NLCP - 5 REITs That Likely Will Hike Their Dividends

Summary

- We buy mainly dividend growth REITs.

- We do so because they tend to outperform other REITs.

- I highlight 5 REITs that will likely hike their dividends in 2023.

Recently, we highlighted 5 real estate investment trusts ("REITs") that are likely to cut their dividend in the near future. These are:

- Global Net Lease ( GNL )

- Necessity Retail REIT ( RTL )

- Tanger Factory Outlet ( SKT )

- Omega Healthcare Investors ( OHI )

- Office Properties Income Trust ( OPI ).

These REITs are either overpaying their dividend, overleveraged, poorly managed, or likely to face deteriorating property fundamentals in the near future. I would avoid them because a dividend cut could result in significant capital losses.

Instead, I would of course rather invest in REITs that are likely to grow their cash flow and hike their dividend in coming quarters.

Today, we turn the tables and highlight 5 REITs that are likely to hike their dividend in the near future. We own positions in these at High Yield Landlord and expect them to outperform going forward:

BSR REIT ( BSRTF / HOM.U:CA )

BSR is a small-cap apartment REIT that specializes in rapidly growing Texan markets.

BSR REIT

It hiked its dividend by 3.8% in 2022, and I think that it is likely to soon announce another dividend hike.

This is because:

- Its rent kept growing at 6% in the most recent quarter.

- Its payout ratio is low at just around 61%.

- It has a strong balance with a low 35% LTV and it even has enough liquidity to buy back shares.

Moreover, many of its peers have just recently hiked their dividends.

Mid-America ( MAA ) hiked its dividend by 12% in December.

Camden Property Trust ( CPT ) hiked it by 6.4% in February.

And AvalonBay ( AVB ) just hiked it by 3.8% a few days ago.

I think that BSR will follow their lead and hike as well.

Today, it is already one of the highest-yielding apartment REITs, paying a nearly 4% dividend yield. It yields so much despite having a low payout ratio because it is heavily discounted, trading at a 35% discount to its net asset value.

We think that a dividend hike could help the market sentiment of the company and push its share price a lot higher. Its NAV per share is $22 but it trades at just $14 at the moment.

Essential Properties Realty Trust, Inc. ( EPRT )

EPRT is a net lease REIT just like Realty Income Corporation ( O ).

But EPRT stands out in the net lease sector because:

- It has one of the strongest balance sheets.

- It has one of the lowest dividend payout ratios.

- And it enjoys the fastest cash flow growth rate:

Essential Properties Realty Trust

Therefore, we think that a dividend hike is likely in the near term.

Most net lease REITs are now taking a more cautious approach in 2023, acquiring fewer properties, and it will result in a slowdown in growth.

But even despite the slowdown, EPRT should be able to hike its dividend by ~5% in 2023. Therefore, you would expect EPRT to trade at a higher valuation than its peers, but it is actually priced at a slight discount. Trading at 15x FFO and offering a 4.5% dividend yield, we think that EPRT is likely to outperform the REIT sector ( VNQ ) going forward.

VICI Properties Inc. ( VICI )

VICI is the largest casino net lease REIT in the world.

You may think that now is a bad time to invest in casinos because we may be facing a recession, but here it is important to consider that VICI is just the landlord, not the operator. It earns steady rent checks from 43-year-long leases with steady annual rent hikes.

VICI Properties

It actually hiked its dividend by 11% in 2020 even despite the pandemic, and by another 9% in 2021. The pandemic was the worst possible crisis for a company like VICI and not even that could stop its dividend from growing.

- Today, its payout ratio remains low at 65%.

- Its rent growth is accelerating because it has CPI adjustments in its leases.

- And it is acquiring new assets to supplement its internal growth rate.

All in all, we think that a 5-6% dividend hike is likely in 2023. Combined with its 4.5% dividend yield, investors are likely to earn double-digit total returns with below-average risk.

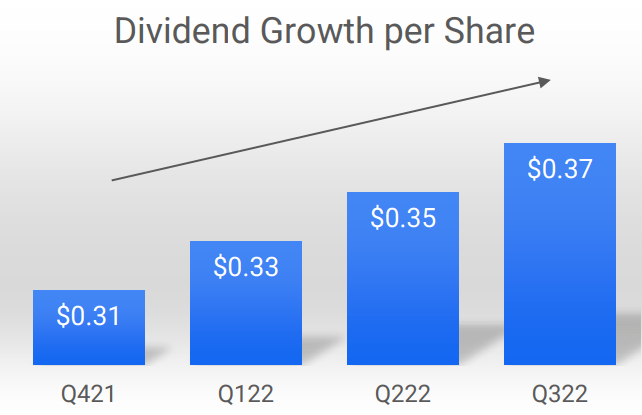

NewLake Capital Partners, Inc. ( NLCP )

NLCP is a REIT that specializes in cannabis cultivation facilities.

It went public in late 2021 and it has since then hiked its dividend in every single quarter.

{kind=link}

Today, the company still has no debt and so it is in a good position to keep acquiring new properties at a high spread over its cost of capital.

It can take debt at a ~6-8% cost and reinvest it in new properties at a ~12-14% cap rate, pocketing the difference.

The company has so much liquidity that it is even buying back shares at the moment.

Therefore, we think that it is likely to continue announcing small dividend hikes in each quarter of 2023.

Today, the company is already priced at a high 8.2% dividend yield so not much is needed to reach double-digit total returns.

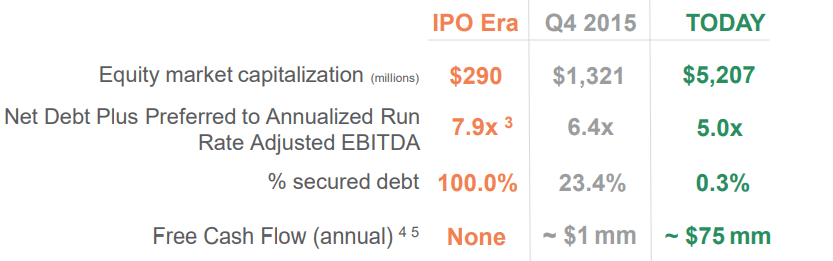

STAG Industrial, Inc. ( STAG )

This last one is the most controversial and many of you will probably disagree with me. STAG is an industrial REIT that has failed to grow its dividend for many years now, but I expect this to finally change in 2023.

STAG Industrial

The reason why STAG didn't grow its dividend isn't that the company is doing poorly. On the contrary, STAG has done very well and even outperformed many of its blue-chip peers like Prologis, Inc. ( PLD ).

STAG Industrial

But STAG kept its dividend low because it was deleveraging its balance sheet and improving the quality of its portfolio. This was dilutive to FFO per share, but it improved the quality of the company and positioned it for a stronger future:

{kind=link}

This took years to complete, but the hard work is now behind. This has left STAG with a strong balance sheet and a low 65% dividend payout ratio even as rents keep growing at a rapid pace.

Therefore, I think that a 5%+ dividend hike is likely in 2023. Such a dividend hike announcement could result in significant upside because STAG is today priced at a large discount to its peers in large parts because of its lack of dividend growth. If this changes, the company's valuation multiple will need to expand closer to that of its peers, unlocking up to 20% upside from here.

Bottom Line

We mostly invest in dividend growth REITs at High Yield Landlord because the dividend hikes often force value appreciation.

If a REIT hikes its dividend by 10%, its share price will also need to rise by 10% for its dividend yield to remain intact. Moreover, we will typically target dividend growth REITs that are undervalued, offering even greater margin of safety and upside potential.

The 5 REITs highlighted in this article are good examples of that.

For further details see:

5 REITs That Likely Will Hike Their Dividends