has grown earnings at a negative rate of 41% these past 3-years. I believe it could do $314mm in earnings this year on NOPAT of $1.3-$1.4Bn, which could inflect well on the stock price.

- It isn't surprising that the market has valued the company at 32.3x forward P/E, ahead of HOLX at 32x, but behind striker at 35x at the time of writing.

- Related to the above, investors are still paying $32 for every $1 in future earnings for ZBH. I would say this could be fair, with my numbers $43 could even be fair for this long-term compounder.

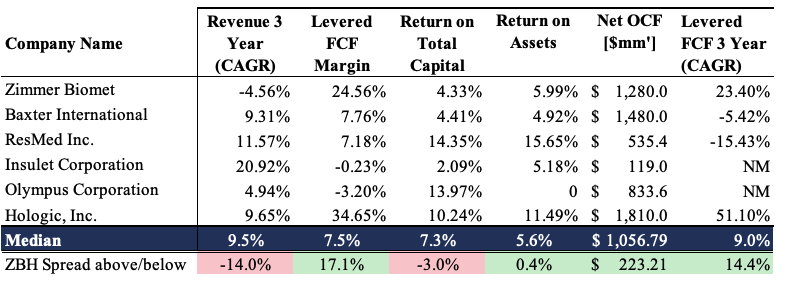

- Taking the median scores of the composite below, Zimmer is ahead of peers in 10 out of 14 measures taken.

- In particular, 3-year FCF CAGR of 23% and 24% FCF margin offsets the 450bps revenue pullback, and outstrips SYK at 3.3% and 9.7% respectively. Still, HOLX takes out the pack in all three metrics.

These aren't unattractive measures for ZBH by any means. But it does fall short on several comparisons. Naturally, when pricing the risk for this company, these must be factored into the debate. More importantly, a thoughtful analysis to see what expectations the market has priced into ZBH's current market cap, to see what could be missing. If so, what reasons are there to expect something different from these expectations?

Fig. 2

{kind=link}

Fig. 3

{kind=link}

Catalysts to move the needle

There are several facts I believe the market may have glossed over too lightly in ZBH's case.

First, start with what the market's current expectations actually are. At the $29.13Bn market valuation, consensus expects 2.9% growth in revenue and 2.5% earnings growth this year, 4.05% and 7.1% respectively in FY'24. To hit these numbers, the market is paying $32 for every $1 of ZBH's future earnings, which is 13.6% above the sector, and a premium nonetheless.

In part, you can consider the 23% geometric FCF growth shown above as one factor to this. But I'd refer the following catalysts into the mix as well.

One, the major growth lever for ZBH going forward is its knees segment in my informed opinion. Note, it pulled $1.83Bn in top-line revenues this quarter , with growth across the portfolio. Knees were especially strong however, with 18% YoY growth to $762mm, driven by growth in the installed Rosa and Persona base. Global knees were up 10% in 2022, and with such a strong first quarter ZBH could see upside on this in my opinion. Figure that ZBH expects "no less" than 300 Rosa installations in any given year. This is a tremendous cadence and is almost recurring revenue. It exceeded this last year by the way. I believe it would be reasonable to expect this trend to continue in FY'23. It also has extended the Rosa indication to shoulder, hips and others, as another tailwind.

Two, it is pleasing to see Zimmer innovating around its core knee offerings. In med-tech, patent protection over design and procedure (creating an intangible asset) offers scalability and keeps the marginal cost of the asset's usage low. What really adds torque to this process - speed of innovation. Successful firms persistently innovate around core product segments, do it quickly, and do it well. They then protect each new advancement, thereby monetizing R&D and additional growth CapEx. To this point, ZBH's Persona Osseo and Keel Tibia launches were completed in Q1. The Persona Osseo has a good feature - it allows surgeons to choose between cemented or cementless procedure up until final implantation. This could be an attractive feature as it gives embedded optionality into using the product. Be sure to watch for the early numbers in this product.

That ZBH continues to see the innovation pump moving is a source of embedded alpha in each of its franchises in my view. It sent >50 new products onto the launch curve from FY'18-'22, all in sustainably growing markets. Management expect another 40 products from now until FY'25, all aiming to hit 4%+ growth markets. I'd prefer this versus more M&A from Zimmer, if I'm being honest. For starters, there is strong research suggesting new products with return on capital are superior to creating value for shareholders. Secondly, I believe Zimmer can utilize the capital more effectively vs. M&A by returning it directly to shareholders.

Fig. 4 - ZBH Q1 FY'23 top-line results

Data: Author, ZBH 8-K's

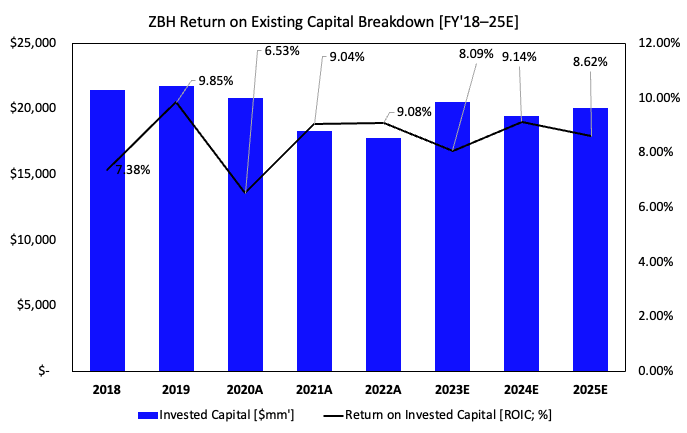

Three, ZBH is a tremendous compounder of post-tax earnings and this trend is poised to continue going forward [see: Figure 6, Figure 5]. Take a step back for a minute, to run your eyes over the business economics:

- Q1 FY'23 knees grew 18.6% YoY to $762mm (growth was 10% in full-year FY'22) and now represents ~42% of turnover.

- This could annualize to $3Bn in knee revenue if my estimations are correct. My numbers have ZBH to do 3.1% growth at the top in FY'23 and clip $7.15Bn, on a flat gross margin of 70.8%, securing $1.33Bn in operating income, or 18.6% margin.

- It wouldn't be unreasonable to see ZBH doing $2.34Bn in core EBITDA and pull this to $314mm in earnings for the year.

These estimates are a scratch above consensus. In the battle for the best top-line, the Street has Stryker to grow revenue 7-8% per year into FY'25, compared to 4-5% for ZBH. This, following a difficult period for ZBH in recent years in getting back to pre-pandemic range of ~$8Bn turnover. Intelligent investors would still be pleased to know that, whilst sales clipped from ~$8Bn in FY'19 to $6.9Bn in FY'22, capital productivity improved from 7.4% to 9.08% ROIC in that time [Figure 5]. This was built from 23% tax-adjusted operating margin and invested capital turnover at 0.4x. Further, ZBH is operating at similar capital intensity to FY'19, albeit on a far smaller capital base ($21.8Bn in FY'19 to $17.8Bn in Q1 2023). My numbers project the invested capital turnover to remain at ~0.4x with after-tax operating margin lifting back to 25% over the coming 3-years. Should this occur, I would expect the market to certainly be hungry for a ZBH feed.

Fig. 5

{kind=link}

Four, in that vein, one might argue these positive expectations are factored into the 11% 1-month rally for ZBH. But there's chance more demand will arrive a little further down the line. You might want to also consider the following points:

- Management updated FY'23 guidance from the Q1 results, now expects 5-6% growth in revenue versus 1.5-2.3% previous. This is actually above my number of 3.1% and calls for $7.35Bn at the upper end of range.

- Gross profit is traditionally steady at 70-71% for ZBH and has headroom to push back to long-term range of 73%+. I believe the unit economics of its knees robotics (inc. ancillary products) are drivers of gross margin because of the tail of income from one unit once installed.

- Central to my investment thesis - ZBH can still compound post-tax earnings for the long-term. In fact, the growth of this firm's net operating profit after tax ("NOPAT") from FY'18-date is superb. Any firm that generates $8.4Bn in cumulative NOPAT over 5-years (like ZBH) tells of a strong ability to create long-term value. I project this to continue, with $1.24Bn in NOPAT anchored this year. This makes for one linear climb when charted [Figure 6] and could continue to ramp if my numbers pull through.

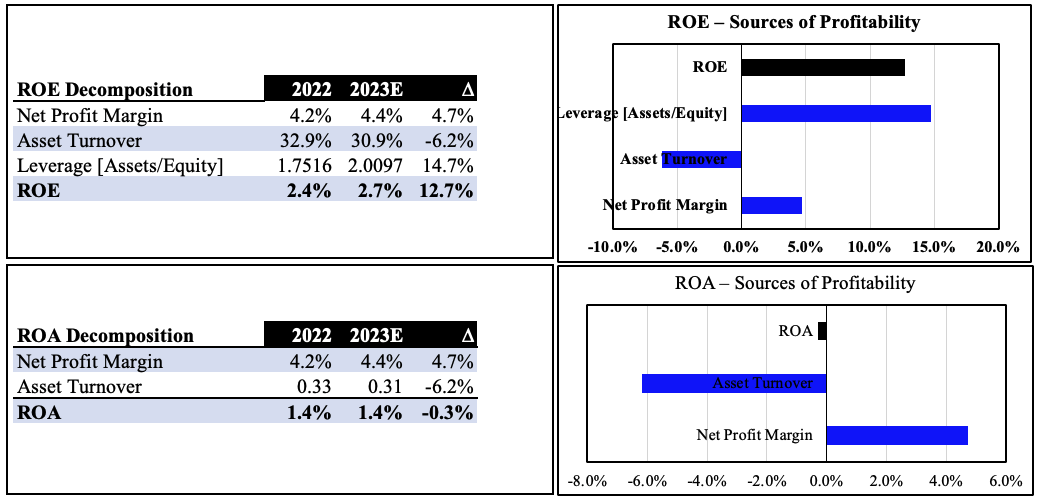

Five, after paring back capital density, the company now has $17-$18Bn in capital currently working in the field. This includes working capital and intangible investments. It is reasonable to see ZBH increasing this base for business growth over the coming 2-3 years, generating profitable revenues. At the current run rate, it is not unfair to see ZBH doing $5-$5.5Bn in cumulative NOPAT into FY'25 and grow by $113mm in my opinion. This could add another point to ROE in 2023, driven by net margin and balance sheet effects [Figure 7]. I would call ZBH to invest $2.3-$2.5Bn on this, slightly below long-term range.

As a potential tailwind, my assumptions call for more capital productivity, and lighter operating capital going forward. By FY'25, I'd be looking for an incremental return on capital of 12.5% from ZBH if all goes according to plan. Assuming an 8% cost of capital (yield composite between the UST 10-year and the S&P 500 forward earnings yield) then ZBH could certainly generate value going ahead. Let's just say, I am expecting to make updates to each of these numbers along the way.

Fig. 6 - The growth in NOPAT is simply superb from ZBH and warrants serious attention [yellow line]. Demonstrates a very good business with very sound economic characteristics that allow it to continue growing each year.

Data: Author, ZBH 10-K's

Fig. 7

{kind=link}

Valuation and conclusion

So far we've discussed many positives for ZBH. Whilst there are many positives, there are negatives too. Chiefly, the price to value axis. If you're looking at a steady-state analysis, ZBH is more than overpriced at 100x trailing P/E (GAAP). Using adjusted numbers, this falls to 19.6x trailing adj. P/E. Neither are hardly a bargain in my opinion. At 15x forward EBIT, this isn't terrible, but could also be considered a negative. You'd want more than 4.9% forward earnings yield if paying either of these multiples in my opinion.

This report dissects ZBH for its ability to grow profits and continue adding value for shareholders long-term. The question is, has the market recognized all of the positive notes mentioned on ZBH thus far in its pricing?

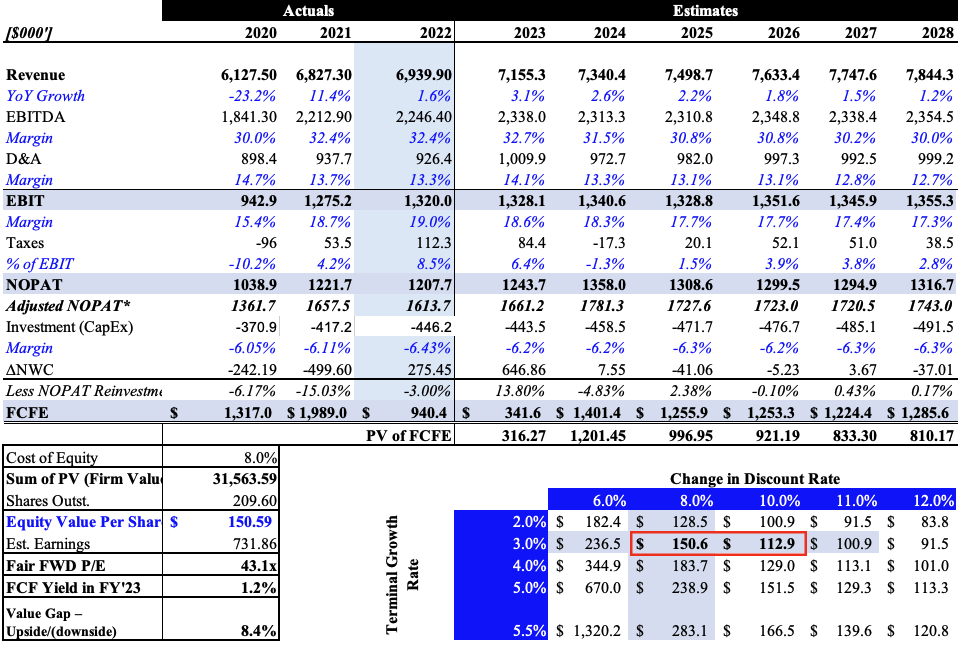

In my opinion, this is best answered in first principles. Regardless of ability, the way ZBH will add value is by throwing off large piles of cash to shareholders. The present value of these future free cash flows comes to $31Bn or $150 per share in my analysis [Figure 8]. This uses an 8% discount rate as previous, 209 million shares outstanding, and looks at reinvesting a portion of NOPAT as additional growth capital. Note, using my FY'23 earnings estimates, ZBH could be fairly valued at 43x forward earnings, considerably above the market's consensus. I would clearly state that, using a 10% discount rate, the valuation is $112 per share, below the market value, and this should be considered too. Hence, the discount rate is important to acknowledge in this appraisal.

From this data, I'd mention these 2 points:

- In my estimation, the market may be undervaluing the free cash flow ZBH can throw off to investors in the future, when using an 8% cost of capital.

- Over the long-term, the market is fairly good at rewarding fair value, and if these forward estimates are somewhat correct, there is a value gap in ZBH's intrinsic value and the current market valuation. Hence there is upside potential to be had in ZBH with these numbers.

Only after putting the points raised in this report together is it abundantly clear. That in mind, I reiterate ZBH as a buy.

Fig. 8

{kind=link}

Pulling all the factors from this report together, it can be best surmised that ZBH has plenty of appeal for the bullish investor. The question of price to value is the elephant in the room. It depends on how one views the trajectory of ZBH's future earnings and cash flows. My numbers project the company to potentially be doing $1.2Bn in FCF by FY'24 onwards and this has high appeal in my playbook. I would see ZBH fairly valued at $150, implying the market has more work to do to see that price target. Net-net, I reiterate that ZBH is a buy.

For further details see:

Zimmer Biomet: Profit Growth Superb, Q1 Knee Growth, But Further Evidence Needed