RBLX - 2024 Rate Cut Playbook: My Top 4 Ideas To Ride A Dovish Fed

2023-12-26 16:17:45 ET

Summary

- 2024 expected to be a bullish year for stocks with Fed rate cuts and double-digit earnings growth for the S&P 500.

- This bullish backdrop recently prompted me to raise my base case target price for the S&P 500 to ~5,300 points by end of year 2024.

- Zooming in on specific ideas, Citigroup, Roblox, Microsoft, and Stellantis identified as attractive stocks to benefit from the dovish Fed pivot.

2024 is poised to be an exciting year for stocks, with the Fed expected to cut rates by nearly 175 basis points, while consensus earnings growth for the S&P 500 (SP500) bucket is expected only slightly below double-digit rates YoY, according to data collected by Refinitiv. This bullish backdrop recently prompted me to raise my base case target price for the S&P 500 to ~5,300 points by end of year 2024.

Following the FOMC projection release on 13 December, traders went all-in to price six cuts worth of 25 basis points each for 2024, suggesting rates could fall to about 3.5% . This is a major paradigm shift in macro, and investors are right to reprice valuations across asset classes, notably bonds and equities ...

... Specifically for equities, I am confirmed in my bullish projection that the S&P 500 is poised to close the 2024 with positive returns. Specifically, with earnings growing at nearly double-digit rates year over year and interest rates projected to dip towards 3.5% based on a CPI below 2% year over year, I posit that the US equity benchmark should reasonably be priced around a 23x multiple .

Zooming in on my bullish equities view, there are a few names that stand out as particularly attractive, poised to enjoy an oversized benefit from the pending rate cuts. In my view, the most promising stocks to ride the dovish Fed pivot are Citigroup (C), Roblox (RBLX), Microsoft ( MSFT ), Stellantis (STLA), and KKR Real Estate Finance Trust Inc. (KREF). In this article, I discuss these names in more detail.

Citigroup: Cheap Valuation Meets Macro Tailwind

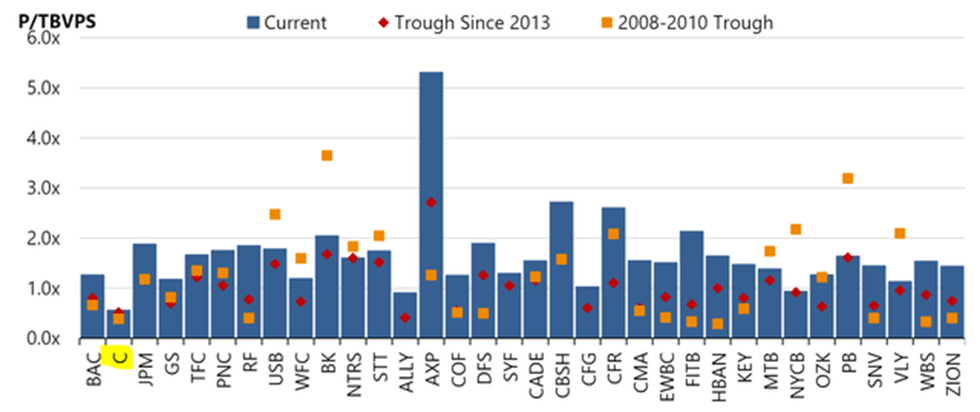

In 2023, bank stocks faced tough times, driven more by sentiment than fundamentals. Specifically, the failures of Silicon Valley Bank and Credit Suisse prompted concerns about rate cycles, leading to industry-wide low trading multiples akin to those during the Great Financial Crisis. Citigroup's stock, for instance, is at 0.6x P/TBV, comparable to past troughs, as highlighted in a Morgan Stanley research note.

{kind=link}

Looking ahead to 2024, sentiment seems set to improve as monetary policymakers gear up for substantial rate cuts. In that context, cheaper rates could positively impact bank stocks in several ways: Firstly, I point out that equity multiples in general are inversely related to rates. Secondly, there is supportive interest income upside, as lower rates both reduce interest income risks as well as stimulate credit demand amid economic activity upticks. Thirdly, lower rates are bullish for Citigroup's investment banking franchise, boosting activities in ECM, DCM, and M&A.

On top of the macro tailwind, I note that Citigroup looks set to materially improve its idiosyncratic business fundamentals. According to the latest commentary of Citi CFO Mark Mason, the bank is poised for a 4-5% CAGR topline CAGR over the next 3 years on a falling operating expense base, potentially achieving a 10-11% ROTE by 2026. Thus, C stock looks certainly poised for a multiples re-rating in 2024.

Roblox: Business Quality Overpowers Valuation Concerns On Lower Rates

Roblox stands out as perhaps the most exciting growth platform listed on the public markets. Like YouTube, the platform leverages an expansive user-generated content model, offering limitless creative possibilities to its vast community of developers and users. On that note, Roblox holds significant growth prospects in areas like international expansion, AI, and advertising monetization, potentially achieving a topline CAGR of >20% annual growth through the next few years.

But while Roblox's growth potential has been well acknowledged by many investors, the upside has recently been overshadowed by valuation concerns. Specifically, at 4-5% 10-year treasury yields is very hard to justify an investment in a long-dated growth asset like Roblox -- independent of the company's business quality. Now, as rates are set to decrease sharply, Roblox implied 8x 2024 forward EV/Sales should become more manageable for investors. In fact, in 2024, I expect valuation concerns to gradually fade, giving investors room to focus more confidently on the company's strategy roadmap covering platform internationalization, AI, and advertising.

Microsoft: Attractive Growth, With Well-Moated Business Model

The argument for Microsoft is very similar to the argument presented for Roblox: Lower rates render Microsoft's rich valuation less dangerous for investors. However, contrasting to Roblox, Microsoft's growth outlook is less speculative and more protected by business model that has outperformed the market for decades. Specifically, Microsoft's growth outlook enjoys robust protection due to several key factors: First and foremost, the software giant's product portfolio spans across multiple sectors, including cloud computing, software, hardware, and services, which mitigates risks associated with dependence on a single market segment; Secondly, the company's strong foothold in the cloud computing arena, particularly with Azure, positions Microsoft favorably amidst the accelerating shift to cloud-based solutions; Thirdly, Microsoft is poised to capture perhaps the largest share of enterprise software growth upside that is expected to be catalysed by AI, citing the company's collaboration with ChatGPT and development Copilot for Microsoft 365. That said, analyst consensus estimates are pricing 2024, 2025 and 2026 earnings growth of 14%, 15% and 18% YoY, respectively.

{kind=link}

Stellantis: 6.3% Dividend Equity Yield With Upside

Lower rates are cutting into yields for fixed income securities, rendering the dividend cash flow from equities more valuable. In that context, Stellantis stands out as an interesting pitch. The company is currently trading at a P/E of around 3.5x, with a proud $24.9 billion of net cash .

Reflecting on such a cheap valuation, it is suggested that Stellantis is facing earnings pressure/ risk. But personally, I do not agree with this narrative. In my opinion, Stellantis' earnings resilience is bolstered by the company's leading economies of scale, evident in its industry-best fixed cost base, coupled with a stellar track record of management execution. Moreover, Stellantis' revenue stream is largely shielded from price wars and margin pressures, predominantly driven by its robust segments in SUVs, pickups, and commercial vehicles, which account for the majority of its revenue.

According to my projections, Stellantis should be very comfortable paying 2023-like dividends in 2024 and beyond ( $4.7 billion , 6.3% dividend yield). In fact, there is likely material upside to the current equity distributions, either in form of dividends or share buybacks. I point out that even without any earnings power, Stellantis' net cash position would cover about 5 years of dividends. On that note, Stellantis' well-protected equity yield contrasts attractively with 2024 forward rates of around ~3.5%.

A Note On Risks

While I hold a positive outlook on equities heading into FY 2024, it's crucial to acknowledge the (general) risks associated with investing in stocks, particularly considering the still uncertain macroeconomic backdrop. In my opinion, there are three key risk factors that warrant attention: Firstly, for 2024, there remains a notable probability of a mild recession in the U.S., which would influence the earnings of companies, including Roblox, Microsoft, Citigroup and Stellantis. Secondly, fluctuations in specific industries can skew relative attractiveness of certain stocks, exposing it to sector-related risks. Currently, there might be an overreliance on major technology companies within the S&P 500, potentially exposing Roblox and Microsoft to valuation risk. Secondly, stocks in general are inherently prone to volatility. This volatility may not align with every investor's emotional tolerance, posing a challenge for those seeking stability or with lower risk tolerance. For the four stocks covered, I view Roblox most exposed on volatility, while Stellantis should be least exposed.

Conclusion

In summary, the anticipated rate cuts set the stage for a promising year for equities in general, and a select set of stocks more specifically. In that context, I am very bullish on Citigroup, Roblox, Microsoft, and Stellantis, which all stand out as strong investment candidates, each poised to leverage the favorable macro environment in their unique ways.

For further details see:

2024 Rate Cut Playbook: My Top 4 Ideas To Ride A Dovish Fed