IDXX - Zoetis: The Animal Drug Monarch In The Era Of Soaring Companion Animal Demand

2023-07-19 18:40:53 ET

Summary

- Zoetis, a global leader in animal health, has seen significant growth since its spin-off from Pfizer, particularly in the companion animal sector due to increased pet ownership.

- Key risks for Zoetis include potential animal plagues, distributors destocking companion products, and the expiration of drug patents, which could all impact growth.

- I believe the animal health industry is more attractive than the human drug industry due to significantly less competition.

Zoetis ( ZTS ) is the global leader in animal health, specializing in animal drugs, vaccines, and diagnostic products. While many people are familiar with pharmaceutical companies focused on human health, the field of animal drugs may be less well-known.

Since its spin-off from Pfizer (PFE), Zoetis has made significant investments in the animal health sector, introducing industry-leading drugs and improving their business efficiency. With an increasing number of individuals choosing to have companion animals at home for emotional support, this trend provides a structural growth tailwind for Zoetis's business.

Investment Thesis

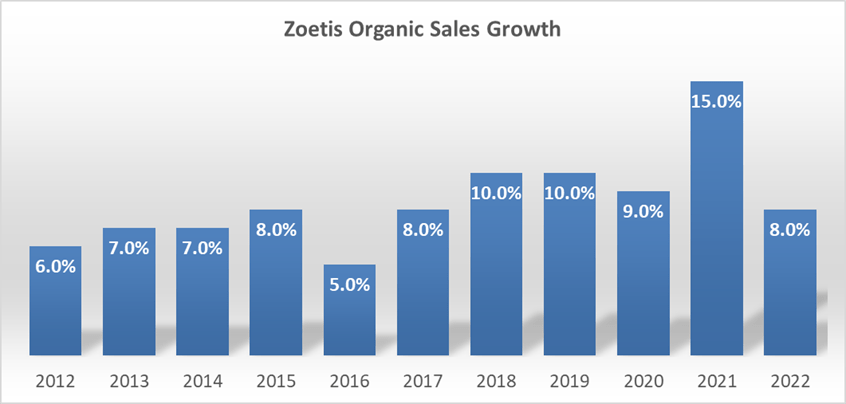

Since its spin-off, Zoetis has experienced substantial organic growth. The animal health industry as a whole is estimated to be growing at a rate of around 4-5%, and Zoetis has successfully captured significant market share over the past few years.

{kind=link}

Industry Leader in Most Product Categories : Zoetis is the industry leader across animal species, and its revenue is almost twice as big as that of its competitor, Elanco (ELAN). I don't believe the competitive landscape will change significantly in the coming years, and I have no doubt that Zoetis will continue to dominate the animal drug industry.

{kind=link}

Thanks to their leading position, Zoetis enjoys much better pricing for their products. Their operating margin was 36% in FY22, which is an extremely high figure in my opinion.

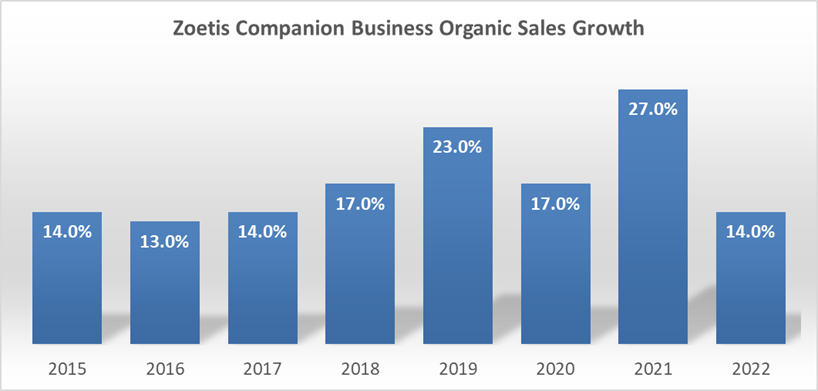

The Human-Animal Bond : Zoetis generates 65% of its group sales from companion animals. The companion business has been experiencing double-digit growth in the past, with the growth rate further accelerated during the COVID-19 period.

{kind=link}

The key growth driver for the animal drug industry is the strong human-animal bond. Pet owners are increasingly prioritizing the health and wellness of their animals. This trend is particularly fueled by Gen Z, millennials, and high-income households, who are actively humanizing their pets. According to Zoetis management team, 86% of pet owners expressed willingness to pay any amount necessary for extensive veterinary care for their pets.

Pets play a crucial role in providing emotional support and can help reduce stress, anxiety, and depression in their owners. They offer unconditional love and companionship, which can have a profoundly positive impact on people's mental well-being.

Livestock Business : Livestock accounts for 35% of Zoetis's business. Zoetis provides vaccines, anti-infectives, parasiticides, and food additives to farmers in this sector. However, compared to the companion animal segment, the livestock business has experienced slower growth, with minimal growth over the past four years.

Looking ahead, it is important to consider that the global population is growing, leading to an increased demand for animal protein sources. As a result, the livestock business is expected to continue growing, likely at a rate similar to that of the GDP in my opinion.

Key Risks

Animal Plague : You might still remember the African swine fever outbreak in 2019. The livestock plague could pose significant financial difficulties for Zoetis. Zoetis's livestock organic sales declined by 1% in FY19 and experienced zero growth in FY20. If there are any future animal plagues, they could potentially affect Zoetis's growth, although the risk is of a short-term nature.

Distributors Destocking of Companion Products : In Q1 FY23, distributors in the US began destocking their high inventory. This was preceded by distributors building up a significant inventory in Q4 FY22, in anticipation of price increases and strong market demand. The near-term destocking is expected to have a negative impact on Zoetis's growth. However, I believe that the destocking trend will diminish in the next 2 or 3 quarters, as the end market demand remains robust.

Zoetis has indicated that while their sales into distributors declined in the quarter, their product sales from distributors to veterinary clinics increased by approximately 8%. Furthermore, product sales from retail channels to pet owners saw a substantial increase of about 35%, affirming a healthy pet care market in the U.S. Additionally, clinic visits increased by 2% in the first quarter, marking the first increase since 2021. These factors indicate that the destocking issue is a short-term risk and not a fundamental concern.

Drug Patent Cliff : Like human drugs, animal drugs are also protected by patents, usually for a duration of 20 years. When a drug's patent expires, generic drug manufacturers can enter the market and produce more affordable versions of the medication, resulting in a considerable decline in sales for the original brand-name drug. In the case of Zoetis, their Draxxin products faced challenges from generic and cheaper alternatives in FY22, but the impact has started to moderate in FY23. Therefore, it is crucial to maintain a diversified product portfolio to mitigate the financial impact of any individual patent expiration on the group level.

Q2 FY23 Outlook

Zoetis is scheduled to report its Q2 earnings on August 8th. The ongoing distribution destocking in the US market is likely to continue putting pressure on their companion animal business. In Q1 FY23, Zoetis's US business declined by 1%, and I do not anticipate a recovery in Q2 and Q3 FY23. The US market is a significant market for Zoetis, contributing to over half of the group's revenue.

In terms of historical performance, Zoetis experienced a 9% growth in US sales in both Q1 FY22 and Q2 FY22, which then slowed down to 2% in Q3 FY22. Considering the comparison bases, I believe they might start to see growth in their US business from Q3 this year.

Furthermore, Zoetis has indicated that they observed more destocking activities in April, so they do not expect the US market to recover in Q2 FY23. However, they have already factored in this weakness into their full-year guidance.

It's worth noting that Zoetis does not provide quarterly guidance but instead offers full-year guidance. Considering that the impact of destocking is already known, I do not expect them to revise down their guidance for the full year.

For the year, Zoetis expects revenue between $8.575 billion and $8.725 billion, representing a range of 6% to 8% operational growth. They also anticipate adjusted net income to be in the range of $2.49 billion to $2.54 billion, indicating operational growth of 7% to 9%.

Valuation

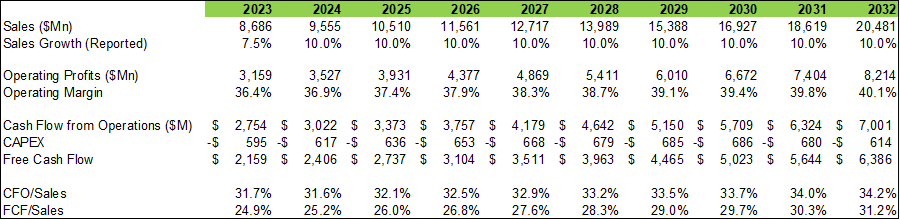

In my DCF model, the growth assumption for FY23 is pretty much in line with Zoetis’s guidance. For the normalized growth, I assume 9% of organic sales growth and 1% of acquisition growth. The operating margin is estimated to reach 40% in FY32 in my model due to operating leverage and higher ASP products launching. The free cash flow conversion is estimated to reach 31% in FY32 in my model. I use 10% WACC, 4% for the terminal growth rate, and 20% for the tax rate.

{kind=link}

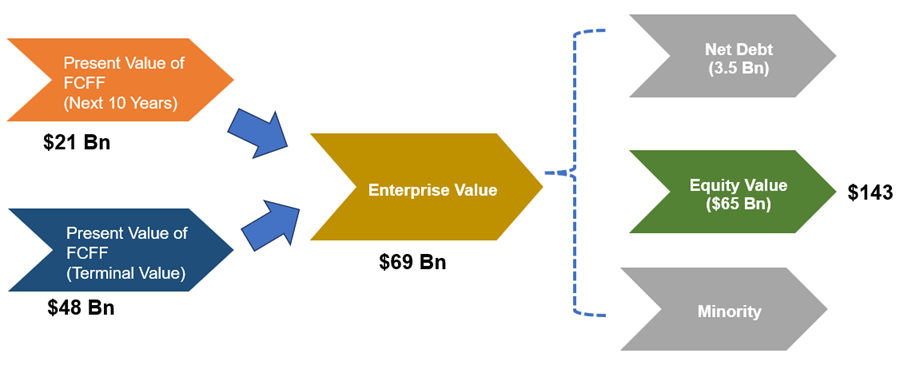

With all these assumptions, the present values of FCFF over the next ten years and terminal value are estimated to be $21 billion and $48 billion, respectively. The enterprise value is calculated to be $69 billion in my model. Adjusting the debt and cash, the fair value is $143 per share, as per my estimate.

{kind=link}

Conclusions

In the animal space, I always view Zoetis and IDEXX Laboratories ( IDXX ) as the two best players. I believe the animal health industry is more attractive than the human drug industry due to significantly less competition. However, I consider Zoetis to be overvalued at its current stock price, and therefore, I assign a 'Hold' rating to Zoetis.

For further details see:

Zoetis: The Animal Drug Monarch In The Era Of Soaring Companion Animal Demand