TMUS - 2 REITs All Investors Should Own

2023-06-12 07:30:00 ET

Summary

- REITs are today heavily discounted.

- Some specific REITs combine lower risk and higher return potential.

- We highlight two REITs that most investors should own.

There are few REITs that everyone should own.

After all, each of us has a unique set of circumstances with different return objectives, tolerance for risk, need for income, time horizon, etc.

Therefore, some investors may favor more speculative names like Medical Properties Trust ( MPW ), while others will seek safety in a blue-chip like Realty Income ( O ).

But on rare occasions, some individual REITs become so compelling that they could make sense for almost every investor profile.

In today's article, I want to highlight two such examples.

These are high-quality blue-chip style REITs that are typically owned by more conservative dividend growth investors, but they have now become so heavily discounted that they are starting to make sense also for more aggressive investors who are seeking upside plays.

American Tower ( AMT )

AMT is the biggest cell tower REIT in the world. It leases towers to companies like AT&T ( T ), Verizon ( VZ ), and T-Mobile ( TMUS ) on a long-term basis and profits from the growth of data consumption:

American Tower

It is a very consistent and predictable business that delivers steady cash flow, and AMT pairs this defensive business model with a fortress, BBB+ rated balance sheet with low debt and long maturities.

As a result, its business is recession-resistant and it isn't heavily impacted by the surge in interest rates.

Moreover, AMT has attractive growth prospects:

- Its leases are long and generally include fixed 3% annual rent hikes.

- In addition to that, AMT is adding new tenants to its existing towers.

- And finally, it is also acquiring/developing new towers to grow its portfolio.

All in all, the company has 5-8% annual growth prospects, which paired with its ~3% dividend yield has historically resulted in above-average returns with below-average risk.

Here is its performance relative to the S&P 500 ( SPY ):

But here's the thing:

REIT share prices have collapsed, and AMT wasn't immune to the crash.

Its share price has dropped a lot more than other REITs ( VNQ ) and that's despite being a much safer and stronger business than most others:

Some REITs own challenged properties like office buildings, others are overleveraged, and some are poorly managed.

Those may deserve to see their share price crash in today's environment.

But that's not the case with AMT.

In fact, even as its share price dropped by 33%, its cash flow rose by 7% - so adjusted for its growth, it is down by closer to 40%, which is quite exceptional for such a high-quality REIT.

As a result, AMT is now priced at a historically low FFO multiple of 17x, down from 25x in late 2021.

I think that 25x may have been a bit much, but 17x is very reasonable. That's the typical valuation of an average REIT.

We estimate that its fair value is around $220 per share, which means that the stock has about 20% upside potential from today's discounted share price.

If you combine this upside with the 3.4% yield and the 6% annual growth, you get very attractive total return prospects from a relatively safe investment, and this is why AMT makes sense today for most investors.

We give it a Strong Buy rating and believe that it offers some of the best risk-to-reward in today's uncertain world.

At High Yield Landlord, we already own a position in its close peer, Crown Castle ( CCI ), we don't have a strong preference between the two.

NNN REIT ( NNN )

NNN REIT is a blue-chip REIT that specializes in "triple net lease" properties, which are single-tenant freestanding service-oriented properties such as Dollar General ( DG ) stores, CVS ( CVS ) pharmacies, and Wendy's restaurants:

NNN REIT

We call them "triple net lease" properties because the lease is structured in a way that's very favorable to the landlord:

- The lease is very long at 10+ years.

- All property expenses are carried out by the tenant.

- The lease includes automatic annual rent hikes, regardless of how the economy is doing.

- The tenants typically enjoy a 2-3x rent coverage, meaning that they earn plenty of profits to cover the rent payment.

- The tenant is highly dependent on your specific property because it is their profit center, reducing the risk of vacancy.

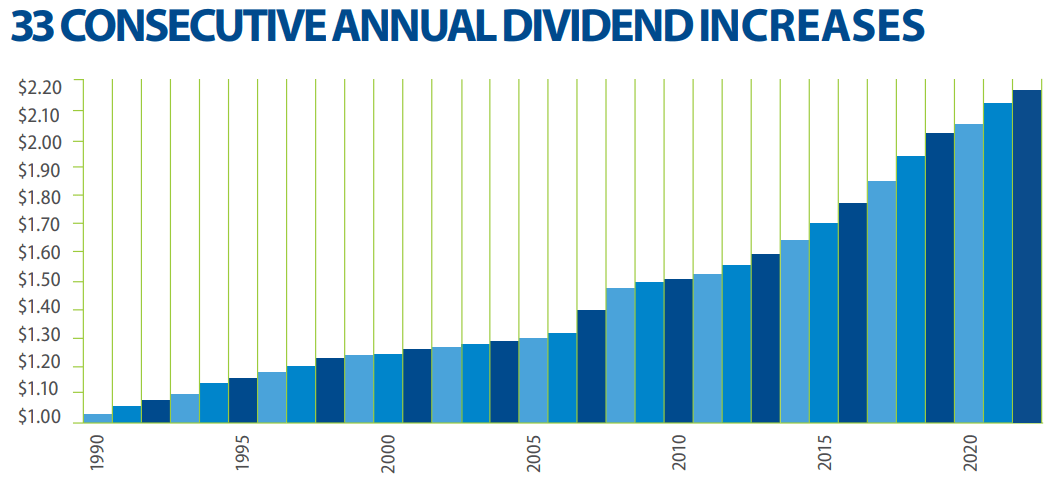

As a result, the cash flow is highly consistent and predictable and the proof is in the results. NNN has managed to grow its dividend for 30+ years in a row and that's despite going through many crises over time:

{kind=link}

Not even the great financial crisis or the pandemic could stop NNN.

Despite that, the market is today again panicking, and it has caused NNN's share price to crash as if its business was finally going to break:

The market fears retail as we potentially go into a recession, but it appears to have overlooked or at least underappreciated the fact that NNN is invested in highly resilient, service-oriented net lease properties.

Moreover, the market also fears the potential impact of rising interest rates, and appears to have underappreciated the fact that NNN has a BBB+ rated balance sheet with a low 30% LTV, all of with a fixed rate, and very long debt maturities at 13 years on average.

Therefore, the impact really isn't significant, and this explains why NNN is able to keep growing at a steady ~5% per year from its contractual rent hikes and new property acquisitions.

We think that the market has overreacted and it has caused NNN's to become undervalued. As of right now, it is priced at just 13x FFO, which compares very favorably to its historic range of 16-24x FFO.

We estimate that its fair value is around $55 per share, which would price the shares at 17x FFO, and result in 30% upside from here.

The 5% dividend yield paired with its 5% growth prospects and 30% upside potential will likely result in very attractive total returns for investors over the coming years, and considering that this is coming from a relatively safe investment, we think that the risk-to-reward is very compelling.

Bottom Line

Blue-chip REITs rarely come on sale.

When they do, don't miss them.

We think that AMT and NNN are two REITs that most investors should own because they offer some of the best risk-to-reward prospects in today's market.

For further details see:

2 REITs All Investors Should Own