ZUMZ - Zumiez: Still Not The Best Time To Buy The Dip

2023-06-14 01:44:50 ET

Summary

- Zumiez shares are down 33% YTD, but it is still not the best time to go long due to potential continued pressure on financial performance.

- The company's 1Q 2023 earnings showed a decrease in revenue and gross margin, with North America being the biggest contributor to the decline.

- Despite the fact that the company is relatively inexpensive in terms of multiples, I believe that it is necessary to wait for an improvement in financial performance.

Introduction

Despite the fact that Zumiez ( ZUMZ ) shares are down 33% YTD, in my personal opinion, this is still not the best time to go long. Although the stock is currently not expensive relative to historical values, I believe that the financial results of the business in the coming quarters may continue to negatively affect quotes and investor sentiment.

Investment thesis

The company continues to face significant pressure on its financial performance. Based on management's expectations and general economic trends, I believe that the company's revenue will continue to be under pressure in the next quarter, especially in the North America region, which accounts for about 80% of total revenue. Moreover, I expect operating margins to be under pressure due to lower business economies of scale, because most of the operating costs (rent, staff) are fixed. In addition, in line with management comments and general industry trends, we see that inventory levels continue to be relatively high, which could lead to increased promotional activity, which is also negative for margins.

Company overview

The company is engaged in the retail trade of clothing, footwear and accessories for men and women through offline and online sales channels. About 80% of revenue comes from North America, and about 20% comes from Europe and Australia. The company currently has 608 stores in North America, 49 in Canada, 80 in Europe and 21 in Australia. The company's stores operate under the brands Zumiez, Blue Tomato (Europe) and Fast Times (Australia). In terms of brand positioning, the company relies on young men and women who are interested in fashion. The company's stores offer a wide range of brands, some of which are presented exclusively in the chain's stores.

1Q 2023 Earnings Review

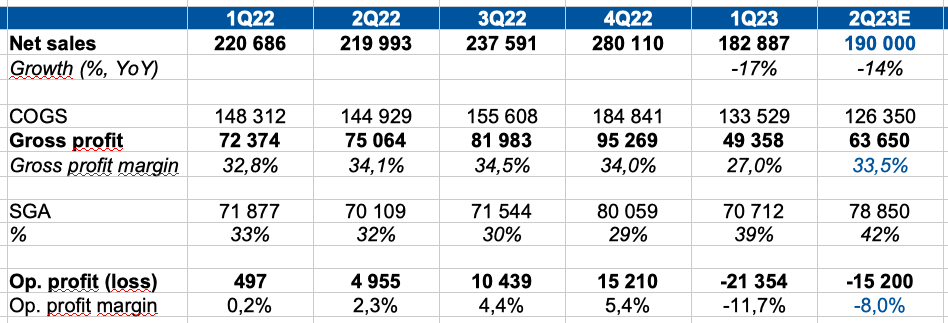

The company's financials continue to be under pressure . Business revenue decreased 17.1% YoY to $182 million. Geographically, North America was the biggest contributor to the decline in revenue, with revenue down 22.7% YoY to $144 million, while Europe and Australia were more favorable, up 13.3% YoY to about $39 million.

While the company cites high inflation and declining consumer spending in the discretionary segment as the main reason for the decline in revenue in North America, I believe it needs to look at a more specific aspect, as revenue in Europe and Australia continues to grow despite the presence of macro headwinds. I believe, based in part on comments from management on the Earning Call, that in the US and Australian markets the company is still gaining market share, and the market segment in which the company operates is less competitive than in the North American market. It is also worth noting the high level of promotional activity in the sector, as a result of which the company is forced to invest in prices, which also negatively affects revenue and profitability of sales.

Gross margin decreased from 32.8% in 1Q22 to 27% in 1Q23 as a result of lower volumes, while most costs are fixed, resulting in reduced economies of scale. Also, as a result, the share of SGA (% of revenue) of expenses increased from 32.6% in 1Q22 to 38.7% in 1Q23, which led to a decrease in the operating profitability of the business.

You can see the details in the charts below.

Company's information (Company's information)

{kind=link}

I would like to note that the company has no debt on its balance sheet, and the amount of cash is $155.3 million, which for me personally is a positive factor in an unstable macro environment.

My expectations

In my personal opinion, the company's financial results will continue to be under pressure in the next quarter. In line with management announcements during the Earning Call following Q1 2023 results , May sales performance, while slightly better than Q1, still remains well below year-ago levels. Management also emphasizes that consumer spending continues to be under pressure.

Thus, I believe that the continued pressure on the consumer will lead not only to continued pressure on the dynamics of revenue, but also on the level of operating margins. Some of the company's expenses, such as rent and staff costs in stores, are fixed, and a decrease in revenue as a result can lead to a deleverage effect, which is negative for business profitability.

In addition, I believe that the increased level of promotional activity in the sector will continue in the next quarter, which may be additional pressure on the product margin. In line with management statements , the company expects sector inventory levels to normalize only in the second half of 2023.

Based on management's expectations for the second quarter of 2023 , which you can see in the chart below, I made my own forecast of financial results.

Company's information (Company's information) Personal forecast (Personal forecast)

{kind=link}

Risks

Promo activity: an increase in promo activity in the sector due to the desire of companies to optimize inventory or increase customer loyalty may lead to the need to invest in prices, which may have a negative impact on the operating profitability of the business.

Margin: decreasing sales volumes can lead to a deleverage effect and put pressure on the operating margin of the business, since most of the costs, such as rent and staff, are fixed.

FX: unfavorable changes in foreign exchange rates may have a negative impact on the dynamics of revenue growth in USD, as more than 20% of the company's total revenue comes from Europe and Australia.

Macro (general risk): high inflation, declining consumer confidence and declining real disposable income could lead to lower consumer spending in the discretionary segment, which could have a negative impact on the company's business growth, especially in North America.

Valuation

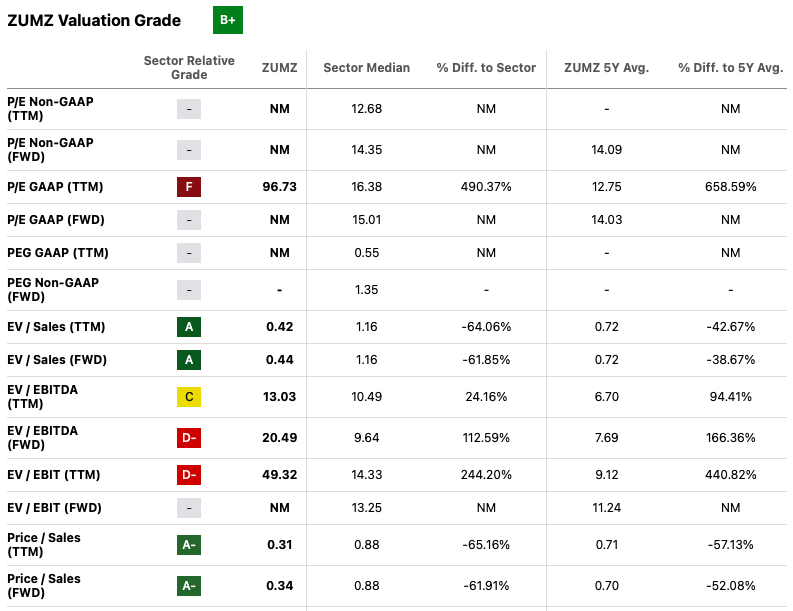

Despite the fact that the company is currently relatively cheaply valued on multiples, I don't think it's worth making a buying decision based on that. For example, according to the P/S ((FWD)) multiple, the company is trading at 0.3, which is significantly below the average value of 0.8, however, in view of the negative economic trends for the company, I admit the possibility of a further decrease in revenue below market expectations and adjustment multiplier. In my personal opinion, it is not worth making a purchase decision only on the basis of a low valuation, it is necessary to wait for fundamental signals of an increase in demand for the company's products, especially in the North America region.

At the moment, it is not easy to talk about the fair price of the company's shares, since the DCF model, which is most preferable for valuing such companies, is too sensitive to the gross margin in the forecast period. In my personal opinion, the company is not valued high in terms of valuation, but the low valuation is due to extremely weak current financials and unclear prospects for the coming quarters.

SA (Valuation) (SA (Valuation))

{kind=link}

Conclusion

Despite the fact that I like the company and its business model, I don't think now is the best time to go long. In my personal opinion, the company's financial results will continue to be under pressure in the coming quarters due to the risk of increased promotional activity, lower revenue as a result of reduced consumer spending and pressure on operating margins due to the effect of deleverage. I will continue to closely monitor the company's Q2 and Q3 2023 financials and management comments and will gladly change my recommendation if I see signs of a normalization in consumer spending and its positive impact on the company's financials.

For further details see:

Zumiez: Still Not The Best Time To Buy The Dip