VRRM - 2023 Mid-Yr Reflections

2023-07-23 21:22:28 ET

Summary

- Manole Capital Management's mid-year 2023 reflections.

- This yr has been driven by large-cap tech companies (the "Magnificent Seven"); Alphabet/Google, Amazon, Apple, Facebook/Meta, Microsoft, Nvidia, and Tesla.

- AI is today's popular buzzword, but we aren't momentum investors or market timers.

- Instead, we focus on our disciplined investment process, philosophy, and strategy.

- Manole Capital's performance was led by Verra Mobility, FLEETCOR, Verisk, CrowdStrike, and Moody’s, while Schwab, Nasdaq, and cell tower REITs were detractors.

Manole Capital Management

Mid-year Reflections

July 2023

We've been active on the research front, with notes on topics like Senator Durbin's credit card legislation, the March banking crisis and the CFPB's attack on late fees. We have already published our 1st and 2nd quarter investor newsletters, which can be read on the Seeking Alpha website. Considering that we're already halfway through 2023, we thought it might be helpful to provide some mid-year reflections.

Expectations:

We saw this Zacks Research table showing "feared outcome versus actual outcome" and thought it was interesting. The worries for 2023 were sizeable, but the results and market responses have been manageable.

| Feared Outcome |

| Actual Outcome |

| Regional Bank Contagion / Financial Crisis |

| Fed intervenes with the emergency lending facility, depositors made whole; JPMorgan intervenes to buy First Republic; banking system remains stable. |

| U.S. Debt Default / Credit Downgrade |

| Congress and the White House reached a deal to extend the debt limit through January 2025. |

| Housing Collapse |

| Housing prices fall, but not precipitously; demand for new homes remains stable. |

| U.S. Economic Downturn / Recession |

| The U.S. economy grew and added jobs in the first half of 2023. |

Stock Performance 1 st Half of 2023:

On a relative basis, companies with free cash flow and those with legitimate valuations (i.e., P/E's or P/FCF, not sales multiples) fared better last year. Instead of just concentrating on value or growth profiles, we prefer to focus on free cash flow and high-quality FINTECH companies. Regardless of what type of environment we encounter, we believe the traits of companies with these characteristics (click here) should outperform. As Warren Buffett preaches, true wealth is not built overnight. It is often built upon a commitment to a value additive process, that often ignores today's day-to-day and short-term market noise.

Last year's best performing and darling sector was Energy, which rose +41.1%. So far this year, the Energy sector is down (5.5%), and it is the second-worst performing of GICS 11 different sectors. 2023 has been a great year for contrarian investors, especially if one adhered to a program of buying last year's biggest losers. The 50 stocks that fell the most last year (in the S&P 500), fell by an average of (31%). These 50 stocks are up a startling +56% this year.

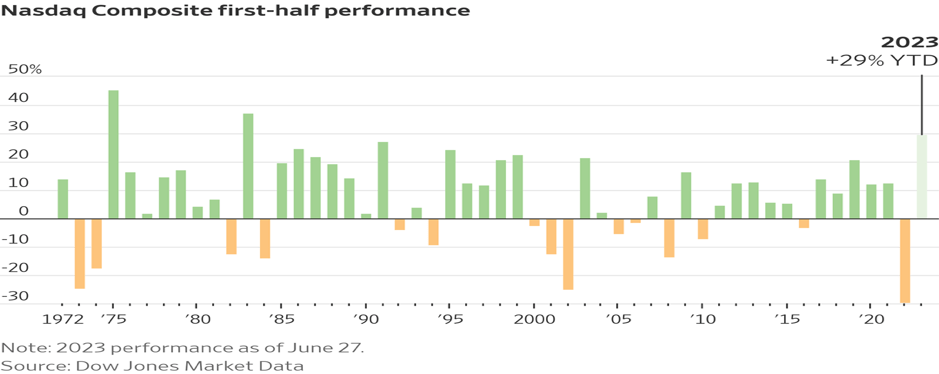

Midway through 2023, we are seeing some clear trends driving performance. While the S&P 500 is up +16.9% this year, it is significantly being pushed higher from only a handful of large, mega cap technology companies. This year, nearly all of the market's total performance is driven by the "Magnificent Seven" stocks of Alphabet/Google, Amazon, Apple, Facebook/Meta, Microsoft, Nvidia, and Tesla. These specific names are up an average of +79% and are contributing to near record levels of concentration. The Nasdaq is up over 31.6%, which is the best first-half performance since 1986. So far this year, the S&P500 IT sector is up an impressive +40.3%.

Looking at this chart from Dow Jones Market Data, one can clearly see that the Nasdaq has been driving overall market returns. In fact, it was the best 1st half for the Nasdaq market since 1983.

Dow Jones Market Data chart (Dow Jones Market Data)

{kind=link}

The "safe haven" trade of 2023 is large-cap, growth names (in technology), especially those that suffered last year. Despite being richly valued (Nvidia trades at 22x forward revenue), these tech companies generate excellent free cash flow, have strong balance sheets, and represent a significant percentage of the S&P 500 (i.e., they can easily be owned by fund managers).

As a market capitalization index, the S&P 500 disproportionally weighs larger companies. The top 5 companies in the S&P 500 now account for nearly a quarter (24.1%) of the entire index. The Nasdaq 100 index is set to adjust the weighting of its 100 components, with the "Magnificent Seven" accounting for more than half that index's weight. Due to this heavy concentration, we will get a 1x, special rebalancing of the Nasdaq 100 index on July 24th to reduce the weights of its largest holdings. There is clearly an over-concentration in these indices, that requires special attention by its gatekeepers.

Manole Capital:

We try our best to understand macro crosscurrents but spend the vast majority of our time on doing bottom's up, fundamental research. We build proprietary models and do deep-dives into the catalysts specifically impacting our companies. We will leave the projections, estimates, forecasts, and predictions to others. Instead, we'll spend our time reading and pouring over company data and presentations.

Year-to-date 2023, our public portfolio performance was led by Verra Mobility ( VRRM ), FLEETCOR ( FLT ), Verisk ( VRSK ), CrowdStrike ( CRWD ) and Moody's ( MCO ). Detractors this year have been Schwab ( SCHW ), Nasdaq ( NDAQ ) and our cell tower REITs. During the second quarter, we were helped by AvidXchange ( AVDX ) and Mastercard ( MA ). We have a modest position in AVDX, but it climbed nicely, up +33%. Mastercard's contribution was positive, as it remains a large position for us, and it was up +8.5%.

Today's market is seemingly ignoring items like profitability, dividend growth, real valuations, and free cash flow. Instead, the market is focused on momentum and enticing buzzwords. However, chasing performance can be dangerous and isn't something we will entertain.

The Latest Buzzword:

This year, we have seen two very different sides of the investing coin. We have experienced wild enthusiasm for AI, as well as panic during March's bank run and volatility. Through both of these different environments, we have remained steadfast in our disciplined investment process. Certain strategies can move in and out of favor, but we are not market timers. We exclusively focus on the emerging FINTECH space and prefer to stick to our long-term investment philosophy.

Some investors chase today's "hot dot" and are enticed by the allure of new buzzwords (machine learning, NFTs, blockchain, the internet of things, big data, web3, chatbots, and now AI). We are quick studies and try out best to learn about new technologies but choose to be patient and conservative.

We understand that topics like Bitcoin and digital currencies might have seemed attractive in 2019, but we prefer to understand what drives their innovation - i.e., the blockchain. In our opinion, the blockchain and a decentralized and open-architecture ledger is much more powerful of an advancement, than another currency to use at Wal-Mart or Target. If you want to understand our perspective on digital currencies, read our published notes on Seeking Alpha from 2017 and again in 2021.

According to a recent Coinbase research report, since the start of 2020, over 50% of Fortune 100 companies have pursued cryptocurrency, blockchain or web3 initiatives. We believe that great businesses adapt and change. For example, back in 1999 and 2000, those that embraced the internet initially thrived. However, over the last couple of decades, every company has become an internet company, right? Looking back to the dot.com era, certain darlings of that era struggled for an entire decade. From March of 2000 to March of 2010, names like Microsoft (down 32%), Cisco (down 66%), Intel (down 61%) and Oracle (down 34%) struggled, while the overall market thrived.

If you take a look at a Cisco chart (during this time period), you will understand our point. While Cisco's earnings steadily grew, the stock was flat for a decade afterwards. From 1999 through 2007, Amazon's stock was down, despite growing revenue by 7x. These weren't bad businesses, but they were generally overpriced and just too expensive. As we are reminded of regularly, "investing is a marathon, not a sprint."

A few years ago, companies that mentioned the blockchain were considered early pioneers of a game changing technology. However, now blockchain technologies have broadened out and been adopted by hundreds of forward-thinking companies. These types of technology shifts can seem scary at first, but often lead to material cost saves and years of productivity gains. We envision a similar path for AI and other business applications, not for a few companies, but for hundreds.

Conclusion:

In mid-March, the market absorbed a volatile banking crisis, which led to some large bankruptcies and fire sales. Some blame for these failures should be assigned to poor internal risk management, while another aspect can be attributable to the large increase in interest rates. In late June, all the major banks (23 of them) cleared the Fed's annual stress tests. According to the Fed, these banks would be able to successfully withstand a severe recession without disrupting critical individual and corporate lending activities. Despite $541 billion in projected losses, these banks were deemed "properly capitalized".

Despite what one hears on CNBC every day, the economy remains quite strong. GDP in the first quarter was +1.3%, but the Department of Commerce and The Bureau of Economic Analysis just revised its prior estimate to +2.0%. Expectations for the 2nd quarter are now at a solid +1.9%.

Earlier in the year, most pundits were calling for a recession, but those fears seem to have abated. The hard landing or looming recession has not appeared. While there are plenty of issues to be concerned with, we remain impressed with the US consumers' resiliency. With a gainfully employed workforce, the US consumer continues to spend. The Fed is wrestling with a convergence of data between weaker inflation readings, an extremely strong jobs market, and modestly slowing consumer spending.

We believe we are properly positioned to succeed in the 2nd half of 2023 and beyond. We hope you have a wonderful summer, and we look forward to speaking with you soon.

Warren Fisher, CFA

CEO & Founder

Manole Capital Management

For further details see:

2023 Mid-Yr Reflections