ZIP - ZipRecruiter: Long Road To Recovery

2023-10-18 05:25:57 ET

Summary

- ZipRecruiter's stock has declined about 64% since its peak in October 2021 due to volatility in the US economy and the tightening jobs market.

- The recruitment industry is facing significant headwinds and uncertainty, leading to a decline in ZIP's revenue.

- We expect job listings to continue declining in the next few quarters but anticipate revenues to start accelerating in the second half of 2024.

Investment Thesis

ZipRecruiter (ZIP) has been quite volatile since its debut in early 2021 as a result of volatility in the US economy and tightening jobs market with the stock declining about 64% since it peaked in Oct 2021. We believe the company is likely to report a 12% EBITDA CAGR during the 2021-2025 period, however, there are significant uncertainties as a result of persistent inflationary pressures and extreme caution by recruiters. The recruitment industry is likely to witness significant headwinds and uncertainty in the near term and we remain on the sidelines as we believe the current discount is warranted due to a challenging macro backdrop. Initiate at Neutral.

Company Background

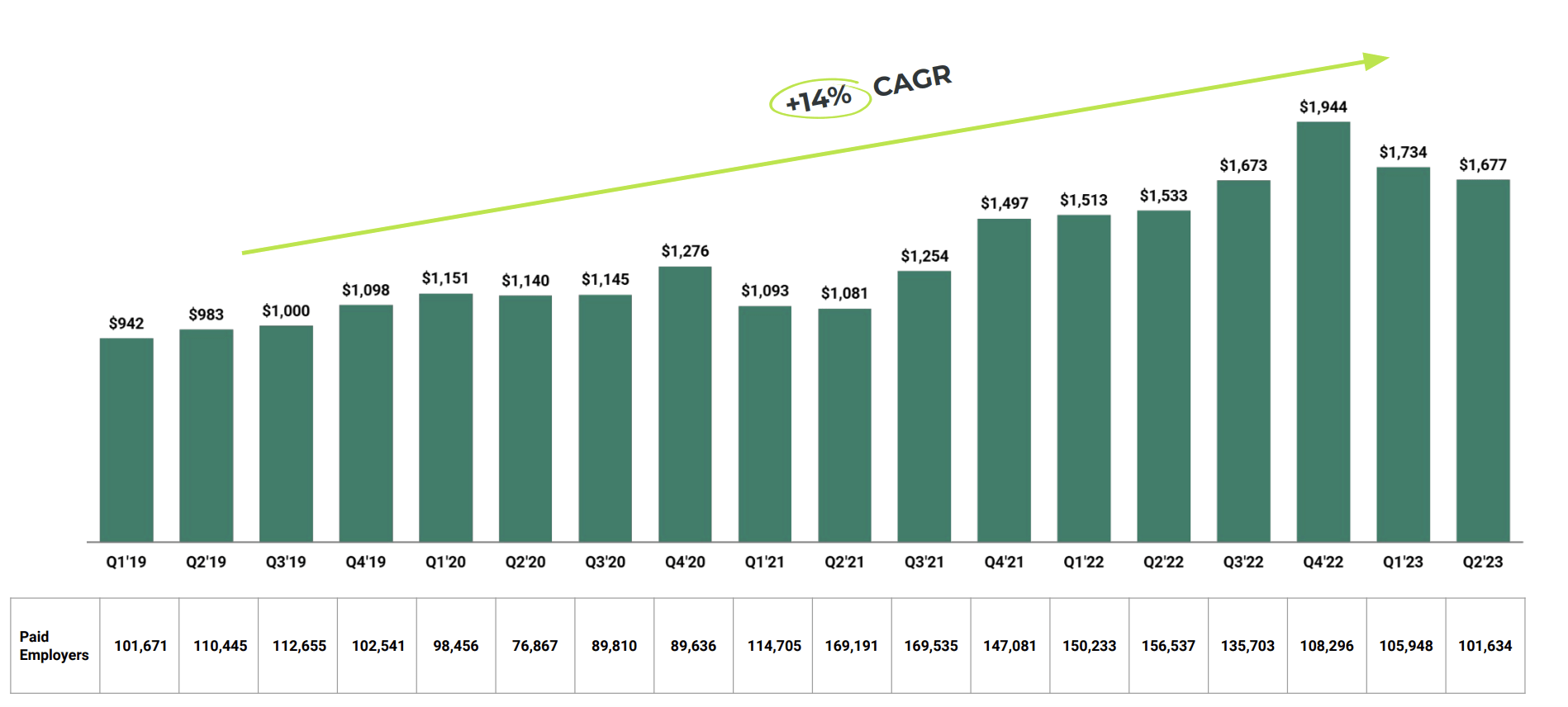

ZipRecruiter is a two-sided marketplace that connects job recruiters with job seekers offering curated job opportunities and candidates for employers. Since its inception, it has served over 3 mn employers connecting with 150 mn+ job seekers. It boasts over 100k in paid employers with average quarterly revenue of ~$1,700, as of last quarter. Its business model is largely reliant on a fixed cost model (80% of total revenues) where employers pay a subscription fee along with a variable model including payment basis cost per click (20% of total revenues). The company estimates that US the employment and staffing temp market is about $280 bn annually of which online is just ~$17 bn (6% penetration). Within online, it has a market share of 30% with the top two players being LinkedIn and Indeed.

Weakening Macros

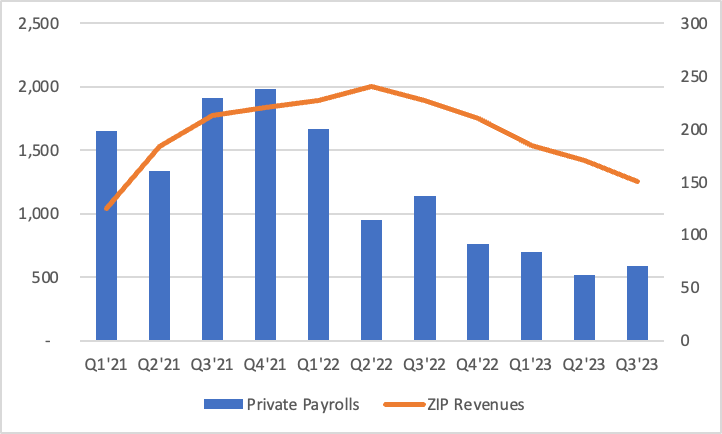

ZIP's revenues are highly correlated with new job listings and macroeconomic scenarios. It has witnessed strong growth in revenues during the period post COVID as a result of uptick in the new jobs post the COVID-19 reset, however, the recent macroeconomic uncertainty and decelerating addition to the non-farm payrolls tally (excluding government jobs) has taken a toll on its operations leading to a significant decline in revenue.

{kind=link}

Note: Q3'23 consensus revenue estimates for ZIP.

In addition, with the Fed continuing to adopt a 'higher for longer' mantra in the wake of sticky inflation, the jobs market is likely to be slowing. ZIP's business model is particularly affected as it has significant exposure to small and medium business customers which are first to pull out during a slowing economy.

Jobs data has been inherently correlated with GDP growth as seen historically, and the expectation of real GDP slowing to 2.2% in 2023 and further falling to 0.8% in 2024 would mean a relatively slow pace of improvement in hiring activity. However, labor market is expected to be persistent due to shortages in some industries but the tightness is likely to linger over the coming quarters. Indeed laid off about 15% of its workforce as a result of decline in job postings and continued uncertainty over the coming few years, while LinkedIn also cut 650+ jobs recently , becoming the second round of its job cuts.

The company anticipates that job listings, which are the company's bread-and-butter, will continue to decline in fiscal years 2023 and 2024. Last quarter, US total job openings were down 3.5% year-over-year, while sponsored job volume fell 33%. In the US, we are expecting job openings will likely decrease to pre-pandemic levels of about 7.5 million, or even lower over the next two to three years.

- Chris Hyams, CEO, Indeed ( Source )

Earnings Preview

ZIP had witnessed strong growth in its paid employers number along with revenue paid per employer driven by robust job market growth post-pandemic. Currently, the average revenue paid still remains above the pre-pandemic levels, however, the paid employers have consistently declined and remain near the pre-pandemic levels. In addition, its exposure to small and medium business customers puts them in a more tricky position who face significant volatility in their business and do not have the depth of capital to rely upon.

{kind=link}

We expect the number of paid employers to likely go below 100k as witnessed during the pre-COVID levels and the revenue paid per employer is also likely to trend downwards around ~$1,300-$1,400 witnessed during the start of the post-COVID boom.

Employers continue to respond to the enduring macroeconomic uncertainty with caution. The number of job openings employers' willingness to pay for those job openings has been declining significantly from the peaks of 2021 and 2022. This trend is consistent among both SMB and enterprise customers alike across multiple industries and geographies. We see this as a macroeconomically-driven reality impacting companies across the recruiting space. This results in the continuation of an atypical hiring pattern.

- Ian Siegel, Co-founder and CEO, ZipRecruiter

We further anticipate revenue to continue to decline for the coming quarter and start accelerating in the second half of 2024 with renewed stability in the job markets and expect the revenues to reach around $650 mn. We expect revenues to further accelerate by 20% in 2025 to around $780 mn, just a tad above the 2021 level. We expect operating margins to decline in coming quarters and further expected to reach above 20% margins, translating to annual EBITDA of $164 mn implying a 13% CAGR growth during 2021-2025 period.

Valuation

ZIP trades at 7.8x Fwd EV/ EBITDA which has witnessed P/E derating as a result of significant changes in the fundamentals post-COVID boom. Excluding the COVID anomaly, the company has traded roughly at an average of ~10x EV/ Fwd EBITDA. Given its unique nature of operations, the company does not have a Direct peer, while Fiverr (FVRR) and Upwork (UPWK) can be considered as indirect peers, however, both companies are essentially beneficiaries in the slowing jobs market which results in a boom in the freelancing market and hence is not a proxy to ZIP's business model.

We believe that given the significant uncertainties in the economy as well as the overall jobs market, there are significant downside risks to an investment in ZIP despite it trading at a relatively lower valuation. We believe the discount is warranted in the wake of stubborn inflationary pressures and significant headwinds within the online recruiting industry and initiate at Neutral.

Risks to Rating

Risks to rating include

1) Any adverse change in the macroeconomic scenario and possibility of a recession can significantly impact the labor market

2) The company may have to resort to lowering its subscription fees in the wake of arresting a decline in its user base

3) The Fed could increase the rates further which can further impact economic growth and labor markets

4) Upside risks include a resilient job market and resumption of strong hiring activity which can accelerate job listings and top-line growth

Final Thoughts

ZIP had volatile earnings since listing as the COVID boom led to significant acceleration in its top line and bottom line growth while the pandemic reset and tough labor market led to the plummeting of its business. We believe there is still significant uncertainty in the overall jobs market as a result of looming recessionary fears. In addition, the consensus estimates $650 mn in revenue for 2024 and while we believe the revenue will likely accelerate about 20% in 2025 to ~$780 mn, this still remains just a tad above the 2021 levels. We Initiate at Neutral as a result of pronounced downside risks and continued uncertainty in the overall economy.

For further details see:

ZipRecruiter: Long Road To Recovery