TMUS - 3 'Strong Buy' REITs At Steep Discounts

2023-06-21 07:30:00 ET

Summary

- REITs are typically priced at a premium to their net asset value.

- Today is an exception. They are priced at steep discounts.

- I highlight what I think could be once-in-a-decade buying opportunities.

REITs are generally priced at a small premium to their net asset value.

This makes sense given that you get to make a real estate investment with the added benefits of liquidity, diversification, and professional management.

But on rare occasions, REIT share prices crash and they become heavily discounted relative to the underlying value of their properties.

This is what has happened over the past year.

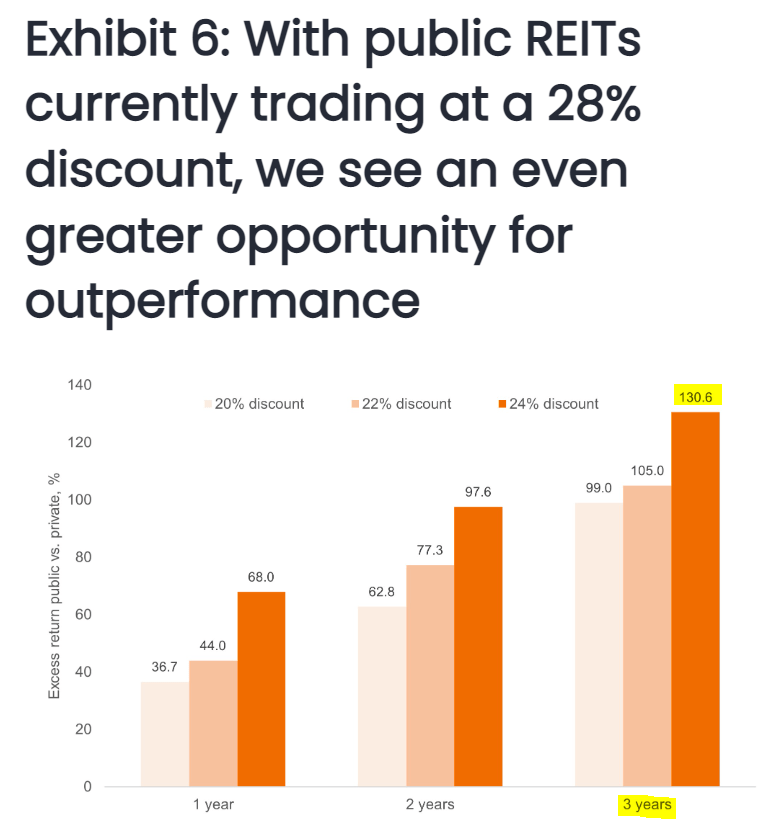

REIT share prices crashed even as their cash flows kept on rising and as a result, REITs are now priced at a ~30% discount to their NAVs on average, which is reminiscent of the great financial crisis:

Historically, whenever REITs have been priced at such low valuations, they have been great investment opportunities.

According to a study by the investment firm Janus & Henderson, REITs have historically generated a 131% total return over the next 3 year period following a market crash:

{kind=link}

Janus & Henderson

Today, the discounts to NAV are actually even larger than what was used in this study - which would indicate that REITs could earn even greater returns in the coming years.

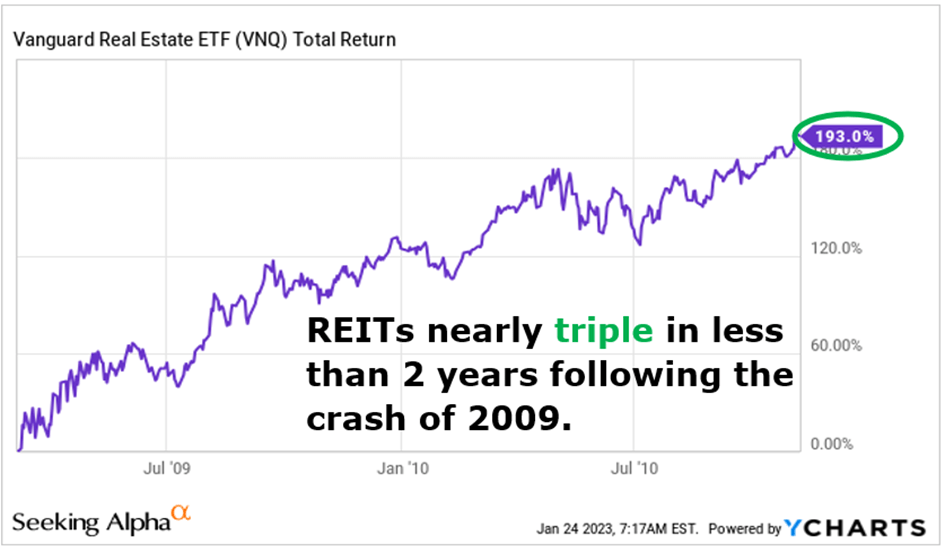

The discounts are today reminiscent of the great financial crisis - which was a once-in-a-decade opportunity to buy REITs as they then nearly tripled investors' money over the following 2 years:

{kind=link}

YCHARTS

Now, I am not saying that REITs will triple your money over the next years, but valuations are exceptionally low again, and so I expect very large gains from certain REITs in the following years.

In what follows, we highlight 3 REITs that present a once-in-a-decade buying opportunity:

Global Medical REIT ( GMRE )

GMRE is a small-cap REIT that has historically done extremely well for its shareholders thanks to its unique strategy of focusing on medical office buildings in secondary markets. These properties are often overlooked by most other investors and this has allowed it to get better cap rates, stronger lease terms, and ultimately, this resulted in massive outperformance relative to REIT indexes ( VNQ ):

Global Medical REIT

Today, its business is still doing just fine.

The REIT is better diversified than ever and it earns consistent and predictable rental income from long-term leases that include steady annual rent escalations. Medical office buildings are quite boring investments, but they are very defensive, whether the economy is booming or not.

But despite that, GMRE's share price has crashed over the past year. It is down a lot more than the average of the REIT sector, likely because of its smaller size and slightly higher leverage than average:

We think that this is an opportunity because the shares are now priced at a roughly 30% discount to NAV, just 9.5x FFO, and an 8.8% dividend yield that's sustainable.

The surge in interest rates is a near-term headwind that will slow down the company's growth, but it does not change the long-term thesis for investing in these properties, which will continue to generate steadily growing income for a long time to come.

I met their management recently at the NAREIT REITweek conference and they explained that they are now focused on deleveraging which I think will eventually help the sentiment of their stock.

I estimate that their fair value is about 50% higher yield and you earn a high 8% dividend yield while you wait. If like me, you think that interest rates will likely return to lower levels in the coming years, then the upside could be realized quite rapidly.

Vonovia (VNA / OTCPK:VONOY )

Vonovia is the biggest apartment landlord of Europe. It owns over 500,000 units, mostly in Germany, but also in Austria and Sweden, which are strong markets.

Historically, the stock of the company has been priced at a ~10% premium to its NAV during most times because the market has perceived it as a "blue-chip" with defensive cash flows, a strong management team, and a safe BBB+ rated balance sheet.

But this changed following the pandemic and Russia's invasion of Ukraine, which sparked a surge in inflation and interest rates.

Investors panicked and run for the exit, causing its share price to drop to its lowest valuation ever, now trading at a 65% discount to its NAV:

Vonovia

Such large discounts are truly exceptional and indicate that the company is going through very severe distress, but that simply isn't the case.

Yes, the company has a fair bit of leverage, but as I noted previously, it still has a strong BBB+ rated balance sheet (just shy of an A-rating) and this is because (1) its debt has a fixed rate, (2) its maturities are long and well-staggered, (3) and most importantly, its assets generate very defensive cash flows. (because of how rents are regulated in Germany, they kept on rising even through 2008-2009!)

Therefore, the company has time on its side. Its rents are steadily growing by 3-4% per year, it is retaining over half of its cash flow to pay off debt organically and then on top of that, it is opportunistically selling some assets to deleverage even faster.

Just recently, it announced two dispositions at near their NAV and this will allow it to pay off its maturities in 2023 and a big chunk of 2024 as well. They achieved these dispositions at peak uncertainty so more will likely follow.

I think that as cap rates expand a bit more, its NAV per share will come down a bit, but even using a more conservative NAV estimate, the shares have 100% upside potential and while you wait, you earn a 4.5% dividend yield.

I love the risk-to-reward and the diversification benefits as part of my portfolio.

Crown Castle ( CCI )

One last name that I have been accumulating lately is Crown Castle.

This is one of the biggest cell tower owners in the world with 40,000+ towers and it also owns a growing portfolio of fiber and small cells - all which benefit from the adoption of 5G and the growth of data usage.

Historically, it has done very well for its shareholders as it was able to steadily grow its dividend by 7-8% year after year:

Crown Castle

Crown Castle

But recently, its share price dropped by nearly 50%.

That's not a correction. That's a real crash!

It implies that something very bad must have happened.

But no, not really. What happened is that CCI ran through a speed bump. Its growth rate will slow down over the next 2 years because it will suffer some lease cancellations due to T-Mobile's ( TMUS ) recent acquisition of Sprint.

The market of course only cares about the short term and so it hates this.

But if you can look past the next two years, then I think that this is a fantastic buying opportunity because the growth is expected to accelerate in 2026 and this will likely lead to a repricing of the stock.

Today, the stock is priced as if the growth story was over with a 5.5% dividend yield and a 25% discount to NAV - a historically low valuation for the company.

But as the growth returns, I expect the stock to reprice at closer to a 3-4% dividend yield, leading to 30%+ upside from here. That's not quite as much as GMRE and VNA, but this is coming from a much safer company and so the risk-to-reward is equally attractive.

Bottom Line

Buying good real estate that's conservatively financed at a large discount to its fair value has always been a good investment in the long run.

REITs have historically always recovered from every market crash and richly rewarded those who had the courage to buy them following corrections.

I don't think that this time will be any different. On the contrary, I think that REITs could be particularly rewarding in the next recovery because the high inflation has led to materially higher rents and property replacement costs.

I have been accumulating REITs over the past year and will continue to do so at these low valuations.

For further details see:

3 'Strong Buy' REITs At Steep Discounts