ZFSVF - Zurich Insurance Group: Premium Growth And Low Loss Ratio Encouraging

2023-05-17 19:24:45 ET

Summary

- Zurich Insurance Group has continued to see significant premium growth in spite of inflationary pressures.

- The company's loss ratio also remains below its 20-year historical average, which is encouraging.

- I continue to take a bullish view on Zurich Insurance Group.

Investment Thesis: I continue to take a bullish view on Zurich Insurance Group (ZURVY) due to rising premium demand and a low loss ratio.

In a previous article back in October, I made the argument that Zurich Insurance Group could see further upside going forward on the basis of strong growth across the Property & Casualty segment as well as longer-term return on equity growth.

Since then, we can see that the stock is up by nearly 20%:

{kind=link}

The purpose of this article is to assess whether the appreciation we have been seeing in the stock can continue taking recent performance into consideration.

Performance

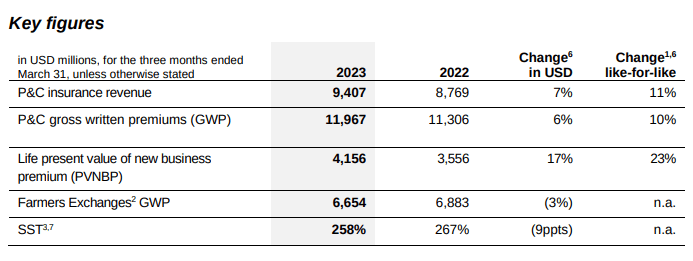

When looking at performance for the most recent quarter , we can see that gross written premiums are up by 10% on that of the same quarter in the previous year on a like-for-like basis (representing the change in local currencies). This was lower on a USD basis at 6% - representing U.S. dollar appreciation against other major currencies over the course of the year.

Zurich Insurance Group: May 2023 News Release

{kind=link}

Additionally, Zurich Insurance Group also saw a strong Swiss Solvency Test of 258% - which remains well above the company's target of 160%.

When comparing premium growth to results for the 12 months ended December 2022, we can see that the combined ratio for the Property & Casualty sector remained constant over the year at 94.3%, while gross written premiums and policy fees were up by 14% on a like-for-like basis:

Zurich Insurance Group News Release: February 9, 2023

{kind=link}

The fact that premium growth has continued into 2023 is encouraging in this regard.

For reference, a combined ratio of less than 100% means that the degree of incurred losses and expenses is less than premiums collected. Given that we are not seeing an increase in the combined ratio in spite of inflation, as well as continued growth in premiums is encouraging.

With respect to inflationary pressures, while retail and SME (particularly the motor business) continued to see pressures from rising costs in the second half of 2022 - this was partially offset by lower weather-related claims and catastrophic losses.

The company forecasts that with price increases starting to take effect and the impact of claims inflation moderating - Retail and SME P&C can be expected to start seeing improved results going forward.

When assessing the profitability of Property & Casualty insurance, another frequently used ratio is the loss ratio. This ratio measures the proportion of loss incurred from the payout of a policy relative to the premium collected for that policy.

For instance, if an insurance company pays out €50 on a policy but collects €100 in premiums for that same policy, then the loss ratio is 50%.

Here is the historical loss ratio for Zurich Insurance Group's Property & Casualty segment from 2003 to the present (assumed to be termed as General Insurance pre-2016).

| 2003 |

| 2004 |

| 2005 |

| 2006 |

| 2007 |

| 2008 |

| 2009 |

| 2010 |

| 2011 |

| 2012 |

| 2013 |

| 2014 |

| 2015 |

| 2016 |

| 2017 |

| 2018 |

| 2019 |

| 2020 |

| 2021 |

| 2022 |

| Loss ratio |

| 73.1 |

| 77.6 |

| 76.4 |

| 70.1 |

| 70.5 |

| 72.6 |

| 70.9 |

| 71.1 |

| 72 |

| 70.3 |

| 68.3 |

| 66.8 |

| 71.8 |

| 66.4 |

| 69.1 |

| 65.4 |

| 64.3 |

| 66.4 |

| 63.1 |

| 63.7 |

Source: Figures sourced from historical Zurich Insurance Group annual reports (2003-present).

To better gauge the potential spread of risk as measured by the loss ratio, a Monte Carlo simulation of 1,000 trials was generated - using a mean of 69.49% and standard deviation of 3.97% as calculated from the historical loss ratios above.

Author's calculations using Python.

It is notable that while the loss ratio saw a mean of just under 70 from 2003 - present, the ratio since 2018 has been below this level. Moreover, Zurich Insurance Group's Property & Casualty segment saw a loss ratio below 65 on 127 out of 1000 trials in the above simulation.

From this standpoint, the fact that Zurich Insurance Group has been keeping its loss ratio below the average seen over the past 20 years is quite encouraging - particularly given the recent pressures of inflation. Moreover, premium demand is continuing to grow quite significantly and higher premium costs as a result of inflation have not been hindering growth in this regard.

Risks and Looking Forward

Going forward, I take the view that Zurich Insurance Group can continue to see growth from here. In addition to a lower than average loss ratio since 2018, we can also see that return on equity has been rising considerably during this time.

ycharts.com

From a valuation standpoint, we can see that the stock looks expensive with its price to book ratio at a 10-year high.

ycharts.com

However, I take the view that given the company's strong performance in the current environment - the stock could continue to see upside interest from here.

One of the risks that I see for Zurich Insurance Group at this point is the potential for a higher degree of catastrophic losses going forward if weather-related claims see a sudden increase. To date, higher inflation has been partially offset by a lower degree of catastrophic losses, which has contributed to growing profitability in spite of pressure on costs and expenses. However, a higher degree of catastrophic losses could tame profitability growth.

With that being said, the company's loss ratio has not exceeded 70 since 2015, and I take the view that Zurich Insurance Group can continue to see growth even if weather-related claims see an increase from here.

Additionally, while premium growth to date has been impressive - crop volumes are expected to decrease in 2023 as a result of commodity price fluctuations. It is notable that crop insurance contributed almost 40% of the like-for-like growth of 14% in gross written premiums for the North American market. As such, lower volumes this year could also mean that we see a risk of moderating premium growth across North America.

In spite of these risks, I take the view that given the company has delivered its highest profitability since 2007 and proposes increasing its dividend to CHF 24 per share - investor interest in the stock is likely to continue and a continued rise in operating profit seems plausible.

Conclusion

To conclude, Zurich Insurance Group has seen significant growth over the past seven months and has demonstrated a lower than average loss ratio in spite of inflationary pressures. I continue to take a bullish view on Zurich Insurance Group.

For further details see:

Zurich Insurance Group: Premium Growth And Low Loss Ratio Encouraging