ME - 23andMe Looking Promising For The Long Term

Summary

- 23andMe has made many strategic acquisitions that have helped the company expand and grow.

- The genomics industry as a whole is expected to have rapid growth in the future due to the convenience of testing kits as well as the decreased prices.

- ME stock has invested a lot into research and development, which puts it in a strong position to continue growing and innovating its products.

Investment Thesis

23andMe ( ME ) has shown to be a viable growth prospect with its broad reach of customers and its trusted brand name. Despite some financial discrepancies and tough competition in the genomics testing space, 23andMe is positioned well to continue growing in the next five to six years through constant R&D as well as strategic investments/acquisitions.

Business Overview

23andMe Holding Co. is a healthcare company that is focused on genetic testing. It operates in two segments: Consumer and Research Services and Therapeutics.

The Consumer and Research Services

The Consumer and Research Services segment is again broken down into three different subsections: the Personal Genome Service ((PGS)), the telehealth business, and the research services. The personal genome service consists mainly of direct-to-consumer genetic testing kits, which give consumers unique and personalized information about their ancestry, traits, and health risks. A bulk of the company's revenues comes from the consumer and research services, especially from PGS with about 89% of total revenues derived from PGS in the most recent fiscal year.

The telehealth subsection is a way for 23andMe to use the data from the genomics tests to help their patients treat certain illnesses or diseases. A patient can interact with affiliated licensed physicians and if prescribed medicine, the patient can have access to their pharmacy with fact and free delivery services.

Finally, through their research services, the company can use their vast database of genetic information to develop new medicine and treatments to certain illnesses. To help with the research, 23andMe has made a four year collaboration with GSK ( GSK ).

Therapeutics

The therapeutics segment consists of drug development as well as research into different therapeutic areas such as oncology and cardiovascular diseases. Currently, the company is the only consumer genomics testing with multiple FDA authorizations for over-the-counter health status reports and they were the first company to obtain FDA authorization for direct-to-consumer genetic tests.

Also, as of March 31, 2022, two of their research programs have entered into Phase 1 trials, one of which is their proprietary program and the other is the immuno-oncology program.

Industry Analysis

The consumer genomics market is a rapidly growing market with a reported value of $1.9 billion USD in 2020 and it is expected to expand at a compound annual growth rate of 19.4% from 2021 to 2028 . The recent COVID-19 pandemic has boosted the demand for the direct-to-consumer genetic testing kits, but also just the growing presence of rare genetic diseases is expected to drive the growth of the market itself as well as increased public awareness about genomics testing. The direct access to the genomic test results allows users to gain knowledge about their own history and about themselves, which assists them in making changes in their lifestyle to better their health. In addition, the prices of these test kits have gone down, which further increases the demand for them.

Competitive Advantage

Some of 23andMe's biggest competitors in the industry are Ancestry.com, Twist Bioscience Corporation ( TWST ), Invitae Corporation ( NVTA ), and Illumina ( ILMN ). However, with the accumulation of the world's largest genomic database, 23andMe provides the best value at its price. In addition, what separates 23andMe apart from many of its competitors is its partnerships. The company's growth depends on constant scientific development in the genomic space as well as increasing its customer base and it does so by forming partnerships with different organizations such as the Michael J. Fox Foundation for Parkinson's disease. Through partnership deals, the company has agreed to provide free testing kits to members of the organization's patient community and in return, the organization encourages its members to enroll in 23andMe's services. They have also secured additional partnerships with famous academic institutions such as the Broad Institute at MIT and Harvard and Stanford University. By forming strategic partnerships with name companies and learning institutions, 23andMe has established itself as a trustworthy genomics testing company and has increased its brand awareness, helping to boost its customers and sales.

Growth Prospects/Opportunities

Product Development

The success of the company and its subscription model depends not only on acquiring new customers but also retaining existing customers and members. This could be done through product enhancements and new product offerings to provide more information for the customer and make it more personalized. This would increase the number of engaged customers who purchase the product.

Acquisitions

Another growth opportunity for 23andMe is strategic acquisitions. In the past two years, 23andMe has acquired Lemonaid Health, a telehealth company. This allows the company to integrate its personalized genomic testing services more deeply into primary care. This now not only helps customers to learn something about themselves, but also to apply what they learned about themselves to their lives and their healthcare. This opens up the door to allow the use of genomic testing to help prevent and also better manage diseases.

Category Expansion

To grow their customer base, the company also has the opportunity to expand past genomics testing into other categories, which can increase the number of people whom they can provide their products and services to. However, expanding into new categories comes with research and development costs, marketing costs, as well as customer acquisition costs. Although a promising opportunity, if the company does not generate enough revenue to cover its costs, it may not recover its financial investments into category expansion.

Financials

yahoo finance

When looking at the revenues, we can see that they have been relatively stable, with slight fluctuations in the past few years. Though 23andMe has a negative operating income, a big portion of their operating expense comes from research and development. The company has recently been putting more into R&D which shows that they are in a good position to continue growing and developing their product offerings in the future. We can also see that 23andMe has a big percentage of their assets in cash, about 48%, compared to 19% from Invitae and 16% from Illumina. This may be a sign that the company is not using all of its cash in the most efficient way. Instead of keeping all that cash on hand, they could be using more of it to invest back into the business.

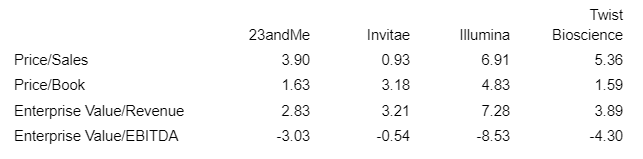

Valuation

{kind=link}

Due to the negative earnings and free cash flow of 23andMe, it's hard to narrow down a solid valuation of the company but if we compare some valuation metrics of the company with its competitors, we can see that 23andMe is relatively undervalued.

Per the recent third quarter financial results, the total revenue of the company for the three months ended December 31, 2022 was $67 million which was an increase of 18% from the total revenue for the three months ended December 31, 2021. The main reason for this growth was the increase in consumer service revenue due to the Lemonaid acquisition and an increase in subscription services. The operating expenses only grew 3.22% from $124 million to $128 million for the three months ended December 31, 2021 and December 31, 2022, respectively. And this increase was mainly due to increased salaries from inflation and an increase in workforce from its recent acquisition. This shows that the company is getting more efficient, allowing the company to continue to grow its sales at a fast rate while the operating costs will start to taper. As a result, based on the company's current growth potential from its acquisitions and increased customer base, I believe that the company can become profitable in the next five to six years.

Risks

Competitor FDA Approval

For some time now, the success of 23andMe has been due to their unique product offerings relative to their competitors. They are the first direct-to-consumer genomics testing company to include FDA-authorized genetic health risk and pharmacogenetic reports. The company's competitors have also started to get FDA approval for their own genetic health risk reports which could draw customers away from 23andMe and as a result, negatively affect their business. However, with the constant investments into research and development, I believe that the company will continue to improve and enhance their products and offer new services unique from their competitors.

Production Problems

23andMe does not have any manufacturing capabilities and they do not plan to have their own production facility anytime soon. The company relies on only a limited number of suppliers to manufacture their genomics testing kits. This may pose a risk to the company because they can't control their own production. Although the company maintains good relationships with suppliers, 23andMe cannot guarantee that it will always be able to meet the demand for its products and if in any case, unexpected events such as a pandemic occur, it will negatively affect the sales of the company.

International Economics Risks

Currently, 23andMe operates and distributes their products in the United States, Canada, and the United Kingdom. The company has visions to expand globally and though that may be a very promising opportunity, there will be lots of regulations and costs associated with it. The company does not have adequate experience in international expansion. In addition, there are different regulations, especially in the healthcare industry, in different countries that would increase the risk of international expansion.

Conclusion

I would rate 23andMe a buy rating. Although the stock price is a bit shaky and volatile, when thinking about the long term, the company has high potential to be big in the genomics testing space with its constant development and just the advancement of technology in the healthcare industry. With strategic partnerships, the company will continue to grow and even expand globally, despite the regulations and high costs.

For further details see:

23andMe Looking Promising For The Long Term