ACTV - 2023: A Year Of Expenses

Summary

- Turning on the news will swiftly tell you what is going wrong in the economy.

- Looking deeper at the underlying mechanism reveals opportunity.

- Supply sensitive areas are well positioned.

Expenses are up across the board in 2023 and it is taking a big bite out of margins. Earnings are declining across most of the S&P sectors and consensus estimates for 2023 are ratcheting down. The outlook for 2023 may seem bleak, but there are underlying pockets of strength.

This report will examine the macro factors challenging the market and identify areas that are better prepared to come out ahead.

Overall macro environment

As you already know, inflation and rising interest rates are major forces right now, but there are many types of inflation and many ways in which interest rates can impact the market.

I think the origin of these problems is a supply problem. Not enough is being produced to meet demand.

High levels of demand is usually a good thing as consumption is the largest component of GDP. High demand is often causally associated with high GDP growth. Demand is good for the economy when companies and workers produce more which causes them to earn more which in turn allows them to demand more.

Since production is up along with the demand, there is enough supply to meet the demand and an economy can achieve growth without inflation.

The current source of demand is different. It is demand without a corresponding increase in production. Allow me to illustrate this with 3 graphs.

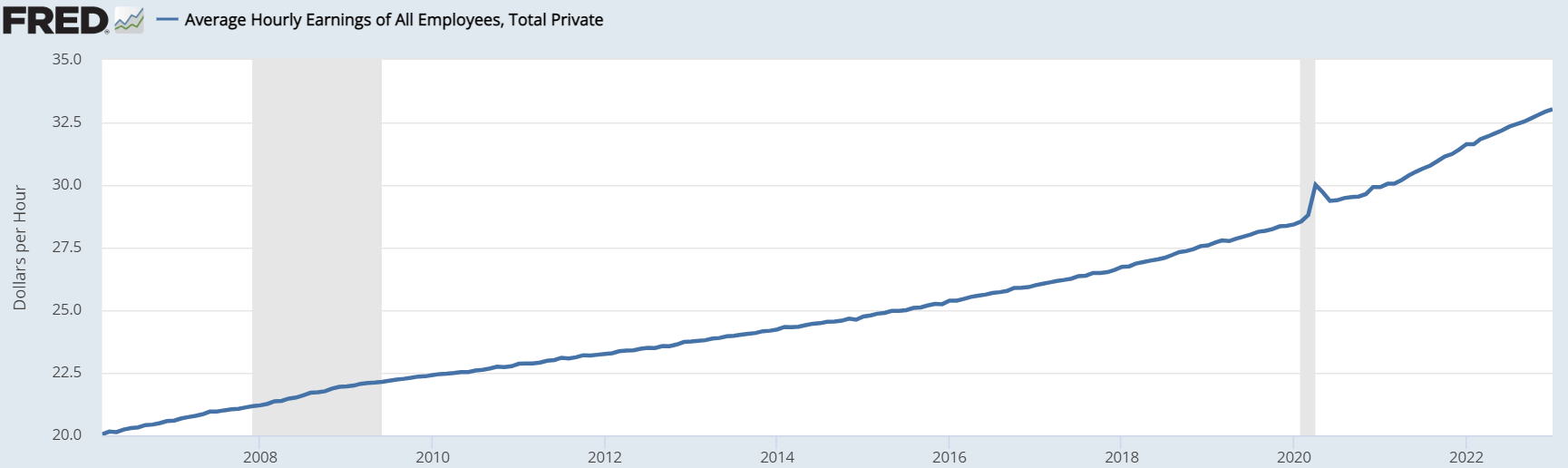

Wages are up significantly.

{kind=link}

In fact, wages have been trending up for a couple decades. I think this is generally a good thing. However, in the past, increased wages have corresponded to increased productivity. That is the favorable economic feedback loop we discussed above. Production --> Wages --> demand --> absorbs the production.

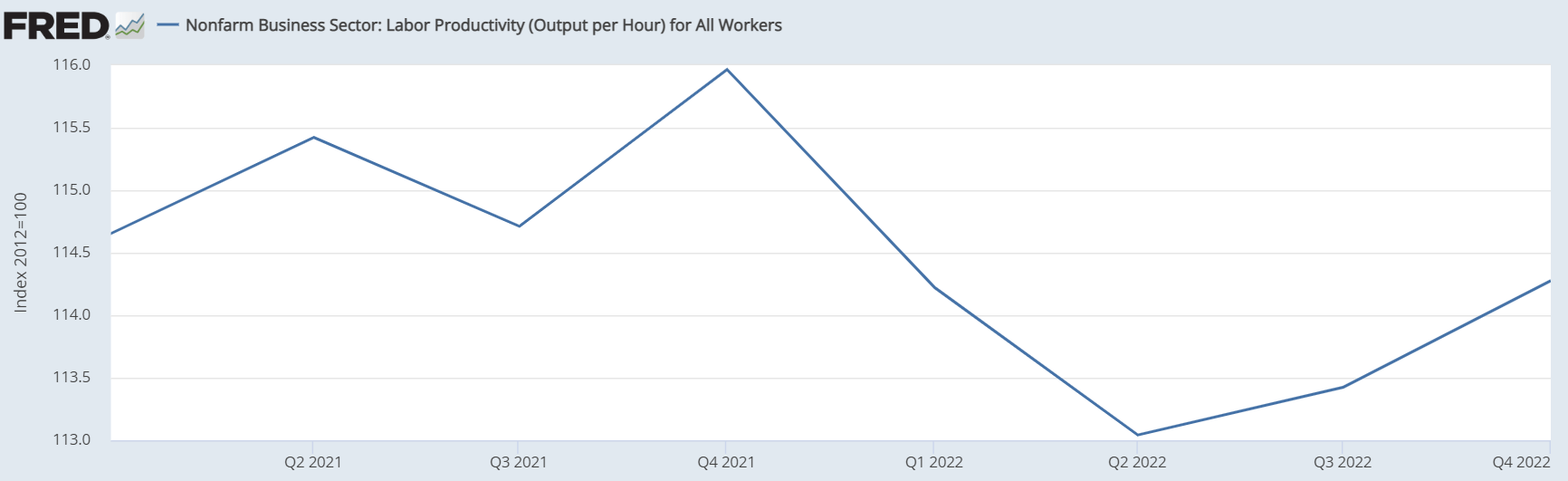

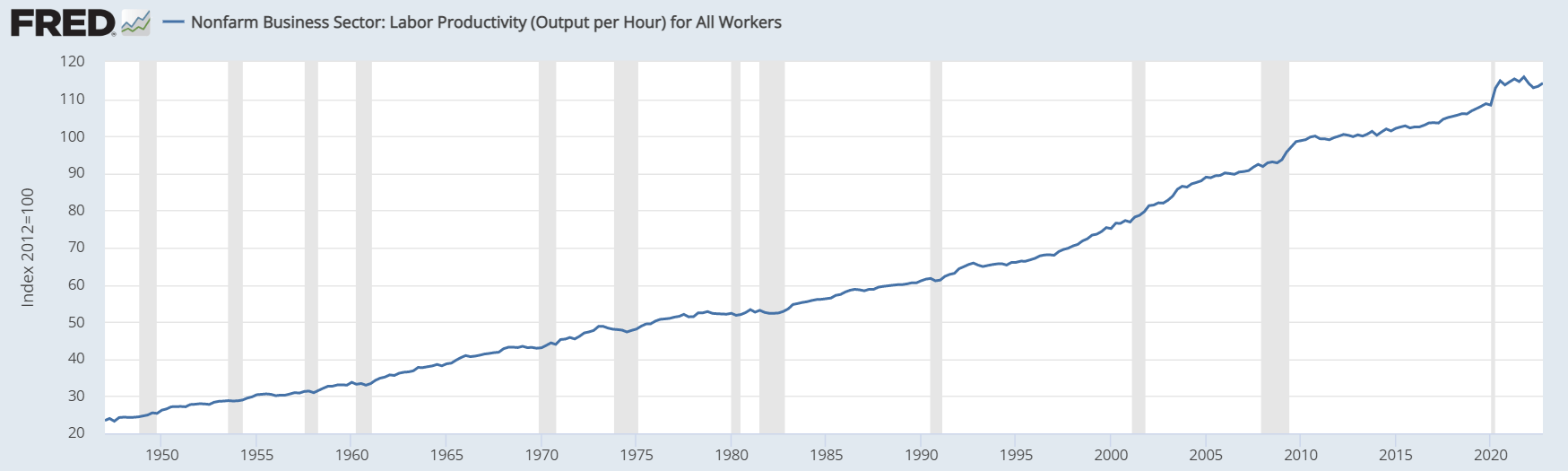

This cycle is different because productivity (output per hour worked) has decreased.

{kind=link}

This is quite an unusual change as productivity has had a 70 year+ uptrend.

{kind=link}

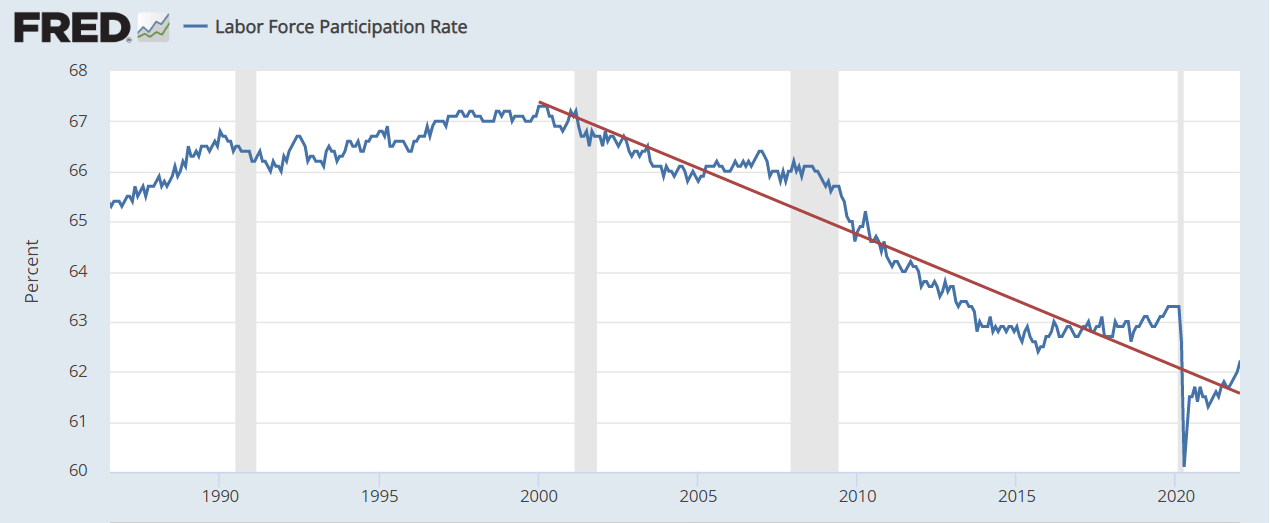

Compounding the problem of lower productivity is a reduction in labor force participation. Participation rate has been declining for 2 decades but until recently it was made up for by increases in productivity.

{kind=link}

Today's economy is the first time we have really had to grapple with simultaneous lower productivity and low labor force participation.

The result is that not enough is being produced but because wages are up across just about every sector, demand is full. It doesn't take much economic knowledge to know that is a recipe for higher prices.

What is being done about it?

When demand is too high for supply there are really only 2 ways to fix it:

- Increase supply

- Decrease demand

I would prefer to see the former as I think it is healthier for the economy, but Fed policy can only directly impact the latter. Blunt instruments are not ideal, but they are the only tools we have.

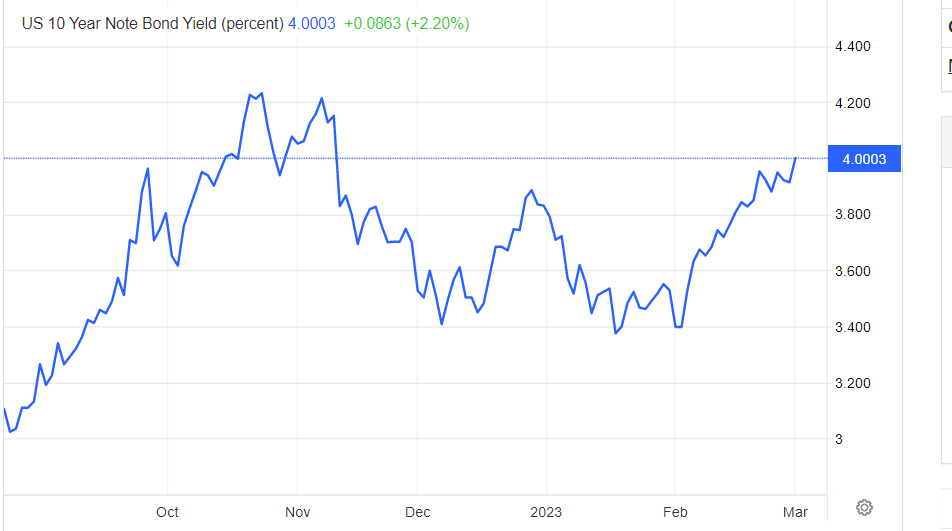

A combination of quantitative easing ((QE)) and rate increases has been implemented in an effort to tamp down demand. So far it has succeeded in inverting the yield curve and dramatically raising cost of capital. At the end of February, the 10 year Treasury yield crossed over 4%.

{kind=link}

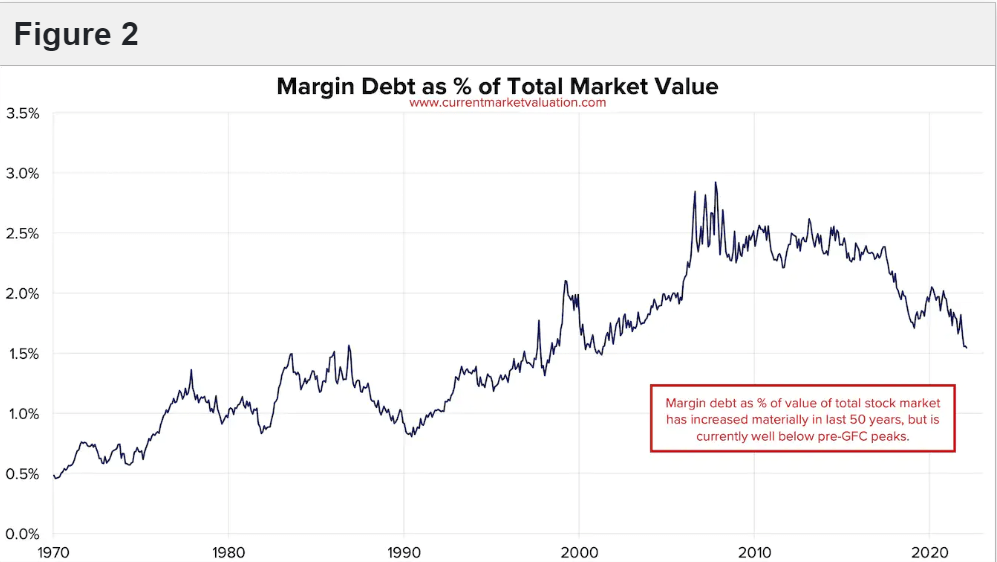

Capital markets are feeling the strain of increased cost of capital. Investors are selling stocks and margin balances have shrunk substantially.

{kind=link}

The theory behind doing this is that it will shrink demand in a couple ways:

- Lower stock market reduces the wealth effect which causes people to spend less.

- Higher cost of consumer borrowing leads to less consumer spending.

- Higher interest on savings encourages saving rather than spending.

Unfortunately, I think there is also some risk of it shrinking supply.

While higher credit card debt cost reduces consumer demand higher cost of capital means less capital investment. Companies have dramatically scaled back on projects that would in the long run increase productivity.

Impact of environment

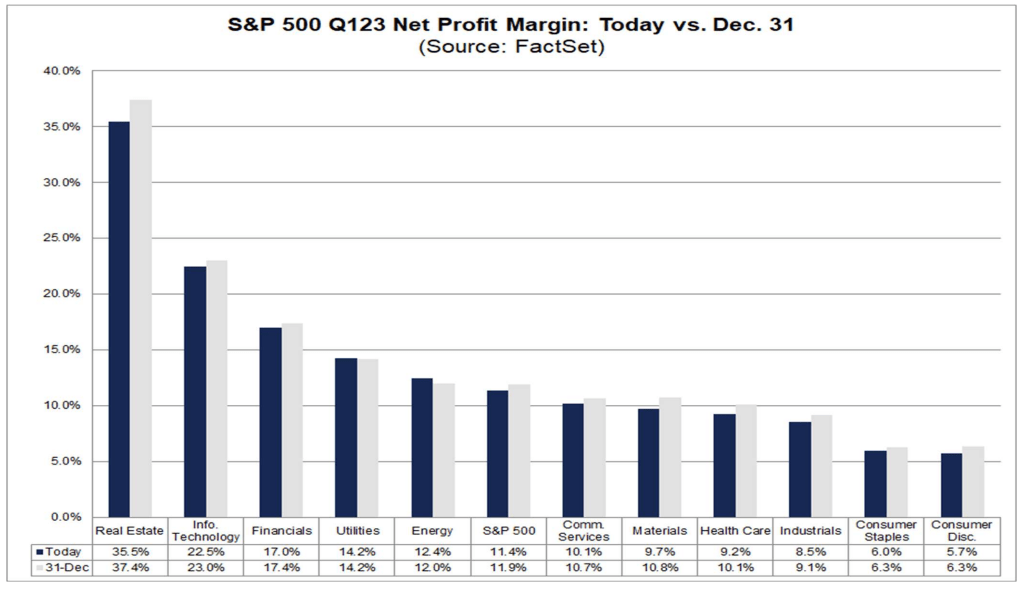

Labor costs more. Capital costs more. Input goods cost more. The net result is higher cost and lower margins. Among the 11 S&P sectors, margins in February as compared to December are lower in all but energy ( XLE ) and utilities ( XLU ).

{kind=link}

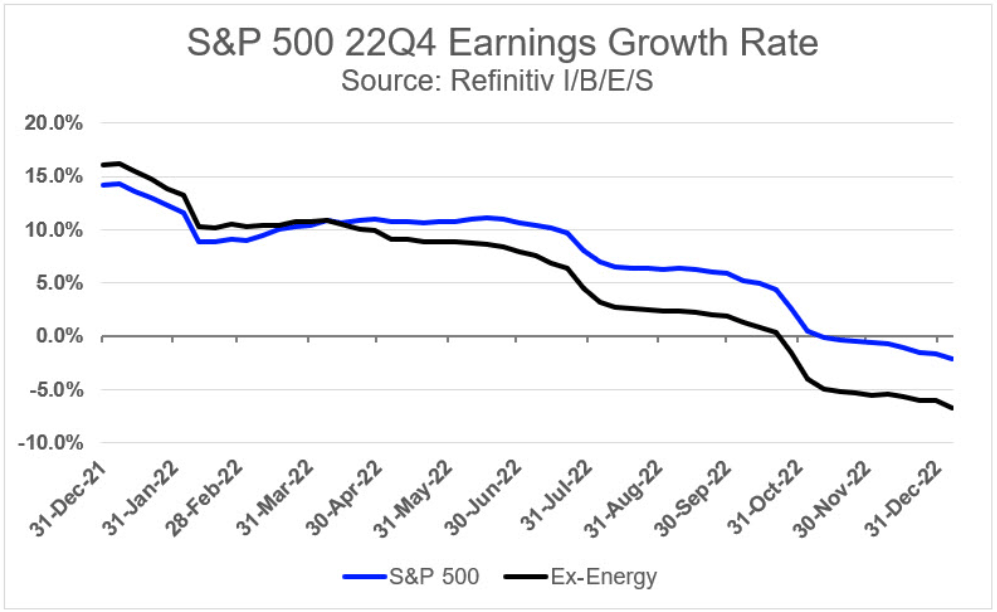

This has taken the growth rate of the S&P negative.

{kind=link}

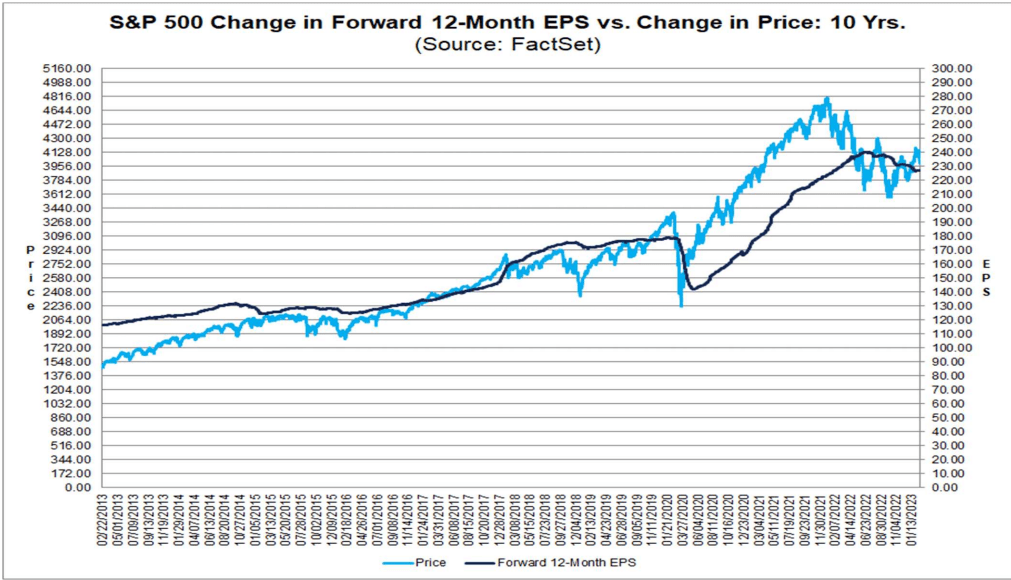

Indeed, analyst estimates for forward S&P earnings have pulled back significantly from 240 in mid-2022 to about 225 now.

{kind=link}

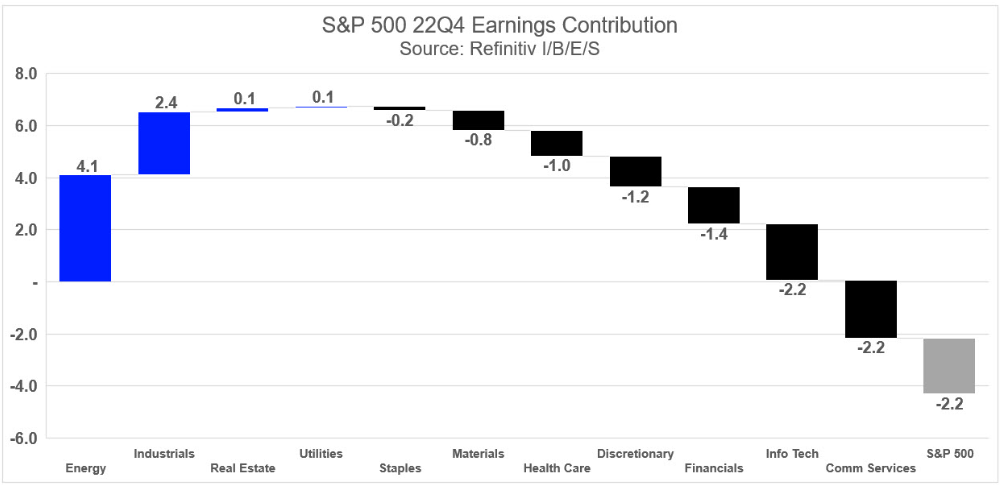

Earnings contribution seems to be worst in the high cost (low margin) sectors with positive contributions from energy, industrials ( XLI ), real estate ( XLRE ) and utilities.

{kind=link}

I want to spend some time digging into why this might be the case because I think it holds the key to which areas are best positioned going forward.

Why these areas are faring better

As discussed above, the Fed is putting pressure on demand, but also constraining capital investment in new supply.

Thus, a well-positioned company is one that is inelastic with respect to demand and elastic with respect to supply. That is largely what these 4 sectors are.

Inelastic demand

How much natural gas does a consumer buy? Enough to heat their home to about 68 to 72 degrees depending on their preference. It is not the sort of item one consumes less of when finances are tight. This keeps revenues flowing for energy and utilities.

Similarly, demand for most industrial goods is largely static with respect to price. Ford isn't going to buy less input parts just because the input parts cost more. They will buy however many parts they need to complete the cars in production.

Real estate demand has areas in which it is elastic. I think hotels, office and self-storage can be foregone if a company or individual is trying to spend less, but other areas are quite inelastic:

- Single family homes

- Apartments - perhaps minor downgrading to cheaper end

- Warehouses

- Manufacturing facilities

- Hospitals

- Communications infrastructure

- Farmland/Timberland

The real estate is rented largely to perform an essential function. It is one of the last things consumers and businesses want to cut.

While these sectors have resilient demand in the face of tightened budgets, real estate and energy are highly sensitive to supply.

Elastic with respect to supply

OPEC exists for a reason. If significantly more oil and gas is produced than is needed to meet demand, prices plummet. This sensitivity to supply is arguably the weakest aspect of the energy sector but right now it is actually being benefitted by the Fed. With capital costs getting so expensive companies are hesitant to take on capital intensive projects such as drilling new wells.

Real estate is similar. When occupancy is in the mid to high 90s landlords have the power. They can charge tenants aggressive rent and the tenants will pay. However, real estate starts to suffer when it becomes oversupplied. Like energy, this is often the source of bad periods in the real estate market. Developers get a bit overzealous and flood the market with too many new properties. However, this too is largely curbed by the Fed activity. With capital tight, new construction has largely dried up. There are some projects that were already in the pipeline, but new starts are at a trickle. To justify development at today's cost of capital, one needs a massive IRR on the project.

The opportunity

The market seems to be entirely focused on the cost side of what the Fed is doing. Interest expense is going to be much higher in 2023 than it was in 2022 and that is a big reason why so many sectors are looking at lower margins.

However, I don't see much focus being put on the impact the Fed is having on supply. Tighter capital conditions are going to materially reduce new supply. This part is bad for the consumer, but great for any company with which the new supply would compete. I think the outperforming sectors going forward are those which are inelastic with respect to demand and sensitive to competing supply which is going to be reduced.

For further details see:

2023: A Year Of Expenses