CME - 2 REIT-Like Dividend Stocks We're Buying With Both Hands

2023-10-12 07:00:00 ET

Summary

- I discuss two stocks that offer high income, resilience during recessions, capital appreciation, and a high barrier to market entry.

- Norfolk Southern is a wide-moat railroad giant with a history of dividend growth, offering attractive buying opportunities despite recent headwinds.

- CME Group, a financial derivatives powerhouse, offers consistent income through dividends and special dividends and is well-positioned to benefit from rising rates and market volatility.

This article was coproduced with Leo Nelissen.

REITs are fascinating - for many reasons.

If you're reading this, odds are you agree with me.

There are many good reasons to have REIT exposure in a dividend (growth) portfolio. REITs typically have relatively straightforward business models that offer high yields and historically competitive long-term returns. They're an excellent means of stabilizing and diversifying the portfolio.

Having said that, I'm also a fan of C-Corps.

Essentially, my career started by focusing on C-Corps. In fact, 19 of the 21 dividend (growth) stocks in my portfolio are C-Corps.

In this article, I want to take a look at two C-Corps that have similar business models to a REIT and offer some of the same advantages. This means steadily rising income, wide-moat businesses, and the ability to beat the market on a long-term basis - all while collecting dividends.

Even better, because of market turmoil, both of these investments are trading at highly attractive prices.

I own both and have been adding aggressively to them since last year. Given their valuations, I'm almost adding to them on a monthly basis now as I believe in the power to grow my net worth and income for many decades to come using these investments.

So, let's get to it!

Norfolk Southern ( NSC ) - The Wide-Moat Railroad Giant

Norfolk Southern is one of the few remaining public Class I railroads in North America.

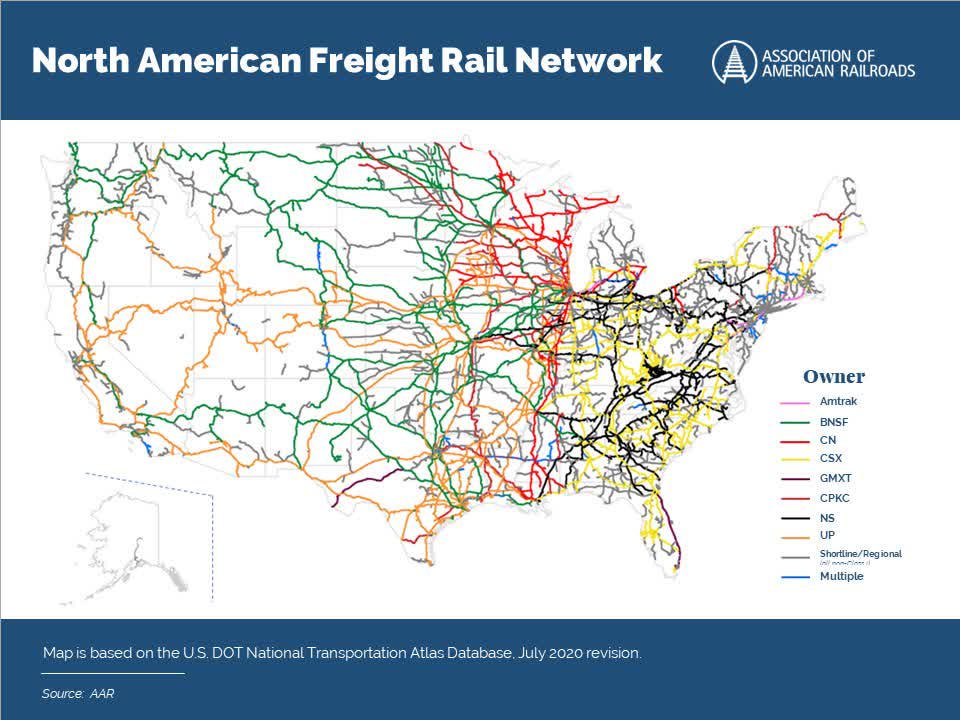

With a $44 billion market cap, this Atlanta-based railroad services every economic hotspot in the east. Looking at the chart below (the black line shows NSC rails), it's almost fair to say that NSC services what used to be the Territory of the Original Thirteen States.

{kind=link}

Not only does the company have a large moat because starting a new competitive Class I railroad is almost impossible, but the company also benefits from the fact that it is a key part of the entire U.S. economy.

It has the largest automotive franchise in the East, the largest steel franchise in North America servicing customers in the Midwest and South (where the steel hotspots are), more than 260 short-line connections, access to 50 ports, and 54 intermodal terminals.

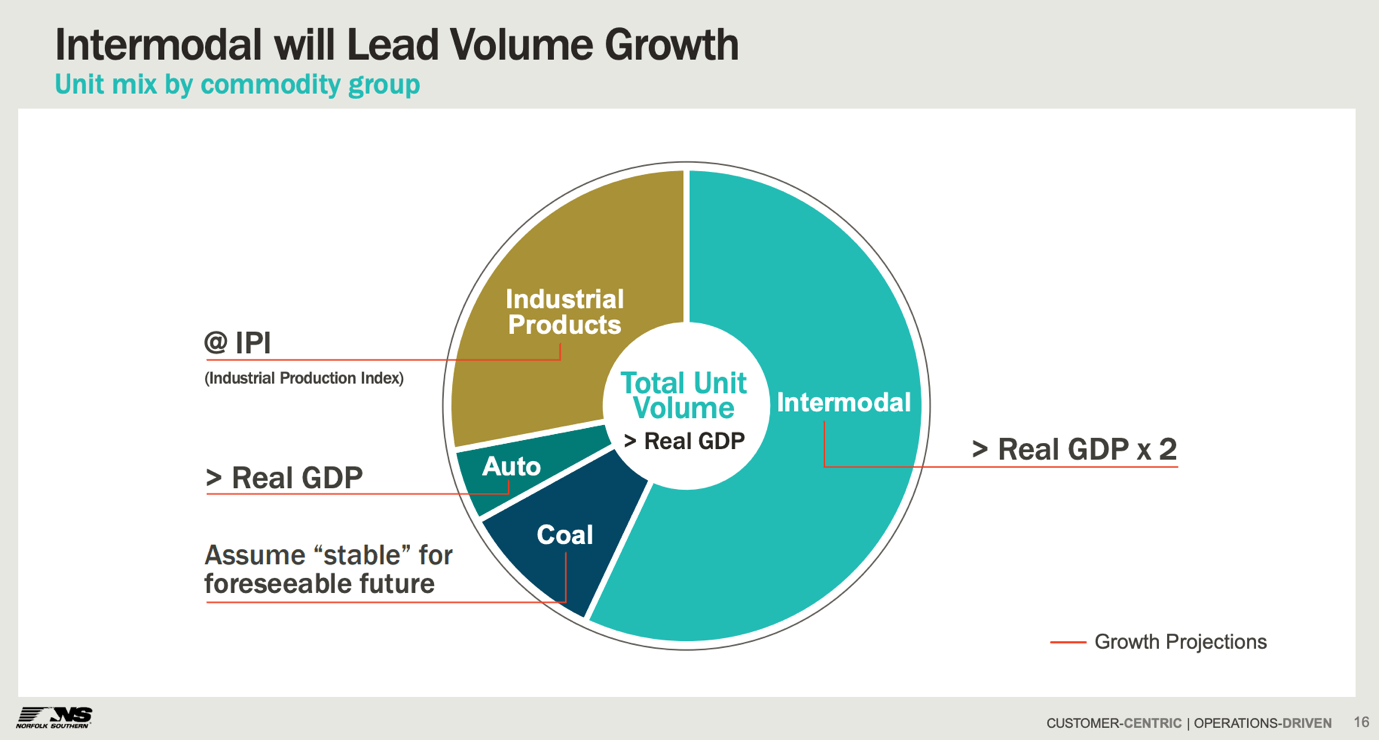

While the company is highly dependent on the economy, it ships products that allow it to outperform GDP growth (even before pricing).

For example, more than half of its volumes come from intermodal, which grows faster than GDP growth (thanks to e-commerce and related trends). Automotive production tends to outperform real GDP growth, while industrial production grows in line with GDP. When including pricing gains in industrial shipments, NSC tends to outperform in that area as well.

{kind=link}

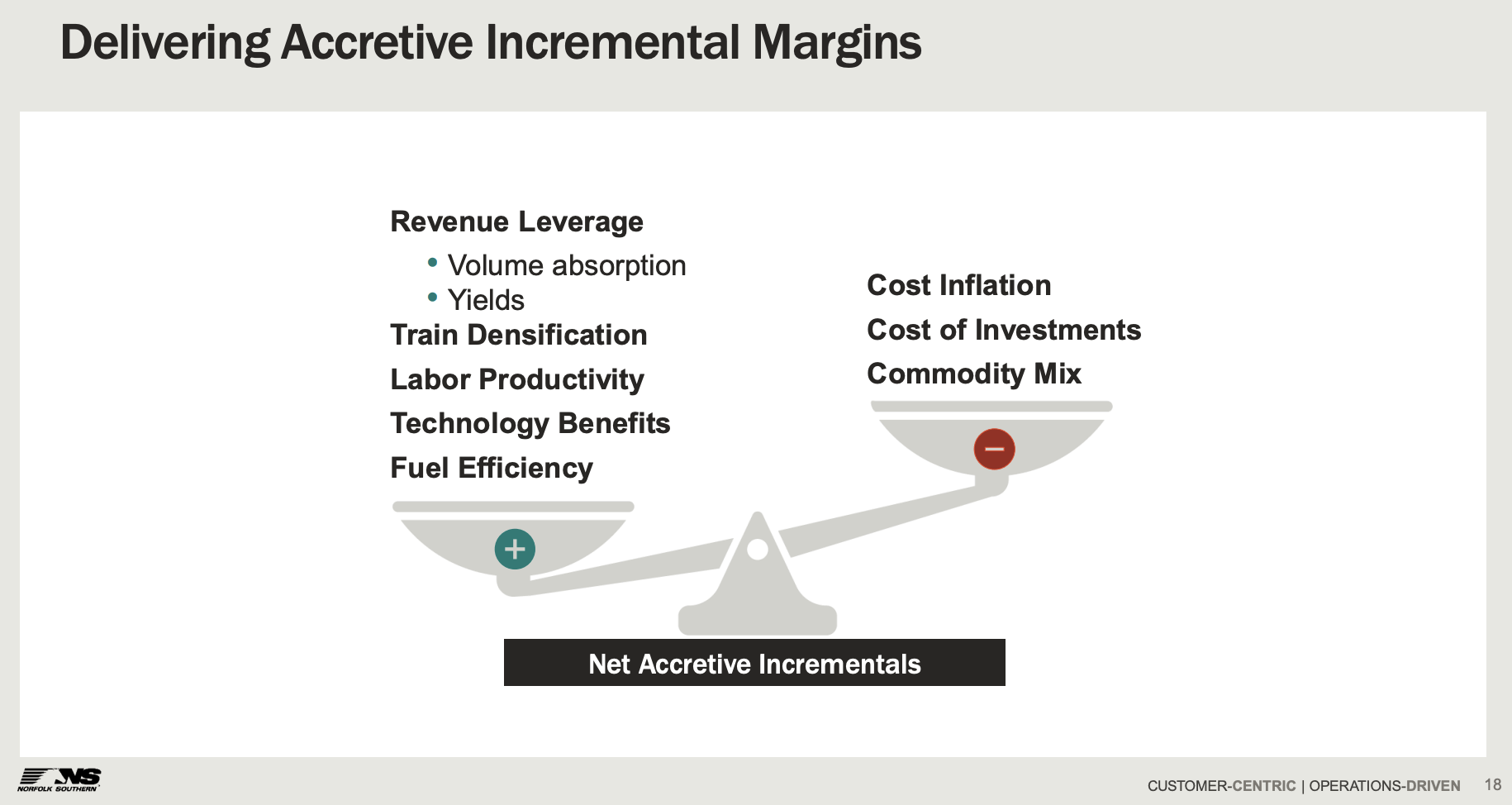

What makes railroads so special isn't just the fact that they have wide moats, but also their competitiveness and efficiency.

Railroads are more than 7x as efficient as trucks. While railroads aren't as flexible as trucks, they're much more efficient long-haul shippers. This also comes with the opportunity to use efficiency gains to drive earnings growth.

Railroads can use volumes, length, labor productivity, technology, and fuel efficiencies to boost their bottom line, offsetting cost inflation, investment costs, and shifts in the transportation mix.

{kind=link}

Most trucking companies are very limited when it comes to ways to improve efficiencies without hurting competitiveness.

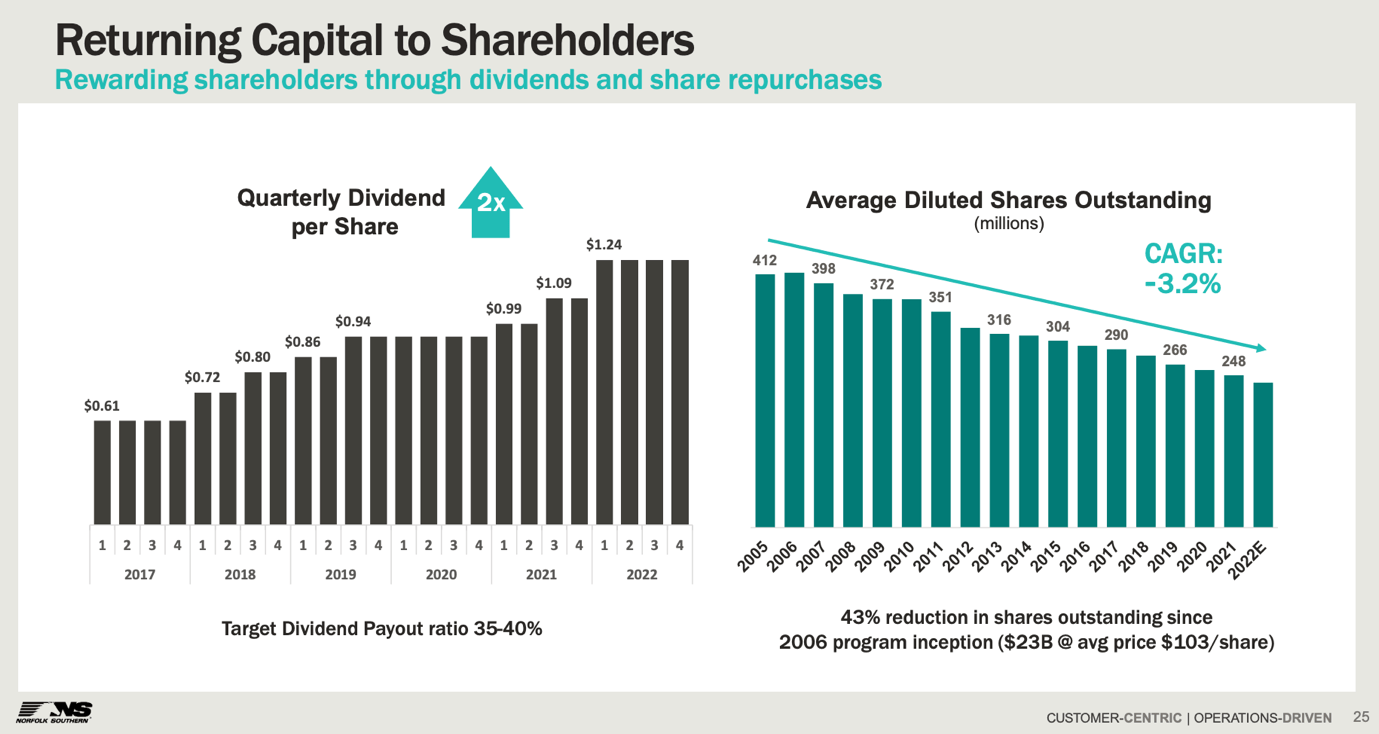

Thanks to these benefits, the company has a terrific dividend track record. Since 2017, the company has more than doubled its dividend. It also bought back 43% of its shares since 2005, which translates to an annual share reduction of 3.2%.

Since 2006, the company has spent $23 billion on buybacks. The average buyback price is $103, which is roughly 50% below the current stock price. That's a very good deal for the company and its shareholders.

{kind=link}

On Jan. 24, the company hiked its dividend by 8.9% to $1.35 per share per quarter. This translates to a yield of 2.8%.

Even during the Great Financial Crisis, NSC kept its dividend consistent. I expect that to happen during the next recession as well - whenever that may be.

Seeking Alpha

Speaking of a potential recession, NSC is currently in a steep downtrend. As strong as its business may be, cyclical headwinds always cause investors to drop NSC shares and allow me to buy NSC shares on weakness.

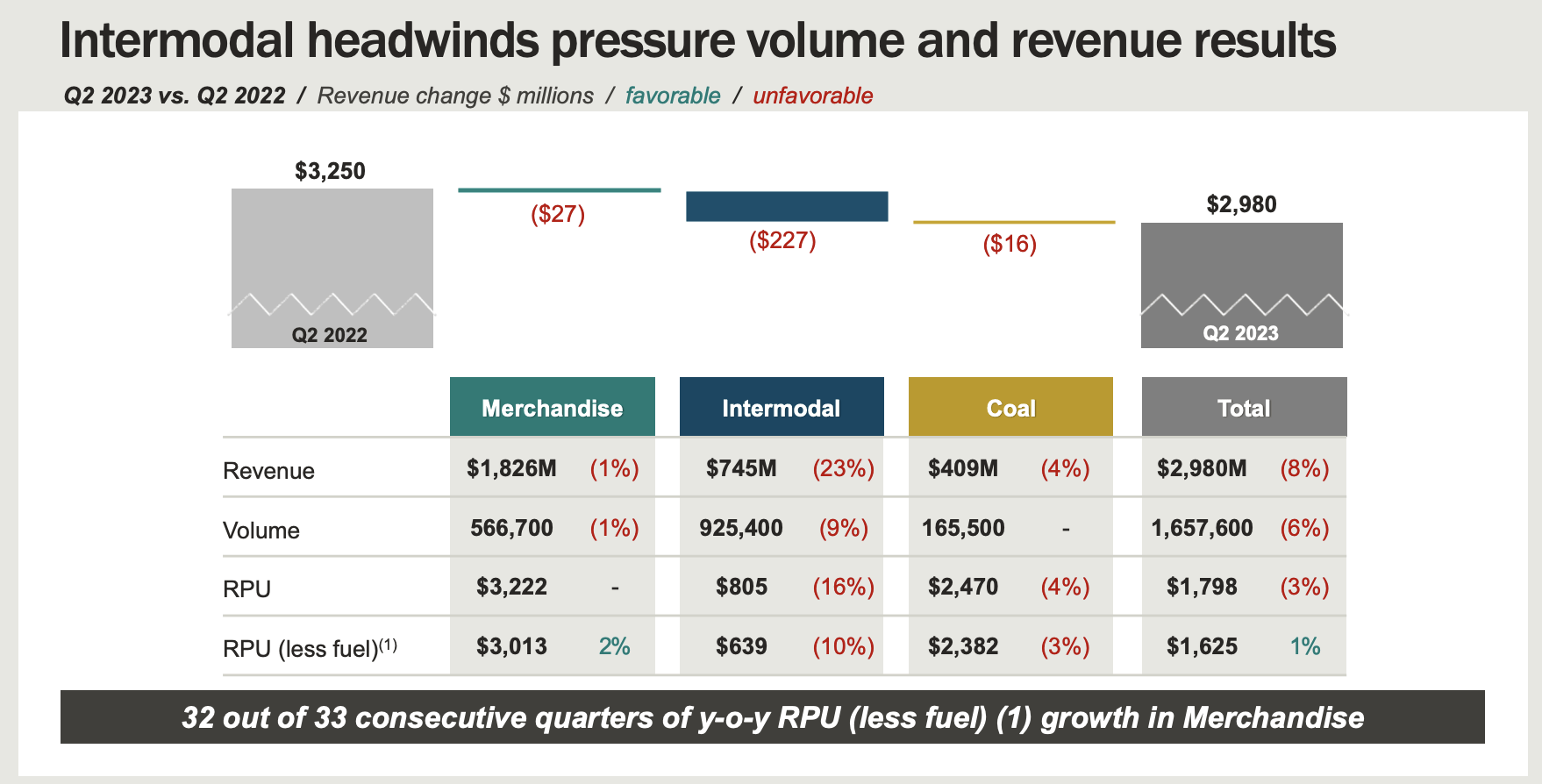

The consumer is weakening, leading to much less intermodal demand. Energy prices have moderated, hurting coal demand, and industrial weakness has weakened merchandise demand.

As a result, in the second quarter, revenues were down 8%, as pricing was unable to offset a 6% decline in total volumes.

{kind=link}

To make things worse, the railroad had to deal with more than $400 million in additional expenses in the quarter due to the derailment in Eastern Ohio, which was all over the news earlier this year.

Hence, the railroad ended up with an operating ratio of more than 80%. Adjusted for this incident, the operating ratio was 66.7%. Prior to the decline in economic demand, railroads were aiming for an operating ratio in the low 50% range (the lower the better).

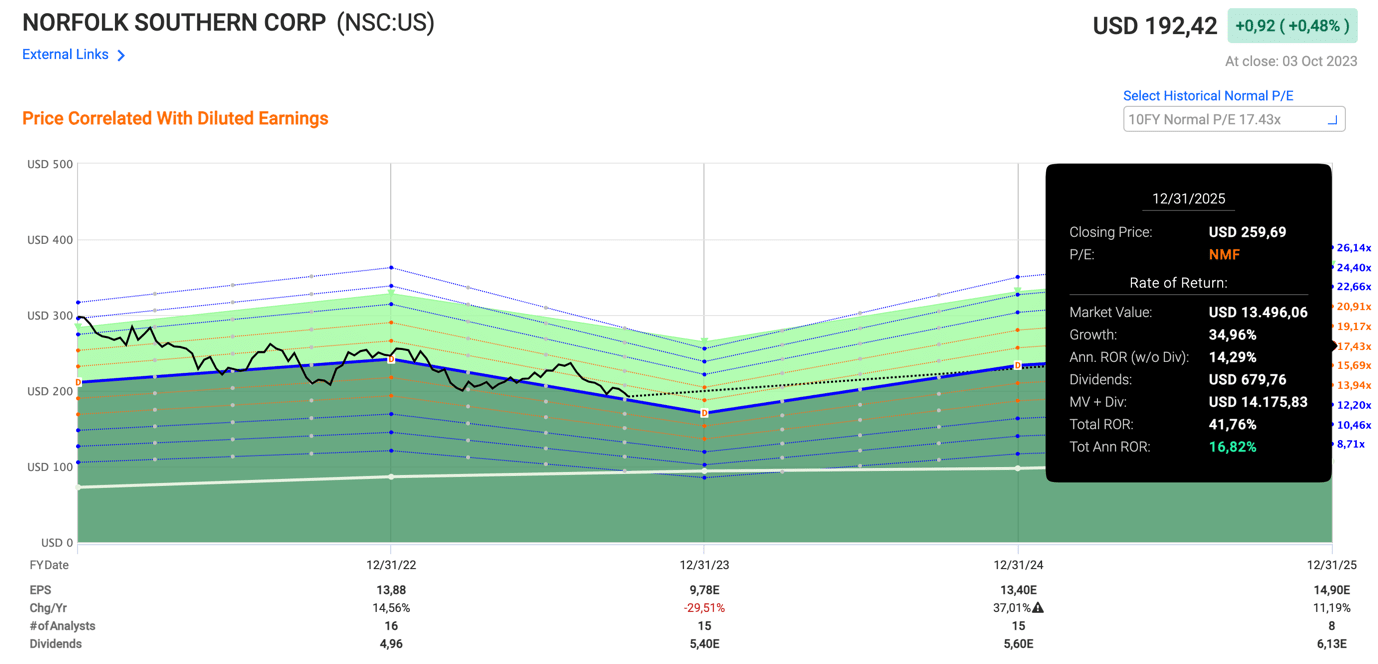

Having said that, while a hard landing could cause the stock to drop another 10% to 15%, the valuation has become attractive. Shares are currently trading close to 17.4x earnings, which is the company's 10-year average. If we assume this valuation holds, we get an expected annual return of 17% through 2025. These numbers incorporate a potential 37% earnings rebound next year, followed by 11% growth in 2025.

{kind=link}

Needless to say, this could come with more downside first.

However, as a long-term investor seeking top-quality stocks, I have started buying more aggressively, as this is one of my all-time favorite wide-moat businesses.

It also comes with a BBB+ credit rating and secular tailwinds like economic re-shoring.

Stock two is different but also a wide-moat powerhouse.

CME Group ( CME ) - Owning The House

One of the coolest REITs on the market is VICI Properties ( VICI ). VICI owns some of Las Vegas' biggest hotels and countless hotels across the nation. Investors make money from the house instead of losing money gambling in one of the company's many casinos.

CME Group is similar.

With CME, investors make money from other people who trade the market.

Founded in 1898, CME Group is a giant that owns the CBOT, NYMEX, the Kansas City Board of Trade, the NEX Group, and COMEX, among others.

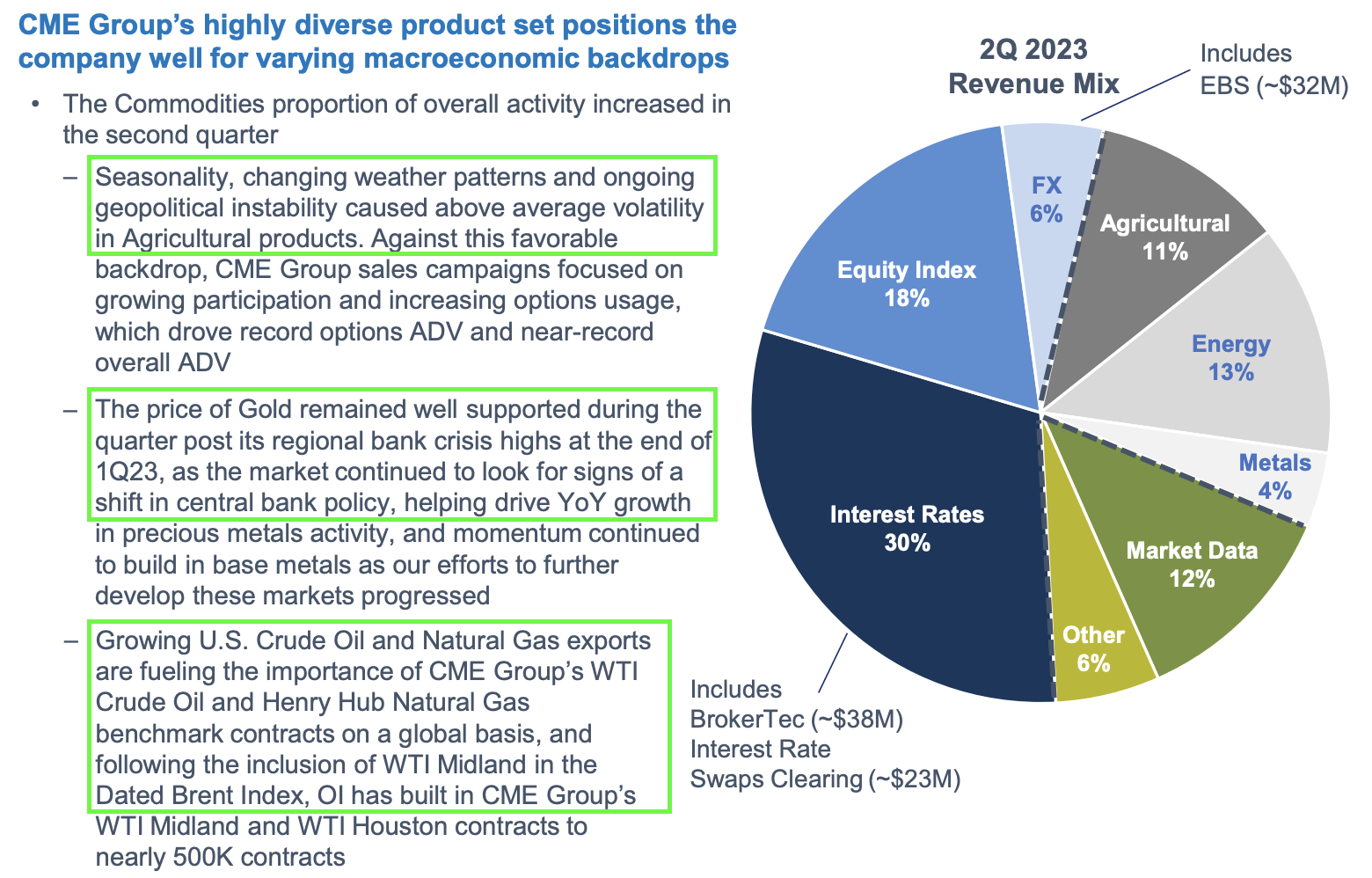

The overview below shows the company's revenue mix, including some comments on second-quarter revenue drivers.

{kind=link}

In total, 30% of its revenues come from interest rate futures and options. The company also has a major footprint in equity indices, where it owns the famous E-Mini contract on the S&P 500. It also owns all major agriculture crop futures, the NYMEX WTI and Henry Hub contracts, COMEX Gold and COMEX Silver, and so much more.

The company also is expanding into options, micro futures (for smaller traders), and exotic futures like lithium. Not only does this allow traders to go wild and speculate on many more products, but it also allows corporations to hedge risks, which is the main purpose of financial derivatives.

In the second quarter, the company saw an average daily volume of 4.7 million options, an increase of 26% compared to the first half of 2022.

The company is also increasingly profitable. In 2Q23, the company made $72.4 cents on each futures/options trade. That number is up from $66.4 cents in 1Q23 due to more commodity trading and pricing changes without the loss of competitiveness.

The company's micro equity segment did well, with a consistent increase in revenue per contract, which shows a combination of product innovation and pricing power.

{kind=link}

Having that said, investors are in a great spot, as CME distributes almost every penny of free cash flow through steadily rising regular dividends and annual special dividends.

Last year, the company paid close to $2.8 billion in dividends, with almost half of it coming from special dividends. In 2022, the company generated $3 billion in free cash flow, indicating a 93% payout.

CME Group

After hiking its dividend by 10% in February, it now pays a $1.10 per quarter per share dividend. This translates to a base dividend yield of 2.2%.

Last year, the company paid a special dividend of $4.50 per share, which would translate to a total yield of 4.3% if the company maintains this special dividend in 2023.

This year, the company is expected to generate $3.4 billion in free cash flow. This would be 13% above last year's result and imply a 4.7% free cash flow yield.

Depending on how generous the company feels and whether it achieves its results, we can expect a total dividend yield close to that number this year - based on the current stock price.

It also needs to be said that CME Group continues to benefit from a number of tailwinds:

- Rising rates and general interest rate volatility require companies to increase their hedging efforts.

- Energy markets have become highly volatile.

- Ever since the Ukraine war started, agriculture commodity markets have become a very crowded place, benefiting future and option volumes.

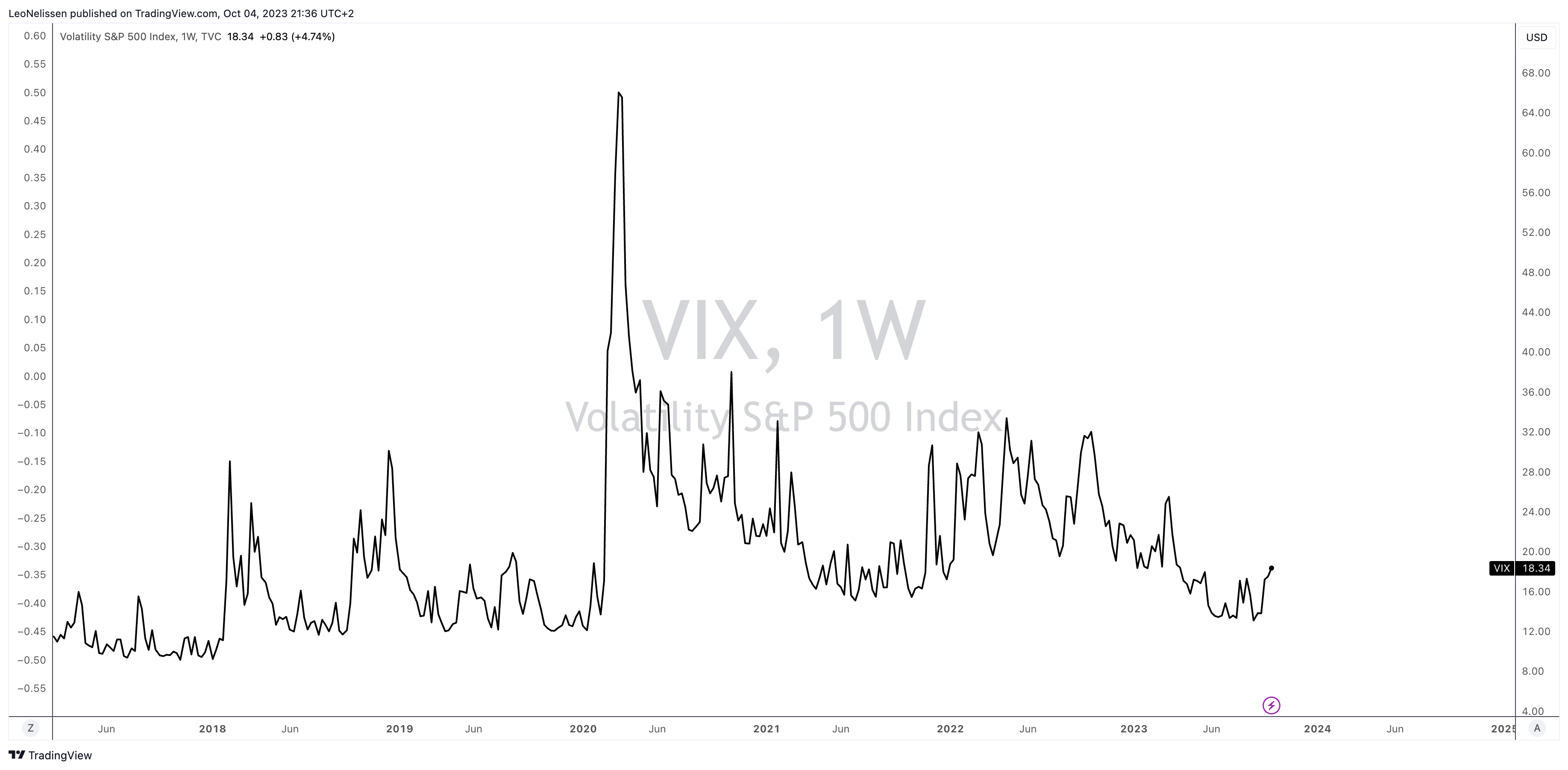

- The S&P 500 volatility index is rising again, as the market seems to be headed for a hard landing.

{kind=link}

While the CME stock price tends to sell off during recessions, the company's revenues tend to increase during recessions (due to higher volatility). This makes CME as recession-proof as most REITs - or better.

Seeking Alpha

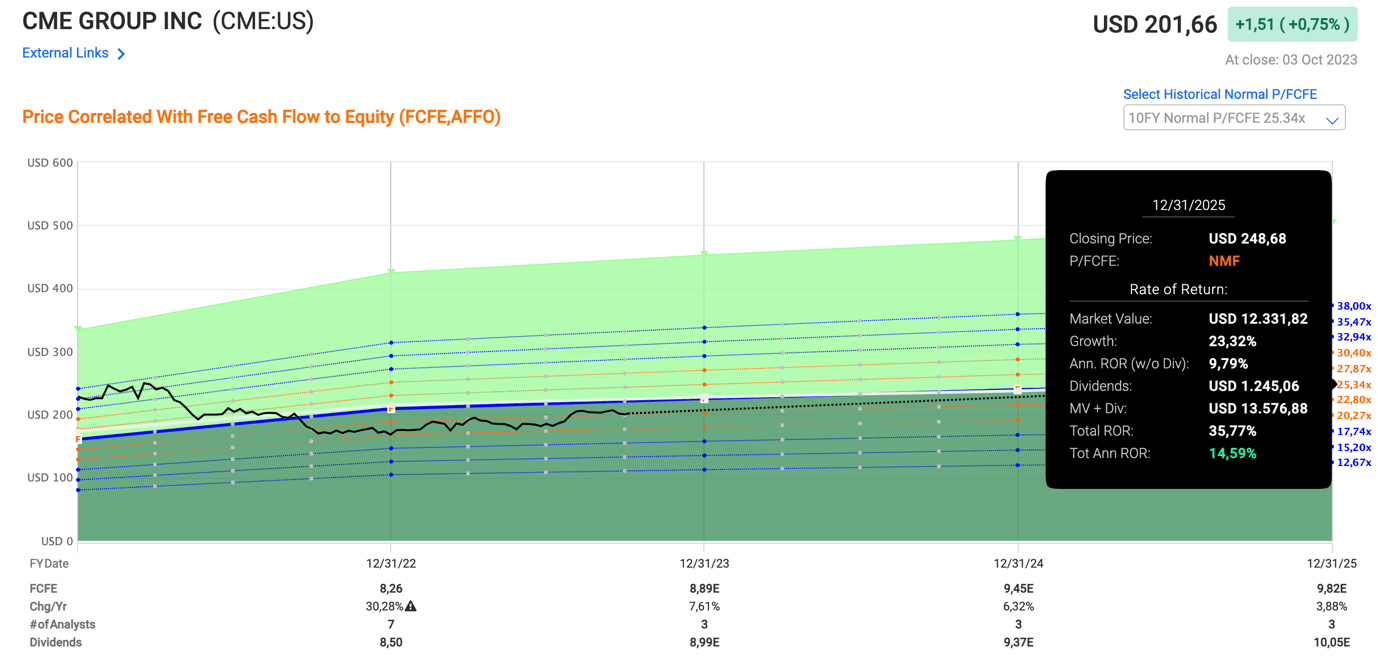

Valuation-wise, the stock is trading at 23x free cash flow to equity ("FCFE"). This is below the 10-year average of 25.3x. If the company maintains this valuation, it could return 15% annually through 2025, based on a 6% average FCFE growth per year during this period.

{kind=link}

While we could see more weakness due to hard landing risks, CME is one of my favorite stocks at the moment, and I'm buying aggressively on weakness.

Takeaway

Investing in REITs comes with benefits like high income, resilience during recessions, capital appreciation, and (in some cases) high entry barriers.

In this article, I discussed two C-Corps that offer similar attributes.

First up, Norfolk Southern, the railroad giant with a massive moat and a history of dividend growth. Despite some recent headwinds, this stock presents an attractive buying opportunity, trading near its historical average valuation. While there might be more turbulence ahead, I'm adding to my position, confident in its long-term potential.

Next, we have CME Group, the financial derivatives powerhouse. Just like REITs, CME offers a consistent income stream through dividends and special dividends. With tailwinds like rising rates and market volatility, it's as recession-proof as they come.

Trading below its 10-year average valuation, CME presents a compelling opportunity, and I'm not hesitating to buy more, especially in the face of potential market volatility.

In summary, these two dividend stocks offer a blend of REIT-like income and the potential for market-beating returns. I'm bullish on their prospects and continue to add to my positions, confident in their ability to grow my net worth and income for decades to come.

Note: Brad Thomas is a Wall Street writer, which means he's not always right with his predictions or recommendations. Since that also applies to his grammar, please excuse any typos you may find. Also, this article is free: Written and distributed only to assist in research while providing a forum for second-level thinking.

For further details see:

2 REIT-Like Dividend Stocks We're Buying With Both Hands