PANW - Zscaler: Stronger Margins And Wider Enterprise Adoption Will Drive Sustainable Gains In Market Share

2024-01-03 05:06:09 ET

Summary

- Zscaler has outperformed the S&P 500 and Nasdaq 100 in 2023, as the company exceeded revenue and earnings expectations.

- The company is well positioned to gain deeper penetration into its market and see higher adoption across its product portfolio, as enterprise demand for AI workloads grows.

- Zscaler's revenue is projected to grow faster than its competitors, and the company has shown strong financial discipline and improved its cash position.

- Moving forward, I expect to see a 17% upside from its current levels.

Investment Thesis

Zscaler (ZS) has outperformed the S&P 500 and the Nasdaq 100 in 2023. So far, the management has continued to exceed revenue and earnings expectations. As a result, it has led to a higher premium being attached to the price multiple of Zscaler.

While there could be short-term volatility in the stock price, as Zscaler's forward price to earnings multiple is pricing in significant optimism, I believe that over a 10-year investment horizon, there is still room for upside of at least 17% from current levels, which would translate to a price target of $260. I believe that to be the case, as the company is well positioned to gain deeper penetration into its serviceable market and see higher adoption across its product portfolio given stronger enterprise demand to secure their AI workloads.

About Zscaler

Zscaler is a cloud-based cybersecurity company that was built on the premise that rapid cloud adoption and increasing workforce mobility will render traditional perimeter security approaches inadequate in protecting users and data and result in a poor user experience. As a result, Zscaler built its multi-tenant and distributed Zero Trust Exchange ((ZTE)) platform, which represents a fundamental shift in the architectural design in order to enable users, applications, and devices to safely and efficiently authorize the utilization of applications and services based on an organization's business policies.

Zscaler has three core product offerings:

-

Zscaler for Users: Provides users secure, fast, and reliable access to the internet, including SaaS applications.

-

Zscaler for Workloads: Secures workloads in public cloud and private data centers, using cloud-native zero trust access services to provide fast and secure app-to-internet and app-to-app connectivity across multi- and hybrid cloud environments.

-

Zscaler for IoT: Reduces the risk of cyberattacks and data loss by providing zero trust security for connected IoT and OT devices.

In addition, Zscaler was named a leader in the 2023 Gartner Magic Quadrant for Security Service Edge .

The company is focused on expanding its customer base both in the US and internationally. Zscaler leverages a land-and-expand approach with existing customers to sell subscriptions for additional users, additional solutions, and premium solution bundles that contain more functionality.

The Bull Case for Zscaler

Expanding market penetration

Apart from being an early innovator in the cybersecurity space, Zscaler has been an excellent operator in this space, in my opinion. They have shown to have operated with laser focus when it comes to identifying their Serviceable Addressable Market ((SAM)) and moving with urgency to acquire customers and deepen relationships by expanding adoption across their product portfolio.

November 2023 Corporate IR Presentation

{kind=link}

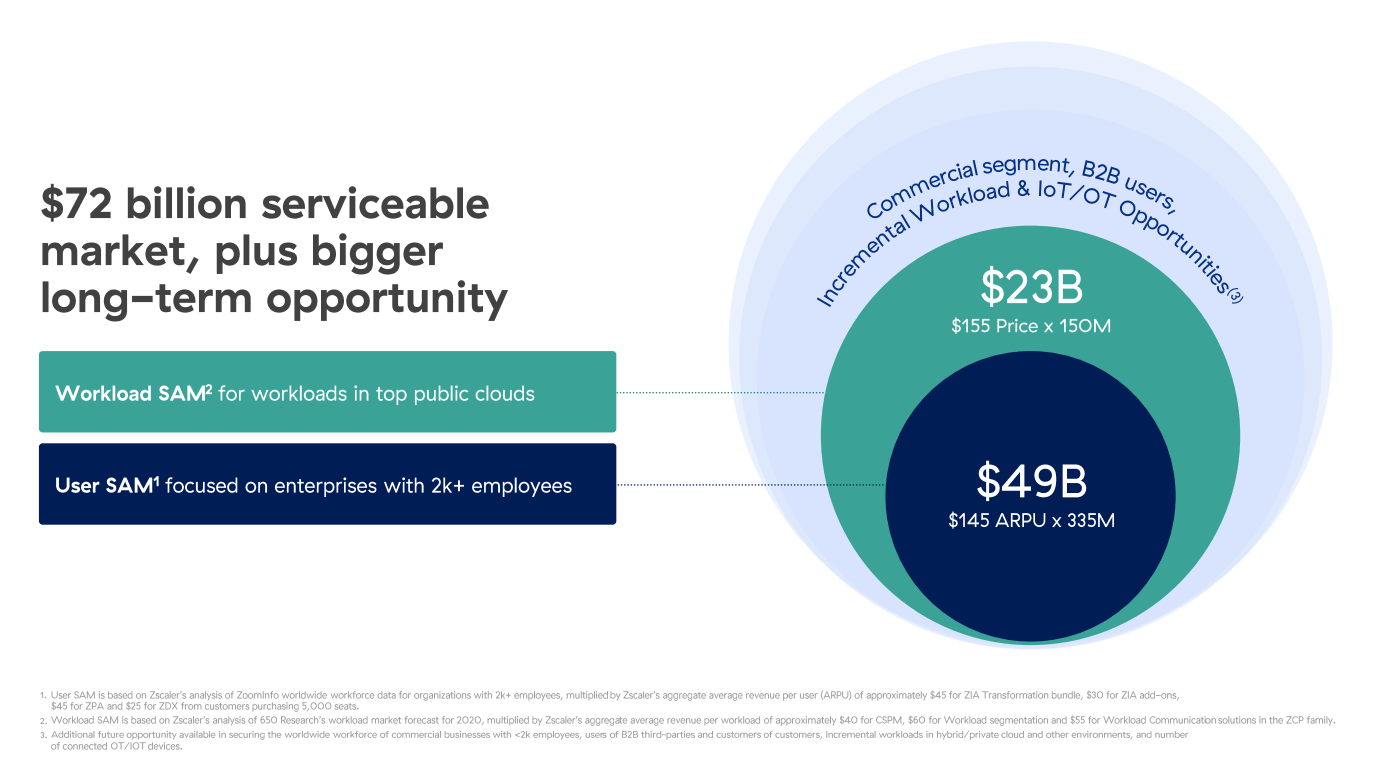

As per their most recent 10K , Zscaler has over 7700 customers distributed across enterprises as well as sovereign entities like governments. Zscaler achieved FEDRAMP authorization, allowing it to sell its ZTE cybersecurity solutions to the US government, directly competing with traditional cybersecurity vendors such as Fortinet ( FTNT ), Palo Alto Networks ( PANW ) and Check Point ( CHKP ). All these developments can be seen as Zscaler deepens its market penetration into its SAM, as demonstrated in the chart below.

Zscaler Analyst Days, Zscaler 10Q's

{kind=link}

From their Analyst Day presentations in 2021 , 2022, and 2023 , I observed that their SAM had remained unchanged at $72B. But their revenue grew over that period of time, which, to me, is a sign that Zscaler is successfully penetrating its serviceable market.

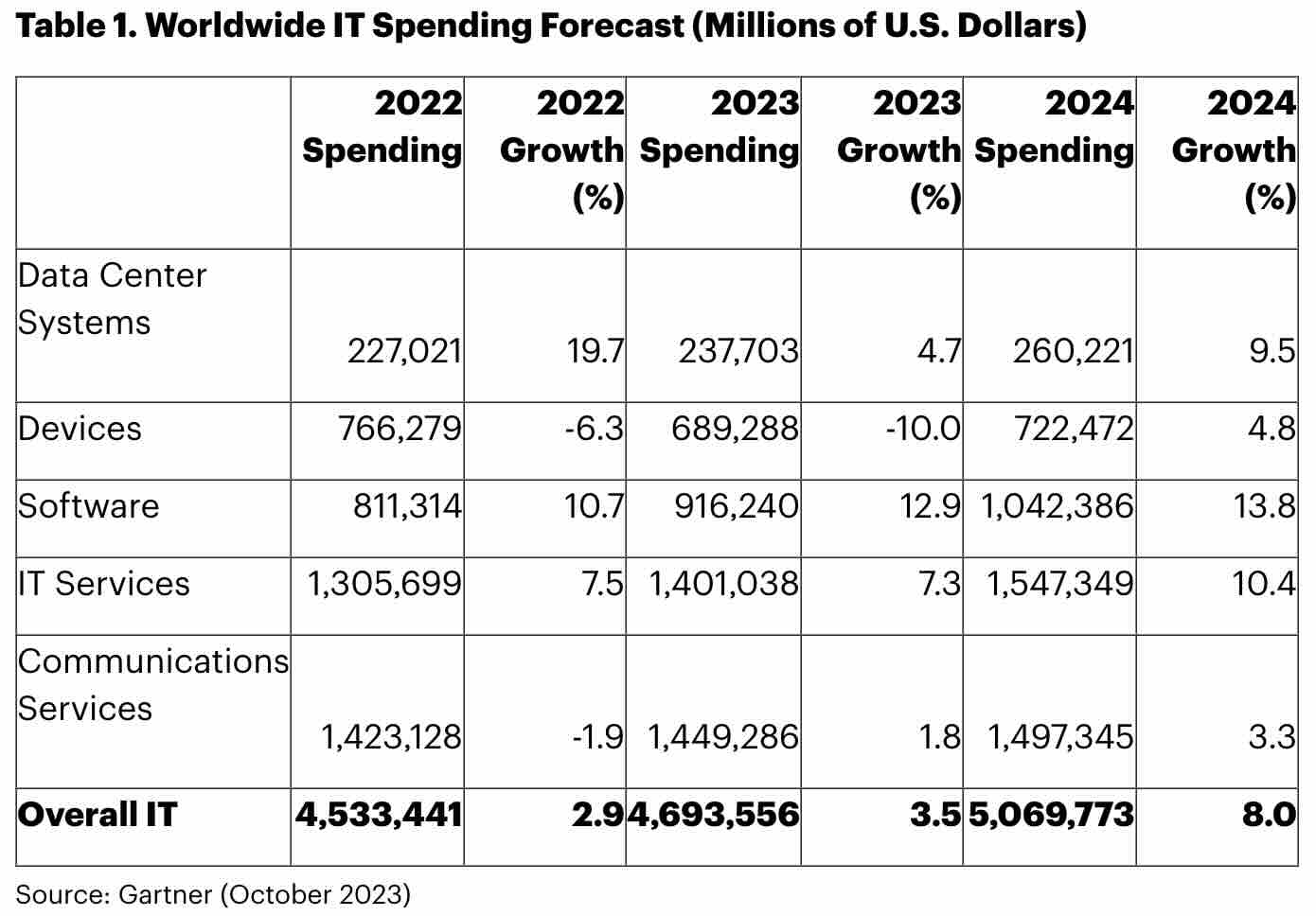

Enterprise spend on cloud-based cybersecurity solutions to lift Zscaler's outlook into 2024

According to a recent research note by Gartner , worldwide IT spending will return to growth in 2024, with spending set to rise 8% YoY. The technology-based research company pointed out that most of the spend in IT will be driven by growing budgets for cloud computing needs, with IT spend towards Cloud Software and IT services growing 10% and 14%, respectively.

Gartner Worldwide IT Spending Forecast

{kind=link}

However, what I found most interesting in the research note was the commentary about how CIOs and technology executives at enterprises were allocating more spend towards bolstering their cybersecurity protection needs. 80% of CIOs reported that they plan to increase spending on cyber/information security in 2024. Here is a quote from the research note that I found actionable for the purpose of this investment thesis:

"AI has created a new security scare for organizations," said John-David Lovelock. "Gartner is projecting double-digit growth across all segments of enterprise security spending for 2024."

Coming back to Zscaler, in the FY24-Q1 call with investors, management noted that the company is well positioned to secure the AI workloads of their enterprise customers. They also noted that by offering AI-specific product bundles, management saw a 20% lift in the average selling price ((ASP)). As more enterprises move to secure their AI workloads, I believe that Zscaler will see significant boosts to their revenue due to the higher ASP lift.

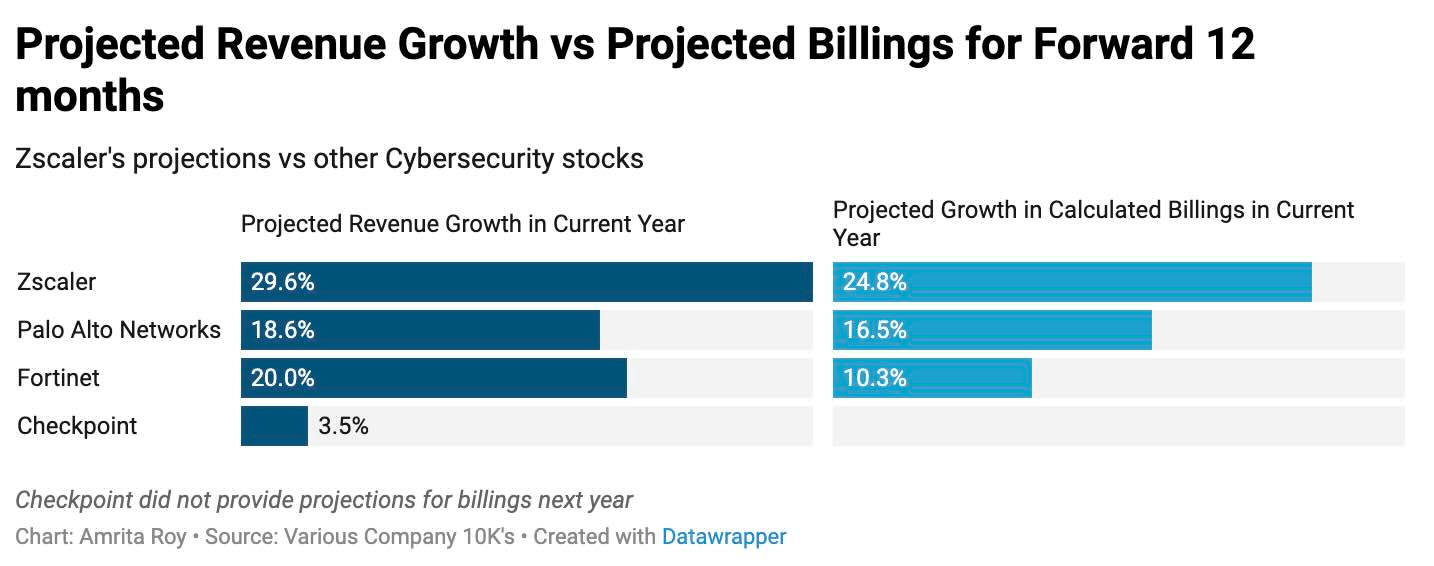

To compare the projected revenue of Zscaler with its competitors, I looked at the forward projections from Zscaler as well as those of its competitors, such as Palo Alto Networks, Fortinet, and Check Point and found that Zscaler is poised to grow its revenue faster than its competitors.

{kind=link}

Zscaler's management continues to drive superior financial discipline

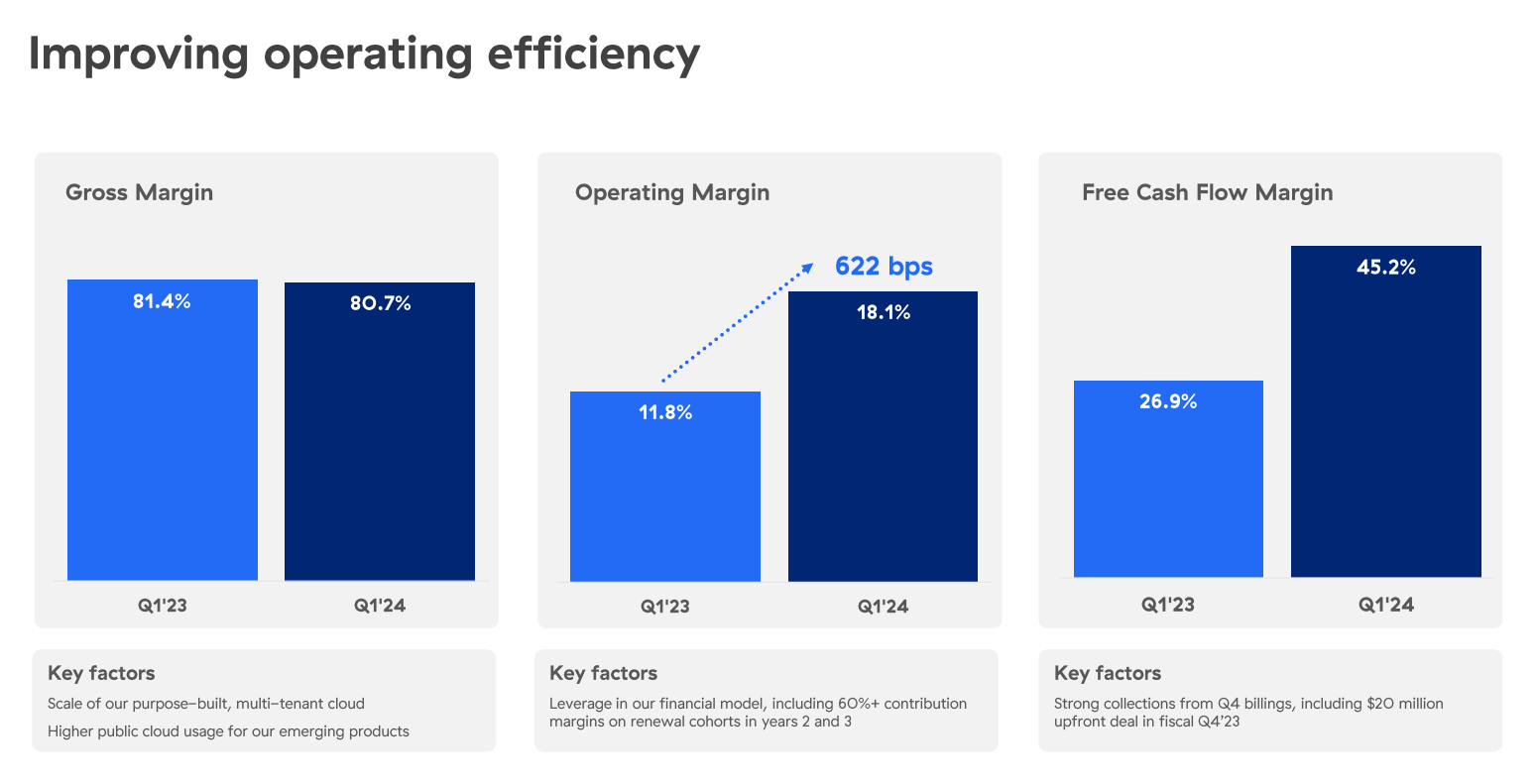

Zscaler produced stellar growth on both the top and bottom lines, smashing expectations by 4% and 36%, respectively, as per its latest Q1 earnings report. Revenue grew 40% YoY to $496M, while non-GAAP operating margin saw tremendous improvement from 11.8% in Q1 '23 to 18.1% in Q1'24. This was driven by streamlining Sales and Marketing spend, which amounted to 63% of Total Revenue in Q1'24 vs. 76% of Total Revenue in Q1'23. I believe that this is indicative of the underlying growing strength of the operational efficiency of the company. As the company grew its revenue by 40% YoY, it also managed to hold its gross margins steady at 80%, driven by the scale of their platform and higher public cloud usage for emerging products.

November 2023 Corporate IR Presentation

{kind=link}

Furthermore, Zscaler has also improved its cash position by 27% on a YoY basis to $2.3B with improved total shareholder equity. In my opinion, this would enable Zscaler to invest in their cybersecurity platform infrastructure with a focus on securing AI workloads. This will continue to drive incremental market share for Zscaler.

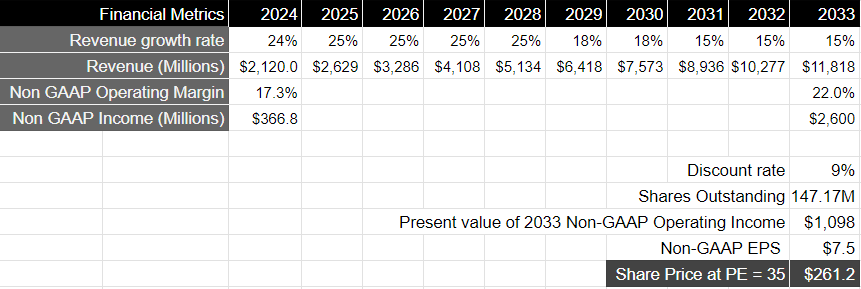

Shifting gears to FY 2024 guidance, Zscaler management is guiding for revenue of $2.1B, which represents a 30% growth on a YoY basis. While this marks a slowdown in revenue growth from prior levels, I believe that given the significant demand for securing AI workloads as well as the penetration into the U.S. Federal agencies customer segment, Zscaler can continue to maintain its revenue growth at the mid-20's level for the next 5 years.

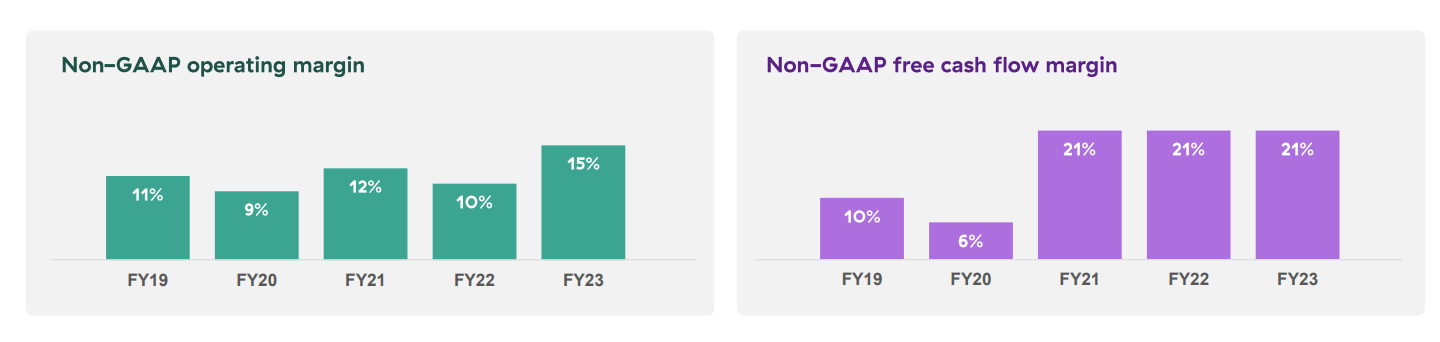

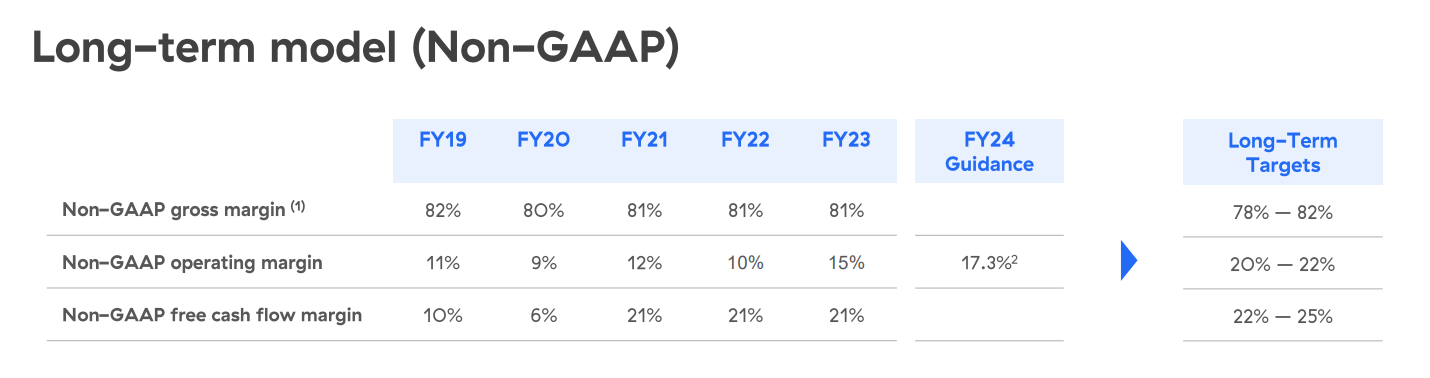

Meanwhile, the management also expects non-GAAP operating income of $365M in FY 2024, which would translate to a non-GAAP operating margin of 17.3%, higher than the non-GAAP operating margin of 15% in FY 2023. One of the things that I particularly like about the company is the management's rigorous financial discipline. Despite being a high-growth company, the management has continually focused on improving profitability, as can be seen below.

November 2023 Corporate IR Presentation

{kind=link}

Moving forward, the management expects non-GAAP operating margin to improve further to 20-22%, which would mean that we can expect non-GAAP operating income to continue to grow slightly faster than overall revenue, which should boost investor confidence further, in my opinion.

November 2023 Corporate IR Presentation

{kind=link}

The Bear Case for Zscaler

Competition Catches Up to Zscaler's cybersecurity technology

The cybersecurity space is a rapidly changing software ecosystem as enterprise demand to secure their internal system perimeters exponentially increases. With the advent of cloud computing and the migration of software into the cloud, enterprise demand has also shifted to securing access to cloud applications.

Zscaler may have had the first-mover advantage by designing their own cybersecurity products suited for the cloud with Secure Access Service Edge and Zero Trust Architecture, but other cybersecurity vendors are catching up. These advancements by Zscaler's competitors may pose real threats to its market penetration if Zscaler's competitors make significant innovation advancements. Legacy cybersecurity vendors such as Fortinet and Palo Alto Networks have already launched cloud-based cybersecurity solutions to compete directly with Zscaler.

What would make it tougher for Zscaler is if cloud computing giants such as Microsoft and Google aggressively pushed their own cybersecurity products to their own existing cloud customers. Both of these cloud titans can bundle their cybersecurity solutions along with their traditional cloud computing products for customers, which could hurt Zscaler's market share. For example, in a rare occurrence, Microsoft's CFO, Amy Hood, shared that Microsoft had achieved $20B in cybersecurity-focused revenue earlier this year. While no other details were divulged as to the underlying type of cybersecurity offering and how this relates to Zscaler's products, it's clear that large companies have huge resources at their disposal to catch up to innovators such as Zscaler over time.

Cybercriminals are able to bypass Zscaler's threat prevention systems

As mentioned in the previous section, the cybersecurity space is always rapidly evolving. One of the other reasons for the scale of innovation that is constantly needed to upgrade the technology is the presence of cyber criminals that are constantly updating their methods to gain unauthorized control of enterprise networks and use their control as ways to extort ransom from enterprise targets. Moreover, the proliferation of AI has allowed hackers to quickly launch different kinds of cyberattacks to take advantage of the enterprise's network. The cost of cybercrime is estimated to reach $10.5T by 2025, which is why most companies are doubling down on securing their networks. However, were cybercriminals able to get past Zscaler's cyber prevention products, it would severely hamper the credibility of Zscaler and have the potential to clinch more deals. We already saw how Okta, an identity protection cloud company that operates in an industry closely related to cybersecurity, saw its value drop -23% over 7 trading sessions in October 2023, right after hackers were able to hack Okta's own internal systems.

Moving forward- I believe Zscaler has an upside of 17%

Zscaler was up close to 100% in 2023, easily outperforming the S&P 500 and the Nasdaq 100. While still away from the all-time high price of $368 that it struck in November 2021, it is still trading at a steep forward price-to-earnings ratio of 90, when its earnings are expected to grow approximately 37% as per management guidance.

If we have to benchmark against the S&P 500, the companies in the index are expected to grow their earnings on average by 10-11% in 2024 . Meanwhile, the index is trading at a forward price-to-earnings multiple of 20. Under the assumption that the US economy continues to grow moderately as per the Federal Reserve's projections at 1.4% with core inflation normalizing to 2.4%, the 10Y US Treasury bond yield should remain anchored at 3.8%. Furthermore, I believe it would be fair to assume that the S&P 500 earnings would come at expectation if the US economy grows moderately as per expectation and avoids a recession. Under those circumstances, I don't expect to see a multiple compression for the S&P 500.

Therefore, if we linearly extrapolate S&P 500's earnings expectation and its forward price to earnings multiple, Zscaler should be trading at a forward price to earnings multiple of no more than 75 for FY 2024. Zscaler is currently trading at a forward price-to-earnings ratio of 90 for FY 2024. That means there could be at least a 20% downside in the short term for the stock. The other way to look at it would be that the current pricing of Zscaler is factoring in the optimism that earnings for FY2024 will surprise at least 20% on the upside. The company has been beating consensus earnings estimates consistently by an average of 15%, and as a result, I believe that the optimism that Zscaler will produce earnings surprises of at least 20% is partially baked into the 2024 price-to-earnings multiple. As a result, should earnings meet management's expectations, I would expect to see short-term volatility in the stock price with the potential for a 20% downside, all things equal. Alternatively, if management once again exceeds earnings expectations above 20%, I believe the stock could have upside from current levels in 2024.

Looking over a 10-year investment horizon, I believe that Zscaler is a buy. I expect the company to continue to produce revenue growth in the mid- to high-twenties over the next 5 years, as it drives further market penetration and slows down to 15-18% between 2028 and 2033. Given management's track record of continuing to improve operational efficiency, I expect operating margins to continue to improve. This is further supported by management's long-term operating margin guidance of 20-22%, as per its analyst day presentation. That would mean that Zscaler produces approximately $2.6B in non-GAAP operating income by the end of 2033, which would equate to a present value of approximately $1.1B if discounted at 9%, or an adjusted earnings per share of $7.5.

Taking the above assumptions into consideration, I believe that the price-to-earnings ratio for Zscaler in 2033 will be around 30-35. Taking S&P 500 as a proxy, where it has grown its earnings by 8% on average over the last 10 years, as per FactSet, with a price-to-earnings multiple in the range of 15-18, I believe that Zscaler should be trading at a price-to-earnings multiple that is at least twice that of S&P 500 in 2033. As a result, I believe that over a 10-year investment horizon, there is room for a 17% rise in the share price of Zscaler to $260.

{kind=link}

Conclusion

There is no doubt that Zscaler has a high premium attached to its forward price-to-earnings multiple. While that can be partially explained by management consistently beating the top and bottom lines, it is possible to see short-term volatility in the stock price. As an investor, I will be watching the competitive landscape very carefully to continue to assess Zscaler's positioning. However, at the moment, my belief is that the company will continue to gain deeper penetration into its serviceable market and see higher adoption across its product portfolio given strong enterprise demand to secure AI workloads. Coupled with management's laser-sharp focus on driving operational efficiency, I believe that the stock has room to climb at least 17% from current levels to $260.

For further details see:

Zscaler: Stronger Margins And Wider Enterprise Adoption Will Drive Sustainable Gains In Market Share