K - 4%-Yielding Kellanova Could Be A Diamond In The Rough

2023-12-20 09:23:13 ET

Summary

- Kellanova, formerly known as Kellogg Company, is now a snack-focused business after spinning off its North American cereals business.

- Over 80% of Kellanova's annual net sales come from snacks and emerging markets, demonstrating a focus on high growth areas.

- Despite challenges, Kellanova has shown sustained organic net sales growth, restored gross profit margins, and above-algorithm growth in operating profit.

Introduction

This year, I have discussed a wide range of consumer staple companies, ranging from companies with strong pricing power like PepsiCo ( PEP ), The Hershey Company ( HSY ), and Procter & Gamble ( PG ) to recovery plays like Kraft Heinz ( KHC ) and Conagra Brands ( CAG ).

One company that was requested by a lot of readers is Kellanova ( K ) , which was formerly known as the Kellogg Company before it spun off its North American cereal business to become a major snack-focused player. The spin-off is now called WK Kellogg Co ( KLG ).

Hence, in this article, I'll take a closer look under the hood, as Kellanova is now competing with two of my favorites in the snack business: Hershey's and PepsiCo.

However, it also comes with a 4.2% yield.

Unfortunately, over the past year, K shares have returned just 24%, including dividends!

Hence, in addition to covering what Kellanova is all about, I want to assess if we can expect the company to keep up with its bigger snack peers.

If that is the case, Kellanova may be a no-brainer, offering both growth and income.

So, let's find out!

The New Kellanova

To quote the Wall Street Journal :

By combining the “Kell,” from Kellogg, with “anova,” which incorporates the Latin word “nova,” meaning new, the name reflects the company’s past and its future, according to Kellogg.

I usually do not comment on these things, but I really dislike this name. This name makes me think of a drug developed by one of the biotech companies on my radar.

Needless to say, it won't impact my opinion of this company. I just wanted to get this off my chest.

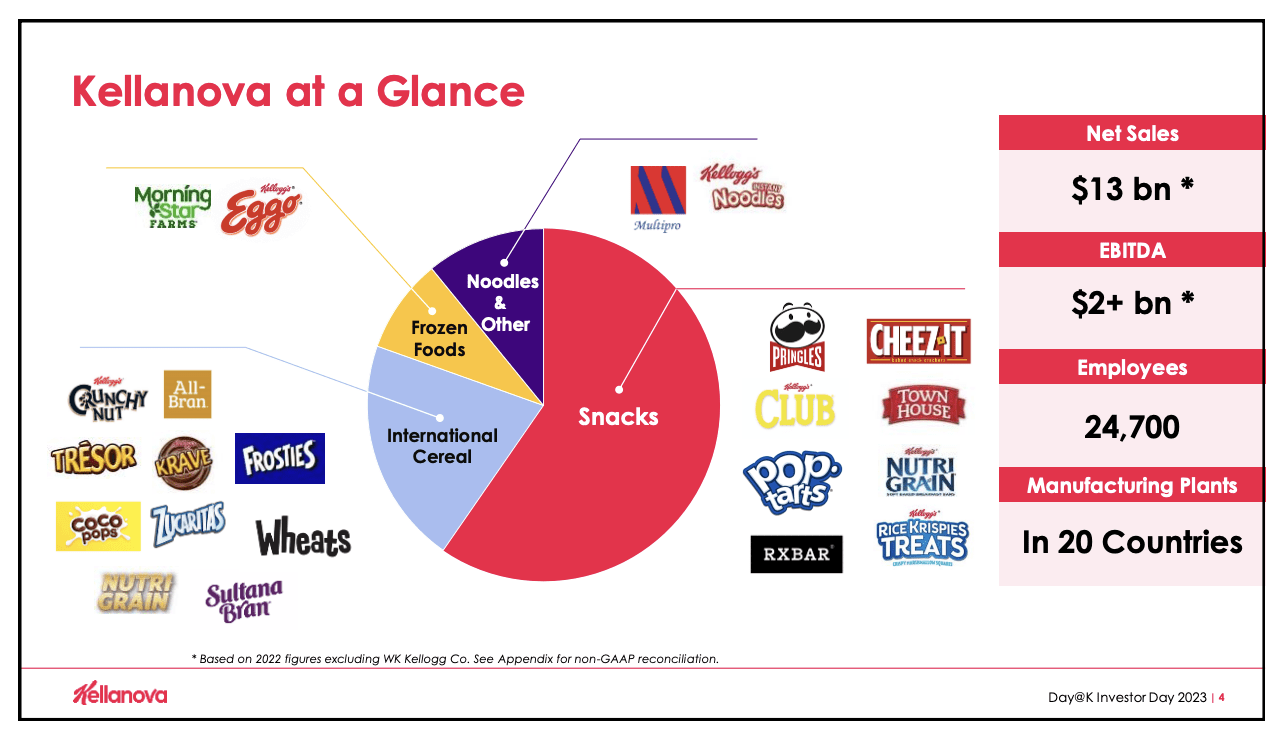

As I mentioned in the introduction, after spinning off its North American cereals business, the company is now a snack-focused business.

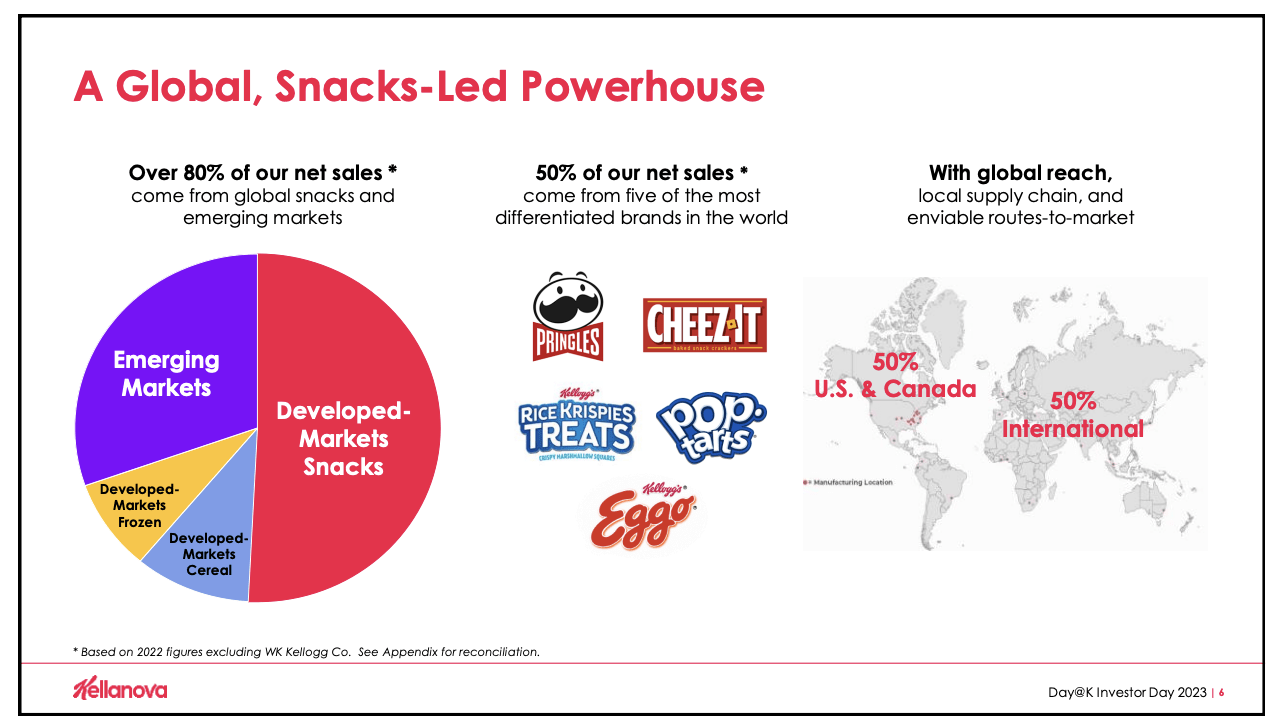

Over 80% of Kellanova's annual net sales come from snacks and emerging markets, demonstrating a focus on high-growth areas. Five key brands, including Pringles and Cheez-It, contribute significantly to net sales.

{kind=link}

Kellanova

The decision to exclude the North American and Caribbean cereals highlights a focus on optimizing and refining the portfolio for enhanced growth prospects.

This strategic move positions Kellanova to allocate resources efficiently, directing efforts toward segments that are poised for significant expansion, allowing it to generate more shareholder value.

According to the company, one of its key strengths lies in its robust performance in emerging markets, particularly in the AMEA (Asia, Middle East, and Africa) and Latin America regions.

{kind=link}

Kellanova

The consistent double-digit organic net sales growth in these regions, despite challenges such as cost inflation and currency fluctuations, shows the resilience of Kellanova's business model.

I agree with this, as every major snack company with good products was able to grow both volumes and prices in emerging markets over the past two years.

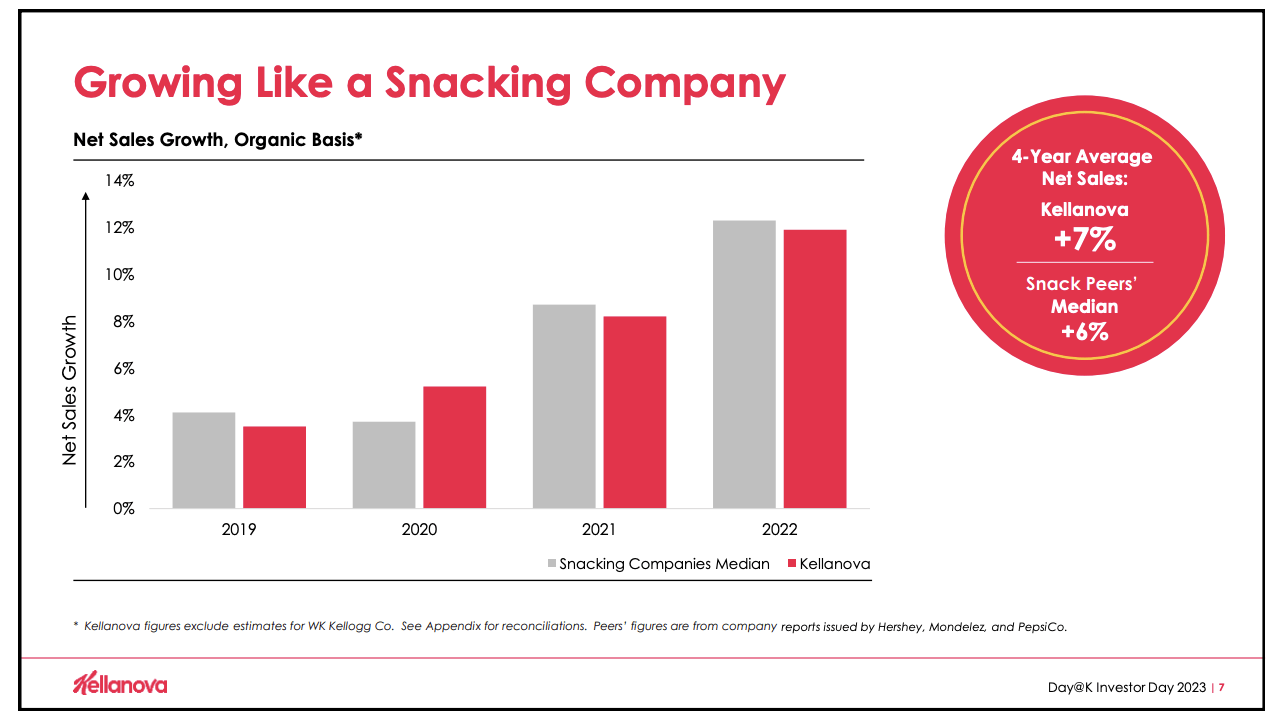

Also, the company's data shows outperforming growth over the past four years (excluding 2023 and mainly due to strong growth in 2020).

{kind=link}

Kellanova

This success is also visible in 2023.

Kellanova Is On Track For Higher Growth

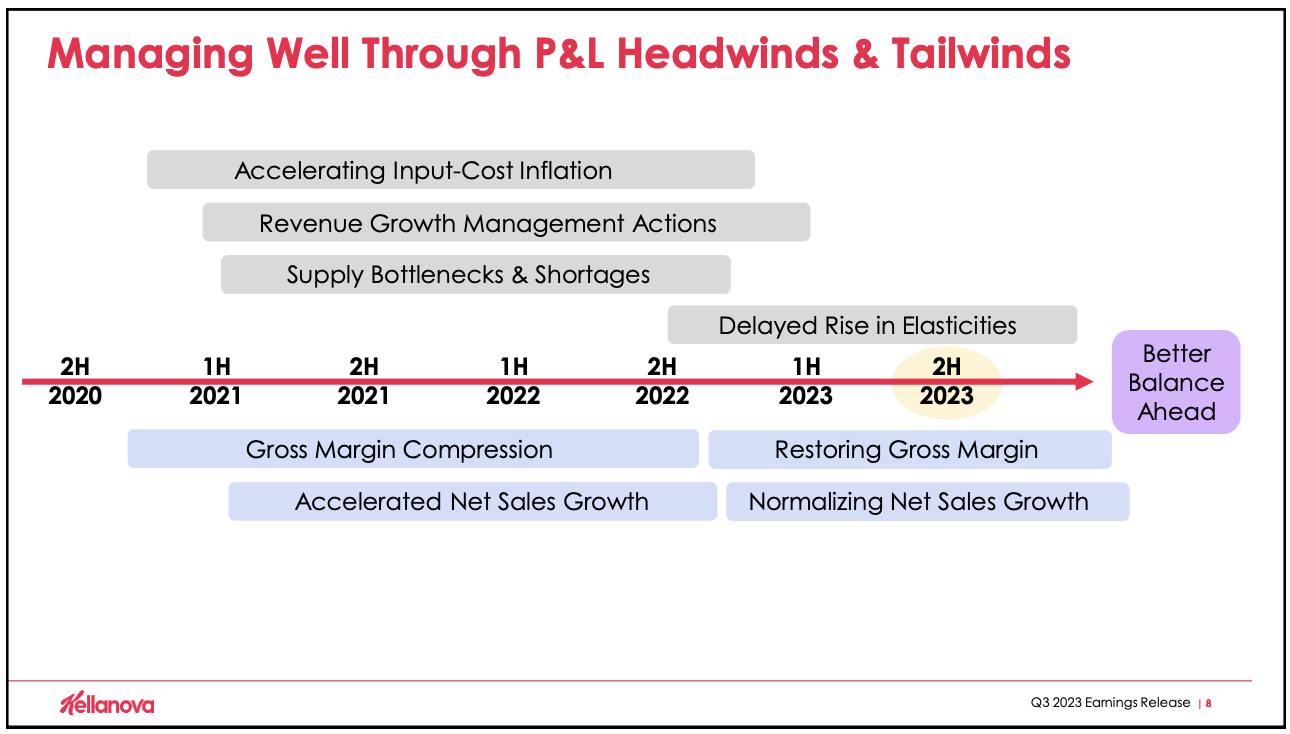

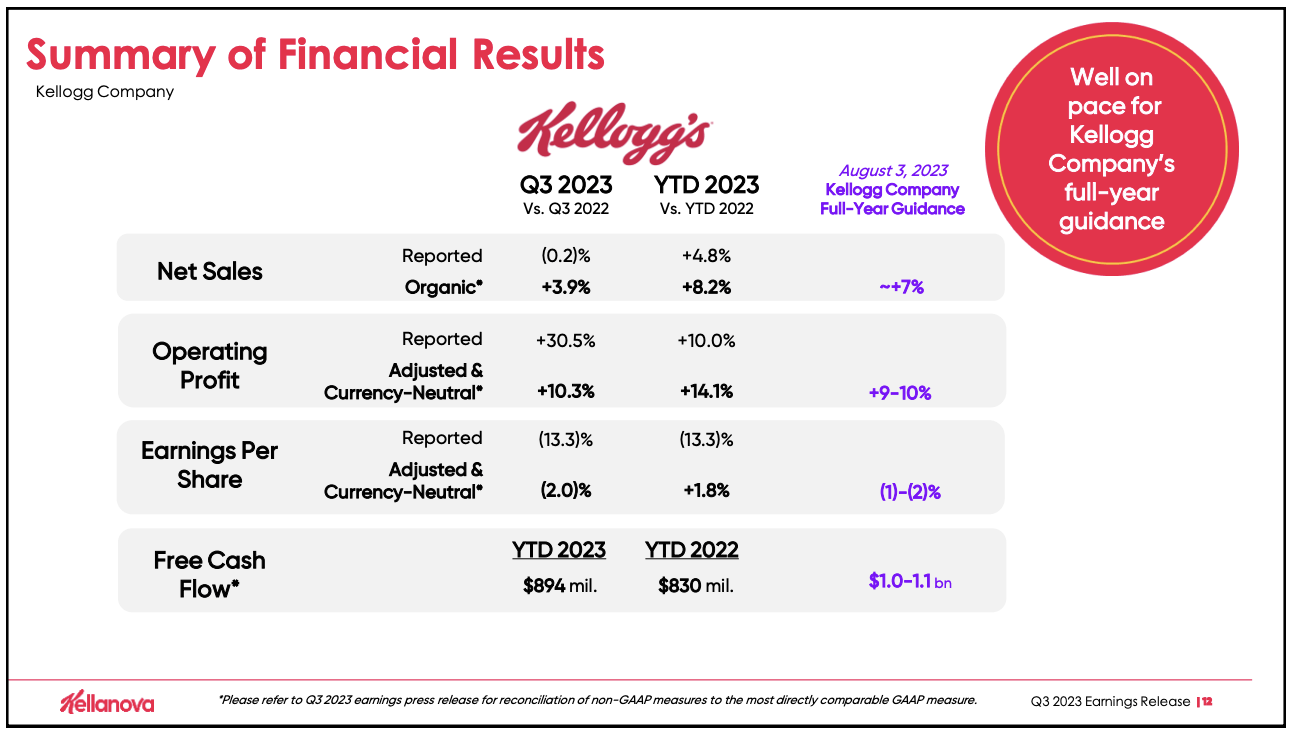

Despite challenges in a financially strained environment, Kellogg Company's third-quarter performance showed sustained organic net sales growth, restored gross profit margins, and above-algorithm growth in operating profit.

After a period of accelerating input cost inflation, supply bottleneck issues, and shortages, the company is now benefiting from easing headwinds, recovering margins, and normalizing sales.

{kind=link}

Kellanova

Having that said, in the third quarter, net sales increased by 4% organically, which translates to 8% growth year-to-date.

Operating profit increased by 10% on an adjusted and currency-neutral basis.

Earnings per share on an adjusted basis decreased by 2% in 3Q23 but increased by 2% year-to-date.

Free cash flow was $894 million, higher than the previous year, putting it on pace toward full-year guidance.

{kind=link}

Kellanova

The big difference between EPS and operating profit was caused by special items.

Reported earnings per share in the third quarter decreased by 13% year on year, due to a non-cash loss on divestiture, incremental up-front costs related to the separation, and higher interest rates and lower pension income, all of which more than offset the benefit of a recovering gross profit margin and a positive swing in mark-to-market. - Kellanova 3Q23 Earnings Release

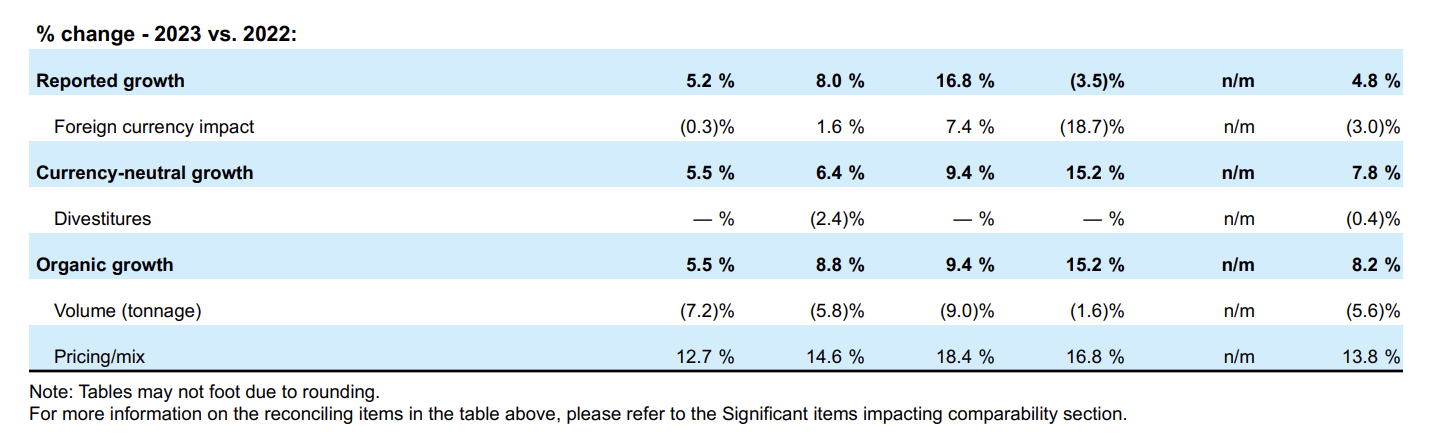

With regard to sales, price elasticities rose globally, impacting volume, but volume performed better than projected.

Price/mix moderated, and the divestiture of the Russian business affected net sales growth by 1%.

Foreign currency translation was a negative 3%, mainly due to the devaluation of the Nigerian naira.

In general, we see that organic volumes were down 5.6%, with pricing/mix gaining 13.8%.

{kind=link}

Kellanova

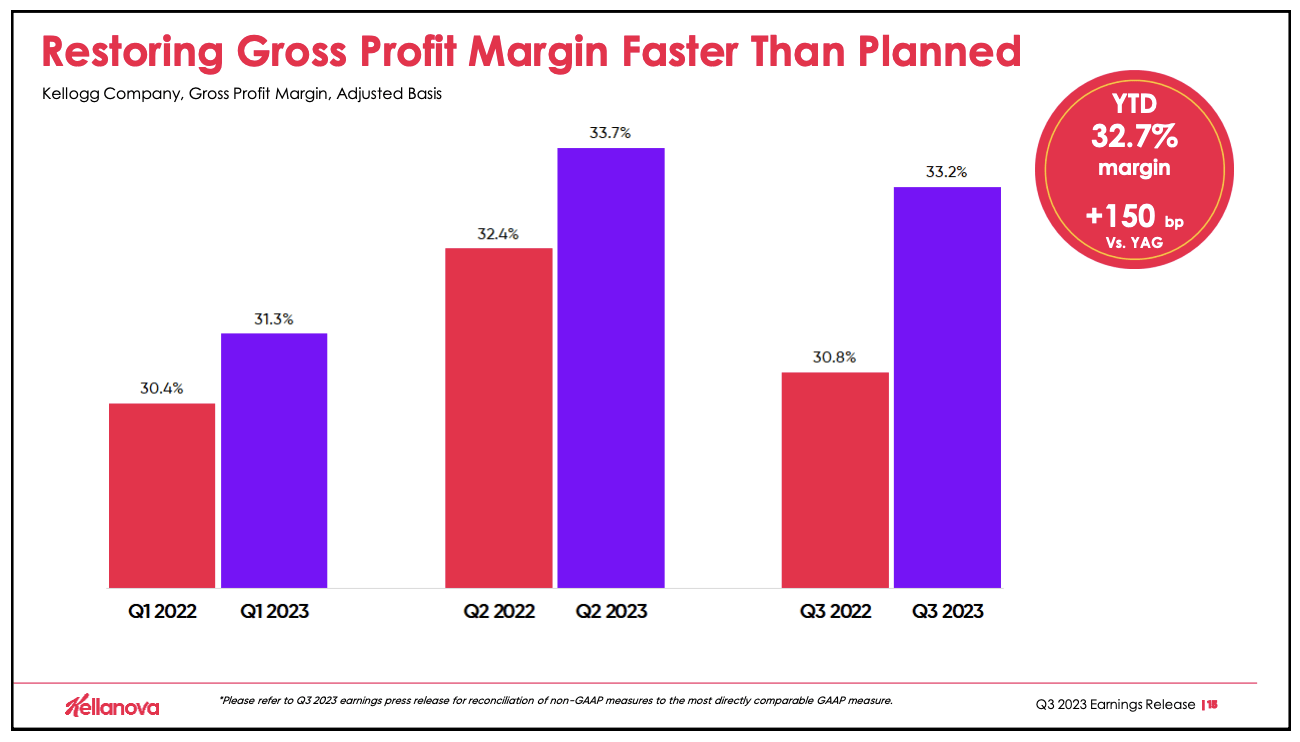

With regard to profitability, despite challenges such as heightened input cost inflation and supply bottlenecks, the focus on growing gross profit dollars has proven successful.

As we can see below, the company has exceeded expectations in restoring gross profit margins, showing year-on-year expansion in each quarter of the year.

Although not yet back to the 2019 pre-pandemic levels, the pace of restoration has surpassed earlier projections.

{kind=link}

Kellanova

The year-to-date margin is a full 100 basis points ahead of the previous year. This improvement is particularly noteworthy considering the divestiture of the Russian business.

As one can imagine, this is also great news for free cash flow.

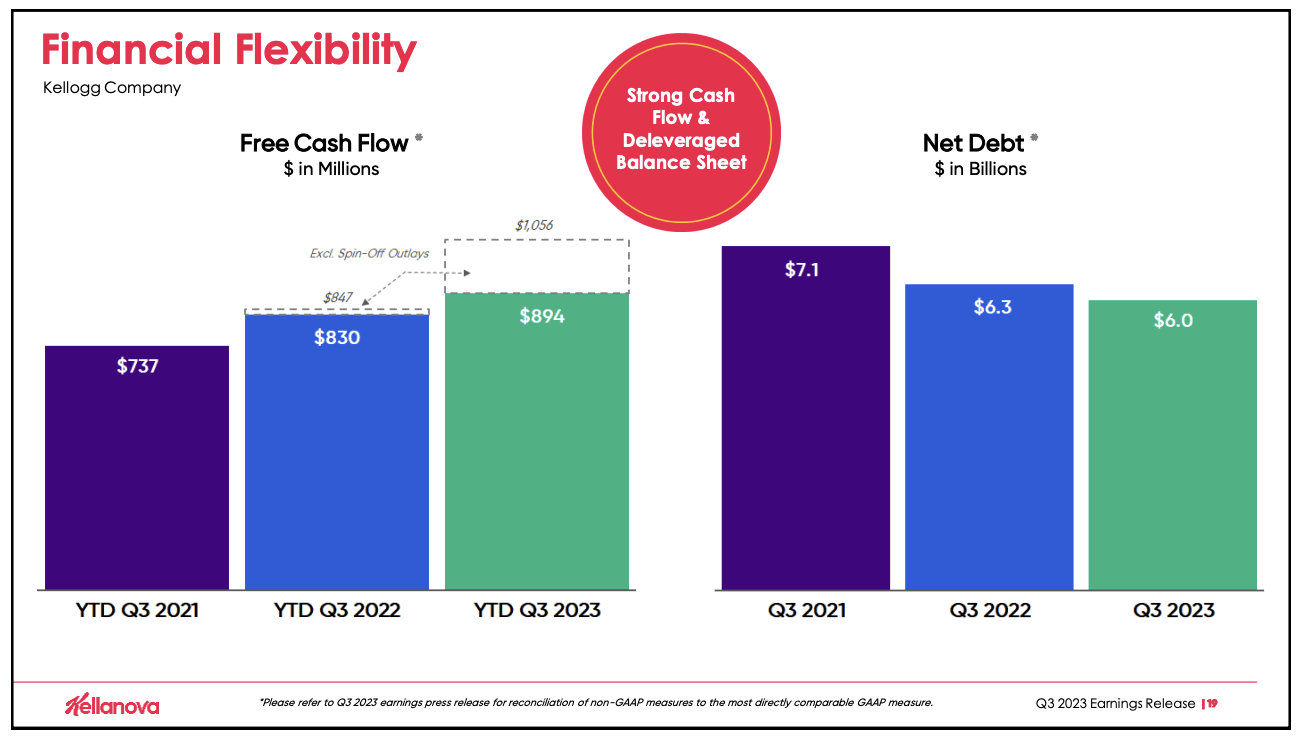

In addition to the encouraging margin trends, Kellogg reported robust free cash flow performance.

Despite one-time cash outlays related to the spin-off and the challenges posed by supply disruptions in the previous year, the year-to-date free cash flow of $894 million exceeded the prior year.

This resilience in cash flow conversion, highlighted on the slide below, positions the company well to achieve its full-year guidance of $1 billion to $1.1 billion.

{kind=link}

Kellanova

If the company is able to achieve this, it could generate a free cash flow yield of 5.6%, which protects its 4.2% dividend yield.

The current dividend is $0.56 per share per quarter. This is down from $0.60 before the spin-off. This is NOT a dividend cut but an adjustment. Investors who hold the spin-off do not lose income.

Ignoring this spin-off, dividend growth has been very poor. Since 2010, the dividend has been hiked by roughly 50%. That sounds like a lot. However, it's not.

For example, a 5% annual compounding dividend growth rate would have resulted in a total growth rate of roughly 90%.

Using my scientific calculator, Kellanova has grown its dividend by 3.2% per year since 2010. That barely beats inflation.

The good news is that the company is in a good spot to accelerate dividends going forward.

- The current dividend is well-protected. A 5.6% 2023E free cash flow yield results in a cash payout ratio of 75%.

- The company is also reducing debt, as we saw in the overview above.

The net debt continued to decrease as the company delivered higher operating profit and EBITDA. This financial strength provides Kellogg with the flexibility to navigate uncertainties and pursue strategic opportunities.

Analysts believe that the company will end next year with $5.3 billion in net debt, which would translate to a 2.4x net leverage ratio. The company has an investment-grade credit rating of BBB.

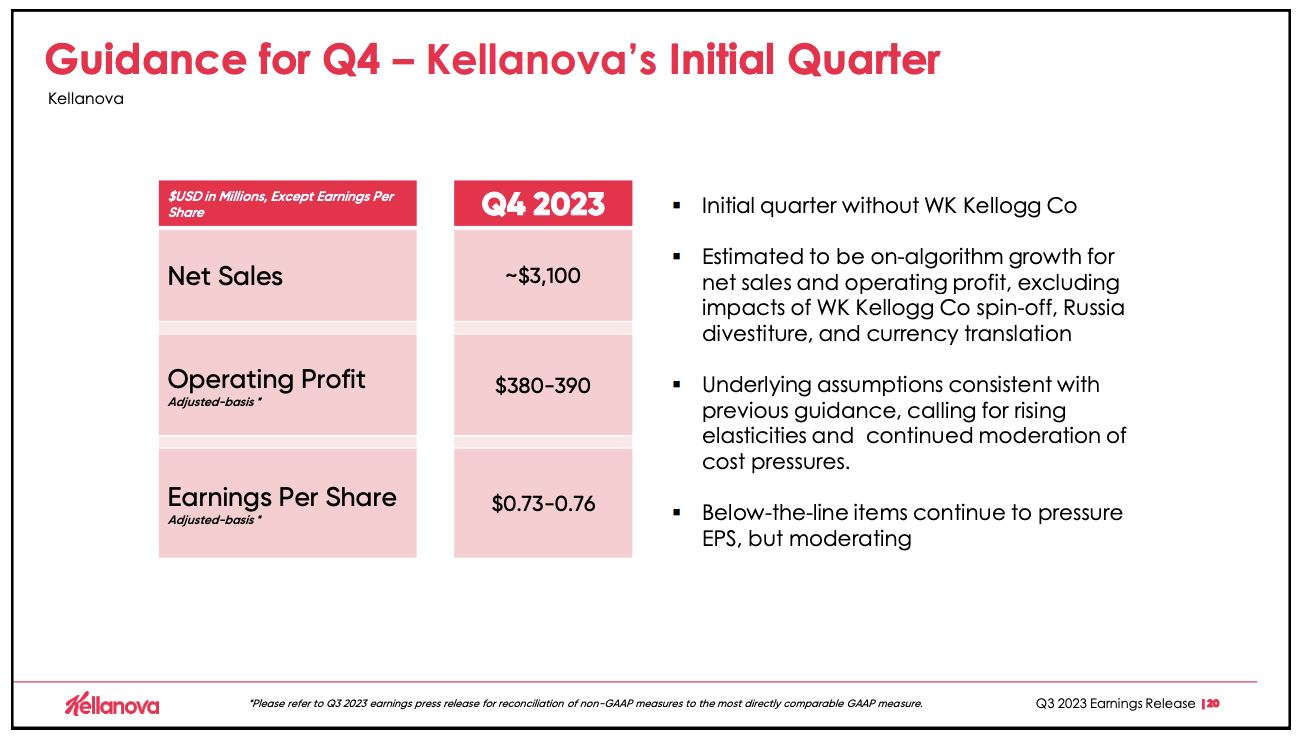

Looking forward, the outlook for Kellanova remains optimistic. The company expects net sales of approximately $3.1 billion in the fourth quarter of 2023.

Despite the divestiture of the Russian business and foreign currency headwinds, the organic net sales growth is projected to align with the long-term target. The restoration of gross profit margin is anticipated to continue, reaching over 33% in the fourth quarter.

{kind=link}

Kellanova

The good news continues as the company's confidence extends into 2024.

Although specific details are not yet provided, Kellogg anticipates sustaining on-algorithm growth in both sales and profit in the upcoming year.

So, how attractive is this 4.2%-yielding stock?

Valuation?

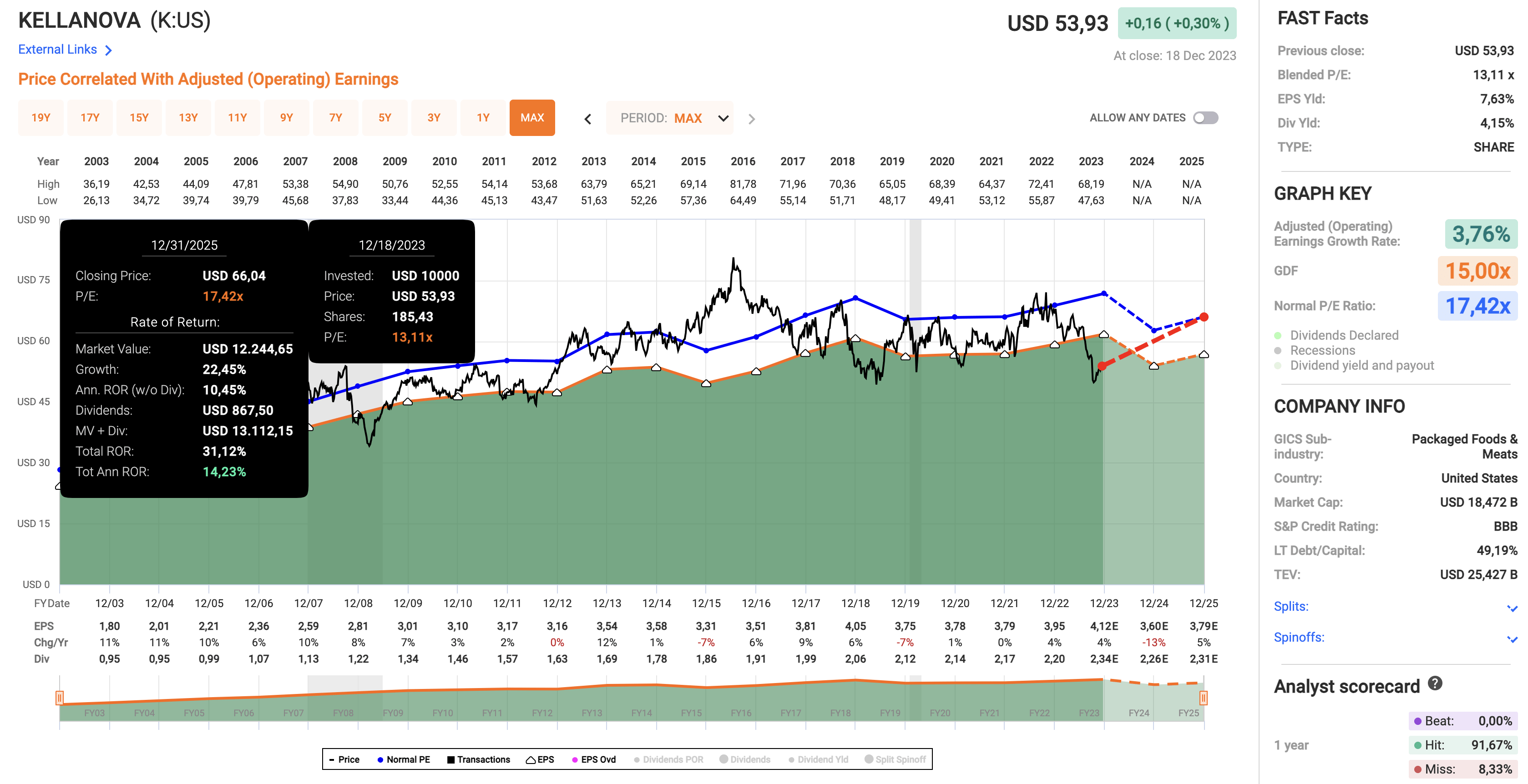

Using the data in the chart below (adjusted for spin-offs):

- Kellanova is trading at a blended P/E ratio of 13.1x.

- Its long-term normalized valuation multiple is 17.4x.

- This year, EPS is expected to grow by 4%, followed by a potential contraction of 13% in 2024. In 2025, the company is expected to grow EPS by 5%.

- Although I believe the company will beat 2024 expectations, I'm using official consensus expectations for the "fair value" calculations.

- Based on a return to its normalized valuation by incorporation of expected EPS growth rates, the company has the theoretical potential to return 14% per year through 2025, including dividends.

- This would imply a fair value of $66, which is 22%.

{kind=link}

FAST Graphs

The current consensus price target is $58, which makes me a bit more bullish than the average analyst.

I will give the stock a Buy rating. However, it needs to be seen if the stock can keep up with its high-flying peers. I expect 2024 to be a major game changer if it is able to grow faster than expected and show that it can quickly recover from the headwinds it faced in prior years.

This includes reporting better volumes!

Takeaway

Shifting focus to snacks and emerging markets, Kellanova boasts robust growth in regions like AMEA and Latin America.

Despite challenges, its third-quarter performance reflects organic net sales growth, restored margins, and resilient cash flow.

With a strategic shift and debt reduction, Kellanova positions itself for potential accelerated dividend growth.

Looking ahead, optimistic projections and a favorable valuation make it a compelling dividend stock.

For further details see:

4%-Yielding Kellanova Could Be A Diamond In The Rough