ZWS - Zurn Elkay Water Solutions: Growth Not Accretive To Shareholder Value Hold

2023-09-14 02:10:35 ET

Summary

- Zurn Elkay Water Solutions Corporation has shown positive growth trends following its Elkay acquisition, but this doesn't appear to have added immense shareholder value.

- The company's economic performance has been soft, with a low rate of return on investments and negative economic earnings.

- Multiples appear stretched, and the market looks to have priced ZWS fairly at its current marks.

- Net-net, rate hold.

Investment summary

Zurn Elkay Water Solutions Corporation (ZWS) has exhibited positive growth trends across 2023 following its Elkay acquisition last year. Deeper analysis reveals the economics on this growth hasn't necessarily added shareholder value.

ZWS is a water management pure-play. It boasts an extensive product portfolio with offerings in water safety and control, flow system solutions, environmentally-conscious and hygienic products, alongside various drinking water products.

This report will unpack the moving parts of the ZWS investment debate, linking this back to the broader hold thesis. There are multiple challenges I've identified that don't align with our core investment tenets. Chiefly, the company's new capital base isn't returning the kind of earnings we'd need to advocate buying this name. Further, the market may have priced the stock correctly at its current levels, keeping the economic performance in mine. Net-net, I rate ZWS a hold, noting weakness in its economic performance the last 12 months. By all measures presented here, these trends could persist going forward. Rate hold.

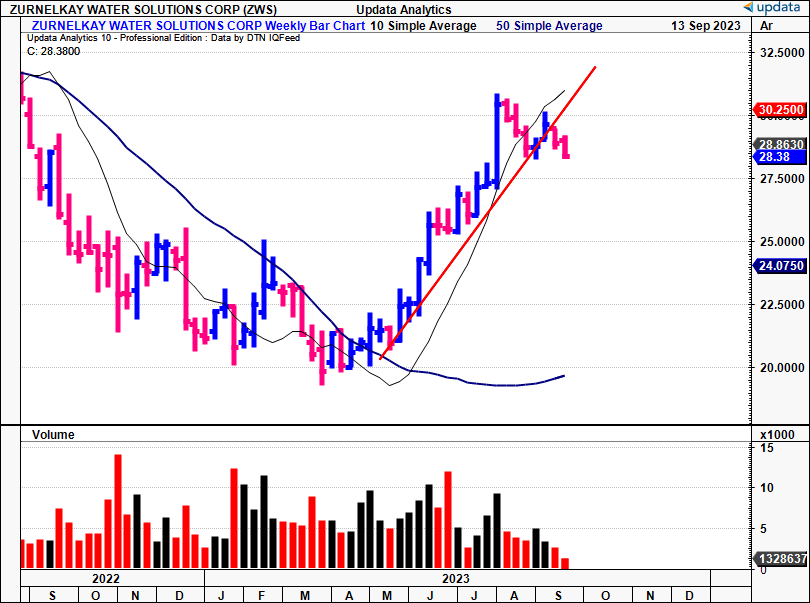

Figure 1.

{kind=link}

Critical investment facts to hold thesis

Overview of recent developments

ZWS put up Q2 revenues of $403mm , up 42% YoY, on core EBITDA of $83mm and operating cash flow of $87mm. Given the momentum this YTD, management has revised its forecast for the year, now forecasting sales between $1.5Bn-$1.55Bn on adj. of EBITDA $345mm at the upper bound. It is eyeing FCF of ~$215mm on these numbers.

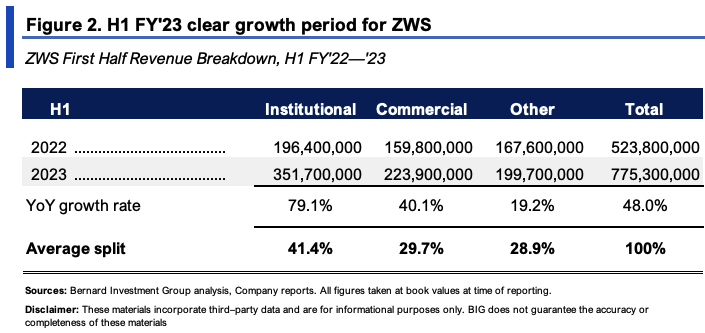

Figure 2 shows the company's YoY growth numbers to its core customers from H1 FY'22-'23, along with the average revenue split. Total sales were up 48% YoY. Critically, institutional customers still make up the bulk of turnover, and sales to these customers grew 79% on last year.

Of the top-line growth in Q2, organic sales were down 500bps YoY, balanced by the 47% growth contribution from its Elkay acquisition. As a reminder, ZWS merged with Elkay in July 2022 (ZWS was known as Zurn Water Solutions at the time) after buying the company for $1.45Bn. Operating income was ~$55mm for the quarter, down 520bps YoY. Despite c.$6mm in cost synergies from the acquisition, higher inventory purchases made last year were realized at the cost level in H1 FY'23, crimping operating profit.

{kind=link}

Economic performance and value drivers

- Economic performance

For all the top line growth exhibited in H1, this hasn't transposed to shareholder value in my opinion.

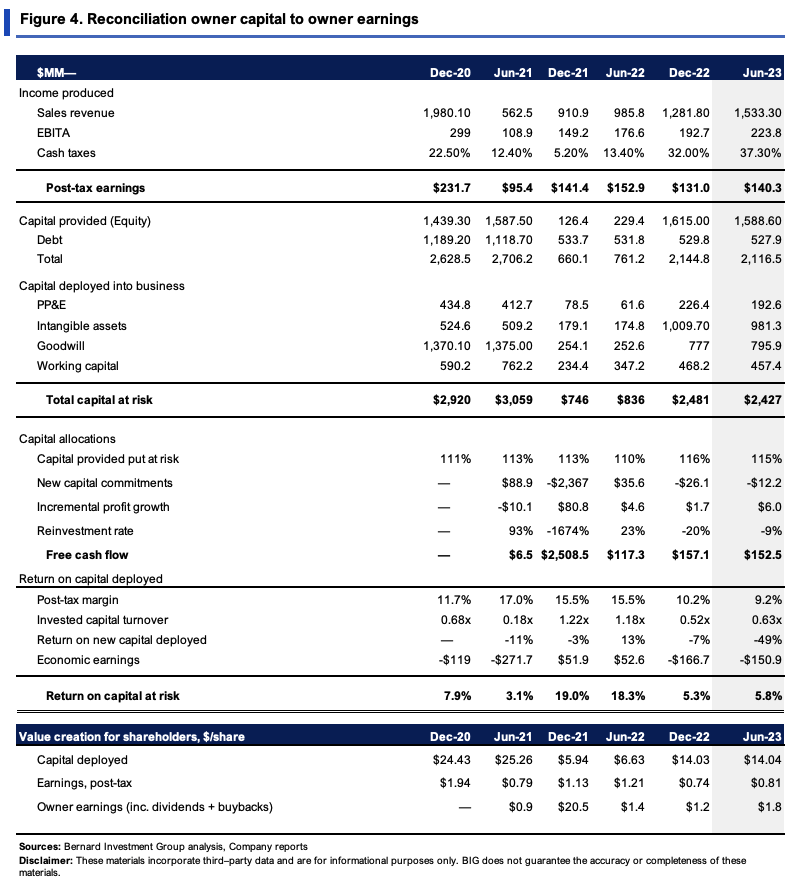

Figure 4 reconciles the capital provided by ZWS' owners to the capital put at risk, and the cash flows + earnings attributable to its owners. The company has put 115% of the capital provided by investors to work in the business, around $2.4Bn as of Q2, or $14.04/share.

The $2.4Bn/$14.04 per share produced $140mm in post-tax earnings, otherwise just $0.81/share, equating to a paltry 5.8% return on investment. As a reminder, a corporation creates value for its shareholders by producing an earnings rate on its investments above the opportunity cost of capital. Here, I define this as the market return on capital (12% based on long-term averages). For our equity holdings, 12% is the required rate of return we look for.

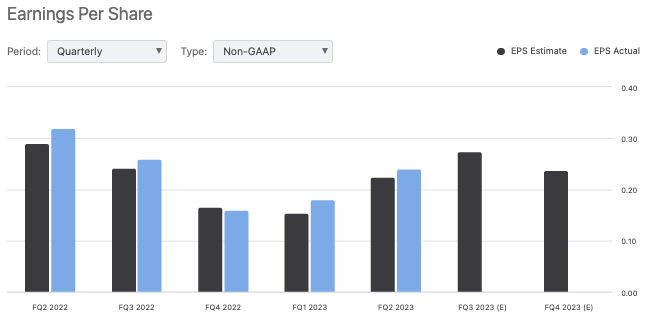

Figure 2. ZWS earnings, actuals and consensus (per share)

{kind=link}

The 6.8% negative spread (5.8%-12% = -6.8%) translates to an economic loss. Growth was therefore destructive to ZWS' value in Q2. The reason? Because the company is investing at subpar rates of return. If you can expect to get 12% by riding the benchmark over the long term, that's the opportunity cost. So you'd want any company to be doing at least 12% on capital to create any value. In that vein, I'd need ZWS to produce at least $291mm in NOPAT off the $2.4Bn of capital to fire up the investment cortex. The fact ZWS grew top-line sales 48% this YTD means nothing if the growth was built on investments that produce less than the hurdle rate. Mathematically, you see this by capitalizing the $140mm in NOPAT at the hurdle rate (12%), and observing it less than the investments made of $2.4Bn (140/0.12 = $1,233 vs. $2,427).

So, despite the fact it spun off $152mm in TTM FCF last period-ahead of $117mm in Q2 FY'22-the earnings rate of return produced on the capital at risk doesn't stack up.

This is because both post-tax margins and capital turnover are painfully low, 9.2% and 0.63x, respectively. Said another way, each $1 in capital brings in just $0.09 in NOPAT and $0.63 in sales-not attractive numbers in my eyes.

{kind=link}

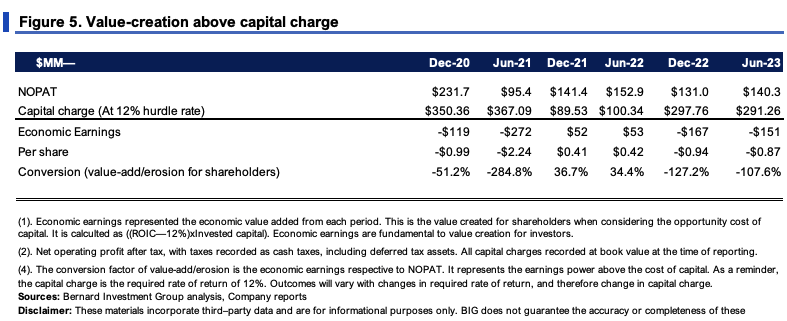

These economics are quantified in Figure 5, which shows the economic earnings ZWS produced from 2020-date. By creating a capital charge at 12% times the invested capital, we can compare what NOPAT was produced above or below this threshold. Note from Q4'22-Q2'23: It's been a series of economic losses, amounting to $1.20/share over these two periods alone. For reference, here, you want 1) economic earnings to be positive, and 2) the conversion factor to be positive and high.

{kind=link}

- Value drivers

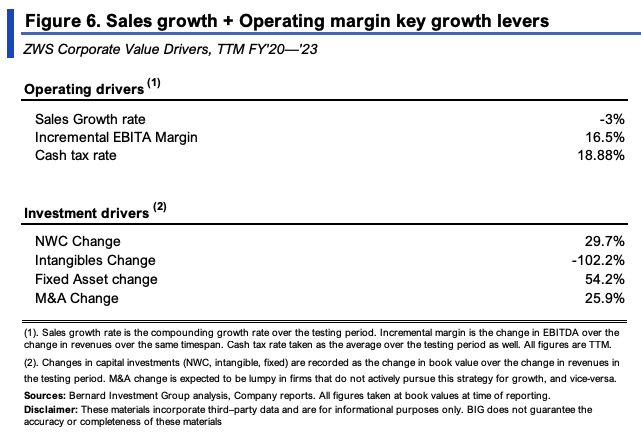

The drivers of ZWS' business returns from the last 3 years are seen in Figure 6. Critically, sales growth has exhibited a geometric loss of 3%, but capital intensity is up 83% on aggregate, measured at the rate of sales change. Further, for each $1 in sales produced, ZWS has put up $1.02 in intangible investment.

{kind=link}

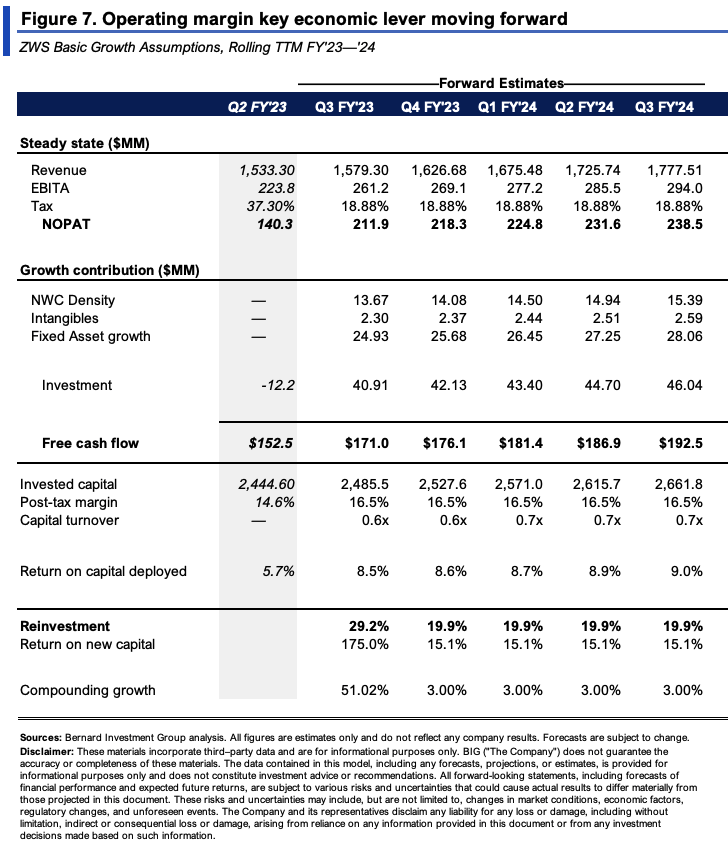

Carrying these basic assumptions forward reveals interesting results. I've changed the sales growth rate to positive ~3%, slightly above global GDP. Should the company continue at this steady state, it could spin off $192mm in FCF by FY'24, but this would only land it an 8-9% rate of return on capital invested. This could see it compound intrinsic value at a cumulative 12% over the coming 12 months, provided all stays the same.

{kind=link}

Valuation and conclusion

The stock is richly priced at 30x forward earnings and 21x forward EBIT, with a PEG ratio of 42x. It has only created $3 in market value for each $1 in net asset value. These figures are right about on point in my opinion, and here's why.

One, the market has priced ZWS at a 2.2x premium to the capital it has put at risk. This says it doesn't expect a high rate of return going forward. This is supported by the fact the 5.8% ROIC isn't conducive to value. Hence, investors have well and truly priced the company's growth in at 2.2x EV/IC.

BIG Insights

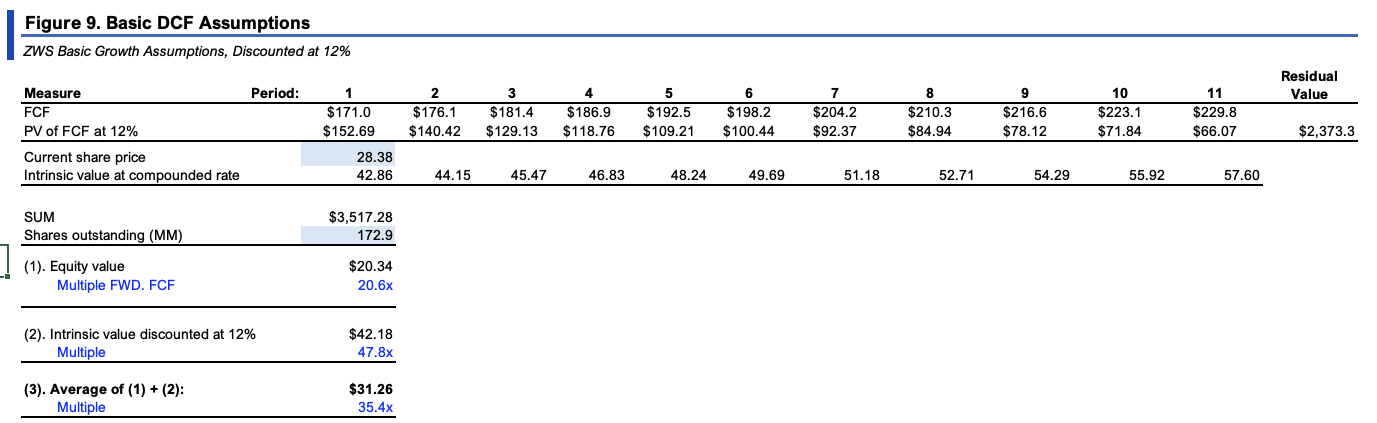

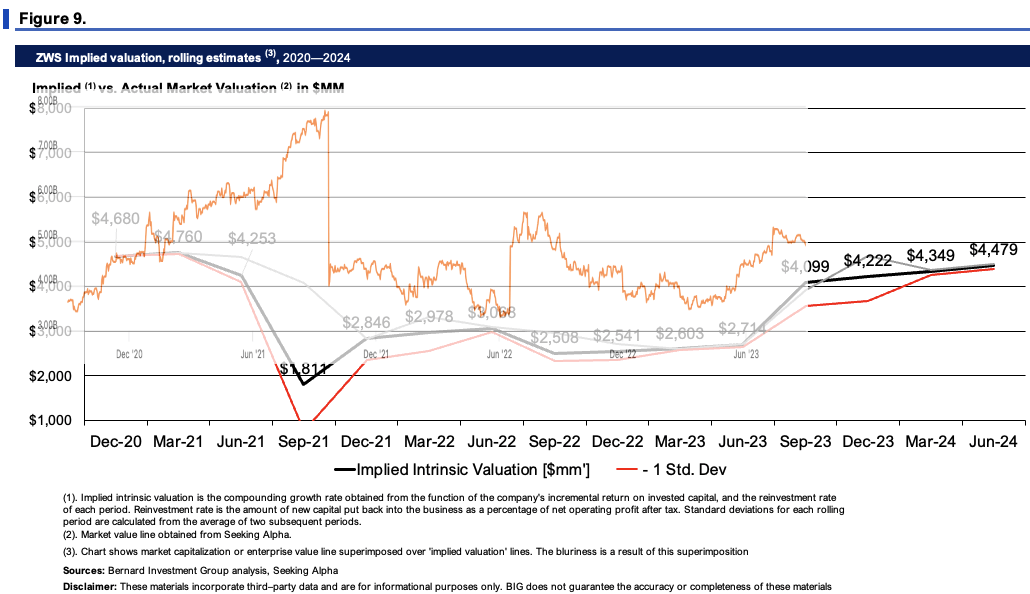

Two, Figure 9, spread across the two charts below, suggests ZWS is about fairly valued where it sells today. The first table projects the FCFs out to 2028 at the steady state seen in Figure 7, discounting back at 12%, arriving at $31/share in implied value. The second chart compounds ZWS' market value at the function of its ROIC and reinvestment rate, getting to ~$4.5Bn in implied market value. Both measures show the company is likely fairly priced at its current marks in my view.

{kind=link}

{kind=link}

In short, there were plenty of growth numbers to talk about in ZWS' first half of '23. Top-line sales up 48%, double-digit upsides in all segments. But the growth wasn't accretive to shareholder value, evidenced by the weak economic performance. Around $2.45Bn of capital produces just $0.81/share in NOPAT, 5.8% return on investment. We are looking for 12% compounders (or more) to fill out equity bucket. It would also appear the market has accurately priced the company at its current values. Net-net, rate hold.

For further details see:

Zurn Elkay Water Solutions: Growth Not Accretive To Shareholder Value, Hold