DM - 3D Systems And The Merger Drama

2023-09-27 03:02:19 ET

Summary

- The 3D printer industry needs consolidation. There has been a soap opera playing out amongst 4 different companies on who will acquire who.

- 3D Systems Corp has seen stagnated growth over the past 10 years. They need something to improve their business.

- The merger between 3D Systems Corp and Stratasys Ltd would be a positive for both companies.

I have been interested in the 3D printer or additive manufacturing market. Having used small scale hobby printers and slightly larger ones within businesses that I operate. I see a lot of growth potential within 3D manufacturing at both a large and small scale. I began my hunt for any 3D printing stocks that would make a good investment. I started by looking at the actual manufacturers of the 3D printing machines. I wrote a previous article about Markforged Holding Corporation ( MKFG ). In that article I discuss more about why I think there is potential in the market and what interests me so much about it.

Following in the same vein as my previous article I want to take a further look into 3D Systems Corp ( DDD ). They are another manufacturer of 3D printing hardware and technology. The company has been in the middle of a soap opera within the 3D printing space. They have an outstanding offer to acquire Stratasys ( SSYS ) another manufacturer of 3D printing hardware. I will discuss this potential acquisition and potential both within and without this acquisition.

3D Systems Corp

3D Systems provides comprehensive 3D printing and digital manufacturing solutions, including 3D printers for plastics and metals, materials, software, and digital design tools. The solutions support advanced applications in two key industry verticals: Healthcare Solutions (which includes dental, medical devices, personalized health services and regenerative medicine) and Industrial Solutions (which includes aerospace, defense, transportation and general manufacturing).

The company generates revenue from the sale of products and services through the Healthcare Solutions and Industrial Solutions segments. Within the products space segment the company offers a range of 3D printers, materials, software and digital design tools. The company develops its own proprietary materials that are used within many of the machines. The company has developed its own proprietary software that helps enable workflow from design to production for companies.

The services segment includes maintenance and training services, advanced manufacturing, software services (subscriptions), and healthcare solutions services.

Financials

One of the things that I want to see is a growing business. DDD has not been that. The company has not seen revenue growth in the last 10 years. The company saw revenues climb to their peak in 2018 and have since seen a decline. It is actually impressive that the company has been so consistent on revenues. The problem is that there is no growth in the business. Revenues in 2013 were $513 million, the trailing twelve months $514 million. So in 10 years' time revenues have not increased. That is not a promising sign for the go forward. I understand that there are blips that come up but to see revenues as flatlined as they are with DDD is not great. The image below shows the revenues for the last 10 years.

{kind=link}

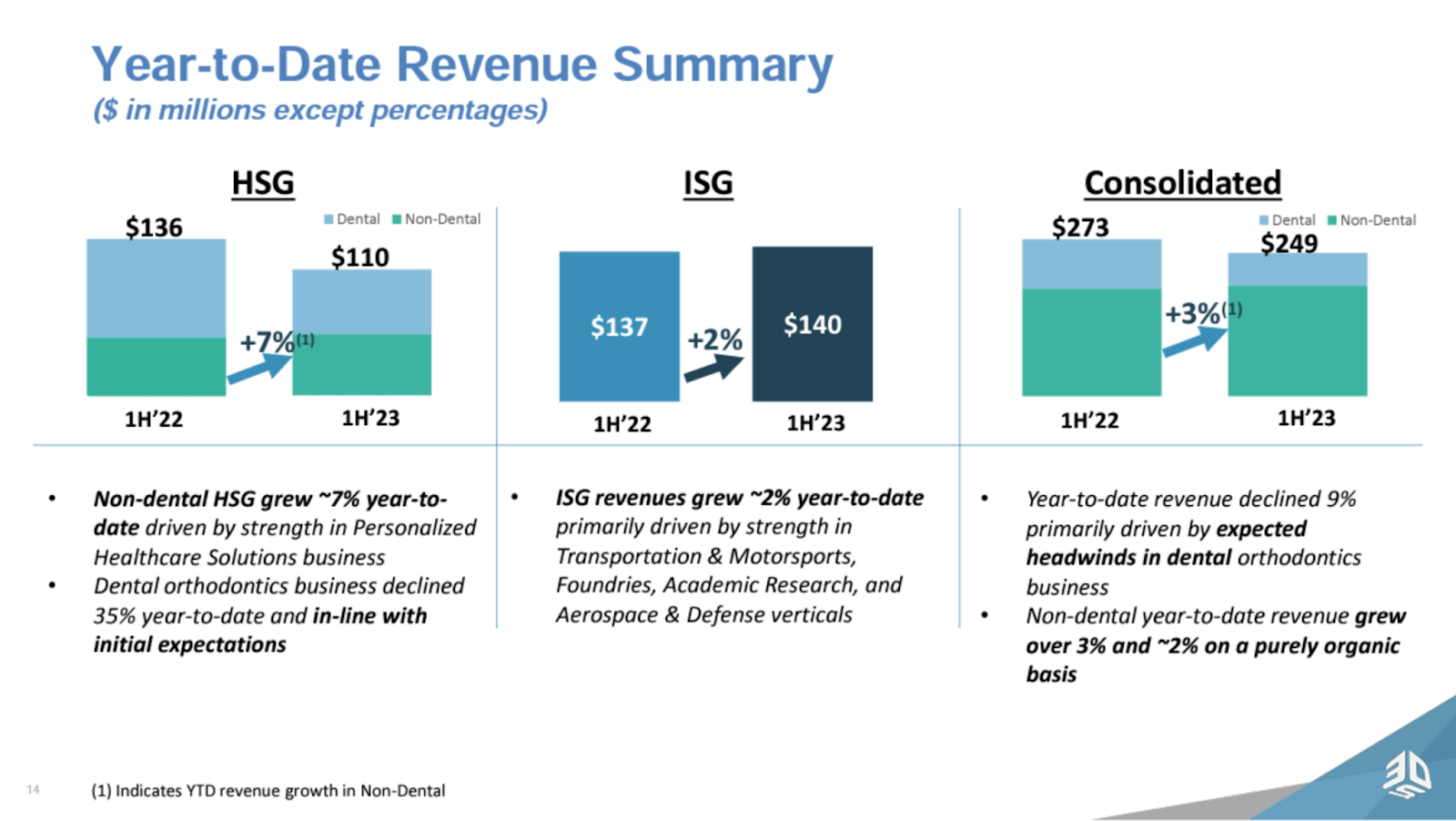

The company has seen a decline in revenues more significantly in the past year. The main cause of this is the large decline within the Healthcare Solutions business. This decline is due to the dental market which has declined significantly in the past year. The dental business saw a decline of 35% in the first 2 quarters to start the year. The rest of the Healthcare Solutions business grew 7%. The Industrial Services segment saw a very modest increase of 2% in the first six months. Overall revenues declined 9% in the first six months of the year.

{kind=link}

There is a leveling off in the dental market so the company should start to see some growth going forward. It is working off a lower base than before due to the decline though so this positive is only a positive due to the negative that preceded it. The company projects high-single to low-double digit growth excluding the dental market. Overall the revenue picture does not look great. The decline might be slowing but there is not a lot of expectation for significant revenue growth in the near future.

One thing that I do like about DDD is that they have a good gross margin. It is not great but it is good. High enough that there is potential for the company to earn a profit. The company had a gross margin of 39.8%, 42.8%, and 40.1% in 2022, 2021, and 2020 respectively. So there has been a little margin pressure over the past year. Their latest quarterly report showed a gross margin of 39%. Not trending in the right direction but not such a significant drop that it concerns me. The company also projected that gross margin will return to 40%+ as revenues begin to stabilize.

The company is loss making and has been since 2014. It has been in the process of being more efficient and cutting costs where it can. Without revenue growth the company has no choice if it hopes to turn a profit. The company is expecting to turn a positive EBITDA to end the year. This is a positive sign that they are getting costs under control to the point where they can be EBITDA positive. If they can return to any form of growth and keep the costs down then they have the potential to have a positive EBITDA next year.

The cash position is another strong point for the company. It ended the latest quarter with $492 million on the books. It used $46 million during the latest quarter. This gives the company plenty of cash as they work to get themselves profitable. The question is if they can actually get themselves to that point.

Regenerative Medicine

One area of growth through which the company is hoping to execute is in the regenerative medicine segment. This is where they are investing a lot of their R&D dollars. This is pretty awesome technology and has a lot of potential if it is successful. A lot of money goes into medical research and medicine each year and it would open a large market for DDD. That being said, this is not an easy area to conquer. Also for much of this technology the company is partnered with biotech companies to perform their functions. It is fine if 3D Systems is able to complete their tasks but means nothing if the biotech firms are unable to get the science to work for them. This puts a large portion of this business out of the control of 3D Systems and increases the risk in my mind.

The regenerative medicine business is currently pre-commercial R&D. This means to me that it is going to be a cash burn for quite some time. The company is planning to invest at least $10 million into the business this year. That is okay if it is able to generate a healthy ROI. A company has to invest to continually advance and stay ahead of the competition. This is truly innovative technology but it is also higher risk, similar to investing in a biotech company. There is a lot of risk within this business line. It carries a lot more risk than building and selling 3D printing hardware and software. My concern is that this branches into areas that are outside of the skill set and know-how of the company. It is something to continue to watch as the R&D continues to progress.

Soap Opera

The 3D printer market is fragmented and there is a lot of competition. I think some form of consolidation is needed for companies to succeed within the space. It is currently playing out a bit like a soap opera. For those that have not been following, four companies have been going the rounds on who might be acquiring/merging with who.

It all started with Nano Dimension ( NNDM ) and Stratasys ( SSYS ). Nano holds 14.5% of outstanding shares of SSYS, on March 9, 2023 Nano offered to acquire the remaining outstanding shares for $18 a share in cash, or a value of $1.1 billion. SSYS rejected that offer on March 22, 2023 and called it unsolicited. While this is going on there was an internal takeover attempt with Nano Dimensions. The largest shareholder attempted to remove the CEO and replace the board members. Both sides were claiming victory. It seriously seems like stuff straight out of Succession. Nano increased the offer on March 30 to $19.55 or $1.2 billion, which SSYS promptly rejected again. Not one to give up, Nano increased the offer again to $20.05 or $1.22 billion . SSYS rejected this last offer on April 13. This would seem to be the end of Nano but we will come back to them later.

SSYS quickly moved onto the next hot item and announced on May 25, 2023 that they will merge with Desktop Metal ( DM ) in an all-stock transaction. The merger would leave SSYS shareholders with 59% of the combined company. This deal is pending a shareholder vote on September 28.

While that deal was in the works 3D Systems Corp ( DDD ) decided they were being left out of the dating scene and decided to make an offer for SSYS. Contingent on that deal SSYS would drop the deal to acquire DM. DDD’s offer was for $7.5 in cash and 1.2 shares of common stock in the new company. The companies entered into discussion and multiple offers were revised and updated. Their last offer (5th offer if I counted correctly) was for $7 in cash and 1.6387 in stock. SSYS determined the following day that the offer was not superior to the DM merger and called off further discussions with DDD. The official offer was delivered on the 14th of September and it will be left to a shareholder vote.

Nano never left the scene and continued to raise their offering to $24 a share and then lastly to $25 a share and also said they would be open to combining with DDD as well after the acquisition of SSYS. The board not only recommended against the acquisition but it also got a little nasty. The company said that Nano’s offer is “misleading, coercive, substantially undervalues the Company as a whole and is NOT [emphasis theirs] in the best interests of all Stratasys shareholders.” A statement about the deal doesn’t pull any punches. “Nano has destroyed significant value and trades at negative firm value,” the company writes. “Yoav Stern, Nano’s CEO, cannot be trusted, has made misrepresentations about Stratasys and is not qualified to manage Stratasys. Since Yoav Stern’s appointment, Nano has spent more than $500 million in cash and increased its revenue by only $44 million.” On August 1st the company officially announced the expiration of the offer as only 5.6% of the stock was tendered, not enough to reach the percentage needed. While it would seem this is the end of the Nano drama, they still control 14.5% of the outstanding shares and therefore have significant voting power on whatever deal is presented. They have come out and stated they will be voting against the DM merger.

This drama has not ended as we are still awaiting the vote on what SSYS will do. The board has made it very clear that it has a preference for the merger with DM. We will have to wait and see how the shareholders choose to vote. The SSYS and DM vote is set for September 28 and DDD acquisition offer will expire on October 5, giving the company 5 days following the vote concerning DM.

For a full list of articles and comprehensive timeline of the events surrounding the drama check out this link .

Merger or No Merger

We have two scenarios from this drama. SSYS merges with DM and DDD continues to operate as a standalone company. Scenario 2 is that shareholders vote against the merger with DM and approve the offer from DDD.

The financial review above outlines scenario 1. The company has seen sales declines and expects slow growth for the remainder of the year. While growth is great it is nothing to get too excited about. Also they need more growth than that in order to generate a profit. Either that or find a way to cut more costs to improve their margin profile. Regenerative Medicine is the pie in the sky hope and potential but that is not going to materialize revenues for some time. I don’t see a lot happening with the business as a standalone business. I think it will continue to operate as it has for the past 10 years.

What does the merged company look like? SSYS is in a similar financial situation as DDD. They have stagnated revenues. They have a good gross margin over 40%. They need to scale and be more efficient on their costs. A merger would seem to make sense if the companies are able to cross sell and increase revenues. They would increase their offering on printers and technology as well as software and processes. They could hopefully cut out a lot of overhead expenses that would overlap. They could combine their R&D efforts and cut costs on that front while increasing output due to combining research and technology. I think the biggest benefit would be the ability to leverage each company's technology and know-how across hardware, software, consumables, and services. It would be a scale play and also a technology play. This is the hopeful scenario of a combination. The doubtful one says that two unprofitable companies don't make a profitable company.

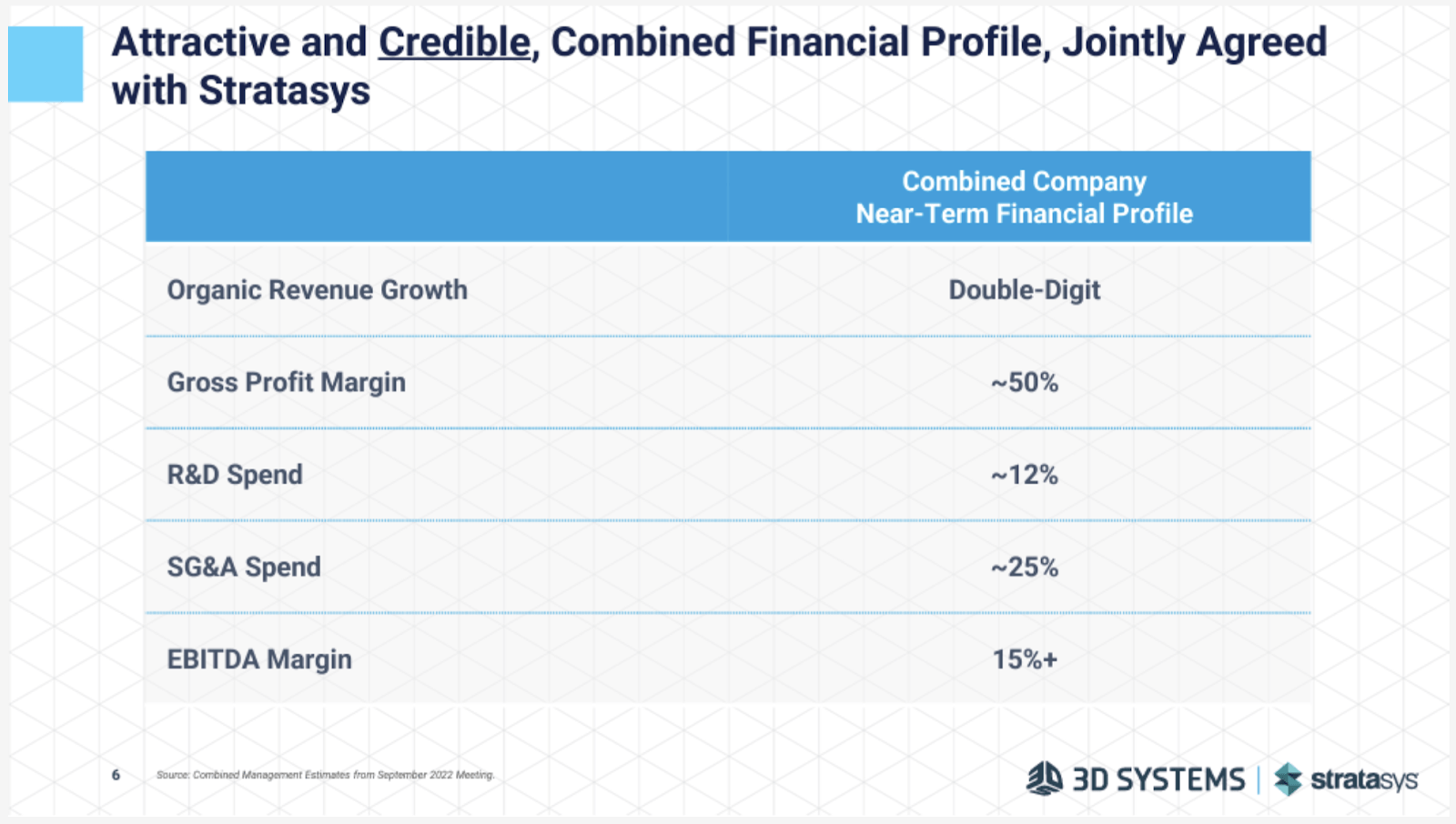

DDD put out a presentation that outlines their expectations of the merger. The image below outlines their expectations on the financials.

{kind=link}

If this were to play out then it would be a significant improvement from the current standing. It would also make for a compelling investment. Currently SSYS has a higher gross margin at 43% and DDD is at 39%. Getting to 50% would be a rather significant improvement. The hope is that with their larger scale they could get higher utilization rates and also lower costs on materials. There are also certain products that overlap. They would be able to cut out certain products and lower costs on that front. The R&D spend goal I think is achievable. They currently operate at 17% and 14% of revenues. I think there would be plenty of opportunity to cut overlapping functions and consolidate costs. SG&A spend also shows a significant decrease from current rates. The two companies currently have SG&A spend that makes up 47% and 39%. I think it might be a bit of a stretch to get to 25% of revenue. There would be plenty of overlap on functions to eliminate and there would be a decline in the SG&A spend as a percentage. I just don't know if they would get to 25%.

I think the actual results probably fall somewhere in between the company expectations and doubtful thinking. Overall I think the merger would be a positive for both companies. Where both companies are in a rather steady run rate on the revenues, scale could help them get to profitability. They would be able to cut costs down as a percentage of revenue due to the combined size. They could also leverage each other's hardware and technology and increase sales on that front. I think the combined company would be a much better investment than DDD on its own. With the high level of uncertainty on the acquisition among other things I would want to wait to see how things played out before jumping into the stock.

Conclusion

The 3D printer market is very competitive. Currently the companies operating in the space have found difficulty being profitable. A consolidation within the industry is needed and warranted. There is a soap opera playing out as 4 companies vie to see who will merge or acquire who. DDD has made a proposal to acquire SSYS. I think the combination would be a positive for DDD. The combined company would have more efficiency with its spending. It would have more scale with its products and this would help the cost structure. It also would allow the companies to increase their technology and product offerings. If a merger would occur then I think it makes for an interesting investment.

There is a lot of risk around the investment as it is unclear how shareholders of SSYS will vote. If the shareholders vote for the merger with DM then DDD will be moving forward on its own for now. As a standalone company I do not see a reason to invest in DDD. They are not showing growth. If it is able to execute on the Regenerative Medicine business then there could be some growth potential. It is too far out at the moment for me to buy into that. They have not grown revenues in 10 years. They are loss making and are not growing to really change that. While the overall market might be growing and therefore there is potential for DDD to grow with it, I would want to see some evidence of that first. So far it seems that new entrants and other companies have been able to capitalize on the growing market and not DDD.

I am a hold on the company for the time being. I do not think the company is a buy as a standalone company. I think the company will become much more intriguing if it is able to complete its merger with SSYS. There is too much risk around it for me to buy at the moment. I have a wait and watch on DDD.

For further details see:

3D Systems And The Merger Drama