WMB - 2024: Light At The End Of The Tunnel

2023-11-30 09:51:26 ET

Summary

- 2023 has been choppy with multiple market disrupters, high inflation and high interest rates.

- The Federal Reserve is on track to achieving a soft landing but it will take some more time. The second half of 2024 will see lowering interest rates in my view.

- I present four stocks, two REITs and two midstream energy companies, that will benefit from the shift in economic policy and market drivers during 2024.

2023 has been an interesting year in which I would use the term "choppy" to best describe it thus far. The year began with declining energy prices as the world's energy markets rebalanced following the outbreak of the Russian-Ukraine conflict. In march, three banks defaulted in the aftermath of a run on Silicon Valley Bank. All the while, the effects of inflation have gripped American homes making everything from essential goods to luxury items more expensive.

As the calendar turns to 2024, investors should be prepared for more of the same... at first. I believe the second half of 2024 will open up opportunities for those who are prepared with long term vision.

How We Got Here

Knowing how you got to where you are is as import as knowing where you are going. At the beginning of 2023 we heard ad nauseam of the impending recession. The federal reserve had no chance of achieving the "soft landing" it desired and the conversations were about WHEN a recession would happen, not IF. This talk is a result of two things.

1. Not understanding how long it took to create the problem.

2. Not understanding how long it will take to fix the problem.

Inflation originally was spurred on by the COVID pandemic combined with low interest rates and economic stimulus policy that was enacted at the time. As the world settled and the initial shock to employment subsided, inflation soared. Cheap borrowing costs and excess cash coupled with inventory shortages allowed inflation to escalate to 40 year highs over an 18 month period. To address misunderstanding #1, the problems with the US economy took 18 months to fully manifest into something measurable.

The Federal Reserve responded early in 2022 (almost a full year after inflation began rapidly increasing) by progressively increasing the interest rates on federal funds in an effort to pull the chord on the parachute and achieve a soft landing.

Now it's time to address misunderstanding #2. The last time you fixed something at home, did it take longer to break it or to fix it? Fixing things takes time, dedication, and care. To the credit of the Reserve, Jerome Powell has consistently given the message that the fix would not be quick, and it would not be painless. What we have seen thus far is continuous pressure to bring the economy back under control slowly.

This is where expectations of the general public do not match up well with reality. The general public demands immediate results. However, if you want the pilot of your airplane to achieve a soft landing, should he or she put the plane down quickly or slowly?

The US economy is almost there, with the landing gear just a few feet above the tarmac. Inflation has steadily fallen from peak levels, and unemployment has begun to creep upwards. Both of these are the key indicators the Federal Reserve desired to see to provide analytical evidence it had tamed the beast that was inflation.

With the job still not complete, the first half of 2024 will continue to be a high interest rate environment. As the cumulative effects of the interest rate parachute continue to build, the economy may finally start to show its first signs of weakness since the pandemic. While no one wants to have a weakening economy, it will be the necessary ingredient to allow the federal reserve to finally start lowering interest rates.

When this finally happens, what will it mean for stocks and how should investors prepare?

1. Buy Real Estate While It's Still Cheap

The REIT sector has gotten hammered as a result of concerns that future growth will be limited by higher interest rates. Higher interest costs reduce the spread between rental income and the financing costs to acquire new properties. This is a valid concern and growth will slow accordingly. However, history shows that this is now the opportunity to buy REITs at an inherent discount to future valuations.

For my REIT case study, I have selected both Realty Income ( O ) and NNN REIT ( NNN ). Both companies operate their properties under the triple net lease business model. This lease structure results in the tenant paying for the majority of the operating costs of the building including the property taxes and maintenance. O is the big fish in the space with a market cap of $39 billion, while NNN is significantly smaller at $7 billion.

Both O and NNN are dividend aristocrats, increasing their dividend since 1998 and 1995 respectively. The trend below compares the yield of O and NNN since 1998 in comparison to long term interest rates. Discounting the market shocks of 2008 and 2020, high interest rates have led to pressure on the share price to drive up yields. As rates decrease, yields follow, indicating share price appreciation in anticipation of future growth.

Refining our time frame to just the last decade's price performance shows significant share price appreciation as interest rates declined in both the 2014-2016 and 2018-2020 time frames. This graph also shows the inverse behavior occurring thus far in 2023 and represents an opportunity to invest in both of these REITs at a discount prior to the federal reserve lowering interest rates. Under the thesis that rates will spur prospects for future growth, both O and NNN should realize material share appreciation. I rate both O and NNN as buys with their share prices severely depressed toward multi-year lows.

2. Take The Guess Work Out of Energy

Energy is what makes our world move. From cars, to computers, to iPhones, it all requires energy of one form or another. As the overall activity of the economy slows down as a result of global governments taking a restrictive stance on fiscal policy, consumption of energy will follow suit. To combat this bearish thesis for energy, OPEC+ has made a coordinated effort to reduce global output and create a price floor of $80/barrel.

The notion of creating a price floor doesn't strike a bullish tone for energy investments. Even though crude always makes the headline news, one commodity does not paint the entire picture for the energy sector.

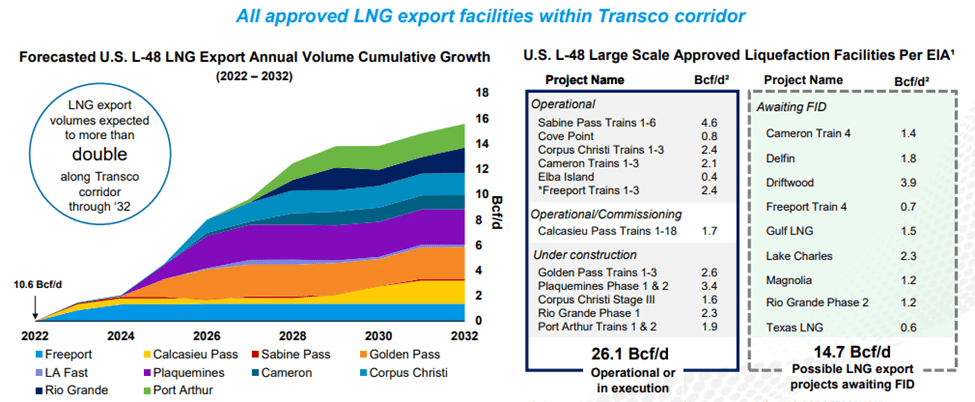

One of the most glaring results of the Russian-Ukraine conflict is the dynamic shift of natural gas supplies to Europe. Europe is more heavily reliant on the US for natural gas supplies than ever before. Accordingly, natural gas liquefaction capacity is scheduled to double as new terminals come online starting in the second half of 2024. These LNG terminals will provide invaluable outlets for cheap US natural gas to be sold internationally.

LNG export growth (WMB Investor Presentations)

{kind=link}

Take notice to the reference to the second half of 2024. Coincident with declining interest rates (which will spur additional economic activity and energy consumption), the natural gas export market will be positioned for massive growth. This creates both domestic and international demand drivers for natural gas markets.

The average investor may flock to commodity producers under these conditions. However, natural gas prices are even more volatile than crude oil, spiking over 240% since 2021. Investors should be selective to balance the risk of commodity exposure with benefits to this bullish play on the commodity. The midstream sector is the ideal play for this role and is the real estate equivalent for the energy industry.

Companies in the midstream space utilize capacity on pipelines, treatment plants and compressors to transport natural gas from the well head to customers around the country and the world. The beauty of this business model is that it has very little commodity exposure and is structured on fee-based and take-or-pay style contracts. Similar to the real estate industry, if the pipes are full, the owners are getting paid regardless of what the commodity price is. These stocks give energy exposure with limited risk to commodity price fluctuations.

Kinder Morgan ( KMI ) and The Williams Companies ( WMB ) stand out from the pack for capitalizing on increased natural gas volumes both nationally and globally. Both of these companies were featured in my LNG export series which can be referenced for a deep dive into the LNG industry.

One of the most redeeming qualities of these companies is their resiliency during market disruptions. Both KMI and WMB grew FCF per share during the COVID pandemic and increased their respective dividends. Not many businesses can match that claim and is a testament to the stability of take-or-pay contracts. KMI and WMB payout a dividend yield of 6.5% and 4.9% respectively.

As volumes increase due to natural gas exports and increased domestic consumption from economic expansion, both firms are situated to increase volumes because of their unparalleled infrastructure network. I have projected that the operational advantages of both KMI's and WMB's assets will allow the companies to increase earnings by 6% and 5% respectively due to LNG exports alone. This earnings expansion will drive continued dividend growth that has been on track since 2017.

I rate both KMI and WMB as buys with macro tailwinds and multiple organic growth projects under construction.

Summary

2024 will start out very similar to how 2023 ends with high interest rates creating economic pressure on the US economy. To this point the economy has bent but has not broken thanks to robust employment. However, this strength is beginning to show some cracks as unemployment creeps higher. This is the essential ingredient the Federal Reserve desires to see to begin the moderation process and reduce interest rates.

That driver will enable REITs to realize multiple expansion as growth prospects return. Coincidentally, economic growth tied with reduced interest rates and LNG export terminals coming online will spur increased volumes on natural gas pipelines thus leading to enhanced earnings in the midstream space.

This investment thesis requires patience and forethought. Investors will be rewarded as they wait with the four stocks I have presented here. O, NNN, KMI and WMB are all high yielding stocks with moderate dividend growth that have upside in the back half of 2024. Investors should be patient as there is light at the end of the inflation tunnel.

For further details see:

2024: Light At The End Of The Tunnel