LHX - 14% Annual Return Potential: L3Harris Is My Favorite Dividend Stock Going Into 2024

2023-12-20 15:35:31 ET

Summary

- L3Harris Technologies has tremendous growth potential and meets the criteria for a long-term investment, including a strong balance sheet and attractive valuation.

- The company's recent Investor Day highlighted its involvement in various domains, such as space and airborne systems, integrated mission systems, and communication systems.

- L3Harris has outlined a compelling longer-term outlook, aiming for $23 billion in revenue and at least 16% margins by 2026, which could result in significant shareholder value.

Introduction

I have to admit that I wasn't planning on writing this article. Not only have we talked a lot about defense companies in 2023, but my most recent article wasn't that long ago.

On November 19, I wrote an article titled With Significant Potential, L3Harris Remains My Favorite Deep Value Dividend Stock .

Since then, L3Harris Technologies, Inc. ( LHX ) shares are up 13%, beating the S&P 500 by roughly 800 basis points. Shares are up almost 25% since my summer article when I wrote that LHX has more than 50% room to run.

Having said that, I'm not writing this article to celebrate the recent surge. After all, some of my prior calls are now breakeven. It's still not a performance to write home about.

The reason I'm writing this article is because we have a lot to discuss.

Since my most recent article, L3Harris Technologies has held its 2023 Investor Day, it has received upgrades and provided us with a longer-term outlook.

On top of that, the company checks all marks when it comes to the criteria I use when picking stocks for 2024 and beyond.

In the 2024 outlook I wrote with Seeking Alpha, I said I'm looking for three key points:

- Safety- I want companies with strong balance sheets to withstand periods of prolonged elevated rates and inflation.

- Quality- I want companies with the ability to grow over time, preferably with secular growth tailwinds.

- Deep value- In light of elevated stock market valuations, odds are we could encounter overall subdued returns in the years ahead (see the chart below). Hence, I want companies that are very attractively valued to provide me with a shot at outperforming the market.

With all of this said, let's dive into the details, as we have so much to discuss!

L3Harris Has Tremendous Growth Potential

Despite the returns I just listed, LHX shares are up just 3% year-to-date, including dividends, underperforming the S&P 500 by more than 20 points.

This year, LHX suffered from investor distrust. In light of elevated rates and budget uncertainties, investors didn't care for this defense contractor, which closed the massive acquisition of Aerojet Rocketdyne.

While LHX is one of the reasons why my portfolio has failed to outperform the market this year, I could not be happier with the buying opportunities this stock provided for us (it's still attractive).

I have been aggressively buying L3Harris for my portfolio and the portfolios of my family, making it one of our biggest long-term investments.

The reason is quite simple: L3Harris has everything we are looking for in a long-term investment.

- It has an anti-cyclical business model , mainly relying on domestic and international government contracts.

- It is a major supplier of all major defense contractors, which lowers competition risks.

- It is a dividend growth stock with a great track record.

- It is at the forefront of defense innovation .

- It has a healthy balance sheet .

- It uses excess free cash flow to buy back stock, enhancing shareholder value.

- It is attractively valued .

With all of this in mind, the company's recent Investor Day was very interesting, as it was the first Investor Day that included the "modern" L3Harris after the Aerojet deal.

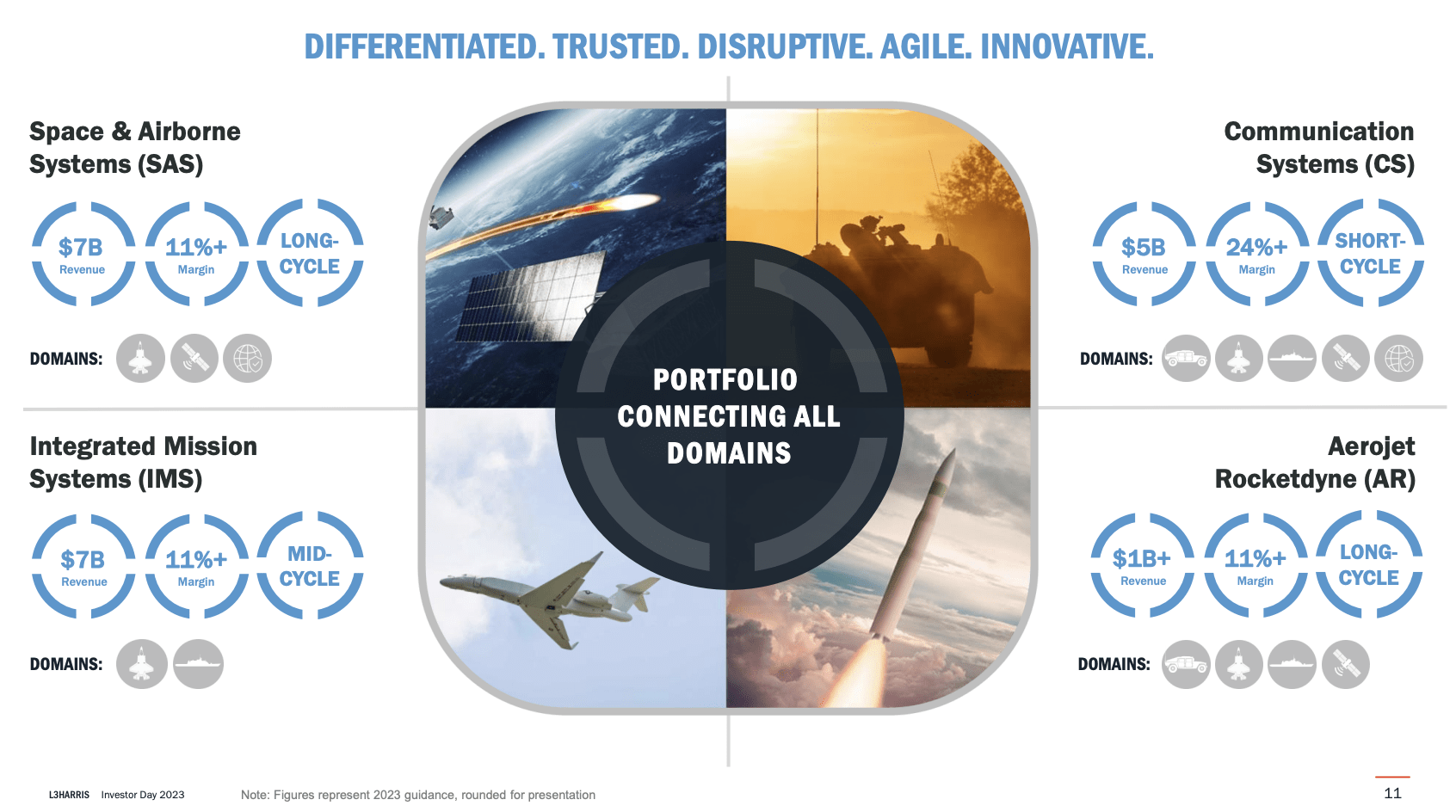

As we can see below, L3Harris currently operates in all five domains, emphasizing a commercial business model that yields higher margins in four key areas:

- Space & Airborne Systems ("SAS").

- Integrated Mission Systems ("IMS").

- Communication Systems ("CS").

- Aerojet Rocketdyne ("AR").

Each of these businesses generates more than $1 billion in revenue. Just one of these businesses is a short-cycle business.

{kind=link}

Unsurprisingly, L3Harris is all about innovation. That's the main reason why I love defense companies. I am not rooting for war, but I'm betting on the need for advanced technologies to keep us safe.

In general, I would make the case that peace is more bullish for LHX than war.

During peace, defense companies aren't rushed to produce, government involvement is less likely, and potential weaknesses in supply chains remain hidden.

Essentially, *if* defense companies wanted to "rip off" the government, doing it during peacetime would be much easier.

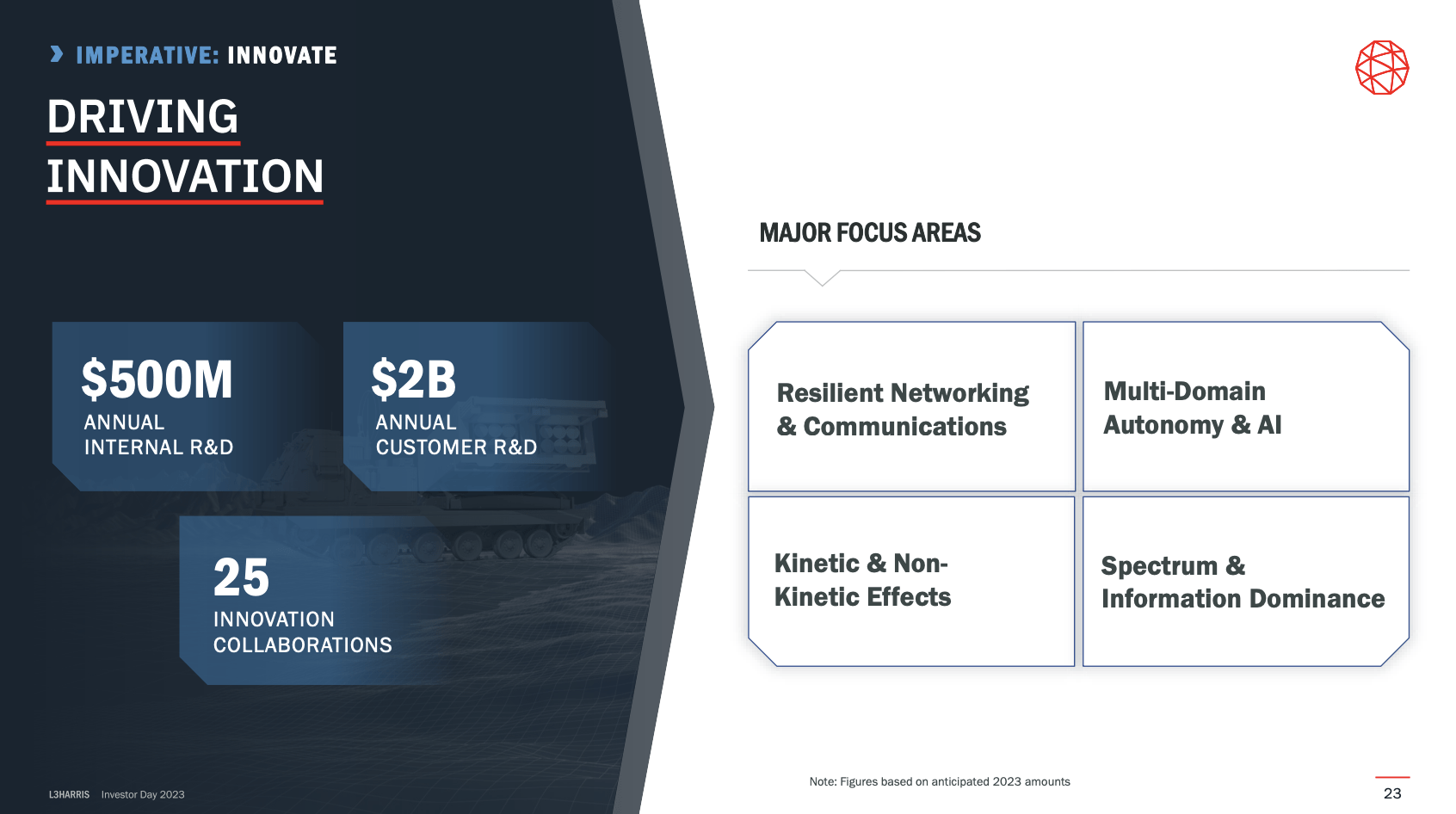

With that said, L3Harris has been actively pursuing research and development ("R&D"), with a notable increase in customer-funded R&D contracts.

While this may impact short-term margins, the emphasis is on positioning the company for long-term strength and innovation. The goal is to bridge the $2.5 billion R&D gap and develop capabilities for future challenges.

{kind=link}

The company is also changing its Board of Directors to reflect diverse experiences from commercial entities, government, mid-tier companies, and primes, with industry veterans like Bill Swanson and Kirk Hachigian joining.

Bill Swanson, for example, is the former CEO of the Raytheon Company, now part of the RTX Corporation ( RTX ).

This is also part of a business review with hedge fund D.E. Shaw, as reported by Seeking Alpha .

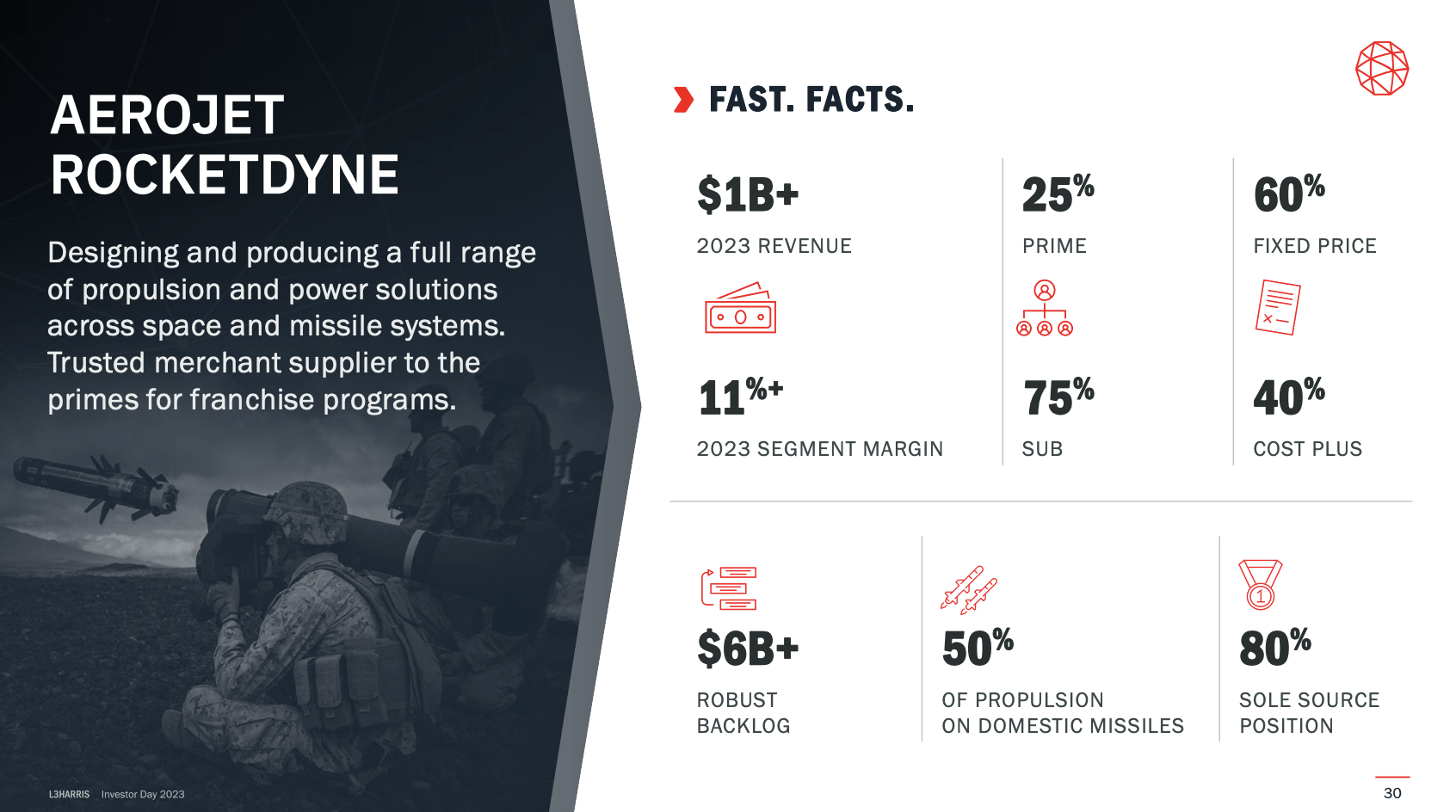

As I already mentioned, the acquisition of Aerojet Rocketdyne was (and still is) a major deal, as it adds a whole new layer of capabilities to L3Harris.

During its Investor Day, the company made clear that Aerojet's involvement in space propulsion and missile technologies is pivotal for L3Harris' strategy.

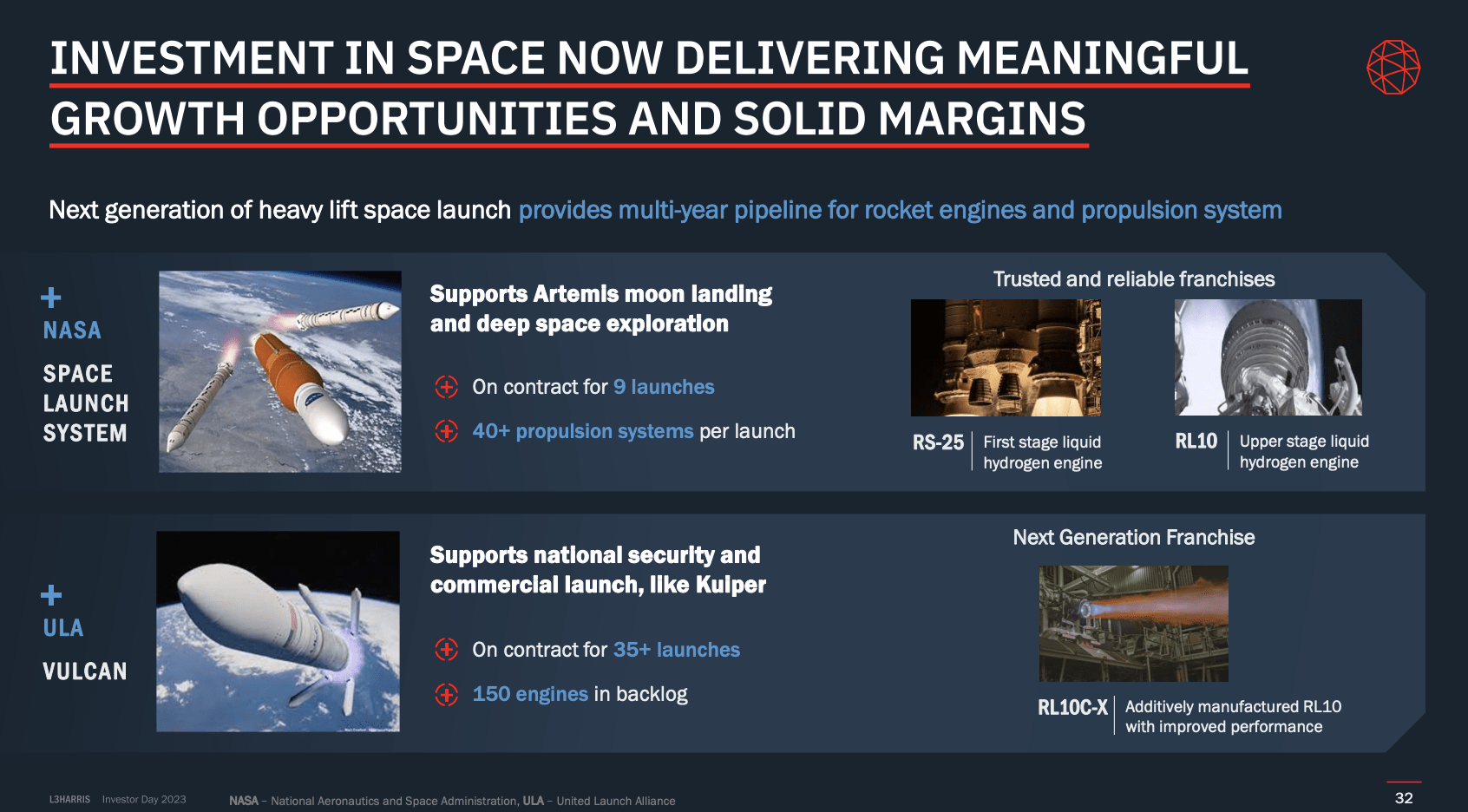

The space business, constituting about one-third of Aerojet Rocketdyne's revenue, is marked by stability, solid backlog, and elevated margins.

{kind=link}

Significant franchises, such as NASA's space launch system and United Launch Alliance's Vulcan Rocket, contribute to this stability.

Moreover, the company's forward-thinking approach is evident in the modernization efforts, such as upgrading the RL10 engine using additive manufacturing to enhance efficiency and reduce costs.

{kind=link}

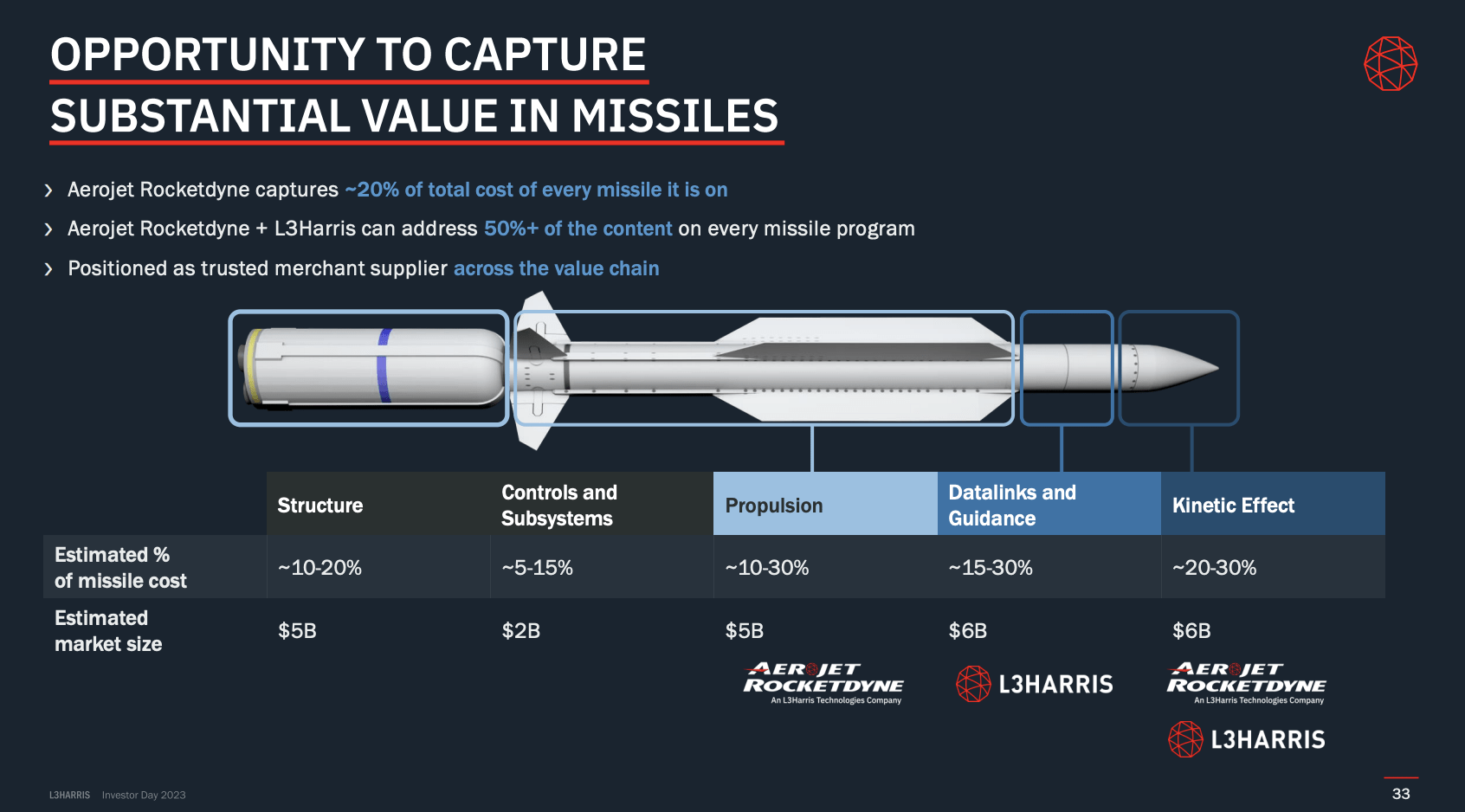

In the missile business, Aerojet Rocketdyne's role in providing propulsion and kinetic effects (warheads) positions it uniquely in the market.

The company highlighted that Aerojet Rocketdyne's components account for about 20% of the cost of any given missile, and, when combined with L3Harris' capabilities, the companies have access to over 50% of the total missile cost.

Think about that for a second.

Essentially, this integrated approach supports L3Harris' vision to be a one-stop shop for all aspects of missile development.

{kind=link}

Moreover:

- The company has products in more than 75% of all domestic missiles currently fielded!

- It has supplied every single surface-to-surface and air-to-air missile.

- Half of all air-to-surface and strategic deterrence missiles have LHX parts.

- 80% of all surface-to-air rockets have components from LHX.

Unfortunately, Aerojet has struggled with some supply issues itself.

L3Harris has addressed this by spending more money.

Since the acquisition, R&D spending has increased fourfold, and capital investment has doubled, showing a commitment to supporting innovation and manufacturing efficiencies, which are key to growing margins on a long-term basis.

The same applies to its space business, which the company is looking to expand.

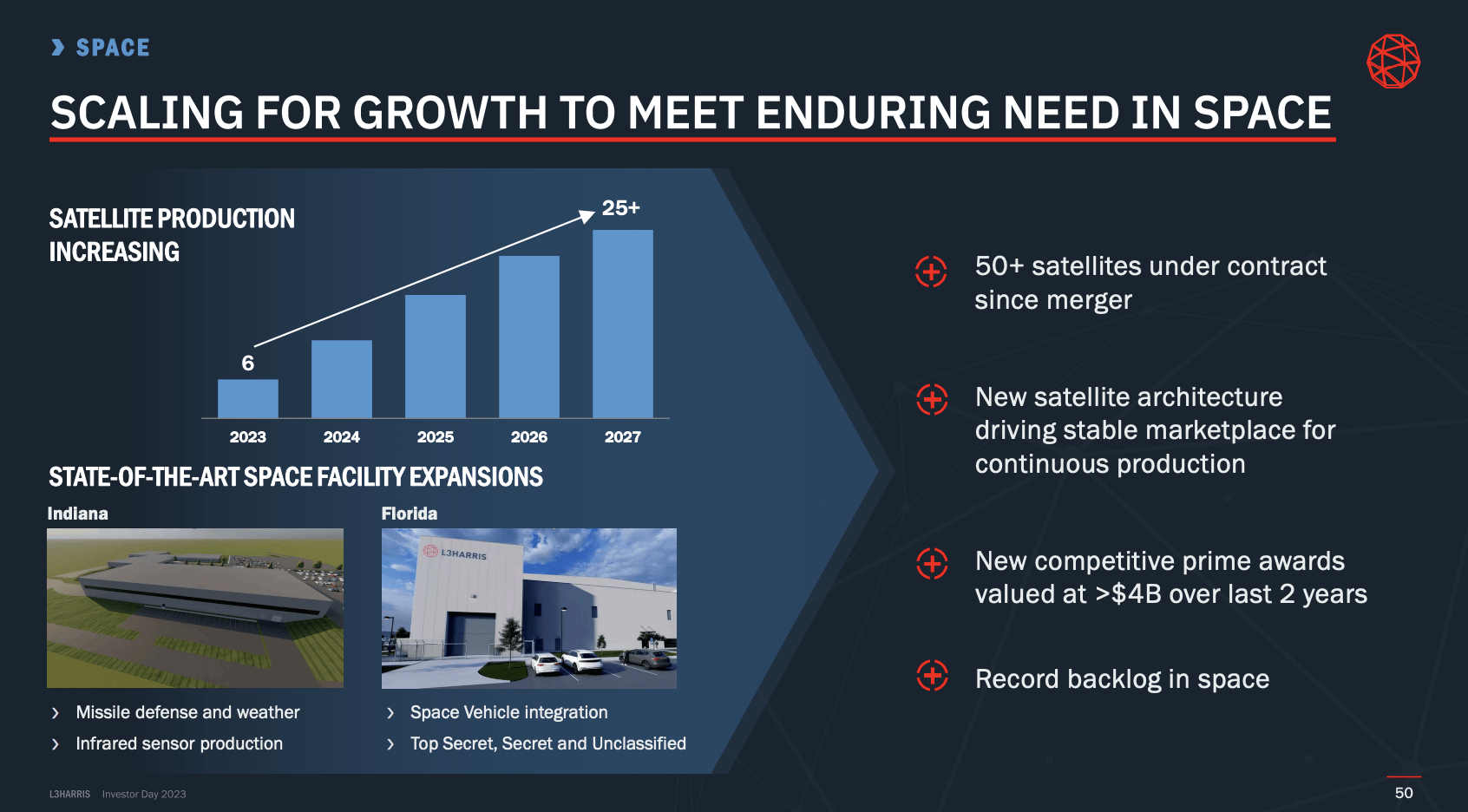

With that said, If there's one thing I cannot stop talking about, it's the opportunities that come with the fast-growing space industry.

To benefit from this, L3Harris is actively scaling its space business to build a reliable marketplace for continuous satellite and sensor production.

The transition from a bespoke model to a continuous flow model reflects an adaptive approach to industry trends, while investments in facilities in Fort Wayne, Indiana, and Palm Bay, Florida, underscore the commitment to expanding production capabilities.

With a new building in Fort Wayne, L3Harris is gearing up to produce one infrared sensor per week, marking a substantial increase in efficiency and output.

{kind=link}

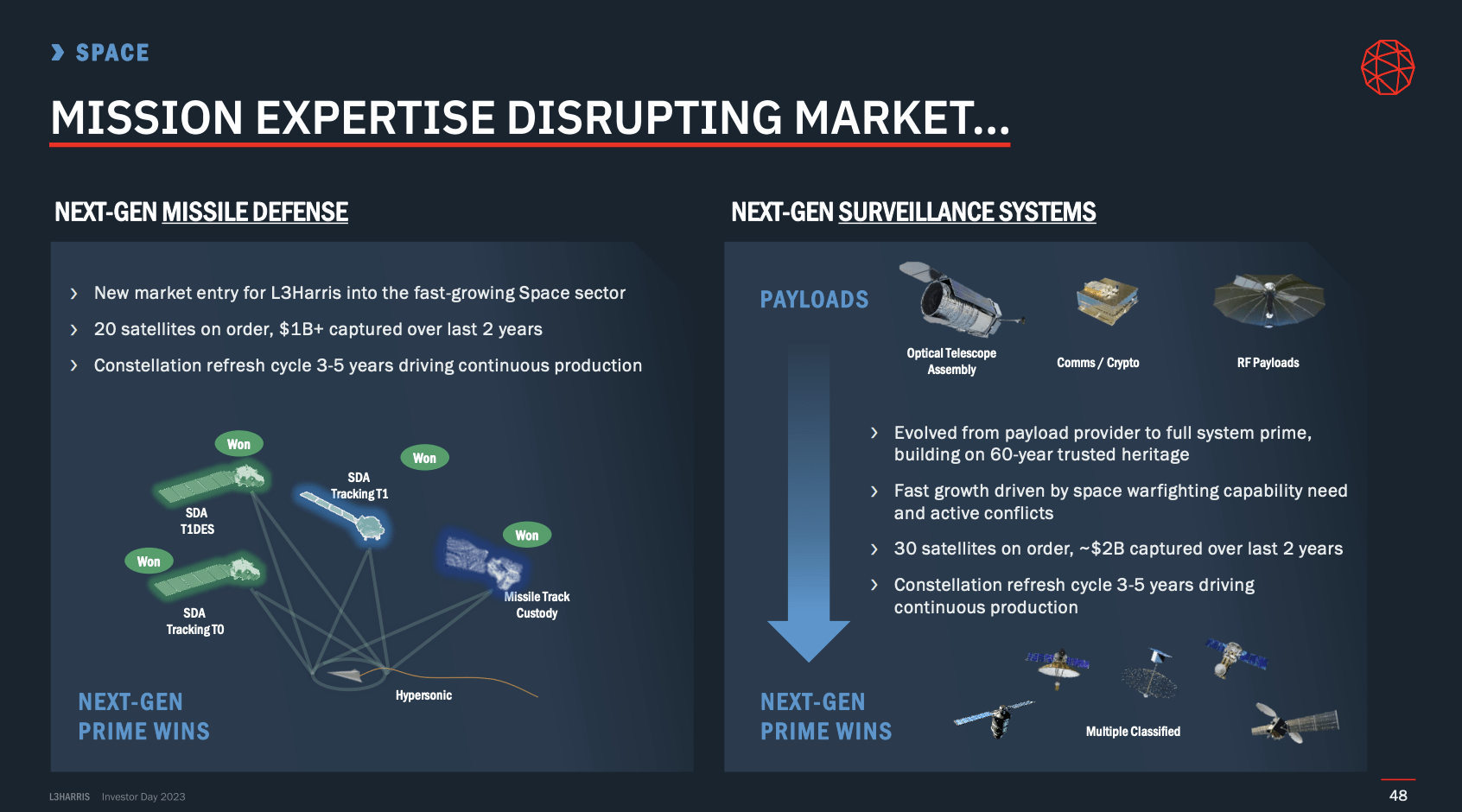

Meanwhile, the company's involvement in next-generation architectures, specifically in missile warning, missile defense, and classified surveillance, aligns with the evolving needs of the defense and intelligence communities.

By winning prime contracts and securing a record backlog, L3Harris is establishing itself as a key player in shaping the future of space-based solutions.

{kind=link}

But wait, there's more!

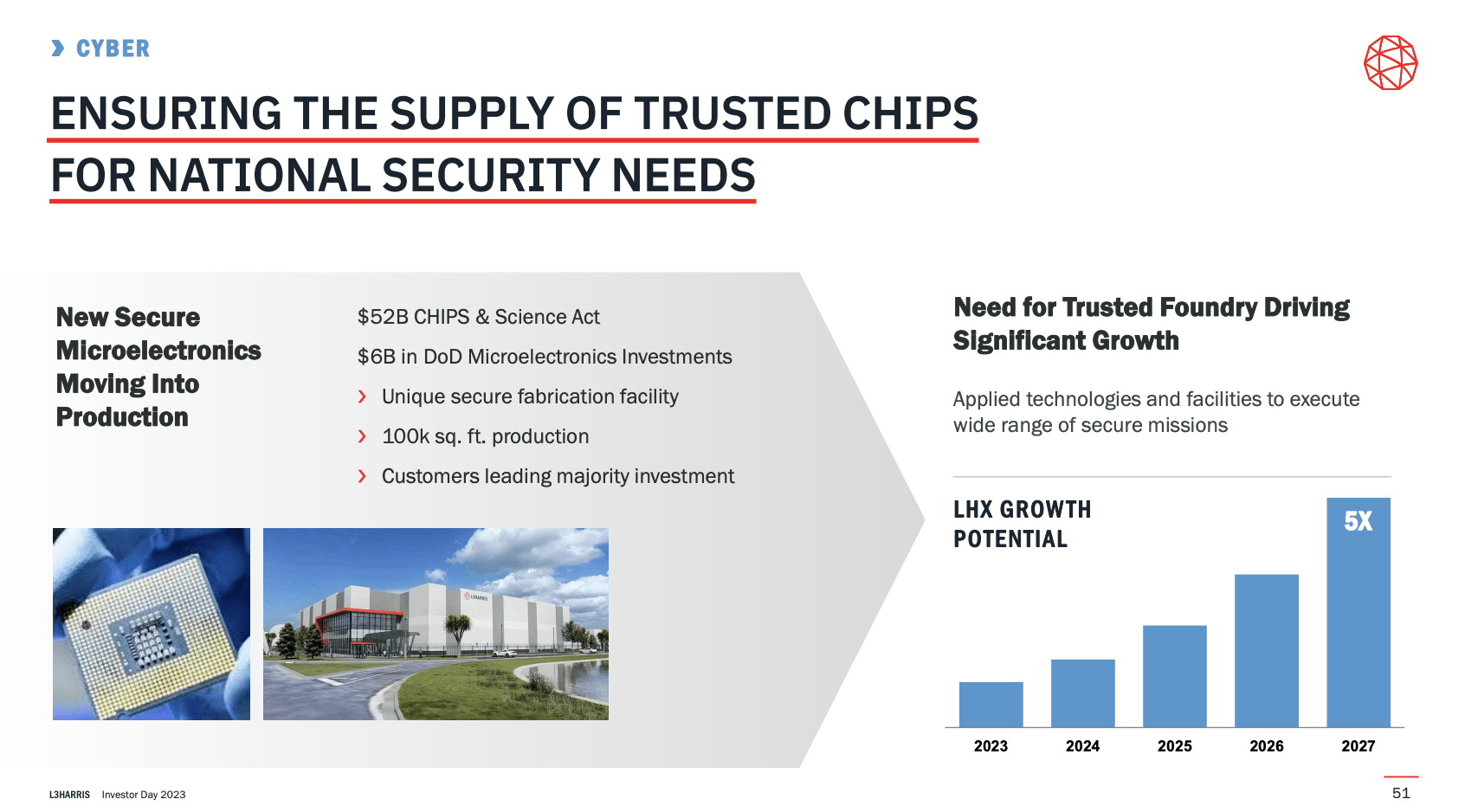

I believe the move into trusted microelectronics is interesting.

The company is recognizing the critical importance of a secure and reliable source of high-performance electronics, especially in times of potential supply chain disruptions.

With over $600 million in backlog and plans for a state-of-the-art semiconductor manufacturing facility in Palm Bay, L3Harris is at the forefront of providing solutions for the defense sector's electronic needs.

{kind=link}

Meanwhile, in the cyber domain, the focus on entering the trusted microelectronics market adds a layer of resilience and adaptability to emerging cyber threats.

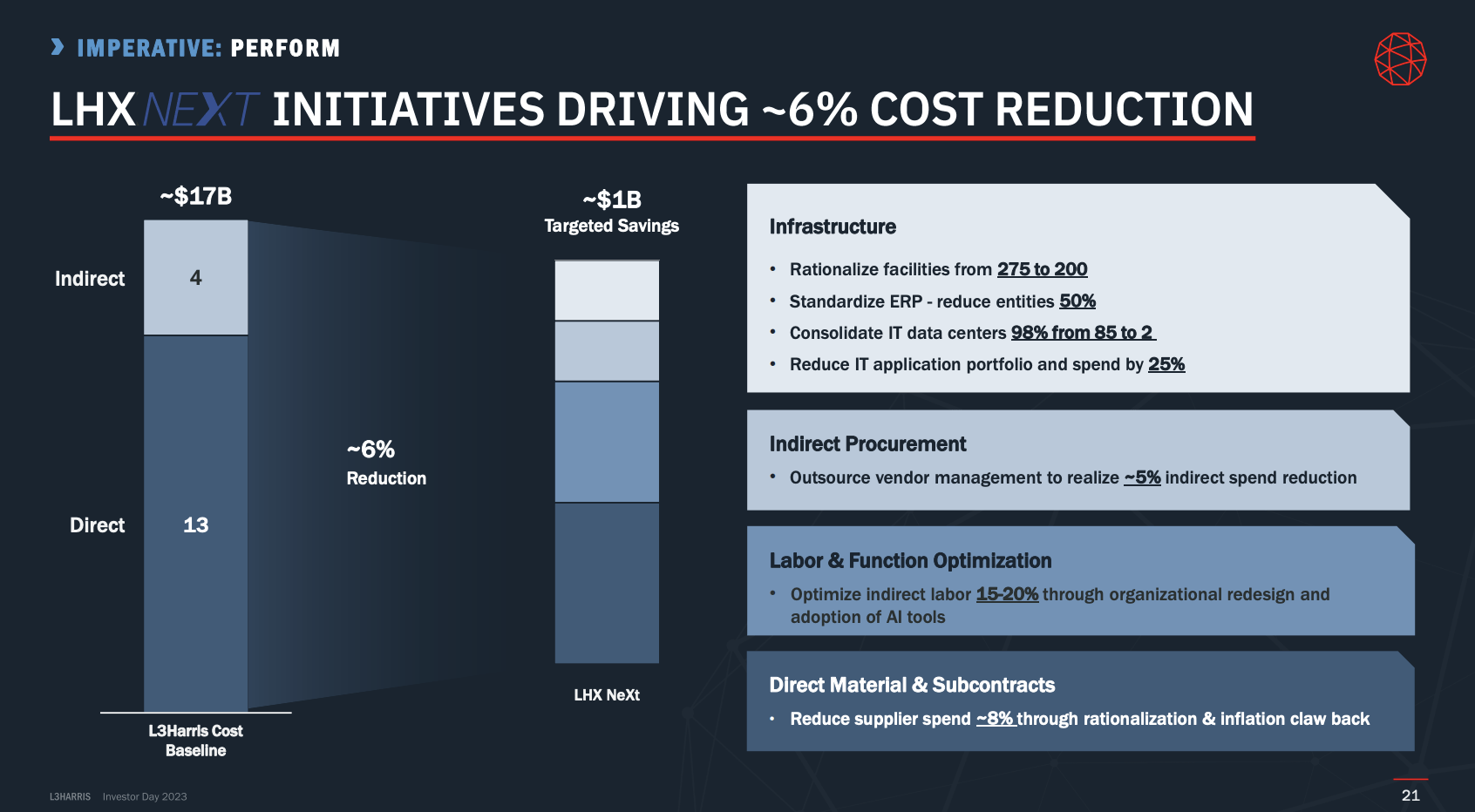

On top of that, the company is cutting costs, as it has presented the E3 initiative, targeting $500 million annually for cost takeout to offset headwinds. The new LHX NeXt initiative, an enterprise-wide effort, aims for a $1 billion run rate in three years, contributing to margin improvement.

{kind=link}

Key areas include direct and indirect spend optimization, workforce and labor restructuring, and leveraging AI and automation for operational efficiency.

The Long-Term Outlook

A very important part of its 2023 Investor Day was its longer-term outlook.

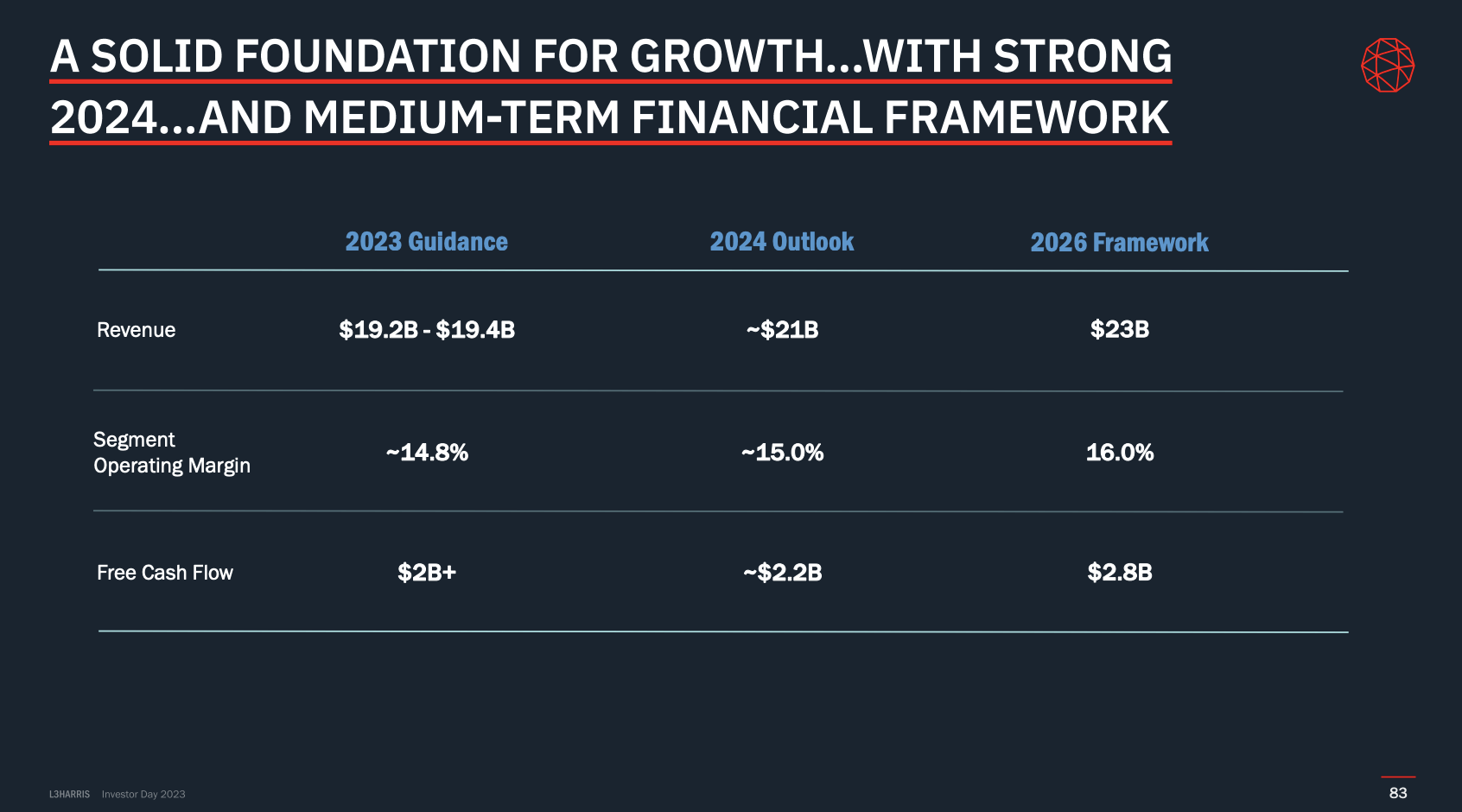

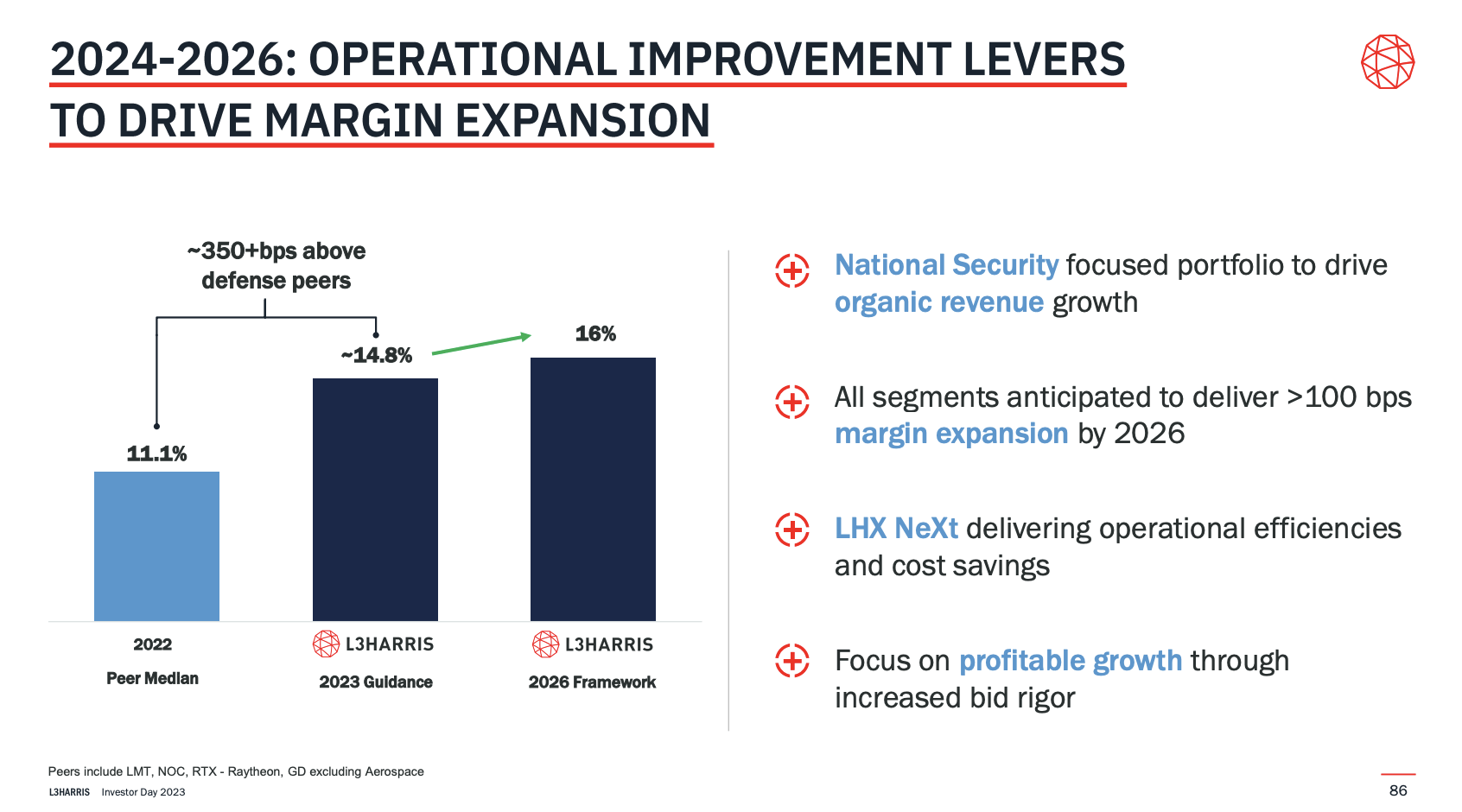

L3Harris outlined a compelling longer-term outlook, focusing on key financial metrics and strategic initiatives through 2026.

The company's vision includes reaching $23 billion in top-line revenue, a significant portion of which is expected to be driven by organic growth, as the company made the case that it is likely done with M&A for the time being.

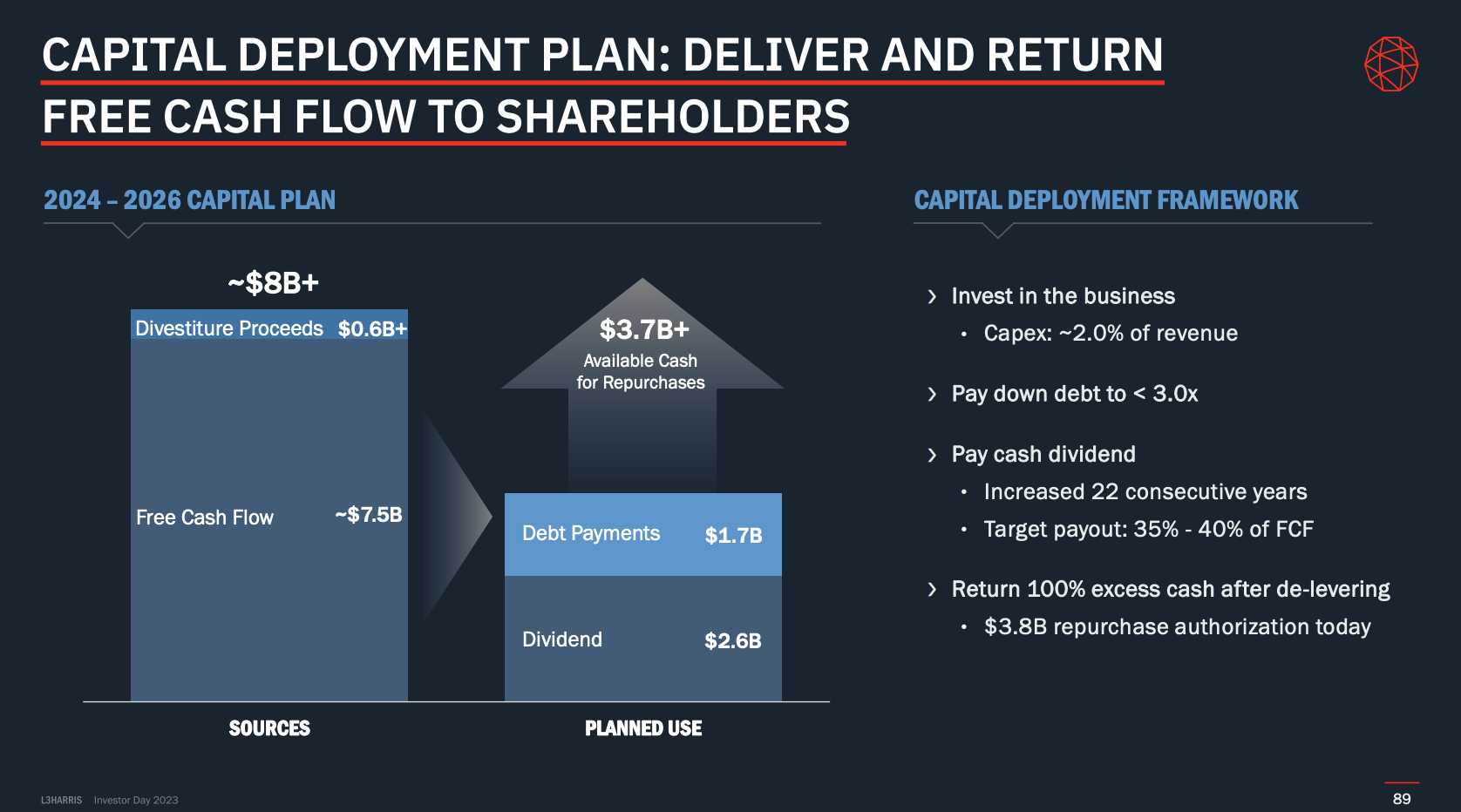

Furthermore, the commitment to achieving at least 16% margins by 2026 demonstrates a strong emphasis on operational efficiency and profitability, which could boost free cash flow to almost $3 billion in 2026.

It would be an increase of roughly 40% to 50% compared to 2023 expectations and imply a free cash flow yield of 7-8%, which is a fantastic number, as it opens up so much room for shareholder distributions.

{kind=link}

The roadmap for achieving these financial milestones includes the execution of the aforementioned LHX NeXt program, targeting $3 billion in gross savings by the end of 2026.

This program is positioned as a key driver for margin expansion and operational excellence, while the emphasis on program execution, better contract negotiations, and risk mitigation showcases the company's commitment to improving overall efficiency and profitability in an environment that has seen a lot of cost-related headwinds since the pandemic.

{kind=link}

The longer-term outlook is complemented by a robust backlog of $32 billion, providing visibility and confidence in meeting the outlined financial commitments.

So, what does this mean for shareholders?

Where's The Shareholder Value?

Even before the 2019 merger between L3 and Harris, investors in L3 benefited from a long history of consistent dividend growth.

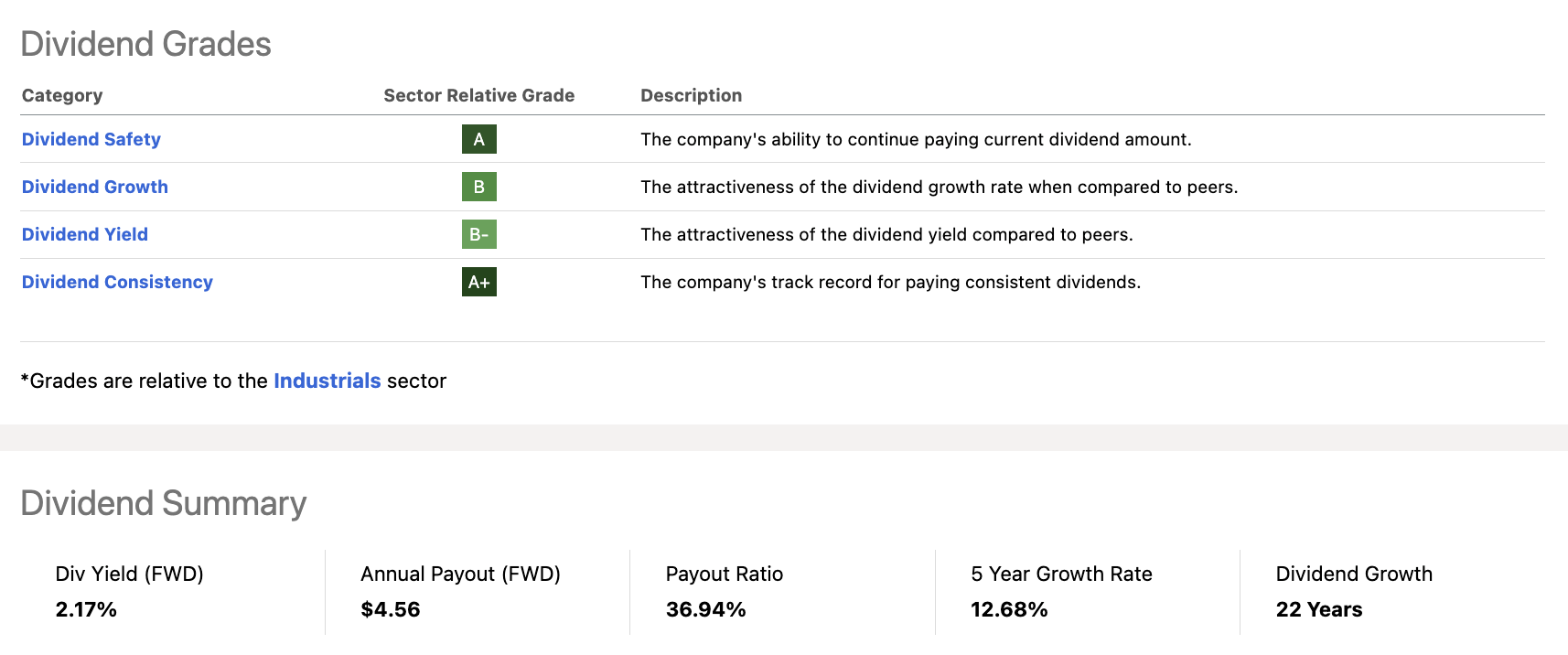

The company has 22 consecutive years of dividend hikes.

Currently, LHX pays $1.14 per share per quarter. This translates to a yield of 2.2%.

This yield is protected by a sub-40% payout ratio. The five-year dividend CAGR is 12.7%.

As a result, it has one of the best dividend scorecards in its sector.

{kind=link}

The company is also a big fan of buying back stock.

Over the past three years alone, L3Harris has bought back 9% of its shares. Most of it occurred shortly after the 2019 merger when the company used the proceeds from divestitures to buy back stock.

With that said, the charts above clearly show that buybacks and dividend growth have slowed.

That's due to the company's focus on post-merger debt reduction.

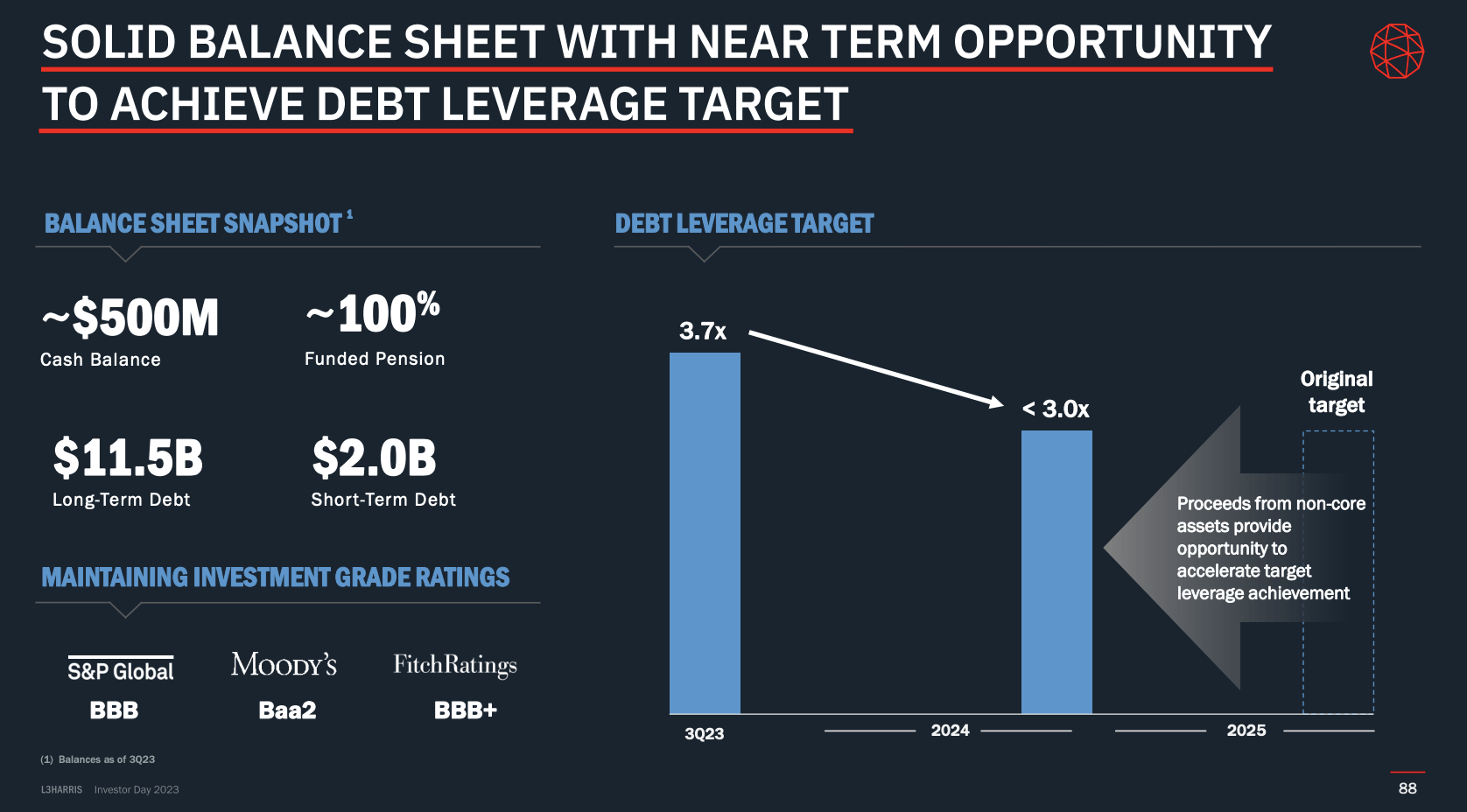

Currently, a significant portion of the free cash flow is earmarked for debt reduction. Achieving a debt-to-EBITDA ratio of 3.0x or lower is a priority, ensuring a healthy balance sheet.

Once it has achieved this target, it plans to distribute every penny of excess cash to shareholders!

{kind=link}

The company, which currently has an investment-grade BBB credit rating, is expected to achieve this target next year.

{kind=link}

As previously mentioned, the company is on a path to generate a +7% free cash flow yield in 2026. This means that next year (or early 2025), it can start to aggressively hike its dividend again and buy back stock, which could result in tremendous shareholder value on a prolonged basis.

This also makes for an attractive valuation.

Over the past few years, LHX has traded close to 22x free cash flow, which I believe is a fair valuation.

Ignoring buybacks and other benefits, $2.8 billion in 2026 free cash flow would indicate a fair market cap of $62 billion ($2.8x22), which is roughly 50% above the current price.

This would imply roughly 14% returns per year through 2026, excluding dividends, buybacks, and debt reduction.

This return is backed by the price/earnings multiple forecast.

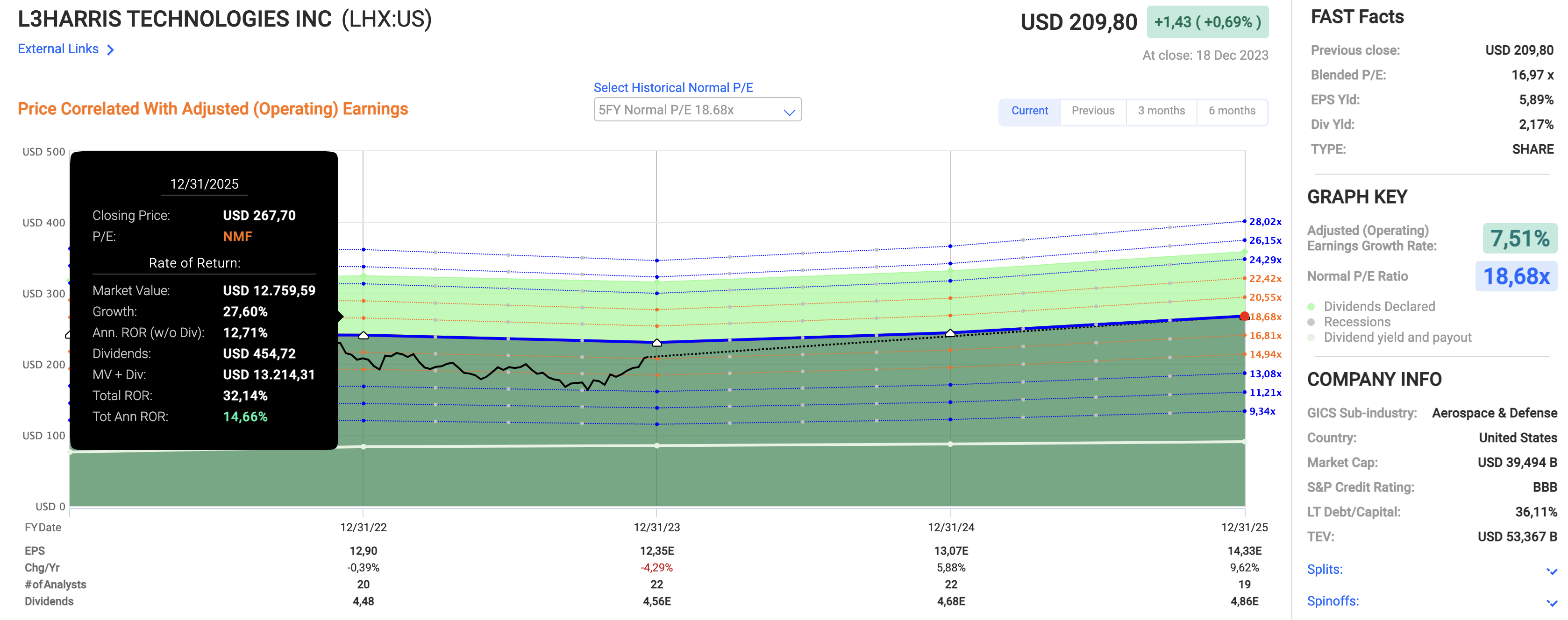

Using the data in the chart below:

- LHX is trading at a blended P/E ratio of 17.0x.

- Its normalized valuation is 18.7x.

- This year, EPS is expected to contract by 4%, followed by 6% growth in 2024 and 10% growth in 2025.

- An 18.6x multiple and expected growth rates suggest between 14% and 15% in annual total return potential.

{kind=link}

On December 15, the company got an upgrade from Deutsche Bank, which upgraded the price target from $184 to $240.

This is 14% above the current price.

All things considered, LHX remains a favorite of mine.

If I could buy just one stock going into 2024, it would be L3Harris.

Takeaway

Despite recent market fluctuations, L3Harris' unique strengths position it as a compelling choice for long-term investors.

From its anti-cyclical business model to a commitment to innovation, L3Harris ticks all the boxes.

The recent Aerojet Rocketdyne acquisition has not only broadened capabilities but also opened doors to lucrative opportunities in the space industry.

With a clear vision outlined in its 2023 Investor Day, including a robust roadmap and shareholder-friendly initiatives, L3Harris appears poised for sustained growth.

The future looks promising with a clear vision, potentially reaching $23 billion in revenue and 16% margins by 2026.

Shareholders can anticipate not just dividends but substantial value as LHX navigates a path of sustained growth and profitability.

For further details see:

14% Annual Return Potential: L3Harris Is My Favorite Dividend Stock Going Into 2024