CME - 2 Buffett-Style Dividend Bargains I Am Buying

2023-06-16 09:00:00 ET

Summary

- My investment strategy, inspired by Warren Buffett, focuses on beaten-down stocks with value and growth characteristics for long-term outperformance.

- In this article, I explain what Buffett is looking for in a high-quality company and how this can help us build long-term wealth.

- I also show you two investments of mine that I recently bought more stock of. Two Buffett-like investments with a bright future.

Introduction

The divergence between growth and value stocks is growing. The economy is close to a potential recession, and the Fed made clear that it will remain hawkish until its job is done - unless it is forced to cut, which isn't bullish either.

In light of these developments, I'm buying beaten-down stocks that come with both value and growth characteristics.

Last month, I wrote a similar article highlighting three stocks that I bought. In that article, I also discussed Warren Buffett's style, which I will elaborate on in this article.

While I would never compare myself to any billionaire investor, I think there are similarities when it comes to buying stocks with the aim of never selling them.

Hence, in this article, I will start by elaborating on the Buffett investment style and explain what I'm looking for in an investment.

So, let's get to it!

What Buffett Is Looking For When It Comes To Investing

Buffett is probably the most well-known long-term investor in the world, with decades worth of experience and public appearances that have allowed observers like myself to understand what he's looking for in an investment.

While he's certainly keeping some secrets for himself, it's not hard to find the basics, as thousands of websites are discussing Buffett-style investments and strategies.

This is from Investopedia :

Buffett belongs to the value investing school, popularized by Benjamin Graham . Value investing looks at the intrinsic value of a share rather than focusing on technical indicators, such as moving averages, volume, or momentum indicators. Determining intrinsic value is an exercise in understanding a company’s financials, especially official documents such as earnings and income statements.

While I like value investing, I wouldn't consider myself to be a typical value investor. Or, to put it differently, I'm approaching value a bit differently.

I like to go for a hybrid between growth and value, companies that are profitable with wide moats and strong free cash flow but also have the ability to grow their business over time at growth rates that exceed GDP growth. These companies have a great shot at beating the market over time.

Now, before I get ahead of myself, here are some factors that make stocks potential Buffett plays. In this case, I asked artificial intelligence to research Buffett's shareholder letters going back as far as 1989.

Here's the result, including the links that were provided:

- Economic Moat : Buffett looks for companies with a durable competitive advantage or an economic moat. This could be in the form of strong brand recognition , high barriers to entry , superior distribution networks , or patents and copyrights . Such advantages provide protection against competition and help sustain profitability over the long term.

- Stable and Predictable Earnings : Buffett prefers companies with consistent and predictable earnings growth . He looks for businesses that have demonstrated stability and resilience rather than those with volatile or unpredictable earnings streams. I agree with that, as I have a hard time dealing with volatile tech or consumer companies that thrive on trends.

- Strong Management : Buffett believes that competent and trustworthy management is essential for long-term success . He looks for management teams with integrity, a proven track record, and a clear strategy for creating shareholder value. I have to admit that this is pretty tough to figure out. Unless you are in direct contact with management, you'll have to rely on the company's track record.

- Free Cash Flow : Buffett emphasizes the importance of analyzing a company's free cash flow, which is the cash generated by the business after accounting for capital expenditures. Positive and growing free cash flow allows a company to invest in growth opportunities, pay dividends, and repurchase shares . As readers may have noticed, I discuss this in almost all of my articles.

- Reasonable Valuation : Buffett seeks stocks that are trading at attractive prices relative to their intrinsic value . He emphasizes the importance of estimating the intrinsic value of a business before considering an investment. Like Buffett, I try to buy companies below what I consider to be their fair value. That may sound obvious, but I'm not chasing charts anymore, betting on companies that may be profitable at some point in the future.

- Long-Term Perspective : Buffett takes a long-term view when investing and focuses on the fundamental value of a business rather than short-term market fluctuations. He prefers to buy and hold investments for extended periods.

Again, I'm not comparing myself to Buffett, but I'm surprised by these results, as it's exactly what I've been doing for many years. Hence, I will use this framework in future articles as well, as I believe it perfectly supports my strategy.

I believe that investors who stick to these results will do very well. This includes avoiding certain money-losing tech stocks that everyone talks about, hyped crypto coins, NFTs, or companies that are highly speculative.

Buying quality investments and letting time in the market do the heavy lifting is the way to go - I think.

So, with all of this in mind, let's discuss the two picks I'm buying.

Norfolk Southern Corporation ( NSC )

My most recent article in-depth article on Norfolk Southern can be accessed here .

While I promised I would stop comparing myself to Buffett, I have to say that we're both into railroads. While Mr. Buffett has owned the BNSF railroad since 2009, which is the largest intermodal railroad and a heavyweight in agriculture, industrial shipments, and chemicals (among others), I'm buying its smaller peer on the East Coast.

As its 1Q23 earnings below show, the railroad generates roughly a quarter of its revenues from intermodal, followed by agriculture, forest, consumer products, and chemicals.

Norfolk Southern Corporation

The railroad connects customers on the East Coast, which was one of the reasons why I bought the stock in 2020. I also own two other railroads that give me exposure to every region and nation in North America. Buying NSC was the perfect fit for my portfolio, thanks to the aforementioned geographic benefits and its consumer-focused transportation mix.

Norfolk Southern Corporation

Not only do these Class I railroads have major moats, but they are also key in every major supply chain imaginable. While railroads are less flexible than trucks (they cannot leave their tracks), they are more efficient and capable of hauling bigger loads.

This also makes them highly cyclical. After all, slowing economic growth will immediately reduce the amount of goods that are shipped by companies.

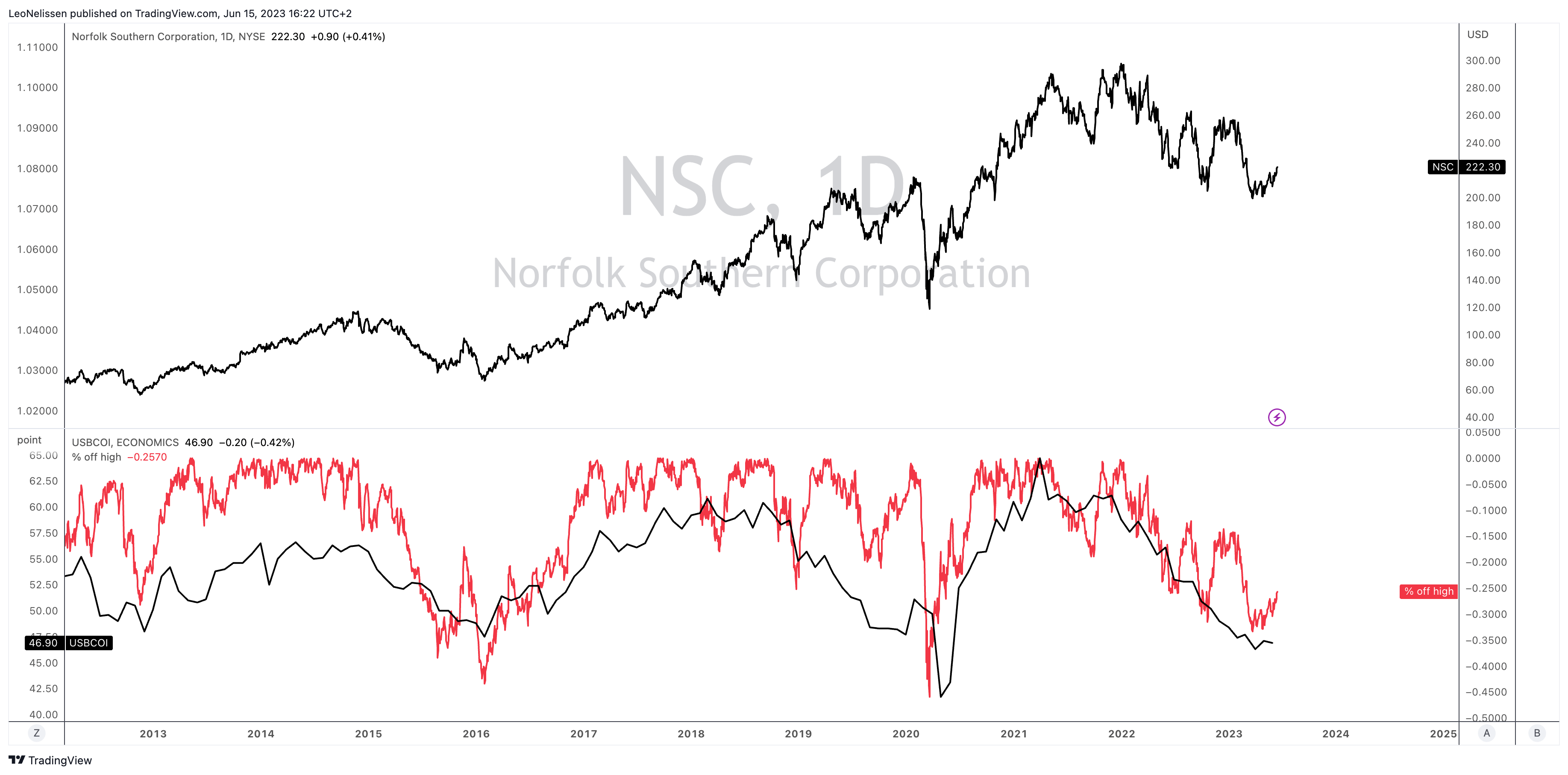

The chart below shows the NSC stock price and the comparison between the leading ISM Manufacturing Index and the % NSC shares are trading below their all-time high. This chart explains why NSC has done poorly since the start of 2022.

{kind=link}

TradingView (NSC, ISM Index)

Note that weakness also included the East Palestine derailment, which ended up costing the company $387 million in the first quarter, causing the operating ratio to rise to 77.3%.

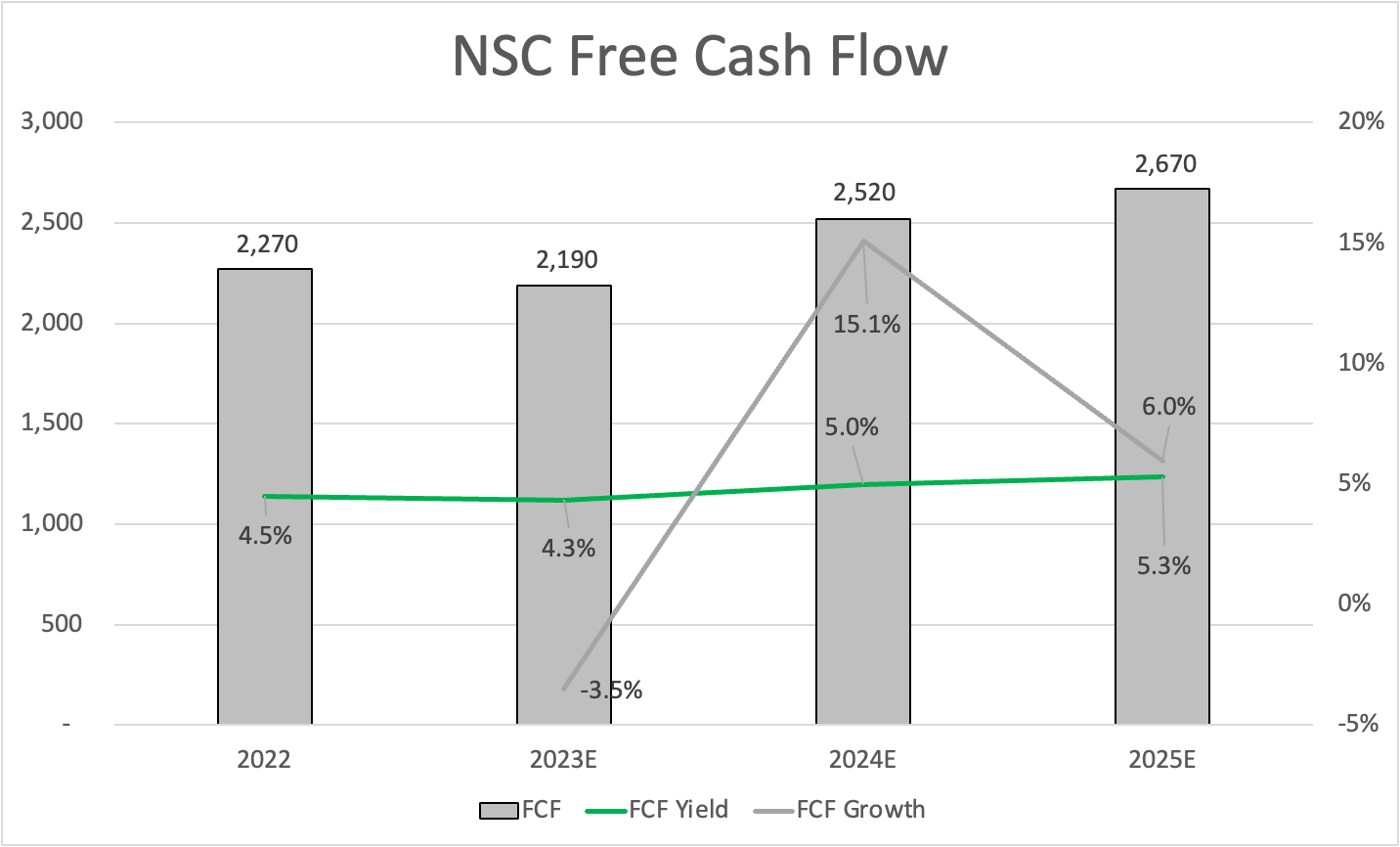

The good news is that even under current conditions, analysts expect the company to grow free cash flow by 15% next year, allowing Norfolk Southern to consistently grow its free cash flow to $2.7 billion in 2025. This implies a 5.3% free cash flow yield, which supports its current dividend yield of 2.4% on top of buybacks.

{kind=link}

Leo Nelissen

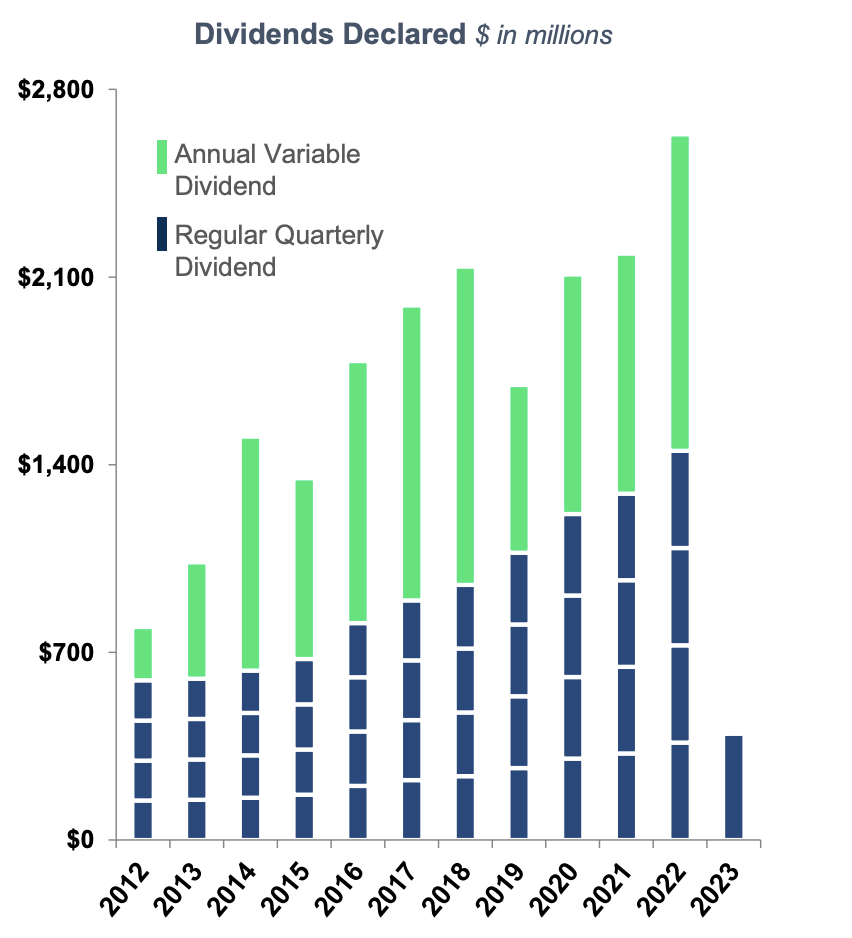

Furthermore, the company has a 2.7x net leverage ratio using 2023 estimates and a BBB+ credit ratio. This allows the company to consistently raise its dividend.

Over the past ten years, the company has hiked its dividend by 10% per year, on average. That number has risen to 11.3% over the past three years.

On a long-term basis, the company will continue to benefit from rail transportation efficiencies, economic re-shoring, and higher export demand for agriculture and energy products as long as the war in Ukraine disrupts international trade flows (caused by, i.e., sanctions).

The company is also reasonably valued. It is trading at 11.1x NTM EBITDA, which is close to the longer-term median.

While the stock could move to the $180 to $190 area if the economy weakens further, I like the risk/reward close to $200, which is why I added more to my position.

FINVIZ

All things considered, I think NSC is a terrific stock that I'm not planning on ever selling.

Stock number two is a financial corporation.

CME Group ( CME )

My most recent article in-depth article on CME Group can be accessed here .

CME Group is a global derivatives marketplace with a robust business model. Formed in 2007 through mergers and acquisitions, including notable exchanges like CBOT and NYMEX, CME Group offers a wide range of futures, options products, and risk management tools.

With a significant presence in various markets such as interest rates, equities, agriculture, and energy, CME Group is a major beneficiary of elevated volatility and the go-to marketplace for futures traders.

With regard to its moat, I believe that CME has a wide moat. While peers are competing in certain areas, the company is the leader in agriculture commodities, equity index futures (it owns the S&P 500 E-Mini), and interest rates. New entrants can only compete with CME if they come up with something so good that major market participants are willing to change. I believe these risks are extremely low.

Thanks to its transaction-based business, CME thrives during periods of market distress and elevated volatility.

While recessions do not necessarily benefit the company's stock price, increased market activity translates into more transactions and profit for the company.

Over the past two decades, CME Group has demonstrated consistent growth in operating cash flow without significant capital expenditure, resulting in higher free cash flow that can be distributed to shareholders.

While CME Group has been involved in significant mergers and acquisitions in the past, the company currently maintains a more passive approach. Their focus is on identifying opportunities that truly create value without the need for external growth.

{kind=link}

CME Group

Hence, the company's regular quarterly dividend and consistent special dividends make almost every penny of free cash flow available to investors.

In 2022, the company paid $8.50 in dividends per share, which translates to a yield of 4.6% using the current stock price. While I cannot predict special dividends, I believe that the company is in a good spot to keep its total dividend yield close to 5%.

Why?

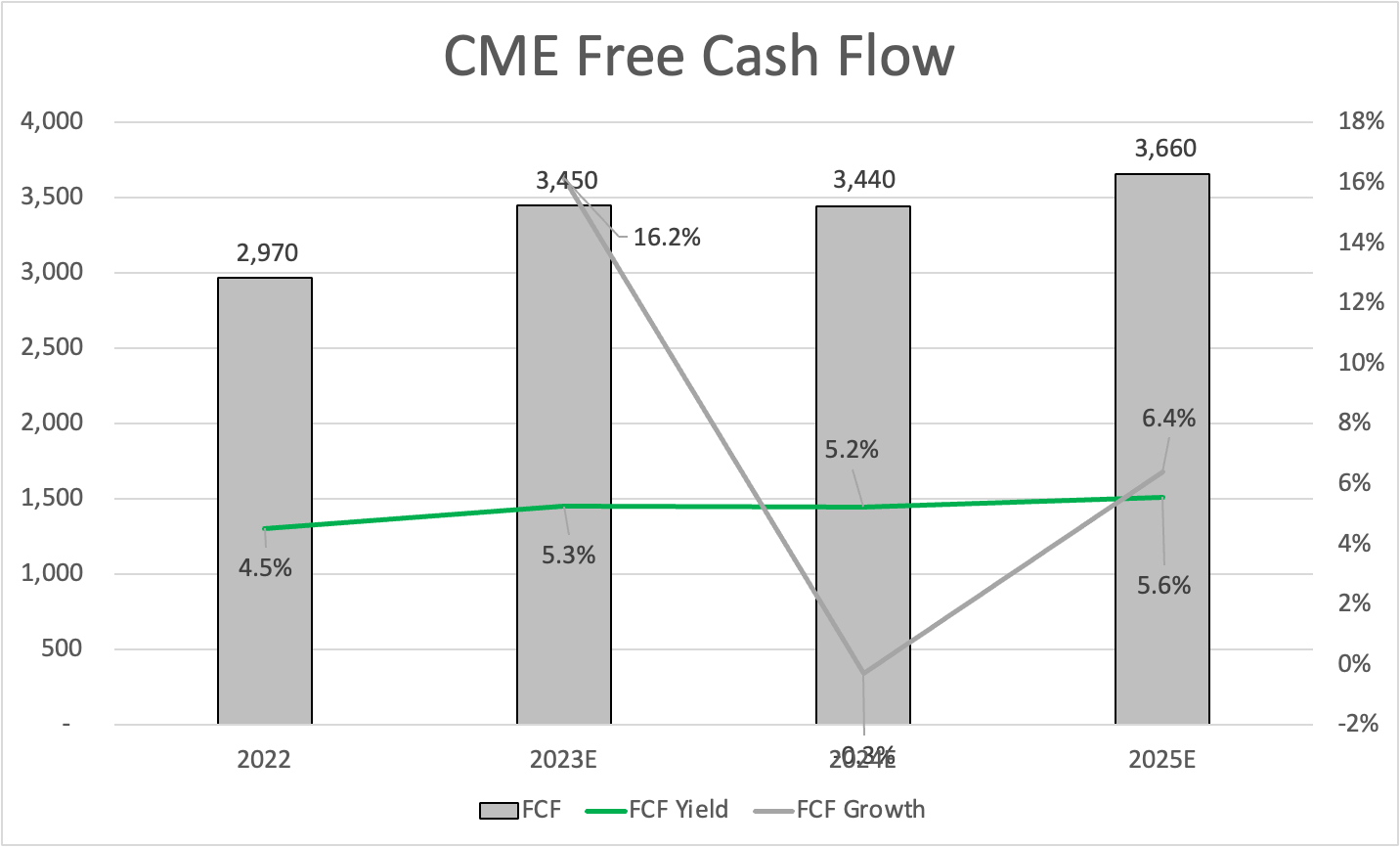

I expect that because the company is expected to consistently grow its free cash flow to $3.7 billion in 2025, excluding unexpected events that could spike volatility. These numbers imply a strong free cash flow yield of more than 5% starting this year.

{kind=link}

Leo Nelissen

Furthermore, trading at 16x LTM EBITDA and below 20x expected free cash flow for 2023, the stock is currently one of the most attractively valued options in over a decade. The company's projected organic growth, supported by solid financials, further strengthens its investment appeal.

While CME is very different from NSC, it also perfectly fits the requirements for a Warren Buffett-style investment. Hence, it's one of my all-time favorite investments in the financial industry, mainly because it's such a perfect way to benefit from the world's most liquid futures and the ever-increasing demand for financial hedging and related activities.

FINVIZ

If the stock price were to fall toward $160 again, I would make it a top-5 position in my portfolio.

Takeaway

In this article, I discussed my investment strategy, inspired by Warren Buffett's style of targeting beaten-down stocks that possess both value and growth characteristics.

By focusing on companies with durable competitive advantages, stable earnings, strong management, positive free cash flow, reasonable valuations, and a long-term perspective, I aim to identify stocks that have the potential to outperform the market over time.

Using this framework, I highlighted two investments that I recently added. The first is Norfolk Southern Corporation, a railroad company with a solid position on the East Coast. Despite short-term challenges, such as derailments and economic slowdowns, NSC demonstrates strong free cash flow growth potential, attractive dividend yield, and reasonable valuation.

The second stock is CME Group, a global derivatives marketplace with a wide moat and a robust business model. As a leader in various markets, CME benefits from elevated volatility and offers consistent dividend payments supported by strong free cash flow generation.

Going forward, I will continue to highlight stocks that I'm buying and elaborate a bit on the fundamental framework used in this article.

For further details see:

2 Buffett-Style Dividend Bargains I Am Buying