ZUMZ - Zumiez: Uncompetitive And Declining Rapidly

2023-10-13 00:44:19 ET

Summary

- Zumiez’s revenue has grown at a CAGR of 2% during the last decade, while its EBITDA has declined at a negative 16% rate.

- We attribute the company’s decline in relevance to increased competition, particularly from e-commerce retailers and fast fashion.

- ZUMZ’s profitability is a major concern, with FCF and EBITDA turning negative. We are concerned that the bottom has not been reached and a recovery will be slow.

- Although we consider the industry a tough sell, Zumiez significantly underperforms its peers and so is highly unattractive in our view of fundamentals.

Investment thesis

Our current investment thesis is:

- Zumiez ( ZUMZ ) is a business that has seen its competitive position decline as its industry dynamics have materially changed. We attribute this to its lack of USP; a factor that makes consumers actively choose to shop with Zumiez compared to its peers. Despite the streetwear trend positioning Zumiez to differentiate itself, we have not seen any meaningful improvement. This is an issue that has not been fixed and potentially cannot be.

- We do not believe investors should consider businesses with such a profile, as a significant decline appears inevitable. In Zumiez's case, the company is FCF and EBITDA negative, with the threat that it will never see an EBITDA-M in excess of 10% again (peer average).

Company description

Zumiez Inc. is a leading specialty retailer that offers a unique combination of clothing, footwear, accessories, and hard goods targeted at young men and women. With a strong presence in North America and Europe, Zumiez is known for its curated selection of popular brands, providing a shopping experience tailored to the youth culture.

Share price

Zumiez's share price performance has been disappointing, losing over 30% of its value during the last decade. This is a reflection of a period of difficulty for the company, with declining financial performance.

Financial analysis

{kind=link}

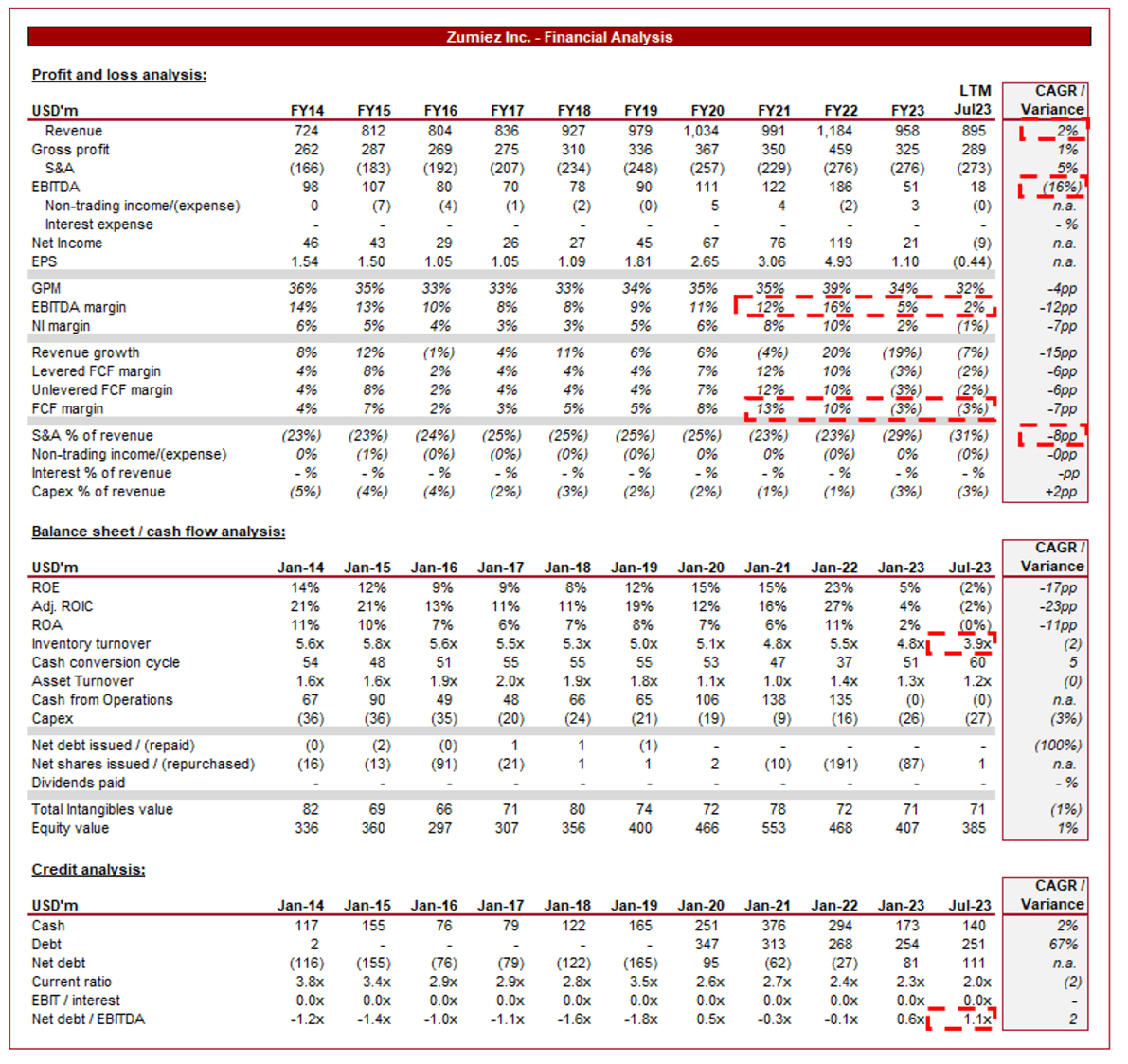

Presented above are Zumiez's financial results.

Revenue & Commercial Factors

Zumiez's revenue has grown at a CAGR of 2% during the last decade, below the rate of inflation. Zumiez has struggled to achieve any level of consistent revenue growth, with three fiscal years of negative growth. In conjunction with this, EBITDA has declined since its FY14 level, at an average rate of negative 16%.

Business Model

Zumiez focuses on the niche market of youth culture, catering to teenagers and young adults. Its products reflect the latest trends in streetwear, action sports, and music-inspired fashion, aligning with the preferences of its target demographic. Beyond this, the company has sought to capture customers outside of its core demographic through the stocking of leading brands, such as Nike (NKE), Vans, adidas, and Converse.

Zumiez offers private-label products and exclusive merchandise collaborations with popular brands and artists. This strategy aims to differentiate the business from competitors, providing unique items that can't be easily found elsewhere. This has been part of the wider streetwear trend, which has taken over fashion during the last decade. Brands are increasingly focused on creating hype and scarcity, which Zumiez's strategy leans into. The issue we see is that Zumiez has been unable to leverage this to drive greater sales in the wider business over time. This suggests a lack of ability to create new, strong relationships with customers.

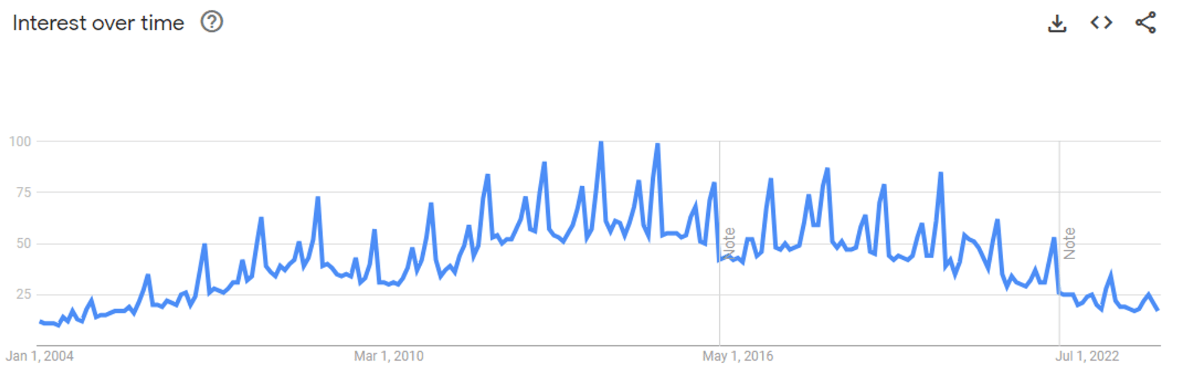

From our research, we understand that Zumiez creates an immersive shopping experience, emphasizing a vibrant and energetic atmosphere within its stores. It often features live music events, gaming zones, and interactive displays, fostering a sense of community. Zumiez has attempted to translate this passion online but we feel it falls flat. The company's engagement online lacks its peers, despite its core demographic being the biggest users. As the following illustrates, interest in Zumiez has consistently declined since ~2015, coinciding with its slowdown in revenue growth.

{kind=link}

Zumiez operates both physical stores and an online platform, allowing customers to shop through various channels. This omnichannel approach is essential in today's retail landscape, as it allows the "traditional" retailers to fight back against the rise of e-commerce. Although we believe this does position Zumiez better, the benefits have not been sufficient.

Zumiez has a solid business model. Its niche focus has allowed the business to develop strong relationships with brands and grow its presence nationally. We are concerned that Zumiez lacks anything material beyond this. There have been numerous opportunities throughout the decade, particularly the rise of streetwear into the mainstream, but Zumiez has seemingly been unable to capitalize.

We see the following three factors as key contributors to offsetting any potential gains:

- Changing Retail Landscape The rise of e-commerce giants, Far East production, and changing consumer preferences for online shopping has posed a material challenge to brick-and-mortar retailers. Consumers now have significantly more choices and less need for loyalty to retailers. Consumers can essentially compare the price of a Nike product across tens of retailers and Nike itself, with no reason to choose Zumiez.

- Fashion Sensitivity - Trends in fashion can be fickle, especially among the youth demographic. This has made the industry incredibly difficult to succeed within, contributing to consolidation to diversify risk. Staying consistently relevant to the ever-changing tastes and preferences of their target market requires agility, constant innovation, and luck.

- Competition - Fast fashion and lower barriers to entry have contributed to increased competition, particularly due to the globalization of supply chains allowing for a rapid reduction in production costs.

Our view is that Zumiez has been able to materially respond to these trends, contributing to a decline in market share.

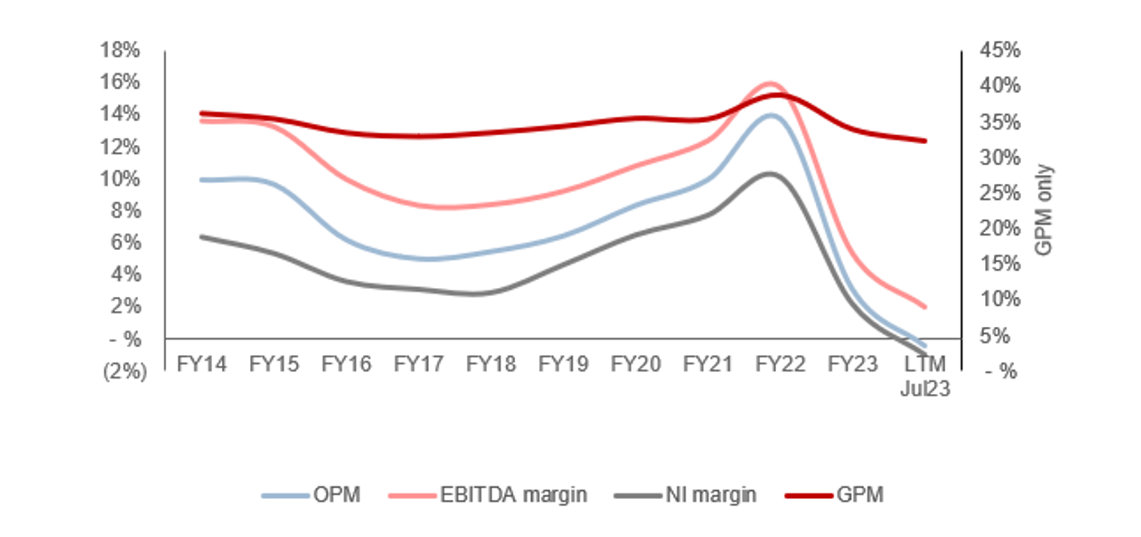

Margins

{kind=link}

Zumiez's margins have experienced a small degree of volatility during the historical period, primarily linked to the level of demand and broader macroeconomic conditions. The company has seen a substantial decline in recent quarters, however, contributing to a complete deterioration in profitability (the reasons for which we will explore following).

Zumiez's "normalized" margins, on the assumption it can return to a double-digit EBITDA level, is a reasonable achievement but does not suggest a strong competitive position. The issue with retailers is that they lack a material moat. Consumers can shop around or go direct-to-consumers, with little downside. Given the competitive landscape will only increase with technological development and globalization, we are skeptical about Zumiez's ability to return to its pre-pandemic levels.

Quarterly results

Zumiez's recent performance has been disastrous, with a rapid deterioration in financial results. The company saw revenue decline by (17.9)%, (19.2)%, (17.1)%, and (11.6)% in the last four quarters (with 6 consecutive quarters of decline). In conjunction with this, margins have sequentially declined, with EBITDA-M turning negative in the last two quarters.

This decline in financial performance is a reflection of the current macroeconomic environment, with inflation and interest rates contributing to a reduction in discretionary spending. This has continued to compound over the last few quarters, as the US has remained committed to bringing inflation under control. We believe market conditions are unlikely to improve until mid-to-late 2024, implying further pain ahead for Zumiez.

Key takeaways from the company's most recent quarter are:

- Management is seeing sales trends improve month-to-month relative to Q1, suggesting it has reached the bottom or that it is impending. The only concern with this is cyclicality.

- The back-to-school season, which is believed to be a good indicator of holiday demand, is showing improvement relative to the last few quarters.

- One of the primary reasons for reduced sales is a heightened promotional marketplace, with Zumiez struggling to compete against increased spending across the industry. This relates back to the company's lack of moat.

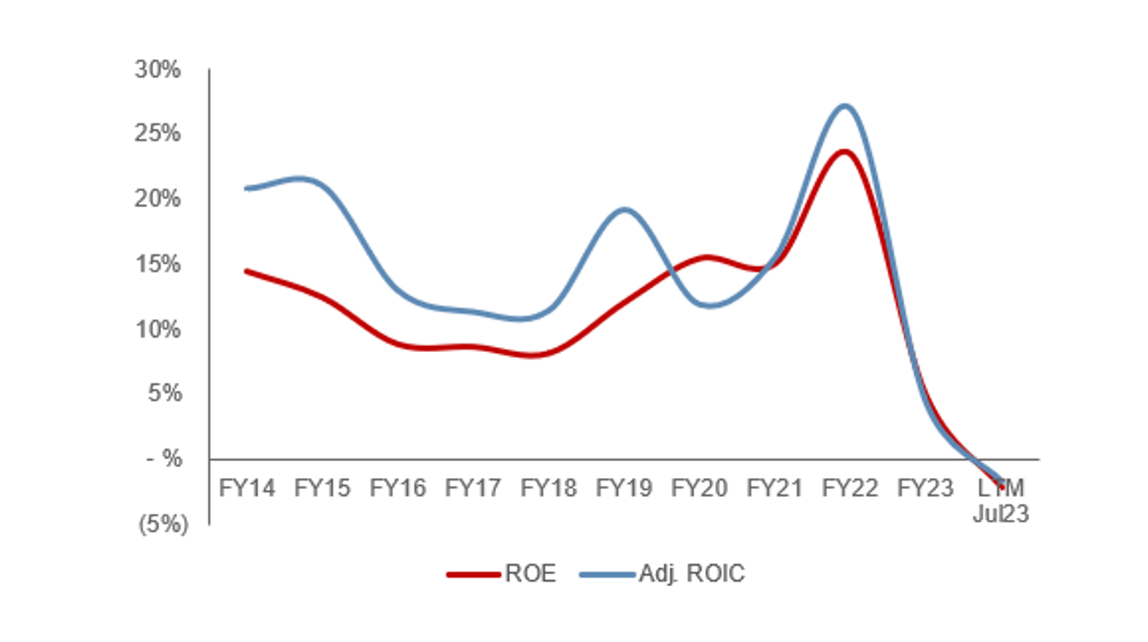

Balance sheet & Cash Flows

Zumiez's balance sheet is relatively clean, lacking reliance on debt to operate the business. This reduces any immediate downside risk, particularly as FCF has turned negative. This is a reflection of declining profitability, as although its working capital position has worsened, it remains at a reasonable level. The inherent issue is that the business is struggling to see goods at breakeven currently.

Historically, the business had generated fairly consistent returns, and at an attractive level. This is a reflection of the inherent risks associated with this industry. Brands and trends change and this risk is only compounded by being a retailer with no moat. A decline such as this feels inevitable.

{kind=link}

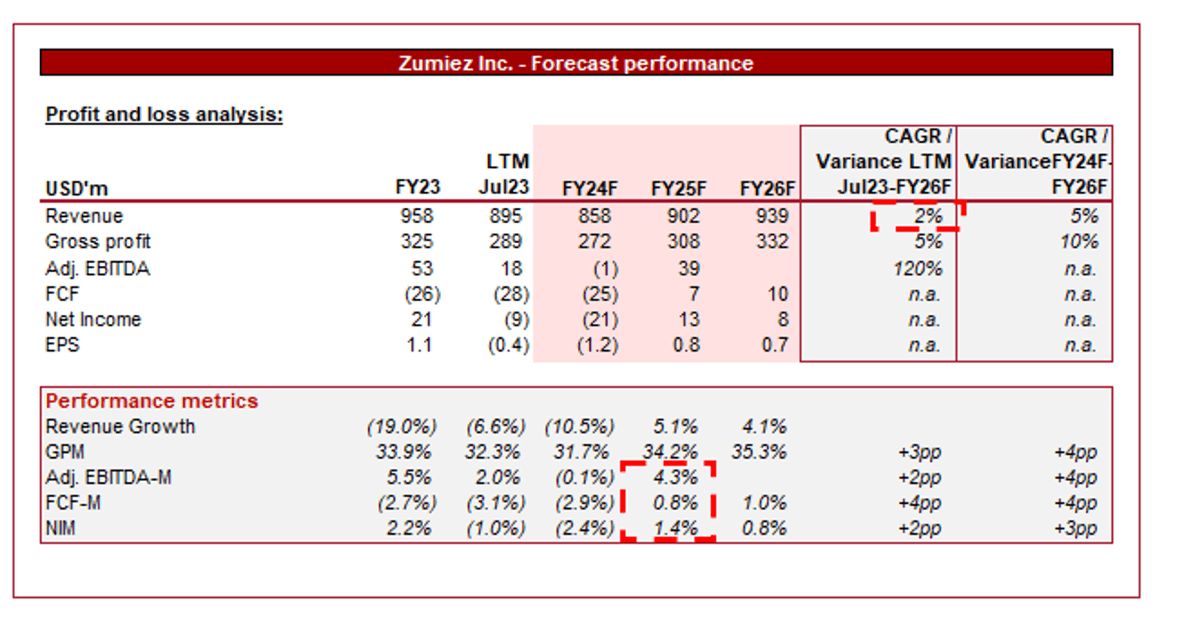

Outlook

{kind=link}

Presented above is Wall Street's consensus view on the coming 3 years.

Analysts are forecasting a continuation of its existing trajectory, with a CAGR of 2% into FY26F. In conjunction with this, margins are expected to gradually improve, with losses for the entirety of FY24F.

These assumptions appear reasonable in our view. Once macroeconomic conditions improve, there will inevitably be a bump in demand as employment improves and expansionary monetary policy returns. This said, margin improvement will not be as easy as expected, with consumers getting used to discounted prices and the ability to shop around.

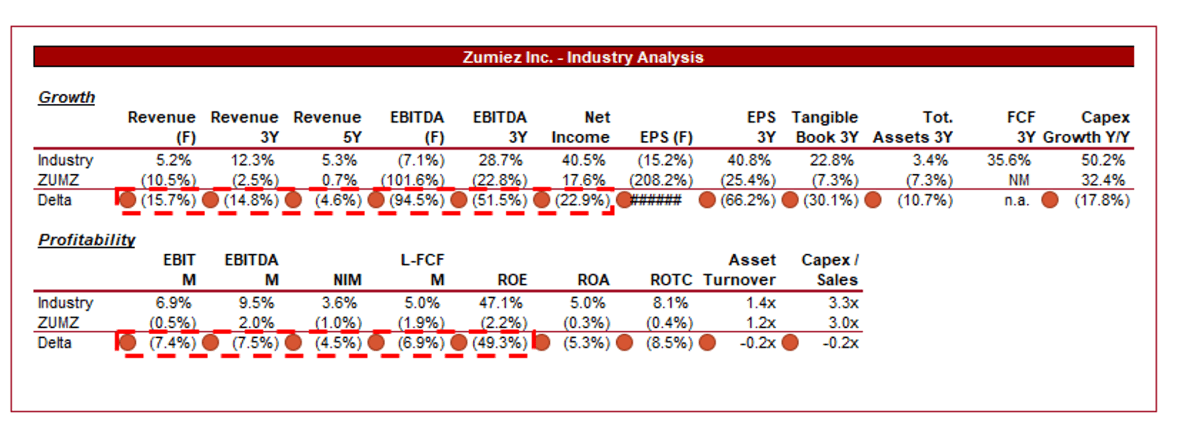

Industry analysis

{kind=link}

Presented above is a comparison of Zumiez's growth and profitability to the average of its industry, as defined by Seeking Alpha (30 companies).

Zumiez is performing terribly relative to its peers. The company is growing at a substantially lower level, even across a longer period such as 5 years. Further, Zumiez is operating with lower margins.

We believe this is a reflection of the company's competitive positioning. The industry cannot be criticized for the depth of its weakness when its peers are substantially better, with a superior forward outlook. The company's niche focus is likely attributable to this. Although consumers resonate with its image, we are unconvinced that price and choice are not still the more important factors.

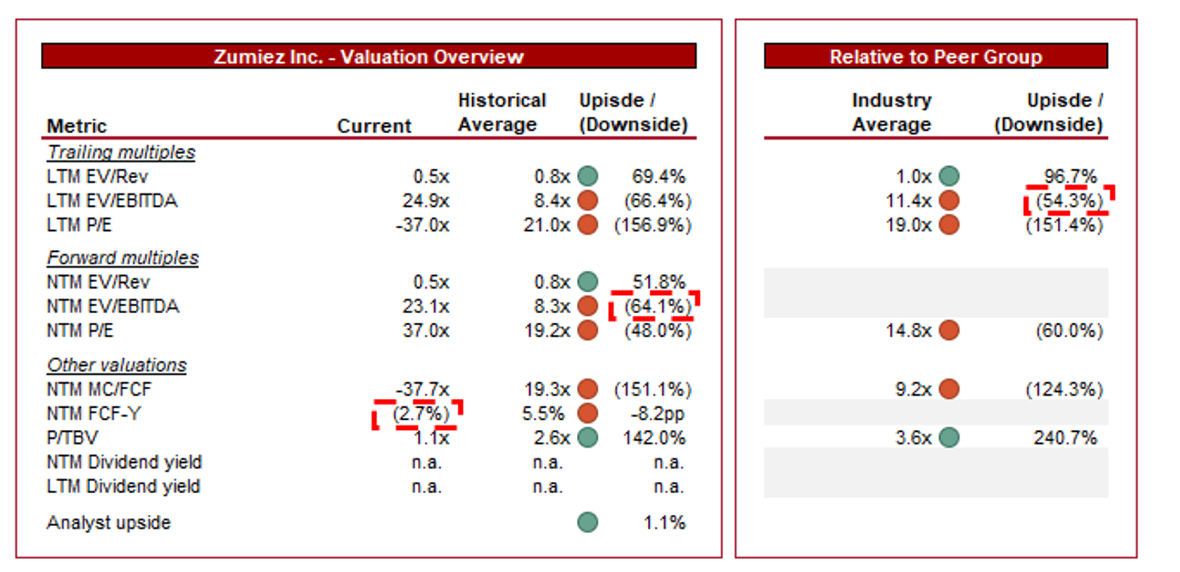

Valuation

{kind=link}

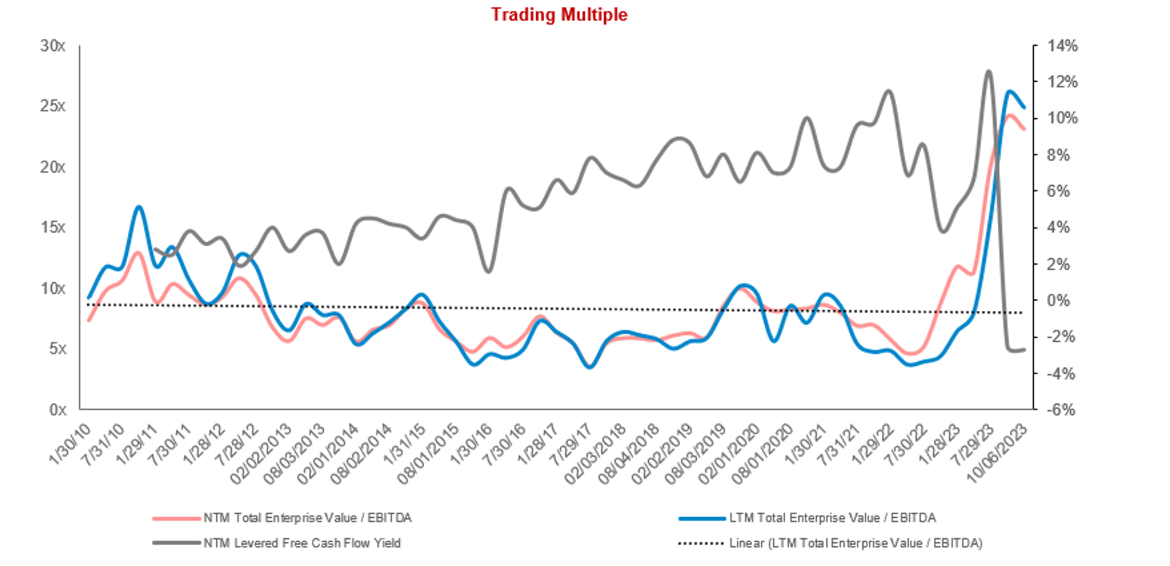

Zumiez is currently trading at 25x LTM EBITDA and 23x NTM EBITDA. This is a premium to its historical average.

Its current premium valuation is a reflection of a spike in multiples following a significant deterioration in profitability. Zumiez's share price has not responded proportionately to this decline. We believe this is a blend of long-term investors and the expectation of a rapid profitability bounce back.

We are completely unconvinced by this business and even that a recovery will be swift. Looking more broadly, however, Zumiez's valuation has incrementally declined since 2010, suggesting even during a period of economic growth and growing popularity in streetwear, this business has not been value-accretive for shareholders. Although its ROE was at a good level, investors saw minimal distributions.

{kind=link}

Key risks with our thesis

The risks to our current thesis are:

- Successful implementation of online marketing strategies - Competition within the apparel retail industry has transitioned online, with success materially driven by the ability to successfully reach consumers through social media and other related avenues.

- Upswing in related trends - Zumiez is a young lifestyle brand, with a strong presence in the streetwear segment. The potential for increased popularity in the segment could bring greater consumer interest.

Final thoughts

Zumiez is a solid business but a terrible investment in our view. The company lacks a material differentiating factor. This has meant it is significantly swayed by industry trends, many of which have acted against traditional retailers. We believe its downward trajectory will continue in the coming years, owing to a lack of commercial improvement.

For further details see:

Zumiez: Uncompetitive And Declining Rapidly