ZYXI - Zynex Is A Quality Company But You Must Pay For Quality

Summary

- Products sold in the past by Zynex for pain management have failed to penetrate the market.

- Zynex's new products are radically different from their predecessors: more specific and innovative.

- The new products the company will market could grow sales far beyond analysts' expectations.

- Zynex is a company with a rich valuation but with great room for growth.

The investment thesis

Despite the recent increase in its share price, Zynex ( ZYXI ) remains attractive to investors due to the innovative new products the company is about to launch on the market, which could significantly grow its revenues.

The core business of this company is the sale of Nexwave, a dual-channel, multimodality IFC, TENS, and NMES device, which through electrical stimulation, can reduce pain in patients suffering from arthritis or localized pain, and the supplies, such as electrodes or batteries, that are used to make it work.

This type of business has been growing linearly and steadily over time, with growth rates declining year by year following the normal cycle of market penetration.

The actual game changer for the company, and the topic of this investment thesis, are the three new products (CM-1600, NiCO CO-Oximeter and HemeOx) that the company wants to market in the next few years through its Zynex monitoring solutions division. These products could radically change the nature of the company, from the current company specializing in the production of a single device to a diversified one that can attack different markets.

Which is the market of new products

The body fluid management market is an ample opportunity for Zynex, as its value is estimated to be around 3.6 billion in the U.S. states alone, while globally, the value will be about 11 billion in 2022. Furthermore, analysts expect this market to reach $18 billion in 2026.

The company does not yet sell the products of the Zynex Monitoring Solutions division in this market. Still, it will start in the next few years, and its products (CM-1600, NiCO CO-Oximeter and HemeOx) have a competitive advantage over competitors.

Why have Zynex's other products failed?

Zynex sells several other products, such as Comfortrac/Saunders (Cervical traction), JetStream (Hot/cold therapy), LSO Back Braces (Lumbar support), and Knee Braces (Knee Support). These products make up about 20% of the company's revenues, and in the past year alone, they are increasing sales, driven by Knee Braces in particular.

Despite visible improvement over the past year, it is safe to say that the company has failed to introduce these products to the market.

The first significant problem is the lack of differentiation from competitors in the market. A quick search on the Internet makes it possible to find dozens of different versions of Knee Braces or Back Braces, the difference being that Zynex's products cost significantly more and have additional features (such as unique safety locks ).

However, most individuals affected by localized pain do not require high-performance products, such as those from Zynex, which are ideal for patients with more persistent chronic pain.

Moreover, when it launched most of its devices, the company did not have a sufficiently trained sales department, and internal resources were limited. As a result, Zynex in 2021 spent 42% of its total revenue on marketing and sales (only $54 million). It is, therefore, no coincidence that the newest product, the Knee Braces , is also the one that is driving sales right now.

Why should new products be more successful?

Indeed having already built up a sales and marketing force, with the knowledge the company has gained over the past few years and the efficiency of sales reps (the company fired all the low-performance reps in the last year), gives these products a significant advantage over others. As announced in the previous conference call by Anna Lucsok:

Sales rep productivity is at all-time high with revenue per sales rep at $430,000 per year [...] we are committed to maintaining a best-in-class workforce and retaining the talent needed to stay competitive

But the crucial aspect is the differentiation these products have from possible substitutes in the market.

NiCO CO-Oximeter is the first laser-based photoplethysmographic patient monitoring technology and allows four species of haemoglobin to be monitored. This technology has proven to be unreliable at times, but as the company's CEO detailed in the latest quarterly report:

It has been noted that the technology in LED systems has an inherent pigmentation bias. But we believe our laser-based solution inherently solves current market problems.

CM-1600 is a device that allows innovative monitoring of fluid changes in patients undergoing surgery, for example. It is 100% noninvasive, and the patient's fluid status is determined using an algorithm. Several physiological parameters are combined to generate a single Relative IndexTM (R.I.) value. Using a proprietary algorithm shields the company from competitors who want to make a similar product.

In addition, these devices are indicated for use within hospitals and operating rooms. Still, they are very specialized (unlike Zynex's other products aimed at a more general audience).

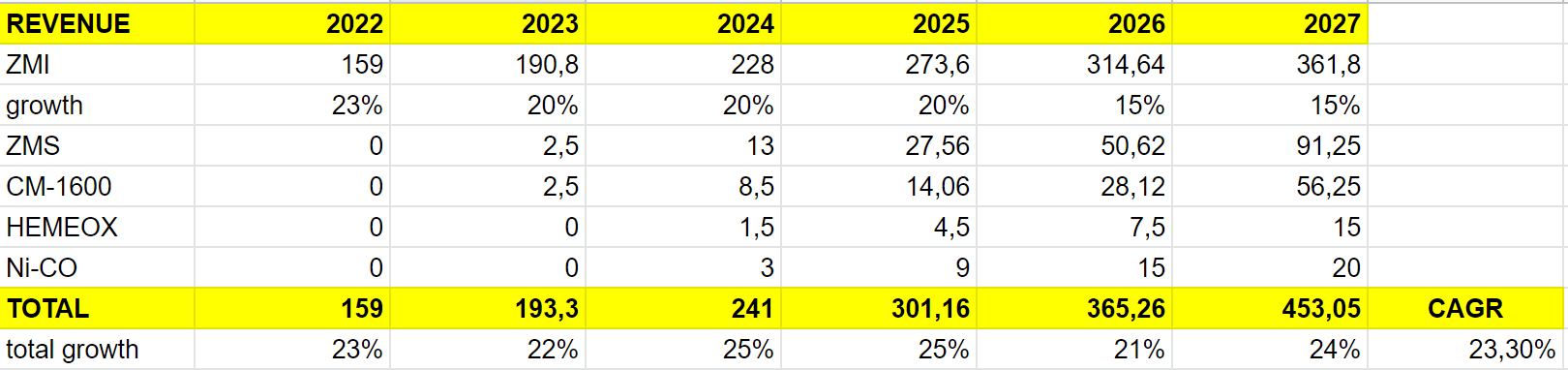

Revenue estimates

Estimating the possible future revenues of a company like Zynex is a rather complex task because of the significant growth the company has experienced in the past few years. This growth in the coming years will slow down, and the estimates I have made take into account the estimates of analysts, who expect a revenue cagr to 2025 of 25%.

{kind=link}

I adopted some assumptions for these estimates: CM-1600 will be commercialized in 2023, while HemeOx and Ni-CO CO-Oximeter in 2024. In addition, the adoption of the products will have to be quite broad. For CM-1600, I estimated that in 2027 it would be used in 1% of U.S. operating rooms (about 225K ). As stated in the previous conference call:

Last week, our team attended the American Society of Anesthesiologists Conference in New Orleans to showcase the product (CM-1600) where we received exceptional feedback

CM-1600 will be priced (conservatively) at $25000 (In this interview with the CEO Thomas Sandgaard, a price of $30,000 had been defined), while for HemeOx, I estimated a price of $750 and for NiCO $1500.

{kind=link}

revenue estimate (own chart)

The resulting cagr is 23.3% for five years, with a final revenue to 2027 of $453 million. Suppose we combine this value with a P.S. of 3.5 (the average value from 2017 to 2022 of Zynex, i.e., the time frame in which the company began to expand significantly). In that case, we get a market cap of $1.5 billion, compared to the current market cap of $600 million. Considering that the company is unlikely to strongly dilute its shares, as it is self-financing through positive cash flow and may continue to make buybacks in the coming years, this valuation implies a significant upside for estimates that are not particularly aggressive.

Main Risks for Zynex

One of the main risks is FDA approval of the company's products. On CM-1600, the risks of rejection are very low, as the device deviates very little from the previous CM-1500 version already approved (a few more features, such as wireless connection). In contrast, approval is more difficult for HemeOx and Ni-CO CO-Oximeter as these are highly innovative products. Therefore, a delay in the approval time would impact the company's revenues and its ability to introduce the products to the market.

Another risk is how the products are sold, which differs from Nexwave and other products for pain management. For example, Zynex will have to contract directly with hospitals and specialty clinics instead of working with insurance companies for reimbursement and physicians for prescriptions.

Finally, the last risk is product pricing, particularly for the CM-1600. A recession could push many buyers to delay or not make a purchase.

Valuation

The valuation is quite rich, with a PE of about 30 and a PB of 8. These multiples are currently justified by the consistent results the company has brought in over the year and the low-inflation nature of its business, which have made this stock very attractive to investors. Analysts expect revenue growth to 2025 of 25% annually and EPS to 2025 of 1.19. However, the company's multiples will likely fall in the coming years as the macroeconomic situation improves simultaneously as the business matures. Still, at the same time, the company could continue to make buybacks, as it has already done three times during 2022, thus raising EPS even higher.

Conclusions

Zynex is a company with a relatively rich valuation, but that is justifiable because of the high growth that analysts expect and the stability of its business. The success of the Zynex Monitoring Solutions division is the key determinant that could provide investors with extraordinarily high returns over the next five years. Determining what share of the market Zynex could occupy is quite tricky at this stage of product development. Even without this part of the business, the company remains very attractive, although the valuation would have to come down to provide an adequate margin of safety. The company is financially solid, and founder Thomas Sandgaard holds 40% of the shares, ensuring a strong alignment between management and shareholder interests.

For further details see:

Zynex Is A Quality Company, But You Must Pay For Quality