NLCP - 3 Specialty REITs You Definitely Should Not Ignore In 2024

2024-01-02 15:51:12 ET

Summary

- REITs offer attractive tax characteristics and higher yields compared to traditional stocks, making them appealing to income-oriented investors.

- Crown Castle, a telecom REIT, has invested heavily in fiber and small cell business, offering potential value for shareholders.

- Equity Commonwealth, an office REIT, has a unique portfolio with a large amount of cash and potential for upside through asset acquisition or liquidation.

- Innovative Industrial Properties is an interesting player in a once "high"-growing market that offers a hefty yield at a good price.

With the New Year now come and gone, investors should take this time to reflect on what opportunities lie ahead for 2024. For many investors, one of the most attractive avenues to explore involves real estate investment trusts, or REITs. In addition to certain tax characteristics that they offer, there is also the benefit that, typically speaking, they pay out distributions that result in effective yields that are higher than what most traditional stocks pay. This makes them particularly appealing for income-oriented investors such as those that are in or near retirement or those who want to bank capital in order to protect against a potential decline in share prices.

As a value investor, I have often struggled with REITs. For starters, they are rarely cheap opportunities. The attractive and consistent cash flows, as well as respectable growth, often means that shares are not all that cheap. They are high quality prospects, however, which is something that should appeal to value investors. And while all value investors differ in their personal preferences, I have historically been distribution-agnostic, preferring instead to focus on total return as opposed to yield.

Having said that, there are three specialty REITs that I have found myself bullish on in recent years. Each firm operates in a niche market and has its own unique characteristics that might be attractive to investors who are looking for that special kind of REIT to jazz up their portfolio. Two of these firms I have rated a "strong buy," while the other has been rated a "buy."

A telecom play

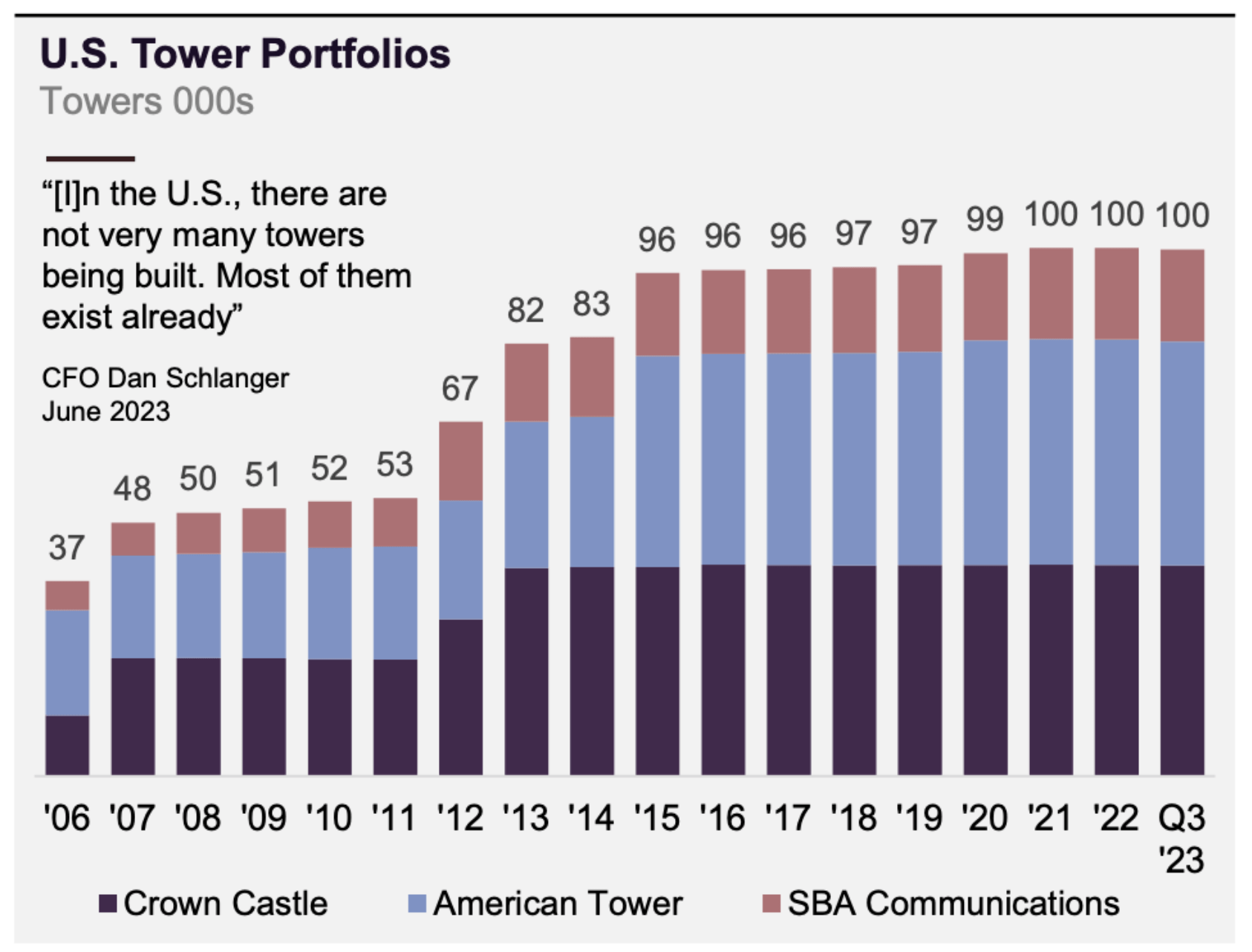

One of the firms that is high on my list in terms of all investment prospects has got to be Crown Castle Inc. ( CCI ). For those not aware, the company is an owner of telecommunications assets, mostly domestic telecommunications towers that it leases out for the purpose of facilitating the transfer of information from any given point to any other given point. Over the past several years, this has become a very mature market when we talk about the U.S. After seeing the number of telecommunications towers grow from 37,000 back in 2006 to 96,000 by the end of 2015, we have seen an almost complete halt in the increase. From 2015 to the present day, we have seen the number of towers in this country grow only slightly to 100,000.

{kind=link}

Seeking out different opportunities, different players in the space decided to tackle different initiatives. The undisputed giant in the market, American Tower Corporation ( AMT ), began growing significantly overseas. Today, only about 47% of its revenue comes from domestic towers, while 45% involves international towers. The rest of its revenue is made-up of data center operations that the company has invested billions of dollars in two. That is a long-term play that is currently not the most profitable. But in the long run, it's likely that data centers will pay off. By comparison, Crown Castle decided to ignore international tower opportunities, instead investing heavily in the fiber and small cell business. Since entering that market, the company has seen its growth slow and it has experienced a great deal of pushback from activists investors.

In fact, last November, I wrote an article detailing how Elliott Investment Management Had decided to come out publicly in favor of making some significant changes, including potentially selling off the fiber and small cell operations of the company. The purpose of this article is not to rehash those details. Rather, I would recommend that you read the aforementioned article. I did conclude, however, that the assessment made by Elliott had significant merit and demonstrated that there was attractive value for shareholders who decided to acquire Crown Castle.

Management seems to be very open to significant changes at this time, as evidenced by the fact that, on December 20th, the firm launched a review process to be conducted by a new committee that will also involve input from Elliott. Regardless of what comes from that, however, the market does seem optimistic about the business. I say this because, since I first rated the company a "strong buy" in early October, shares have generated a return of 25.4% compared to the 9.4% seen by the S&P 500 (SP500).

Given such a large increase, investors would be wise to wonder if I am still as bullish on the company as I was back then. The answer is absolutely. This is the case even though management is forecasting a rather weak 2024 fiscal year. You see, according to management, EBITDA for 2023 should come in at around $4.42 billion. However, higher expenses and other factors are expected to drive this down to $4.16 billion in 2024. Meanwhile, AFFO (adjusted funds from operations) should drop from $3.28 billion in 2023 to $3.01 billion this year.

{kind=link}

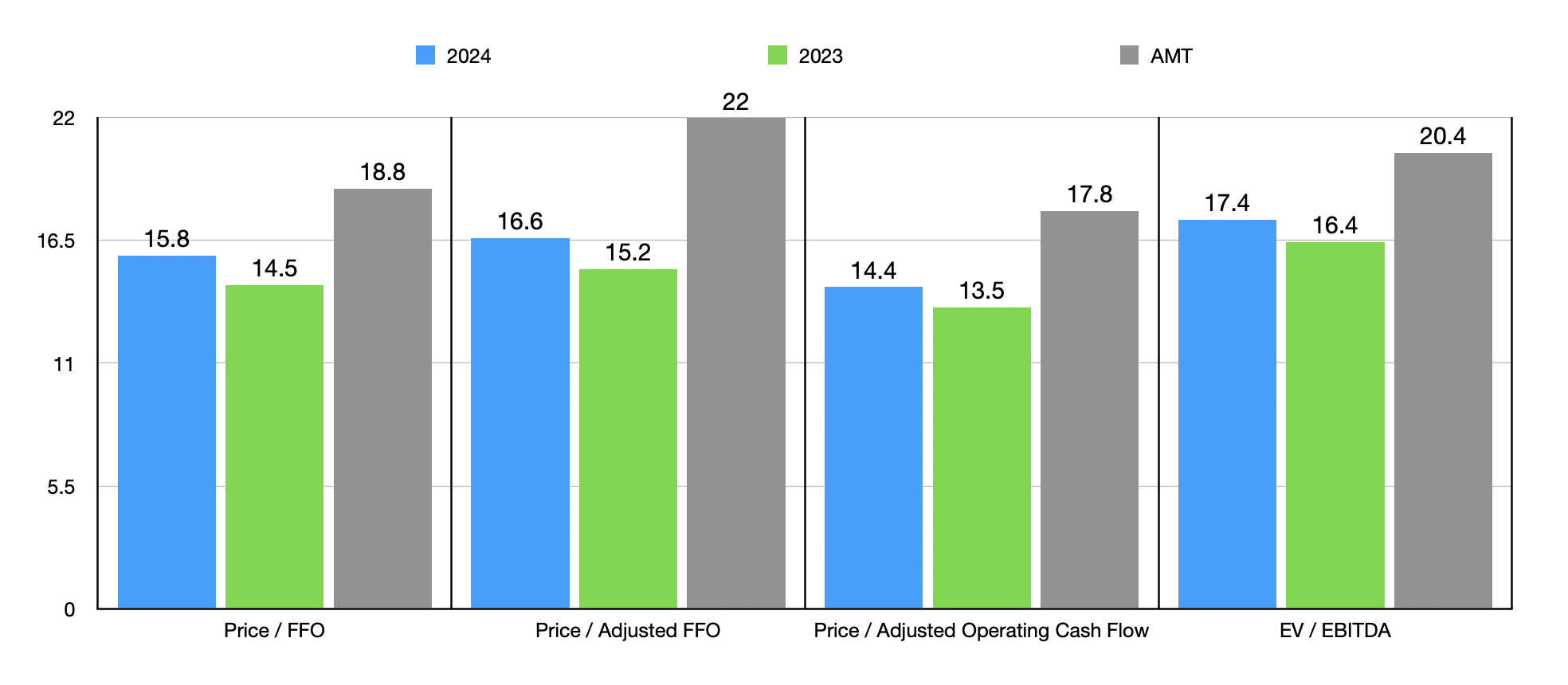

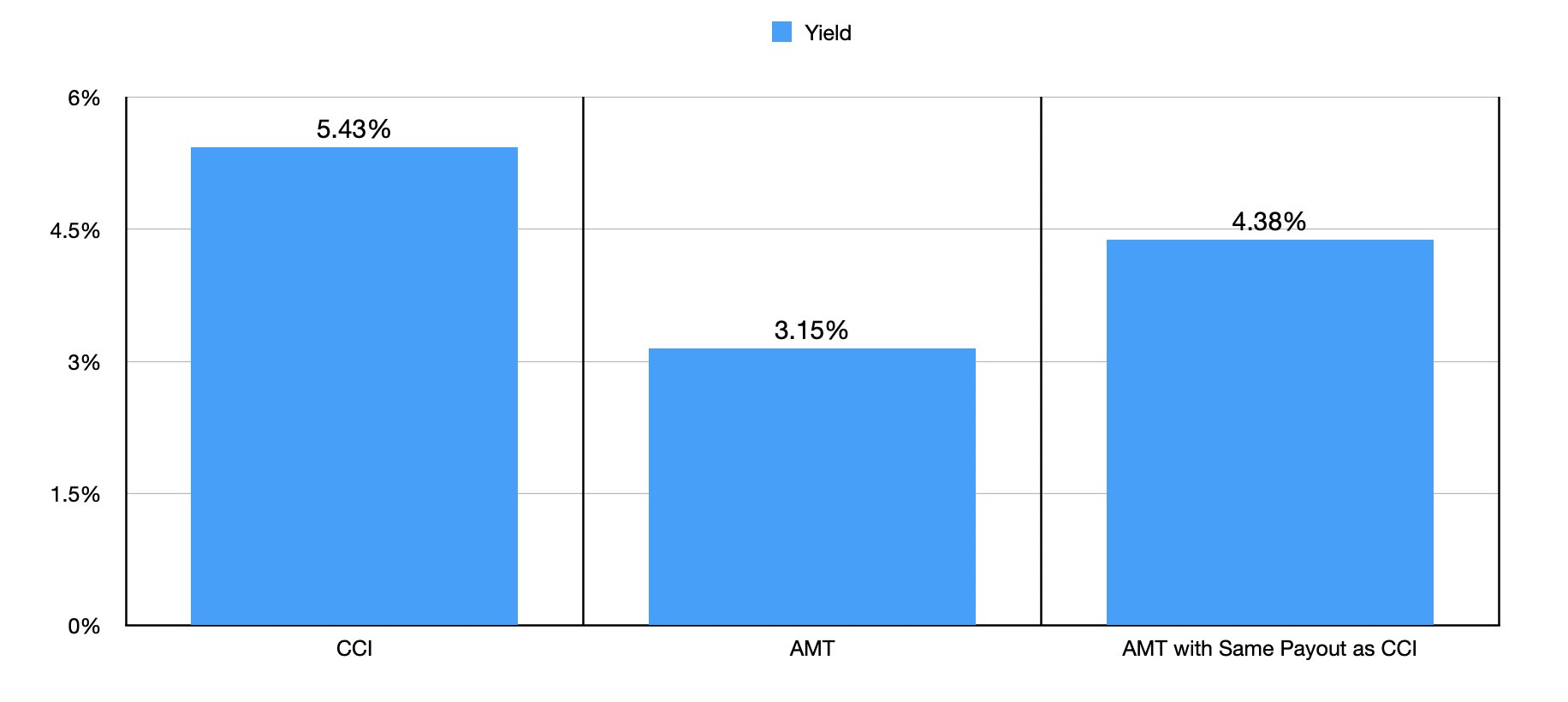

In the chart above, I decided to value the company using these estimates and relying on the assumption that other profitability metrics should drop at the same rate that these should. As you can see, shares are still quite a bit cheaper than what rival American Tower happens to be trading for. Of course, the picture is more complicated than that. There are positives and negatives behind owning shares of either business. Let's look at the topic of yield. If we use the most recent price for each firm, the yield paid out by Crown Castle happens to be 5.43%. That's significantly higher than the 3.15% paid out by American Tower.

{kind=link}

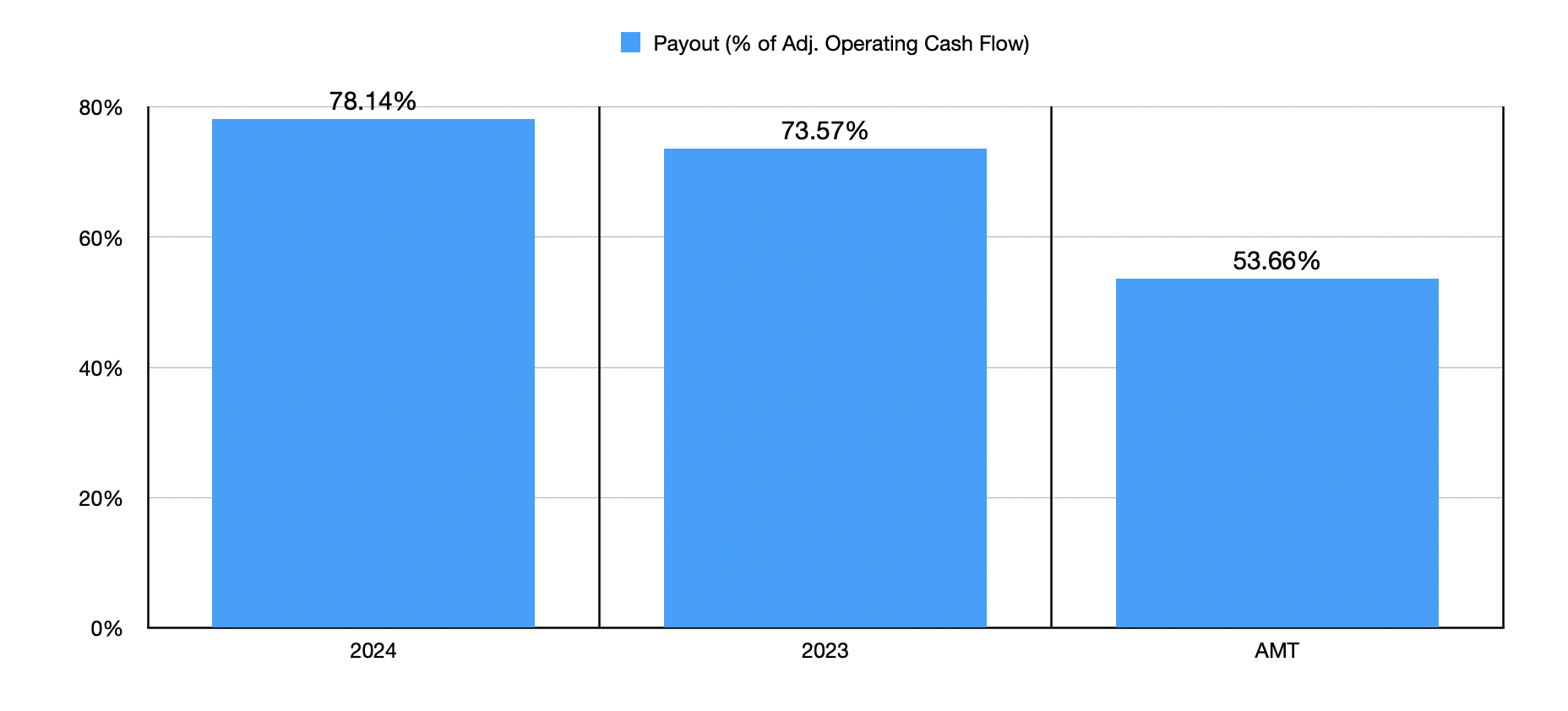

This does require some additional depth, however. If we use the more conservative 2024 estimates, Crown Castle is paying out 78.14% of its adjusted operating cash flow toward distributions. Given that only around $53 million of its capital expenditure budget is expected to involve maintenance costs, subtracting that out from adjusted operating cash flow is more or less irrelevant. This is not an area that requires significant upkeep costs. So almost all of the adjusted operating cash flow produced by the company should be free for distributions, growth, and debt reduction.

By comparison, American Tower is paying out 53.66% of its adjusted operating cash flow toward distributions. This means that it has far more wiggle room than Crown Castle currently offers. But even if American Tower were to increase its payout to match what Crown Castle distributes, and if shares of American Tower were to remain unchanged, its yield would still only hit 4.38%.

{kind=link}

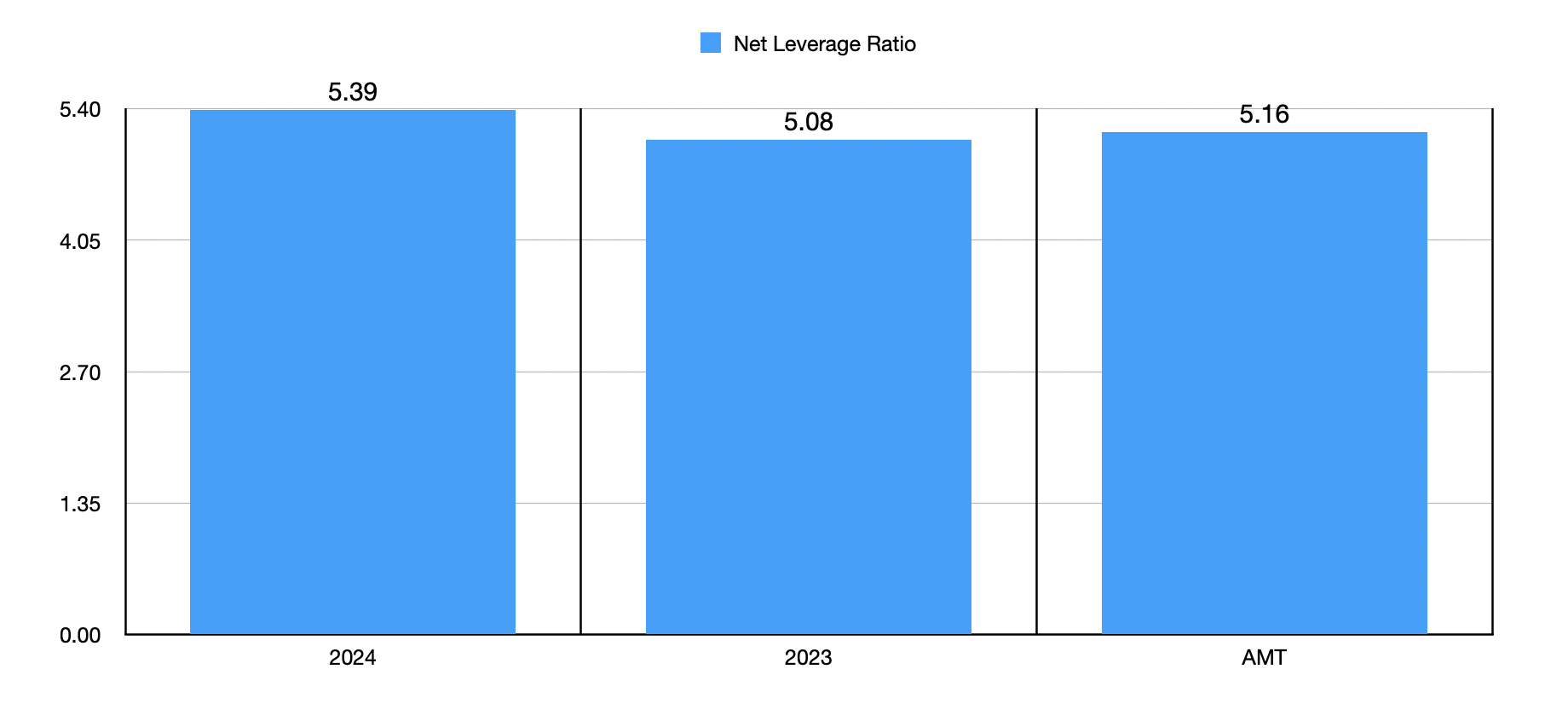

When it comes to leverage, the companies are very close to one another. The net leverage ratio of American Tower is 5.16. If we use the 2023 estimates for Crown Castle, we get a reading of 5.08. And if we use the 2024 estimates, this rises only modestly to 5.39. These differences are, in my opinion, little more than a rounding error. Although the distribution paid out by Crown Castle is more appealing at this time, the one downside that is significant regarding the company is that its distribution growth has been remarkably slow compared to what American Tower has achieved.

{kind=link}

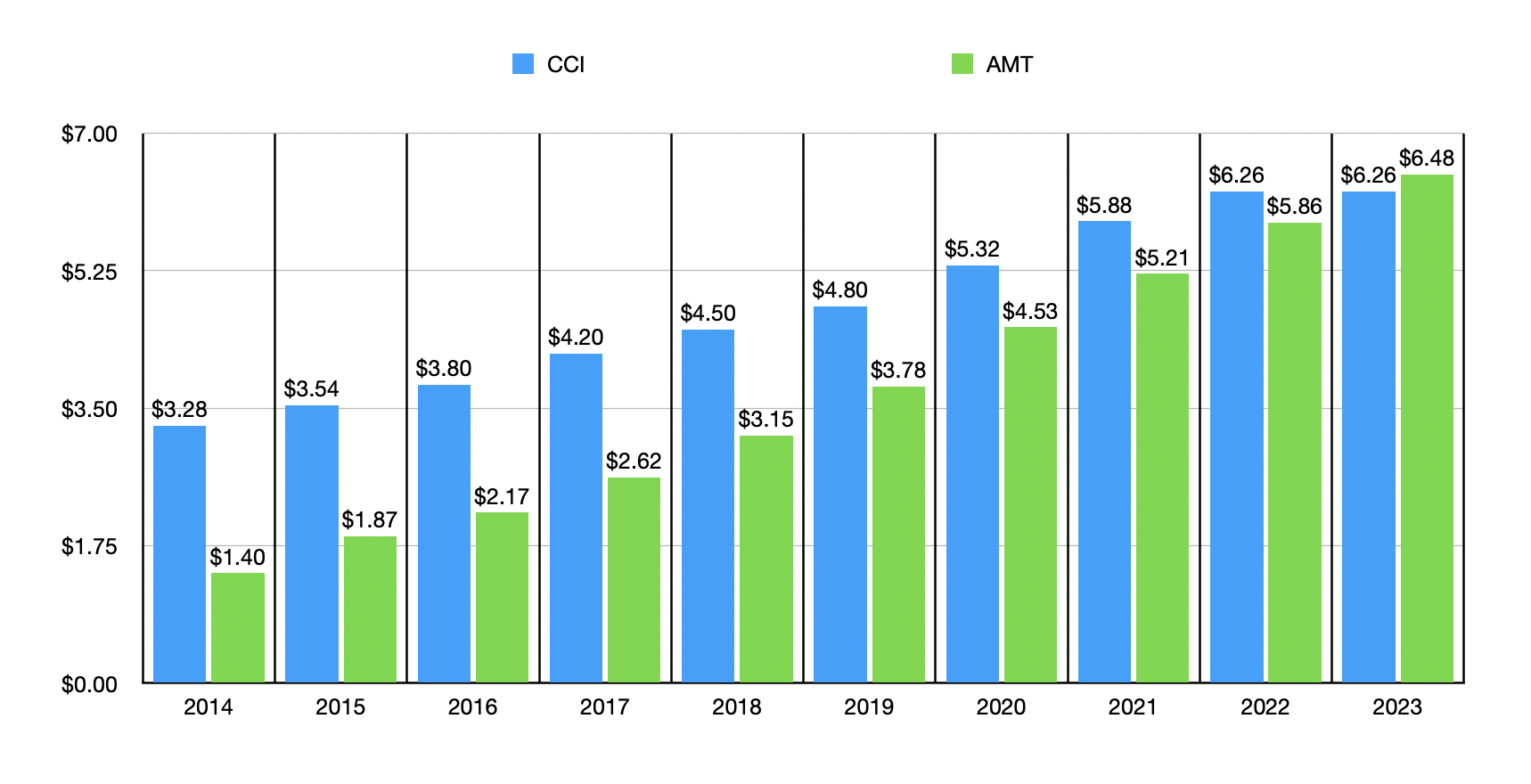

Back in 2014, Crown Castle paid out $3.28 per share each year. By 2022, that number had grown to $6.26 for an annualized growth rate of 8.4%. Over the same window of time, American Tower had seen its distribution grow from $1.40 per share to $5.86 per share for an annualized growth rate of 19.6%. For 2023 through potentially 2025, the management team at Crown Castle has indicated it intends to keep the distribution unchanged at $6.26. By comparison, the effective distribution on an annualized basis for American Tower had grown to $6.48. As the company continues to grow more rapidly than its competitor, we are likely to see continued outperformance on the growth side for the distribution in favor of American Tower. Even so, given how cheap shares of Crown Castle happen to be and the robust distribution currently paid out, not to mention the potential value that could be unlocked from its fiber and small cell assets, I do still prefer Crown Castle even as the stock has risen nicely.

{kind=link}

An office REIT worth considering

Right now, pretty much anything tied to the office space market is considered to be very unattractive. And this is for a very good reason. Even prior to the pandemic, there was a subtle shift away from workers being in the office and instead working remotely. But the pandemic rapidly accelerated this trend and, to some extent, made it likely that we will never go back to the days of office dominance. Regardless of what your views are on this shift, it is a reality that is causing issues for any companies related to the ownership and leasing out of office assets.

Using the most recent data available, for instance, as of November of last year, the vacancy rate of all office assets in this country came out to 18.2%. That's the highest on record. But when you look at utilization rate, the picture is far worse. Even today, with the pandemic long since over, the office utilization rate is hovering at between 50% and 60% of what it was prior to the pandemic.

Ground zero for this pain will likely be any REITs that specialize in the ownership of office properties. However, as I pointed out in an article published in June of last year, Equity Commonwealth ( EQC ) is a different animal entirely. For those looking at the company the first time, the picture will look very different than what a traditional REIT might look like. For starters, the company's market capitalization right now is $2.06 billion. And yet, in the first nine months of 2023 , the firm generated revenue of only $45.4 million. That is materially lower than what you would expect for a company this large. When you start digging deeper, you start to understand why the picture is this way. Over the span of around nine years, management sold off 164 properties and three land parcels, with the properties accounting for 44.3 million square feet. The company ended up bringing in $6.9 billion of cash, plus $704.8 million of stock in another REIT. Today, it now has only four properties in its portfolio that comprise 1.5 million square feet of space.

After paying down its debt to nothing, the company accumulated A tremendous amount of cash. By the end of the 2021 fiscal year, the business had $2.80 billion of cash and cash equivalents on its books. But over time, management bought back common stock in the firm and paid out some distributions. In the first nine months of last year, the business repurchased $60.2 million of common units. That was down, however, from the $130.5 million of purchases reported for the same window of time one year earlier. On the other hand, in February of 2023, management paid out a special distribution of $4.25 per share, amounting to $468.2 million.

{kind=link}

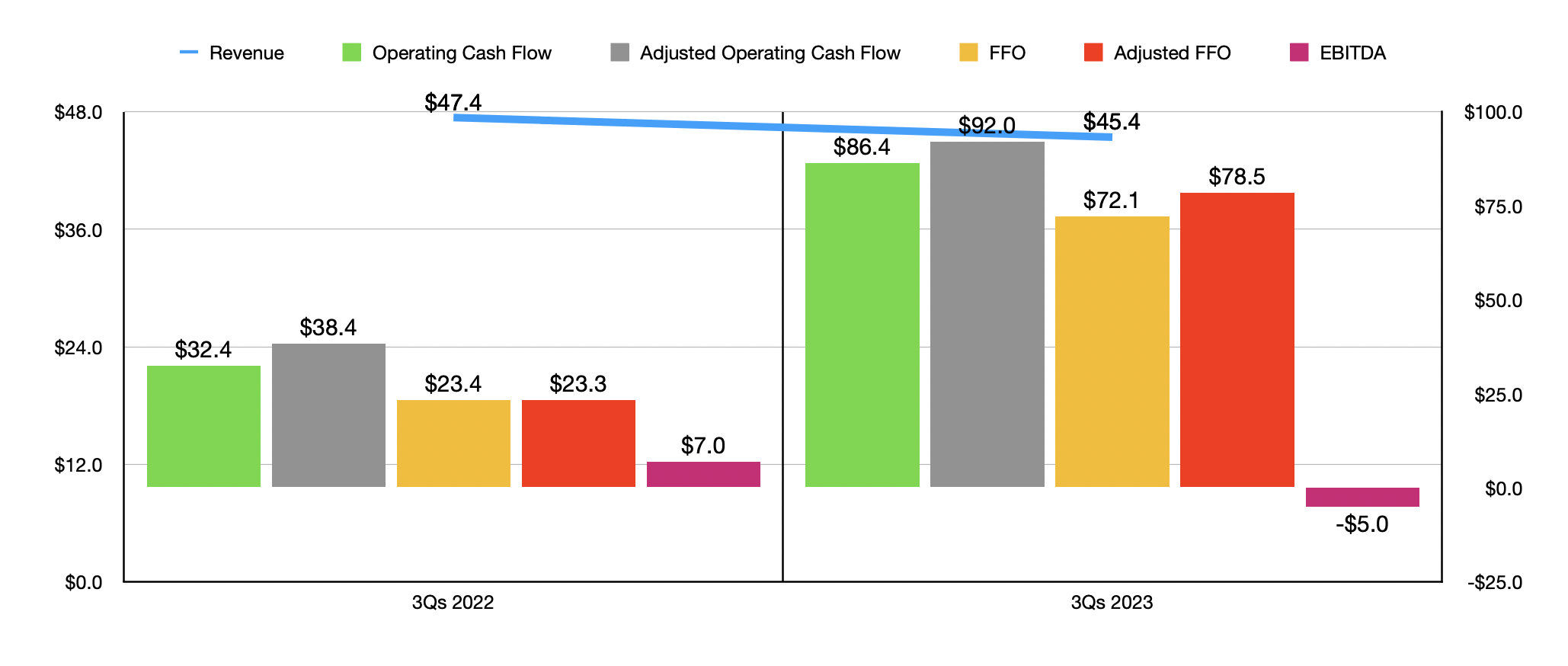

When it comes to overall profitability, the picture for the company is quite attractive. Despite the modest amount of revenue, it generated $86.4 million in operating cash flow and $92 million of adjusted operating cash flow in the first nine months of last year. In the chart above, you can see these numbers and others, and how they stack up against the same window of time one year earlier. It's incredibly rare for profits to be higher than revenue, even in the REIT market. However, management has benefited tremendously from investing that excess cash in this high interest rate environment. While I fully expect interest rates to begin falling this year, as long as they stay elevated, the business should do well to generate additional positive cash flows.

{kind=link}

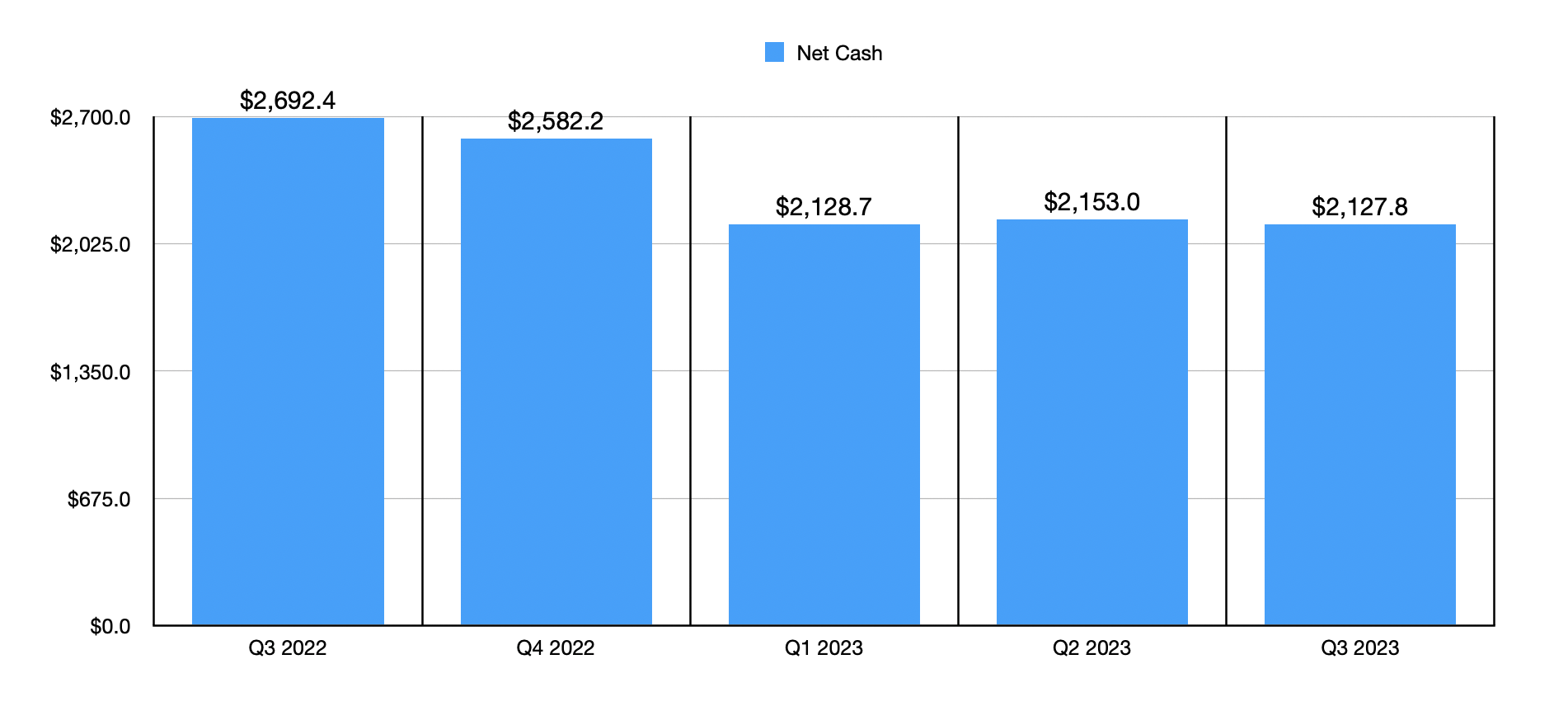

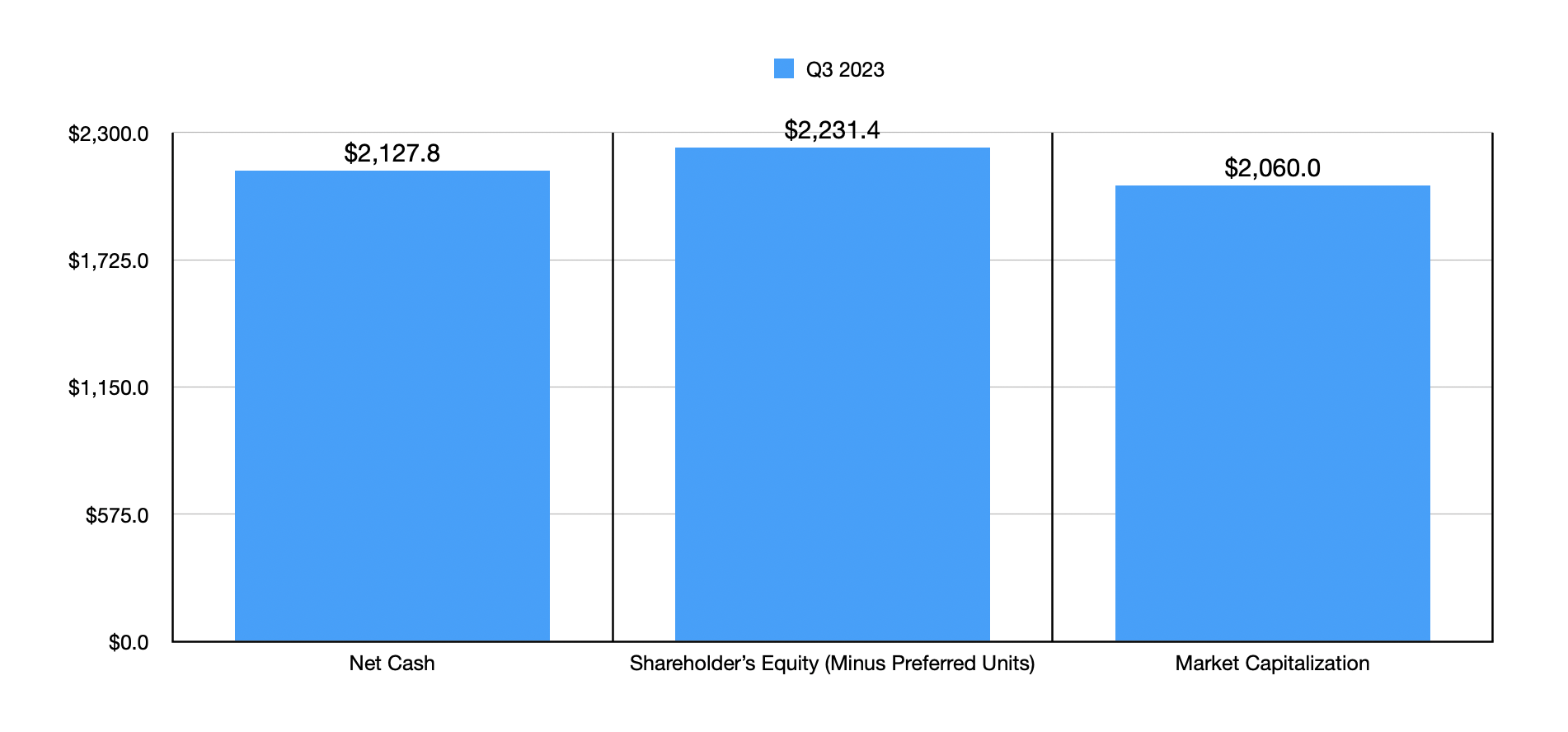

In my opinion, the best-case scenario for shareholders is that, as interest rates fall, management will decide to use the $2.13 billion in cash and cash equivalents that the company has, in addition to potential leverage, to buy up attractive assets. To be perfectly honest, given my own view regarding the office space market, I would strongly prefer that it diversify into almost any other type of real estate. But even if we assume that management will just continue to payout the cash to shareholders until the company dwindles, that's not all that awful a situation. At present, the book value of equity of the company, after stripping out $122.9 million in liquidation value of preferred units, is $2.23 billion. Given how shares are priced right now, this means that just by buying the stock and liquidating the company, shareholders should get upside of 8.3%. That's on top of cash flows that will likely be $70 million or more per annum for this year and likely $40 million to $50 million per annum each year thereafter.

Absent something horribly stupid happening, I struggle to imagine a scenario where shareholders could actually lose money on this name. However, the market has so far disagreed with me. Since my bullish article on the company back in June of last year, shares have seen downside of 7.2% while the S&P 500 has been up by 10.7%.

{kind=link}

The days of "high" growth are gone

The last niche REIT that I would like to point you to is one that I have been bullish on for some time. The company in question is Innovative Industrial Properties, Inc. ( IIPR ), which owns and operates real estate that caters to the cannabis industry. By and large, the firm has grown by means of acquisition, approaching cannabis operators that were looking for additional cheap capital that could be used to grow in what was, a few years ago, a rapidly growing space. It would buy those assets off of the cannabis firms and lease them back to them, often under long term agreements. Even today, as the industry has died down, Innovative Industrial Properties has a weighted average time remaining on its leases of 14.9 years. When it comes to the industrial REIT market, this is considered quite high compared to what I have typically seen, with a usual range of between five and eight years.

{kind=link}

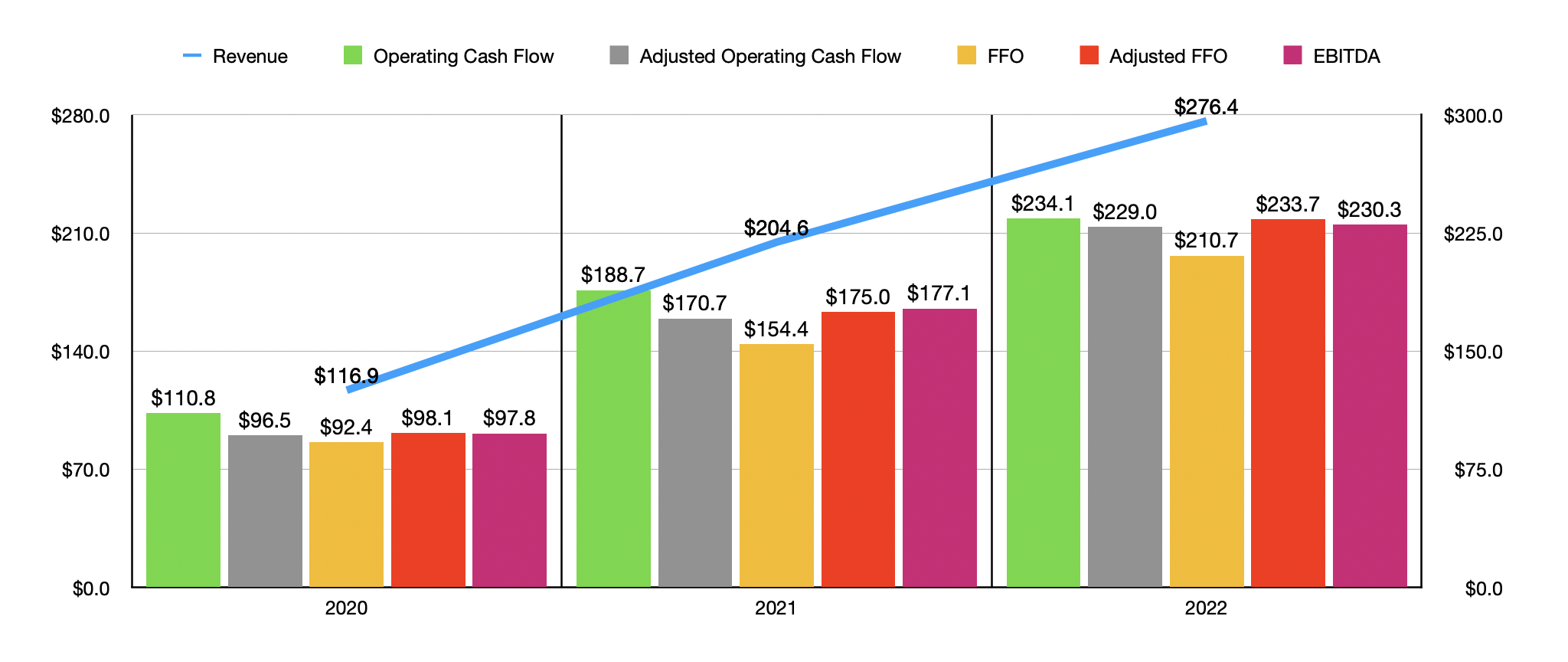

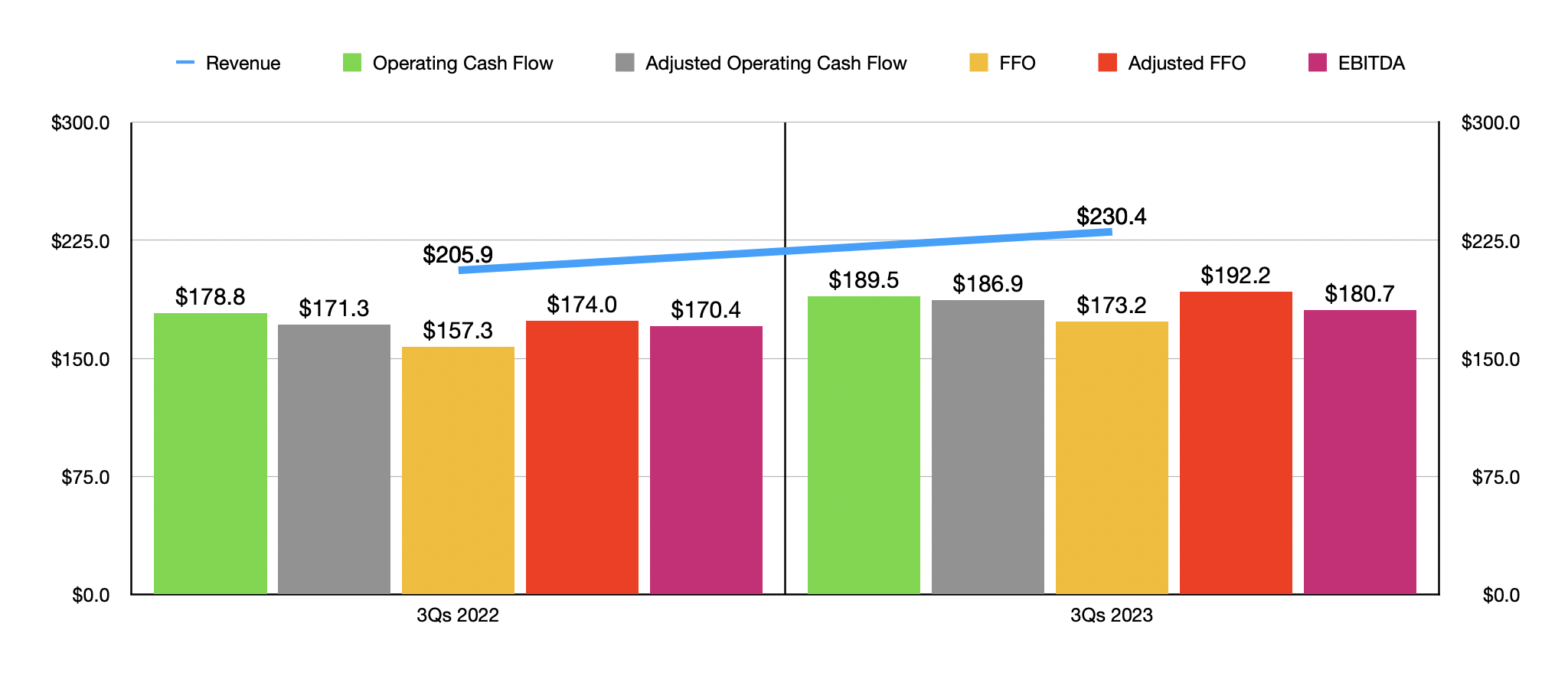

Even up through 2022, Innovative Industrial Properties was taking advantage of the continued legalization of cannabis, not only for medicinal purposes, but also recreational purposes, to grow. In 2020, for instance, the company generated revenue of only $116.9 million. By 2022, sales had grown to $276.4 million. As you can see in the chart above, profitability metrics for the company have followed a similar trajectory. And in the chart below, you can see that it has enjoyed continued growth throughout 2023, with that data covering the first nine months of that year compared to the same time of the 2022 fiscal year.

{kind=link}

In the past, the excitement in the market, combined with large amounts of cash on hand and low interest rates, made it easy for Innovative Industrial Properties to expand variant but those days of rapid growth are coming to an end. In 2021, the company purchased 14 properties comprising 2.27 million square feet of space. That cost shareholders about $288 million. In 2022, the company purchased only nine properties that made up 591,000 square feet and that cost a much more modest $166.6 million. And in the first nine months of 2023, the company acquired only 215,000 square feet of space for a paltry $35.2 million. Despite this slowdown, shares have done quite well. Since I first rated the company a "buy" back in 2019, shares have seen upside of 70.6% when you include the distributions that it pays out. That almost matches the 71% upside seen by the S&P 500 over the same window of time.

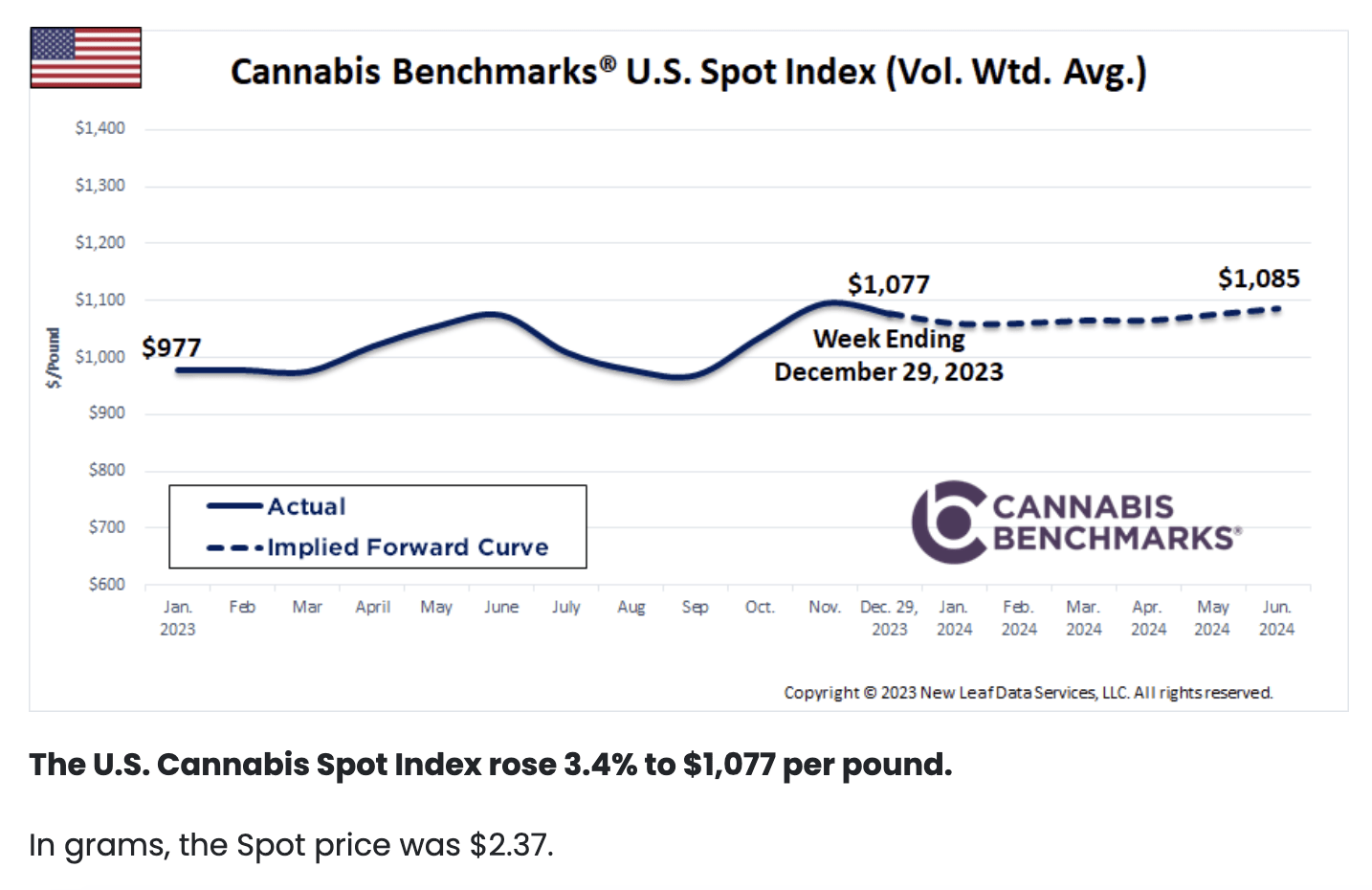

While the pandemic certainly had an impact on the cannabis market, the big problem for the space involved and over investment in cannabis production capacity. Demand was significantly overestimated and hopes that a national ban on the product would be lifted proved to be premature. The good news, and this is what gives me hope, is that there are signs that the worst for the industry is now over. For the week ending December 29th of 2023, the spot price per pound of cannabis was $1,077. That's up from the $977, an increase of 10.2%, compared to what was seen at the same time one year earlier. Current forecasts call for the spot price to rise further to roughly $1,085 per pound. It's also important to note that Florida and Pennsylvania are seeing significant pushes to legalize it for recreational purposes. And in November of last year, my home state of Ohio became the 24th state to legalize it for recreational users.

{kind=link}

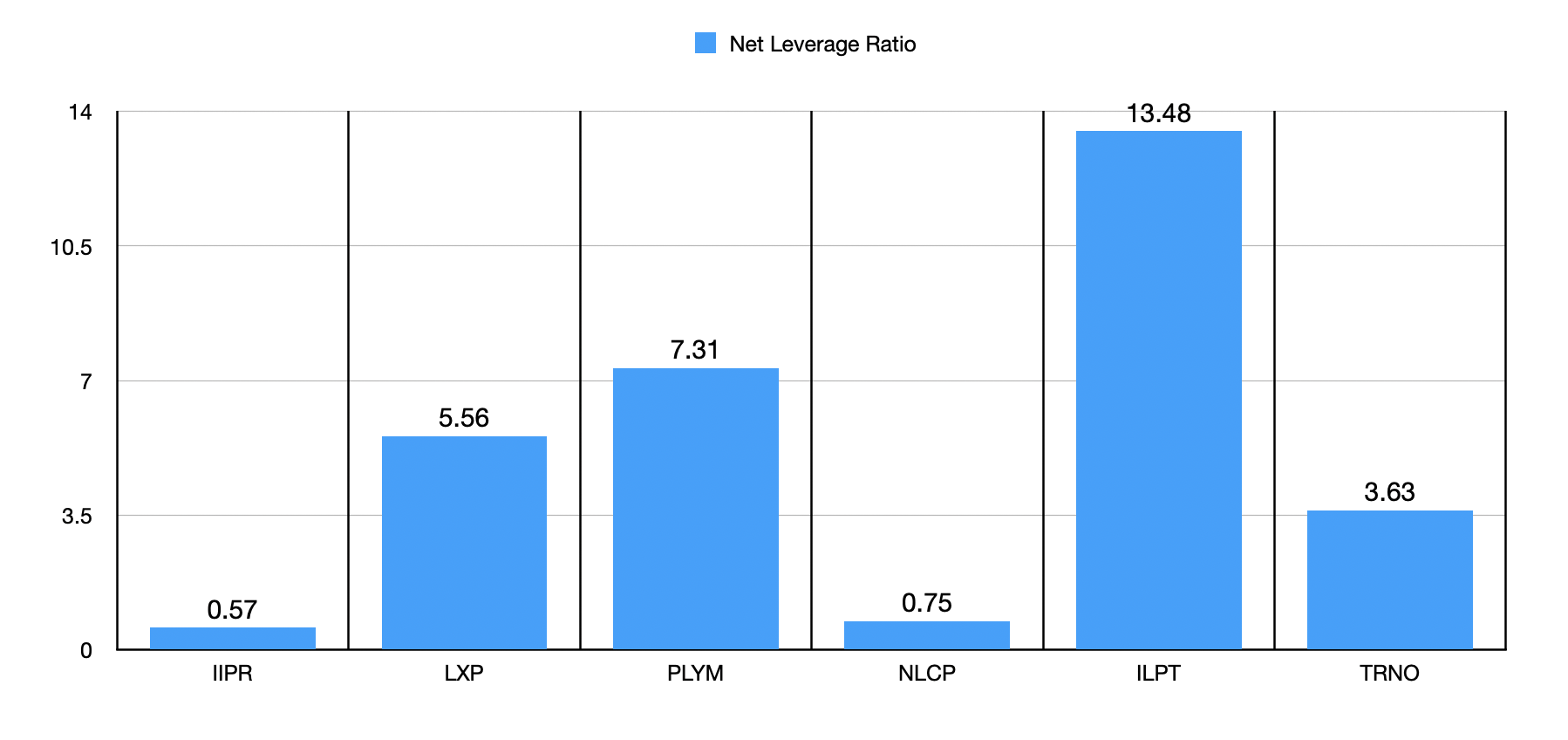

In addition to the industry showing some signs of recovery, there are other benefits to the company. For starters, its net leverage ratio is only 0.57 based on my estimates. In the chart below, you can see its net leverage ratio compared to the net leverage ratio of five other industrial REITs. Only one of these, NewLake Capital Partners ( NLCP ), is comparable to this at 0.75. It's no coincidence that NewLake Capital Partners is also another cannabis REIT.

Author - SEC EDGAR Data Author - SEC EDGAR Data

{kind=link}

{kind=link}

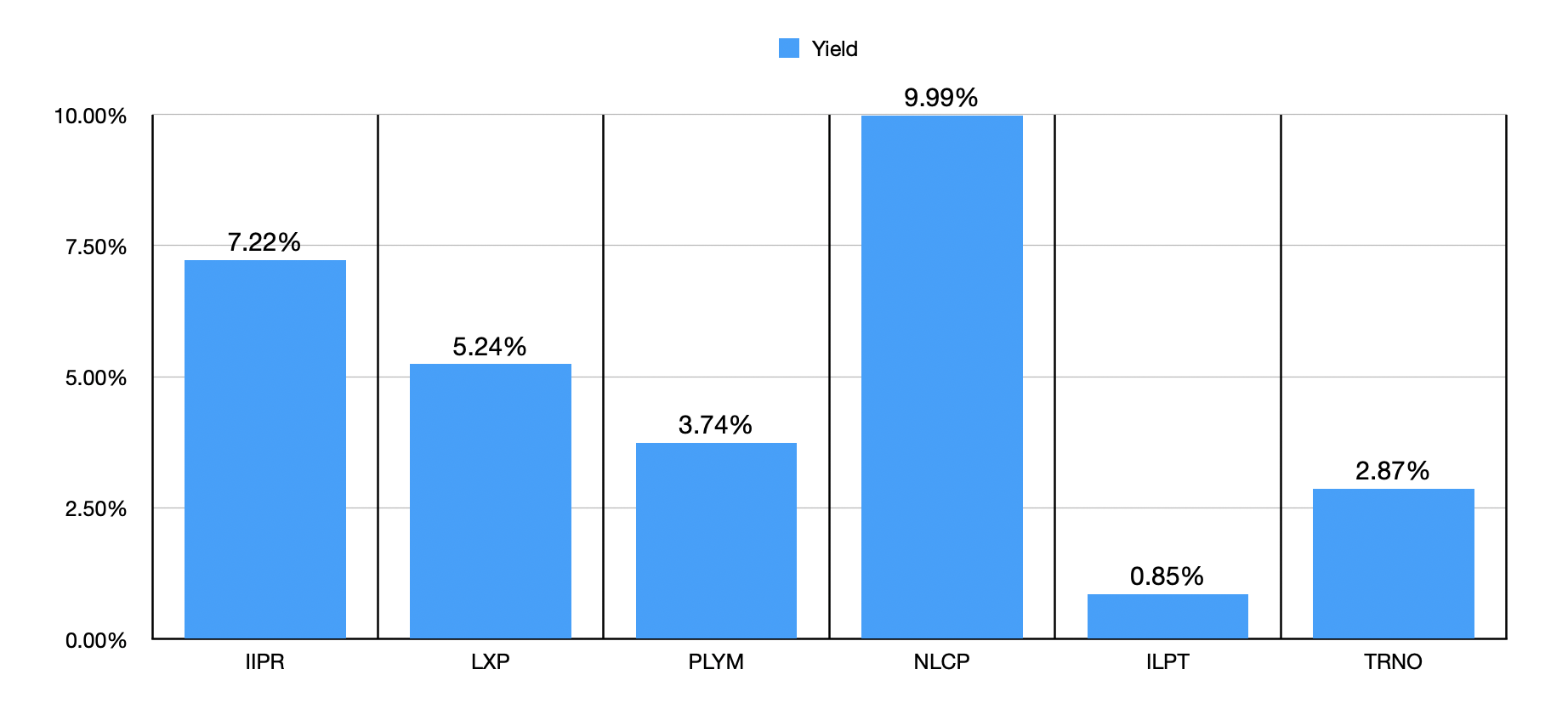

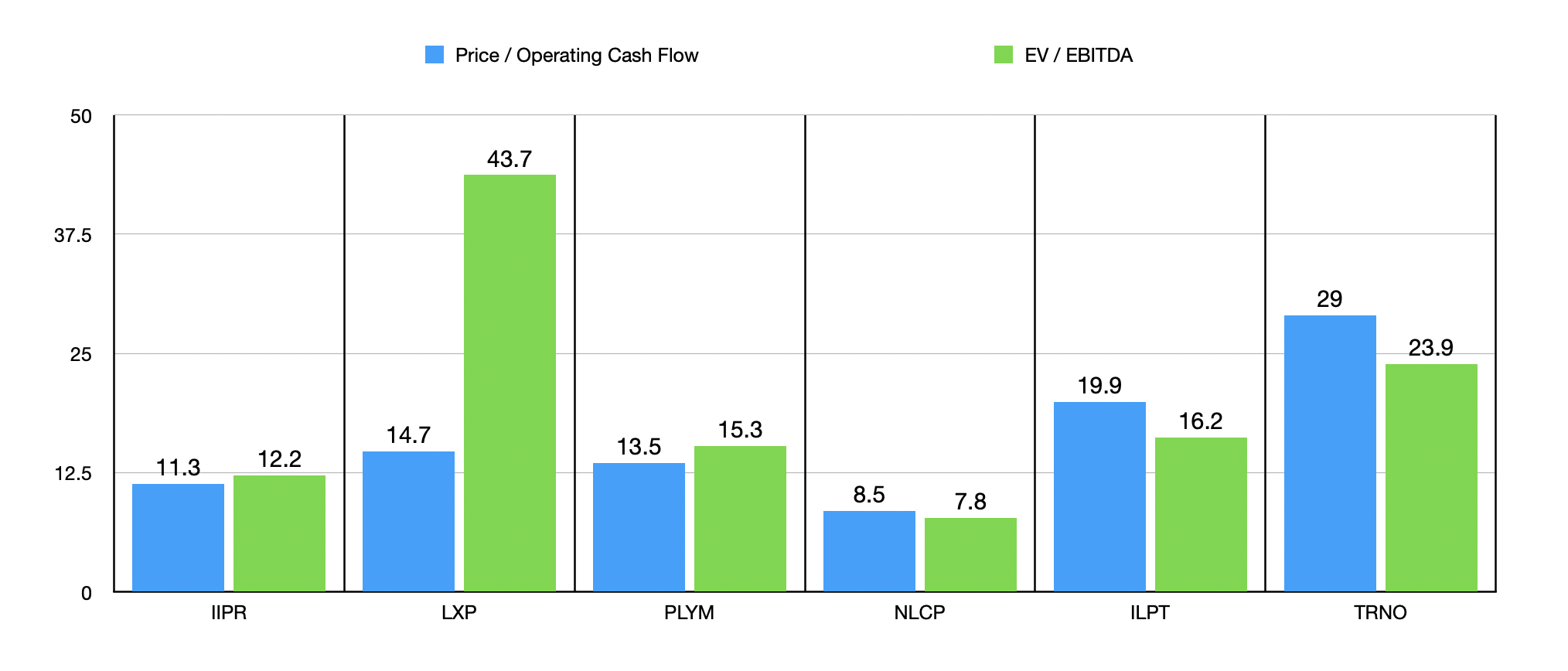

In the next chart, I also showed the yield of each of these companies. Even by REIT standards, Innovative Industrial Properties pays out a hefty amount of cash, with an effective yield of 7.22% as of this writing. Of the other players in the space, only NewLake Capital Partners is higher at 9.99%. I then, in the chart below, decided to value all of these companies using two different valuation metrics. Only one of the five firms ended up being cheaper than Innovative Industrial Properties using either of the metrics. As you might imagine, that company is none other than NewLake Capital Partners.

{kind=link}

Now, given the comparable net diverge ratios of both businesses, and the lower share price and higher yield that NewLake Capital Partners offers, you might wonder why I am promoting Innovative Industrial Properties instead of it. Simply put, in my view, NewLake Capital Partners is the riskier of the two businesses. For starters, Innovative Industrial Properties is far larger, with 108 properties under its belt compared to 37. The days of rapid growth are likely in the past, meaning that it would be more difficult and potentially expensive for a smaller player to scale. But, in addition to this, there is the issue of exposure. 25% of NewLake Capital Partners’ revenue comes from its largest tenant, with a whopping 79% coming from its top five largest tenants. These numbers for Innovative Industrial Properties are much more modest at 15% and 40%, respectively. So in the event that the cannabis market continues to struggle, Innovative Industrial Properties will almost certainly be more stable by comparison.

Takeaway

For investors looking for interesting REITs with unique conditions, I definitely believe that the three companies that I highlighted in this article should be taken very seriously. Two of them payout rather hefty yields relative to similar firms. All three of them have characteristics that distinguish them from their peers and, absent something unexpected occurring, I have a hard time believing that these firms will prove to be bad or subpar investments. For now, for the reasons I have already stated throughout this article, I am keeping the companies rated as they were rated previously, with the first two as "strong buy" prospects and the other being a "buy."

For further details see:

3 Specialty REITs You Definitely Should Not Ignore In 2024