ZFSVF - Zurich Insurance Group: Improving P&C Results Help Drive Growth

2023-10-31 17:18:26 ET

Summary

- Zurich has seen a step-up in underwriting profitability in its core P&C segment in recent years, helping to drive solid business operating profit growth.

- Ownership of Farmers Group compliments its core insurance operations nicely, with revenues and operating profit derived from management fees and therefore largely shielded from underwriting risk.

- On a 15x multiple of 2022 EPS, these shares look priced for double-digit annualized returns over the next few years, given Zurich's growth outlook.

Insurance may be a largely commoditized business, but multinational giant Zurich (ZURVY) stands out in a crowded field, with its composite insurance business complemented nicely by its ownership of the very profitable Farmers Group.

Zurich's ADSs have only returned around 32% from their pre-COVID highs. While that maps to a fairly pedestrian CAGR of around 7.6%, around one-third of that has come from CHF/USD movement with much of the rest coming from the dividend. Said differently, Zurich hasn't seen all that much movement in its underlying shares these past three years. With management targeting 8% annualized EPS growth and the stock trading at a very reasonable 15x earnings, now might be a good time to pick up the shares at a reasonable price.

Improving Record In P&C

My bullish outlook on Zurich has three main sources. First of all, Zurich has a sound and improving track record in terms of underwriting profitability in its core Property & Casualty ("P&C") segment, which encompasses common non-life lines (e.g. car insurance, home insurance and so on), as well as more specialized types of commercial insurance. P&C accounted for around 60% of Zurich's overall business operating profit ("BOP") last year, skewing more to commercial insurance (~75% of 2022 P&C BOP) as opposed to retail (25%).

Zurich has been steadily improving underwriting profitability in its P&C segment. Like all insurers, Zurich's earnings come from two broad sources. The first is from underwriting profits, which is to say retaining more from customer premiums than it incurs in claims-related expenses (i.e. the loss ratio) and on its own operating expenses (i.e. the expense ratio).

Zurich's loss ratio has seen steady improvement in recent years, albeit the year-to-year evolution is quite lumpy because man-made and natural catastrophes are a component of claims costs. For instance, in 2020 the overall loss ratio increased by over 2ppt to 66.4%. This was driven entirely by a big uptick in catastrophes, as COVID-19 (e.g. event cancellations) and civil unrest in the U.S. (e.g. property damage) led to a sharp year-on-year rise in claims. Excluding catastrophes, Zurich's loss ratio has improved by 400bps over the past five years (fig 1).

Fig 1. (Data Source: Zurich Insurance Group Annual Reports)

As a result, underwriting profitability has improved markedly (fig 2). There is a very good chance that these improvements are structural in nature (e.g. driven by data/analytics and digitalization), and so I expect this to be a permanent rather than transient improvement in what is Zurich's largest business line.

Fig 2. (Data Source: Zurich Insurance Group Annual Reports)

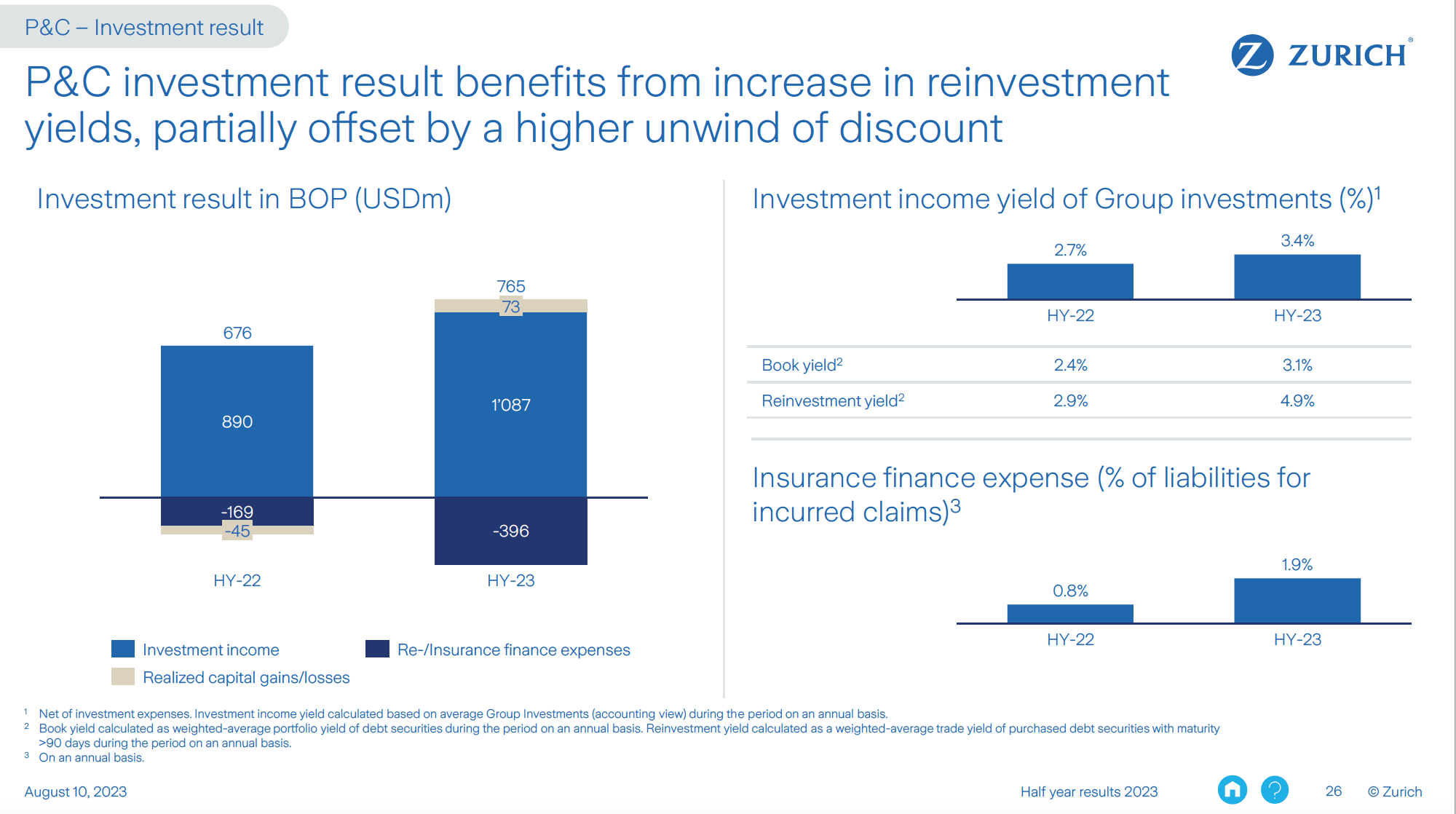

The second source of earnings is investment income. Insurers receive premiums upfront and then pay out claims later on, so they can invest premium cash in assets like bonds to boost returns. Investment income contributed around $1.8 billion to Zurich's P&C revenues last year, but this will increase as higher interest rates create the opportunity to invest at higher yields. For example, in P&C, maturing debt securities were being reinvested with an average yield of around 4.9% in H1 2023 compared to an average book yield of 2.4% in 2022 (fig 3).

Fig 3. (Source: Zurich Insurance Group 1H 2023 Results Presentation)

{kind=link}

If my math is right, this will add around $300 million in extra investment income to its P&C segment this year, which should further act as a nice tailwind to already solid segmental BOP growth (fig 4).

Fig 4. (Data Source: Zurich Insurance Group Annual Reports)

Farmers Group Lifts Underlying Profitability

The second reason I like Zurich is its ownership of Farmers Group. Farmers Group provides services to the Farmers Exchanges, which collectively make up one of the largest non-life insurers in the US (fig 5).

Fig 5. (Source: Zurich Insurance Group October 2023 Investor Presentation)

{kind=link}

Farmers is owned by its policy holders, but Zurich's role through Farmers Group is to essentially provide the mundane services like preparing policy documents. This makes for a nice fee-based business line as Farmers Group simply collects a slice of premiums in exchange for its various management services. This also makes it useful in a period of elevated inflation, as Farmers Group's fees essentially just track the volume of premiums written but without the risk associated with elevated claims costs.

Data Source: Zurich Insurance Group Annual Reports Data Source: Zurich Insurance Group Annual Reports

The key point to take away is that Zurich isn't really exposed to underwriting risk here, and that makes this segments cashflows particularly stable and also high quality. Just to illustrate that last point, Farmers Group contributed around the same to overall group BOP as Zurich's entire life insurance division last year (around $1.9 billion), but with the caveat that is doesn't require anywhere near the capital backing that life insurance products do. This boosts Zurich's overall profitability, and is one of the reasons why management can target a ~20% medium-term return on equity going forward (fig 6).

Shares Look Moderately Undervalued

The final reason I like Zurich is that its current valuation is very reasonable. The ADRs (ticker: ZURVY) trade for $47.60, equivalent to around 15x 2022 underlying EPS.

For the FY23-25 period, management is targeting an 8% EPS CAGR (FY22 base year) and a greater than 20% underlying ROE (i.e. after stripping out things like mark-to-market gains/losses on its investment securities pile and so on). Assuming Zurich does meet its growth targets, FY25 EPS would land around the $40 per share mark (~$4/ADS), which on a 15x multiple would lead to a ~$60 stock.

Fig 6. (Source: Zurich Insurance Group 1H 2023 Results Presentation)

{kind=link}

This looks doable based on the growth drivers I outlined in prior sections, chiefly the structural improvement in P&C underwriting profitability, the tailwind from higher interest rates and the Farmers' fee-based line being linked pretty much exclusively to premiums volume. I would also add that P&C still has some natural growth drivers in it. For example, Zurich's commercial business is dominated by large corporates, with the firm planning on expanding into the middle-market space.

The dividend payout ratio is targeted at around 75% net income, so quick math would imply around $9-$10 per ADS cumulatively over the next three years. Adding that to our $60 target price would make for a total return of around 45% over the next three years, equal to a ~13% CAGR. For Zurich to be at fair value (at a ~9% hurdle rate), I think it would have to trade closer to $53/ADS, leaving the stock around 15% undervalued at the moment. Buy.

For further details see:

Zurich Insurance Group: Improving P&C Results Help Drive Growth