ZTR - ZTR: Remain Cautious Despite Distribution Cut

2023-12-13 20:13:32 ET

Summary

- The ZTR fund cut its distribution in August, as warned in my prior article.

- The new distribution rate should be sustainable in the short term given ZTR's strong performance rebound.

- However, with elevated equity valuations and normalized interest rates, forward asset class returns are poor, and it is unclear how ZTR can maintain a 9.6% NAV distribution yield.

At the beginning of the year, I wrote a cautious article on the Virtus Total Return Fund Inc. ( ZTR ), noting that although the fund paid an attractive distribution yield, the fund's modest returns meant that the ZTR fund was not earning its distribution.

The title of my previous ZTR article was " Balanced Fund With An Unsustainable Yield " and that title proved to be apt, as the ZTR fund slashed its monthly distribution by 37.5% in August, from $0.08 per month to $0.05 per month. To be honest, I take no pleasure in being proven right on the ZTR fund and other similar 'return of principal' funds like the Brookfield Real Assets Income Fund Inc. ( RA ). As I have been writing repeatedly, investors who buy these amortizing 'return of principal' funds are at risk of losing both principal and income, so the best course of action is to recognize the danger and stay away.

Investors were blindsided by ZTR's large distribution cut and punished the fund severely, sending the fund down 14% in the month of September. However, in the last few weeks, ZTR has staged a dramatic rebound and ZTR shares are actually back to pre-distribution cut levels (Figure 1).

{kind=link}

Figure 1 - ZTR has staged a dramatic decline and rebound since distribution cut (Seeking Alpha)

Has the August distribution cut reset investor expectations for the ZTR fund and is it worth a buy now?

Fund Overview

First, a brief overview of the ZTR fund for those unfamiliar. The Virtus Total Return Fund follows a 'balanced fund' model with a 60% target allocation to equities and a 40% target allocation to bonds. The equity portfolio is managed by Connie Luecke of Duff & Phelps ("D&P") and the bond portfolio is managed by David Albrycht of Newfleet. Both D&P and Newfleet are affiliates of Virtus.

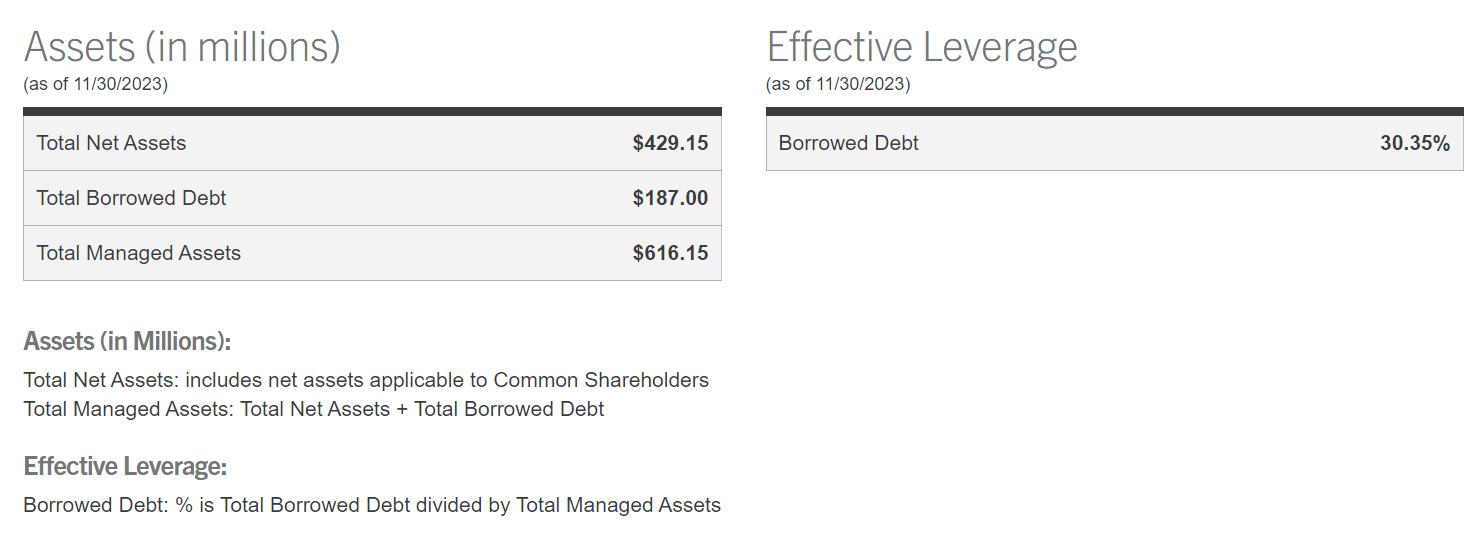

The ZTR fund is fairly popular with investors with $429 million in net assets and charged a 2.26% net expense ratio in fiscal 2022 (Figure 2).

{kind=link}

Figure 2 - ZTR AUM (virtus.com)

Although the ZTR fund has target asset allocation ratios of 60% equities and 40% bonds, the managers do have discretion to adjust the asset allocation as they see fit. As of August 31, 2023, 73% of the portfolio is allocated to equities and 26% is allocated to fixed income (Figure 3).

{kind=link}

Figure 3 - ZTR asset allocation (morningstar.com)

The ZTR fund's equity portfolio is modeled after D&P's global infrastructure strategy. D&P manages the Virtus Duff & Phelps Global Infrastructure Fund ( PGIUX ) with essentially the same holdings (Figure 4).

{kind=link}

Figure 4 - ZTR's equity portfolio is modeled after D&P's Global Infrastructure Fund (Author created with screenshots from virtus.com)

The ZTR fund's fixed income portfolio is modeled after Newfleet's multi-sector core plus strategy. Unfortunately, Newfleet does not offer a standalone multi-sector core plus fund for us to compare fund allocations and investment returns.

Returns Continue To Underperform Low-Cost Balanced Funds...

I have two main concerns with ZTR. First, the ZTR fund has delivered poor long-term returns to date. On a trailing basis to November 30, 2023, the ZTR fund has delivered 3- and 5-year average annual returns of -1.9% and 2.3% respectively (Figure 5).

{kind=link}

Figure 5 - ZTR historical performance (morningstar.com)

Investors should note that Virtus took over management of the fund in 2016 (the fund was formerly called the Zweig Total Return Fund), so historical returns longer than 7 years do not reflect the current portfolio management team.

Figure 6 shows the historical returns of the low-cost Vanguard Balanced Index Fund ( VBIAX ), offered by Vanguard with 3 and 5 Yr average annual returns of 3.0% and 6.2%, respectively. Comparing the two funds, the ZTR fund has underperformed by 4.9% p.a. over 3 years and 3.9% p.a. over 5 years.

{kind=link}

Figure 6 - VBIAX historical returns (morningstar.com)

With Distributions Being Paid Out of Capital

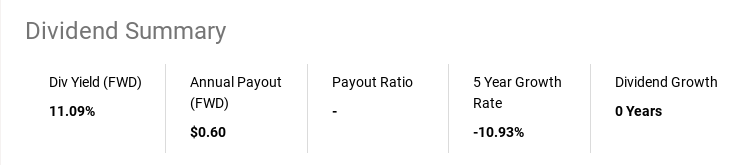

Yet, despite poor returns, the ZTR fund was paying a $0.08 distribution prior to the recent distribution cut. At the current $0.05 / month distribution rate, the ZTR fund is still yielding 11.1% (Figure 7). On NAV, ZTR is currently yielding 9.6%.

{kind=link}

Figure 7 - ZTR is still yielding 11.1% despite cut (Seeking Alpha)

Unfortunately, the large gap between the fund's total returns and its distribution yield suggests that the ZTR fund remains an amortizing 'return of principal' fund that does not earn its yield over the long run.

Short-Term Performance Driven By Loosening Of Financial Conditions

To be clear, ZTR's short-term performance has been impressive, with the fund returning 12.0% on an NAV basis in November, with market performance even more impressive at 14.3%.

This rebound in the ZTR fund was primarily driven by a loosening of financial conditions, as investors pivoted from expecting additional interest rate hikes by the Federal Reserve to now expecting the Federal Reserve to cut interest rates 5 times in 2024 (Figure 8).

Figure 8 - Investors now expect the Fed to cut 5 times in 2024 (CME)

But I Worry About Forward Returns On Elevated Valuations

The problem is that with U.S. equities currently 'expensive' at 19.0x Fwd P/E (and global equities not far behind at 16.0x), it is hard to argue for large forward returns from ZTR's equity holdings (Figure 9).

{kind=link}

Figure 9 - U.S. equities trading at 19.0x Fwd P/E (yardeni.com)

Similarly, with 10-year treasury yields having fallen dramatically in the past month from almost 5% to 4.2% currently, it is hard to see much additional upside in bonds unless the economy goes into a recession and the Federal Reserve returns to zero interest rate policies.

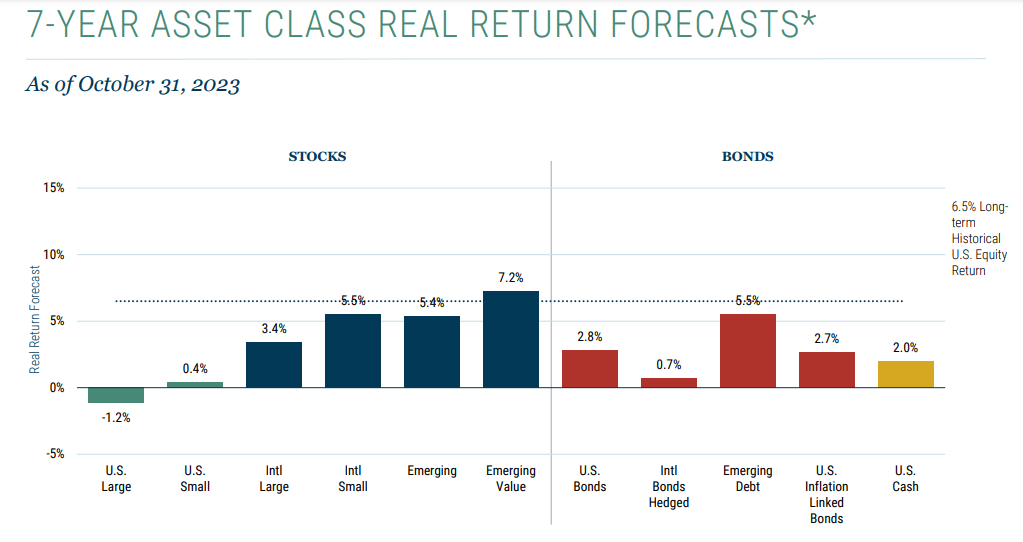

In fact, research from the well-respected institutional asset manager GMO suggests investors should expect subdued future returns for most asset classes as valuations have gotten elevated (Figure 10).

{kind=link}

Figure 10 - 7-year forecasted asset class returns (GMO)

In a low forward return world, I continue to worry that ZTR's 9.6% NAV distribution rate may be too high.

Conclusion

After a distribution cut, ZTR's distribution rate has fallen to an 11.1% yield or a 9.6% NAV distribution rate. In the short run, this distribution rate should be maintained for a few quarters, especially after ZTR's strong near-term rebound.

However, looking further out, I worry ZTR's distribution may not be sustainable as the outlook for asset class returns is not attractive given elevated valuations. I continue to advise caution regarding ZTR's shares.

For further details see:

ZTR: Remain Cautious Despite Distribution Cut