FTS - 5% Yielding Dividend Aristocrat Bargains You Don't Want To Miss

2023-09-23 07:35:00 ET

Summary

- Rising long-term rates have hammered some sectors and have many investors worried about how companies will finance themselves in the future.

- The rise in rates is primarily due to rising term premiums created by the bond market losing confidence in the Fed, achieving 2% long-term inflation.

- Small companies are at far higher risk of having to refinance at much higher rates. Large dividend blue chips are the safe choice in a higher-rate world.

- A-rated dividend aristocrats are the safest source of high-yield, including these 5 high-yield names you can safely buy today.

- They yield 5.2%, have an A-credit rating, a 36-year dividend growth streak, and are expected to almost quadruple the S&P 500's returns through 2025, while yielding 3X as much.

Interest rates are on many investors' minds as the Fed meets this week to decide on rate policies and provide new economic forecasts.

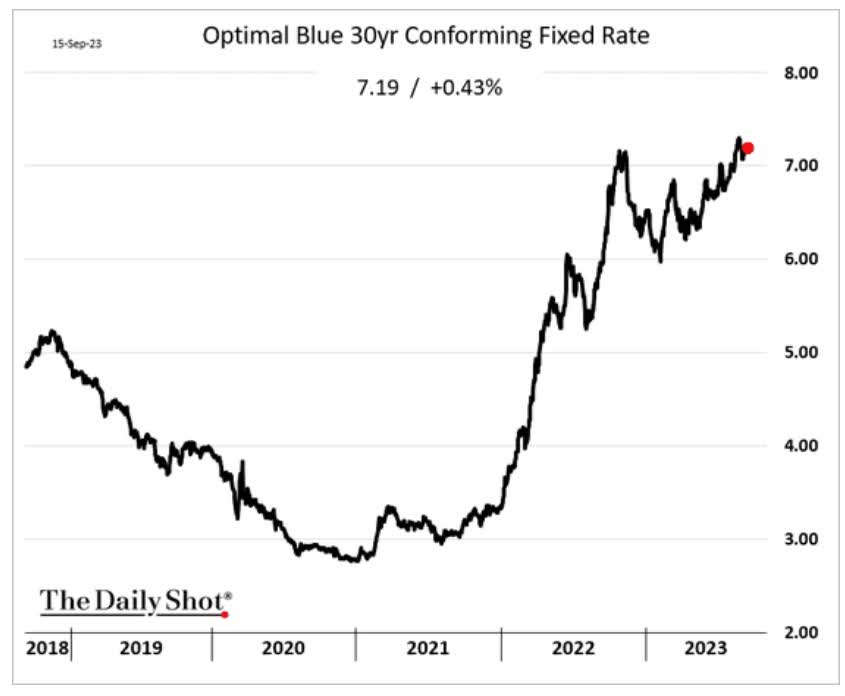

In recent weeks and months, long-term interest rates have soared, helping trigger big corrections in utilities and REITs.

- It's The Best Time In 10 Years To Buy These 5% Yielding Dividend Aristocrats

- It's The Best Time In 10 Years To Buy These Sweet REIT Bargains .

But, of course, rising rates and falling stock prices are not a threat to smart long-term income investors.

Those who buy the bluest of high-yield blue chips, such as A-rated high-yield aristocrats, have nothing to fear from rising rates, and here's why.

Why Are Rates Still Rising When The Fed Isn't Hiking?!

You might wonder if the Fed is done hiking or close to it, then why are long-term interest rates still rising?

{kind=link}

This is due to the term premium, the risk premium bond investors require to own long-term bonds over short-term ones.

For 15 years, the Fed was willing to buy record bonds, and inflation was very stable, resulting in a compressed term premium.

In fact, at the record low rates in 2021, the term premium was about -1%. That's how you got 0.5% 10-year yields 2.6% 30-year mortgage rates, and inflation-adjusted interest rates of -1.5%. Money wasn't just free; companies could borrow at negative rates.

The era of free money, negative rates, and Fed bond buying is over. And that naturally causes the term premium to go up, resetting higher to historically normal levels.

Historically, the inflation-adjusted or real yield on long-term bonds averages about 1.5%. Today, it's 2% and has been climbing for months.

Why The Bond Market Is Losing Faith In The Fed

{kind=link}

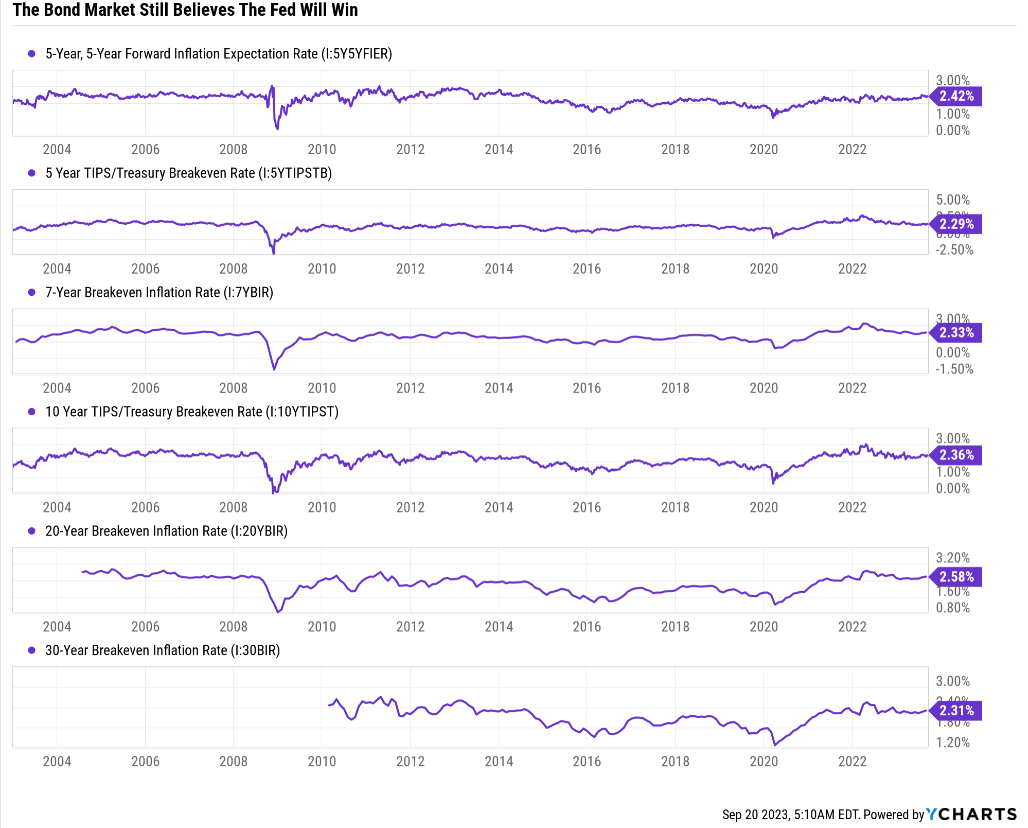

The bond market tells us what it expects long-term inflation to be through various breakeven rates. The Fed's favorite metric is the 5-year, 5-year forward. That means "what the bond market thinks inflation expectations will be in 5 years." So, a 10-year inflation expectation.

Note how it's been climbing steadily since the Pandemic and the Fed's record money printing.

The bond market thinks that over the next 5% to 30 years, 2.3% to 2.6% inflation will be the norm. A return to 2% is now off the table, and here's why.

Why The Fed Is Still Behind The Curve

The Fed keeps saying its "data dependent" and will set rates based on whatever the preponderance of the data says is appropriate to get inflation down to 2% eventually.

{kind=link}

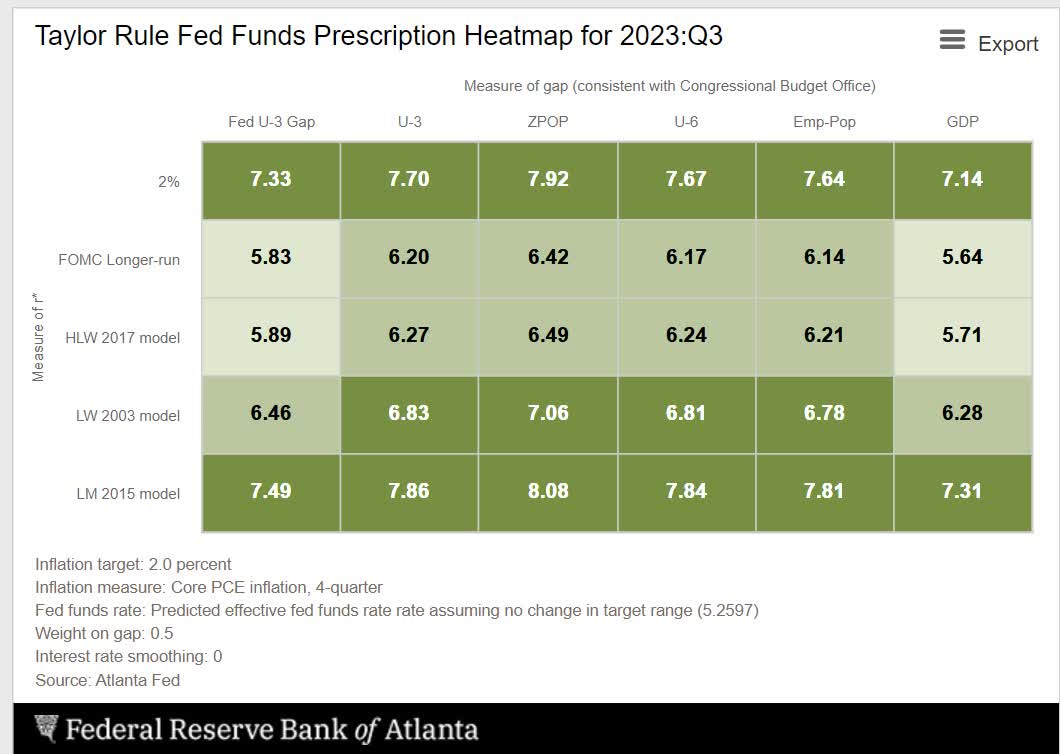

If that were true, the Fed fund rate would be 7% to 8% today, based on the Fed's models.

Other models say the Fed should be at 5.5% to 8%, but none say the Fed should be at 5.25% and sitting tight rather than hiking.

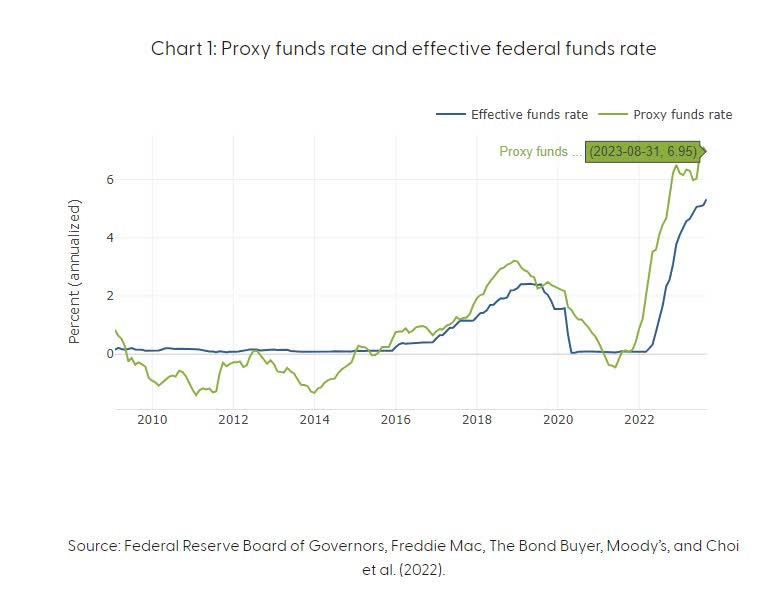

OK, but what about QT or quantitative tightening? The Fed is reverse money printing at a rate of $90 billion per month, and the U.S. Treasury is selling $1.5 trillion in bonds this year, which also sucks money out of the economy.

{kind=link}

The San Francisco Fed estimates that factoring in QT, bond selling from the Treasury, and the regional banking crisis, the real Fed funds rate is 7%, just 0.25% to 1% below what the Fed's models say is appropriate today.

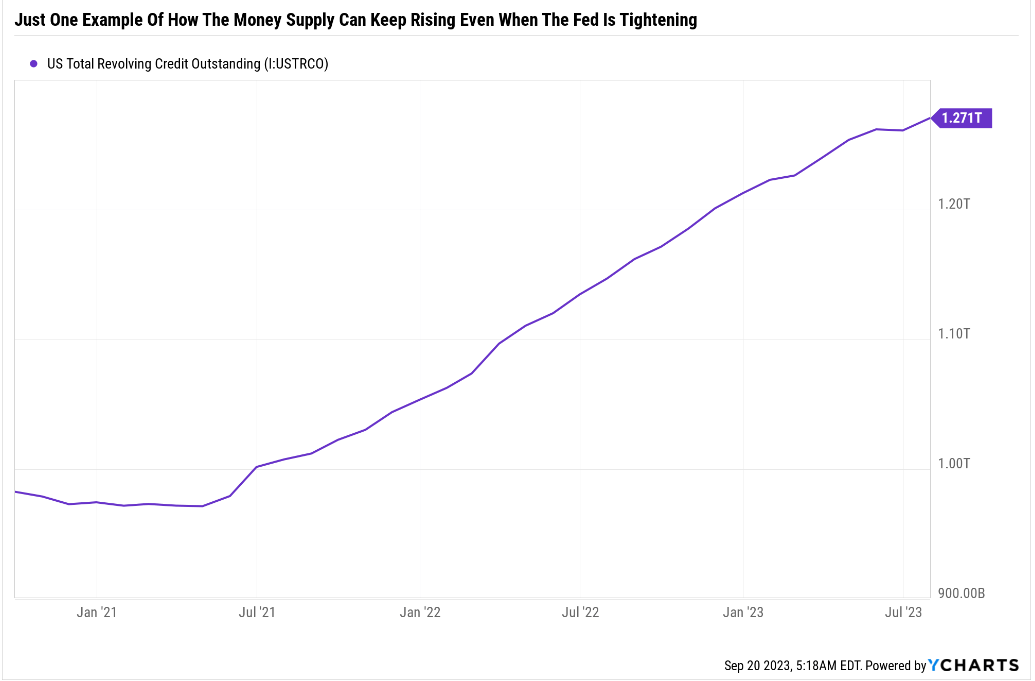

So how on earth could inflation not be coming down fast? Because 85% of the money supply is controlled by bank lending.

When the bank gives you a credit card, and you spend money on it, that is money your bank prints via credit.

{kind=link}

There are now 1 trillion credit cards in the U.S., averaging 3 per person or 4 per adult.

Despite record 22% interest rates, consumers are still borrowing because the job market is strong and, so far, very resilient. There is still some excess savings from the Pandemic (runs out by the end of the year per economist consensus) and some revenge spending.

As a result, we see an economy that just won't quit and inflation that won't return to 2%.

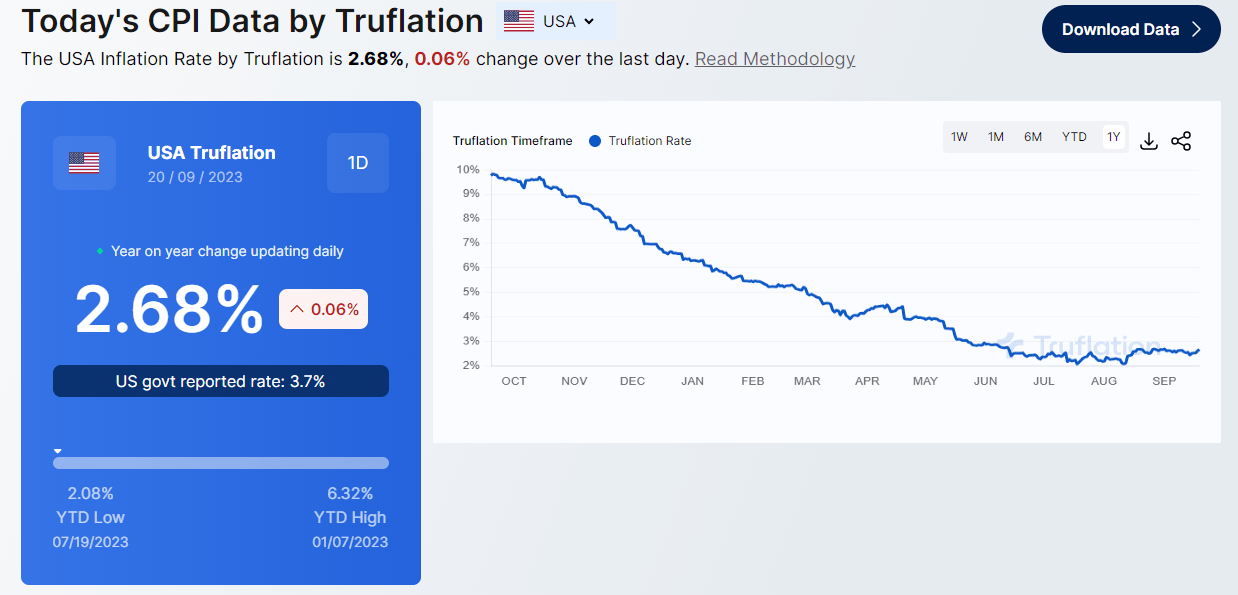

10 Million Data Points Updated Daily

{kind=link}

The Fed doesn't dare officially mention this model, which is available for free and far more accurate than any monthly inflation report from the government.

- Inflation is now just above the bond market's upper end of inflation expectations.

Imagine how it would look if the Fed suddenly switched metrics that made it look better. The Fed has to stick to core PCE, its official inflation metric since 2012.

{kind=link}

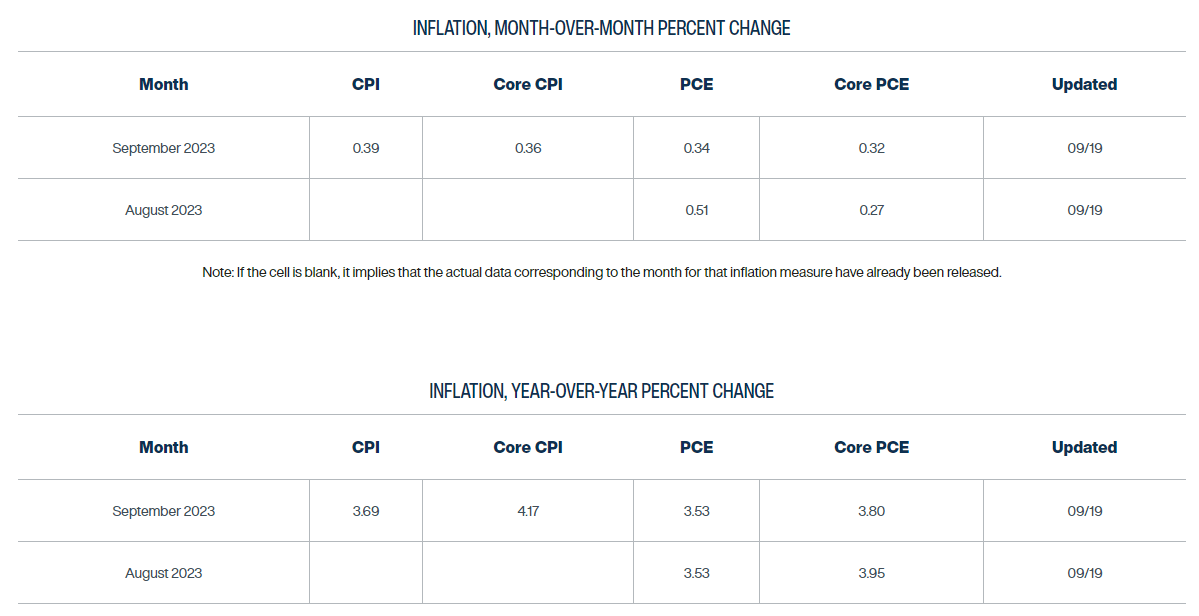

Inflation reports lag by one month, so those September numbers are what the Cleveland Fed's daily inflation model predicts in mid-October.

- 3.7% YOY on CPI (headline inflation), same as now

- 4.2% YOY on core CPI (4.4% today)

- 3.8% core PCE YOY (official metric)

- 3.9% core PCE YOY (annualizing month-over-month).

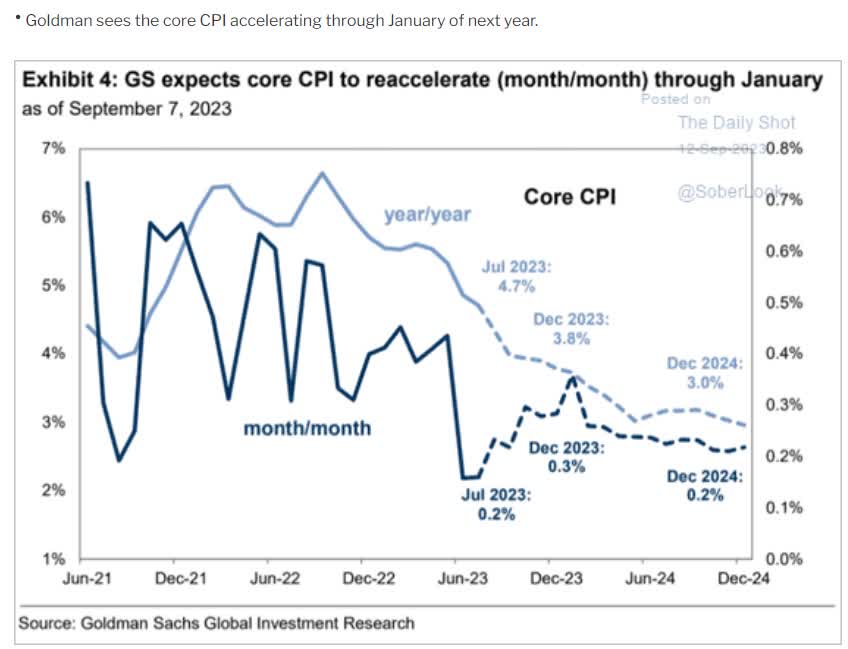

The Fed's official inflation gauge, which it has repeatedly vowed to bring back to 2%, is stuck at 2X its official metric, and Goldman thinks that CPI will accelerate through January.

{kind=link}

In fact, by the end of next year, Goldman thinks headline inflation will still be 3%.

The bond market says the Fed will throw in the towel, unofficially changing the goalpost and declaring victory around 2.3% to 2.6%.

{kind=link}

What does the bond futures market think? The billions that professional money managers are using to hedge interest rate risk?

The bond market says the Fed is done hiking. Are rates high enough? Nope. Does the Fed care about 2% inflation? Nope. 2.5% or so is good enough, and that's why the bond market is now only estimating a 96% chance of a recession in 2024.

- down from 100% since October of 2022.

The Fed isn't willing to do whatever it takes to get to 2% inflation, at least according to the bond market.

There is still a 96% chance of recession next year, with the bond market saying it will begin by June or July.

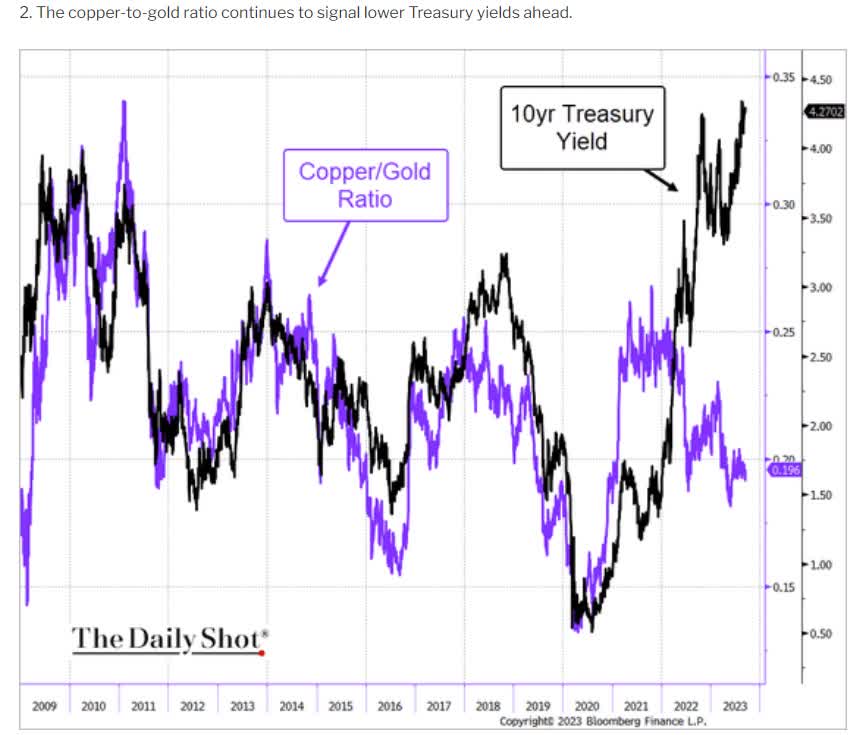

So why are long-term rates still rising?

{kind=link}

Shouldn't the 10-year yield (US10Y) be 1.75% and 30-year yields 2% right now? According to the copper/gold ratio, yes.

{kind=link}

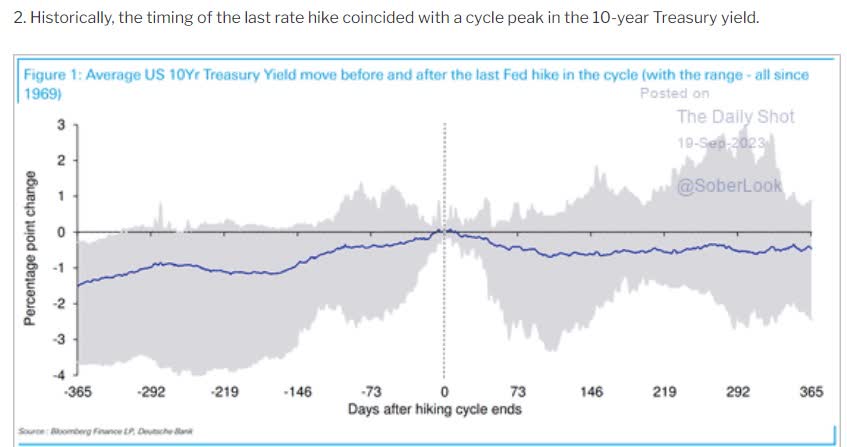

Doesn't the 10-year yield historically peak right when the Fed is done hiking, which the bond market says happened in July?

Yes, but note that the longest lag to peak 10-year yield was about 300 days or ten months.

- long rates should peak no later than November of 2024

- unless we are setting a new record lag this time

- created by historic and unprecedented events like $9 trillion in stimulus, super fast rate hikes, and a Fed that lost its nerve at the last minute.

There you have it. My best-educated guess about why the term premium is rising is based on the bond market becoming uncertain about the Fed's intentions.

When the Fed was hiking 0.75% every six weeks, the bond market was very confident we would soon be in recession and inflation would soon be back to 2%.

There was no need for a steadily rising term premium. Not when the Fed was so obviously going to prevent this.

{kind=link}

But now that the Fed is suddenly going soft? Suddenly, the Fed is willing to hold rates higher but not high enough, and longer but possibly not long enough?

Now, the bond market thinks the Fed might allow 2.6% inflation (what it is now) for the next 20 years. Maybe the Fed will allow for 3% inflation or even 4%?

When the bond market no longer trusts the Fed's 2% promise, it will demand a higher term premium.

Even if the Fed holds rates at current levels for the next year, some economists think the 10-year yield could rise to 4.5%, 5%, or even 5.5% (Bill Ackman is hedging against this doomsday scenario).

Yes, some intelligent analysts, even Billionaires, think that long rates could rise by about 1.2% more before they finally peak.

Is that the most likely outcome? Not. Is it a zero risk? Nope.

And that's where A-rated high-yield dividend aristocrats come in.

Why A-Rated High-Yield Aristocrats Are The Ultimate High-Rate Long-Term Investment

If long rates do soar 1.2% more in the next year, the best investment of the following year would be 3X short-long TLT ( TMV ).

But what if you're a long-term income investor not looking to make a speculative "doomsday scenario" trade? What if you want to earn an excellent, safe, growing yield and let company management worry about interest rates?

{kind=link}

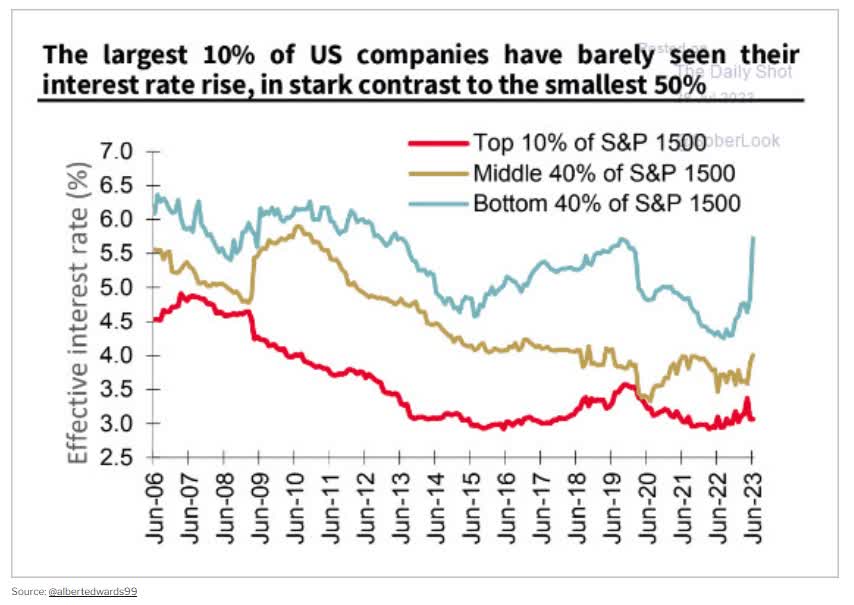

Small companies are a lot more sensitive to rising long-term rates. They have naturally higher capital costs because they don't have diversified cash flow streams, strong credit ratings, and the ability to sell billions in bonds.

{kind=link}

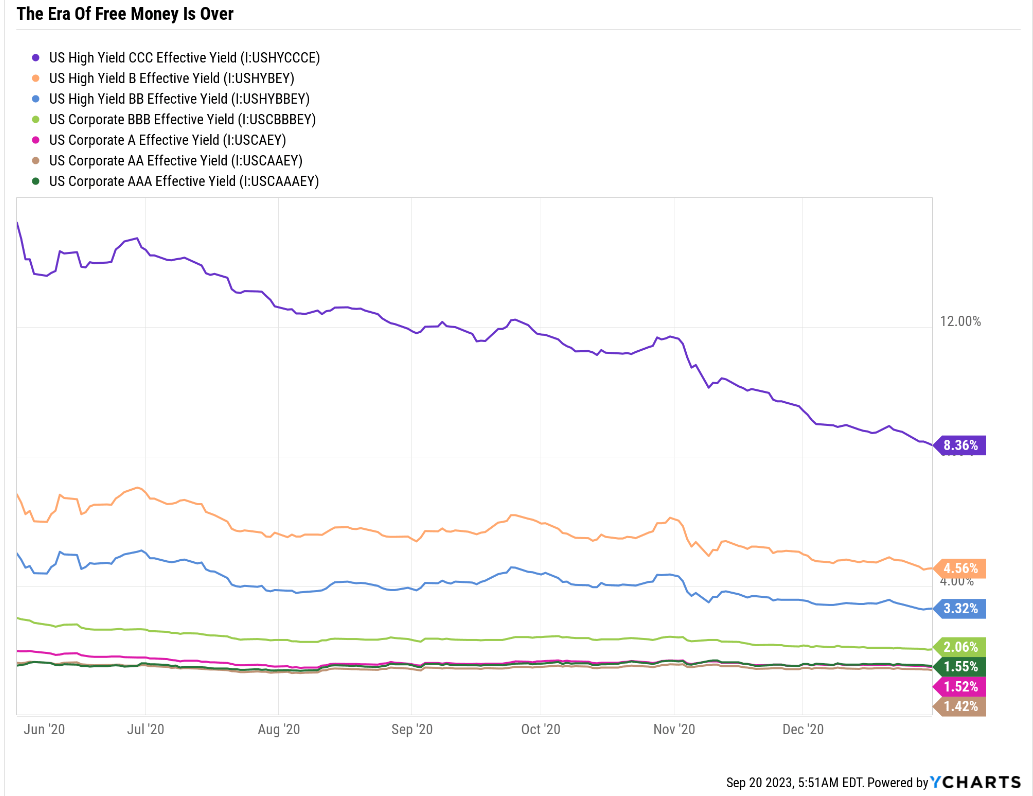

After the Pandemic, the Fed bought so many bonds, and stimulus was so plentiful that even CCC rated companies could borrow at 8.4%.

S&P

Yes, companies with a 59% chance of bankruptcy could borrow at single digits, while junk bond BB-rated companies could borrow at 2.1%, just 0.7% higher than AAA-rated titans like JNJ and MSFT.

That was insanity, and now we're back to reality. Money has a cost, and zombie companies that can't earn a sufficient profit don't deserve to survive.

Stronger, healthier, and better-run companies will absorb their resources and customers. It's the creative destruction of capitalism at work.

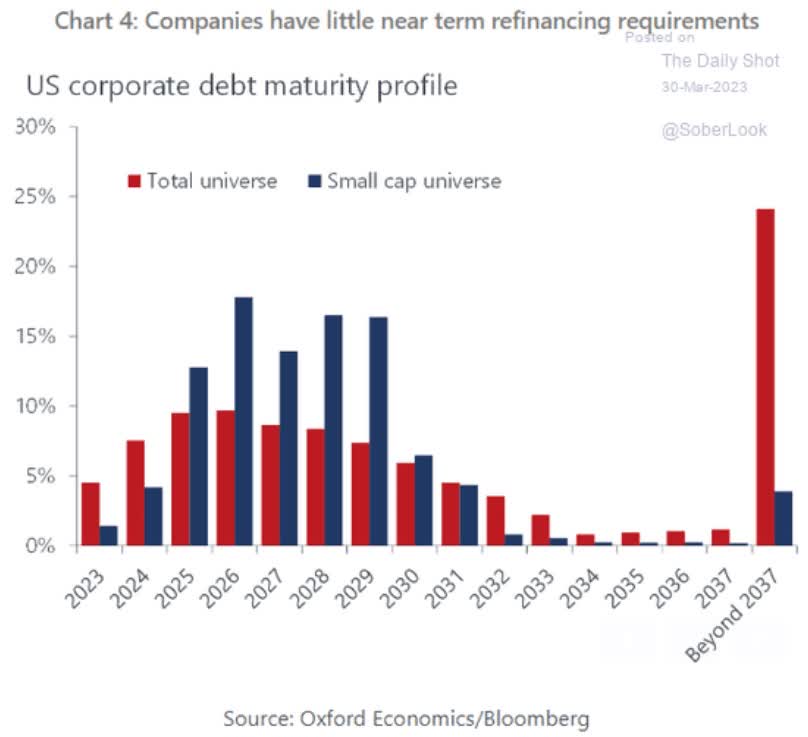

But you don't want to own those weak companies drowning in debt that needs to be refinanced at today's much higher rates.

{kind=link}

Imagine a scenario in which the Fed doesn't hike more, inflation drifts lower slowly or stays at 3%, and we avoid recession.

The long end of the yield curve drifts higher to 4.5% or even 5%. And then the refinancing cliff hits.

Small companies would have to refinance almost all of their debt, not at 2% as they borrowed in 2020, but at 6% to 7%.

Over several years, savvy managers will see the crisis coming and deleverage.

But some zombie companies will get crushed by a tripling of interest costs.

The same is true even for some large companies. You don't want to be overleveraged and suddenly have to pay 2X or 3X more for interest.

And income investors certainly don't want to own a high-yield company whose dividend is likely to be the first thing cut to pay those higher interest rates.

But that's where A-rated aristocrats come in.

How To Find The Best A-Rated High-Yield Aristocrat Buys

The Dividend Kings ZEUS Research Terminal is the screening tool I use for every article.

- 504 of the world's best blue-chips

- including every dividend aristocrat, champion, king, and foreign aristocrat

- and future aristocrats

- and Ultra SWANs (mostly wide moat aristocrats)

- and 40 of the world's best growth stocks (to turbocharger income growth).

| Step |

| Screening Criteria |

| Companies Remaining |

| % Of Master List |

| 1 |

| "lists" and "Dividend champions" |

| 135 |

| 27.00% |

| 2 |

| Non-Speculative (No Turnaround Stocks, investment grade) |

| 116 |

| 23.20% |

| 3 |

| BHS Rating "reasonable buy, good buy, strong buy, very strong buy, ultra value buy" |

| 34 |

| 6.80% |

| 4 |

| A-Credit Rating Or Higher |

| 30 |

| 6.00% |

| 5 |

| Sort By Yield |

| 0.00% |

| 6 |

| Top 5 Dividend Aristocrats |

| 5 |

| 1.00% |

| Total Time |

| 1 minute |

That's how I could screen 504 companies down to 5; for the best A-rated high-yield dividend aristocrats, you can safely buy in a higher for longer environment.

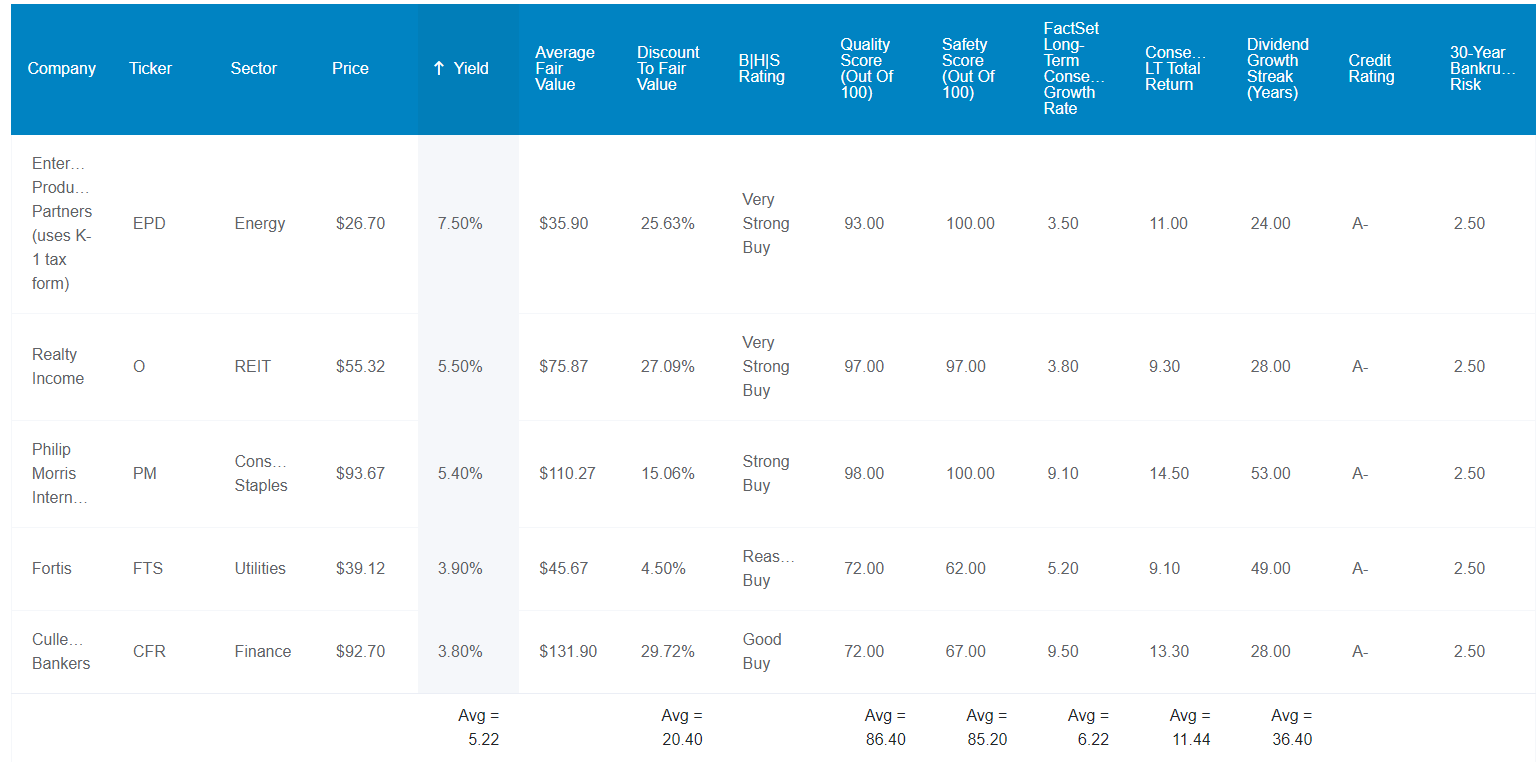

The 5 Best High-Yield A-Rated Dividend Aristocrat Buys

{kind=link}

I've linked to articles about each company's investment thesis and risk profile.

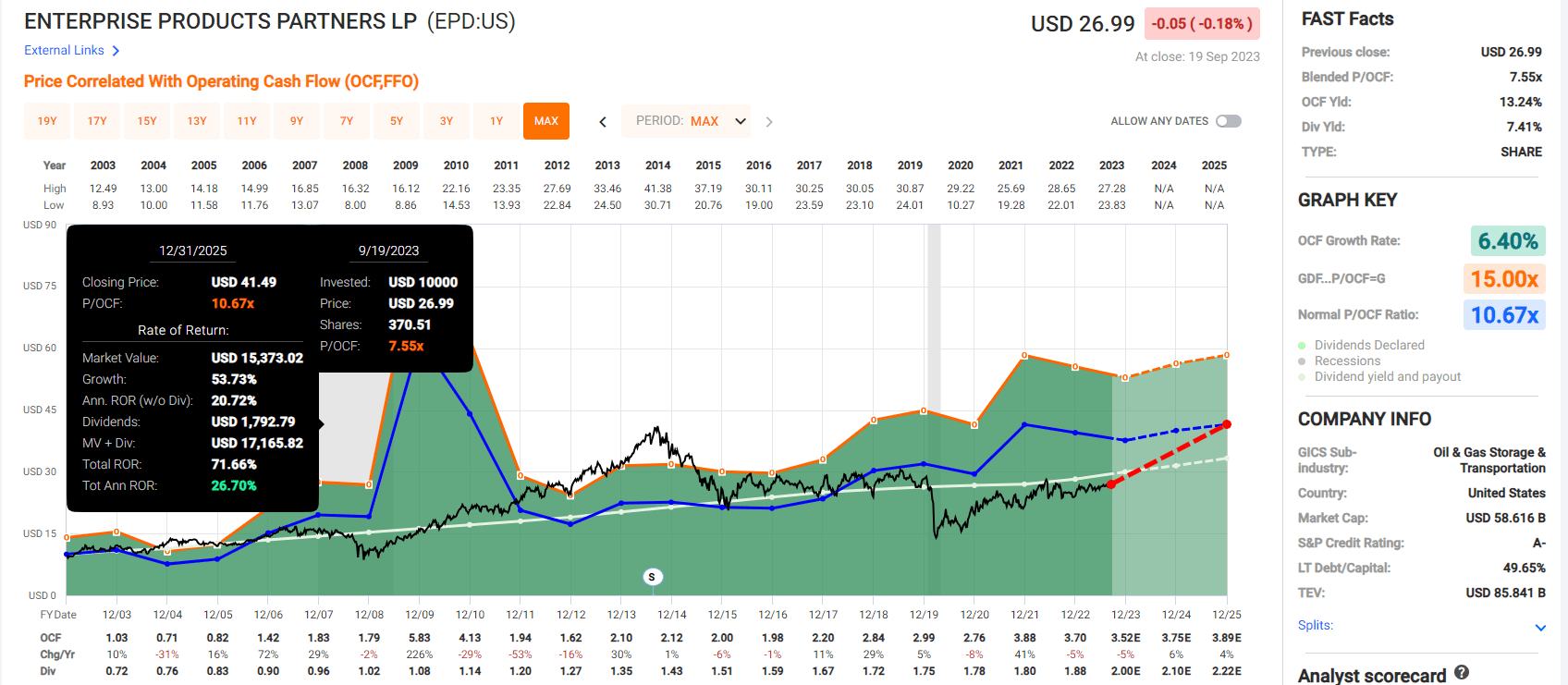

- Enterprise Products Partners ( EPD ) - uses K1 tax form

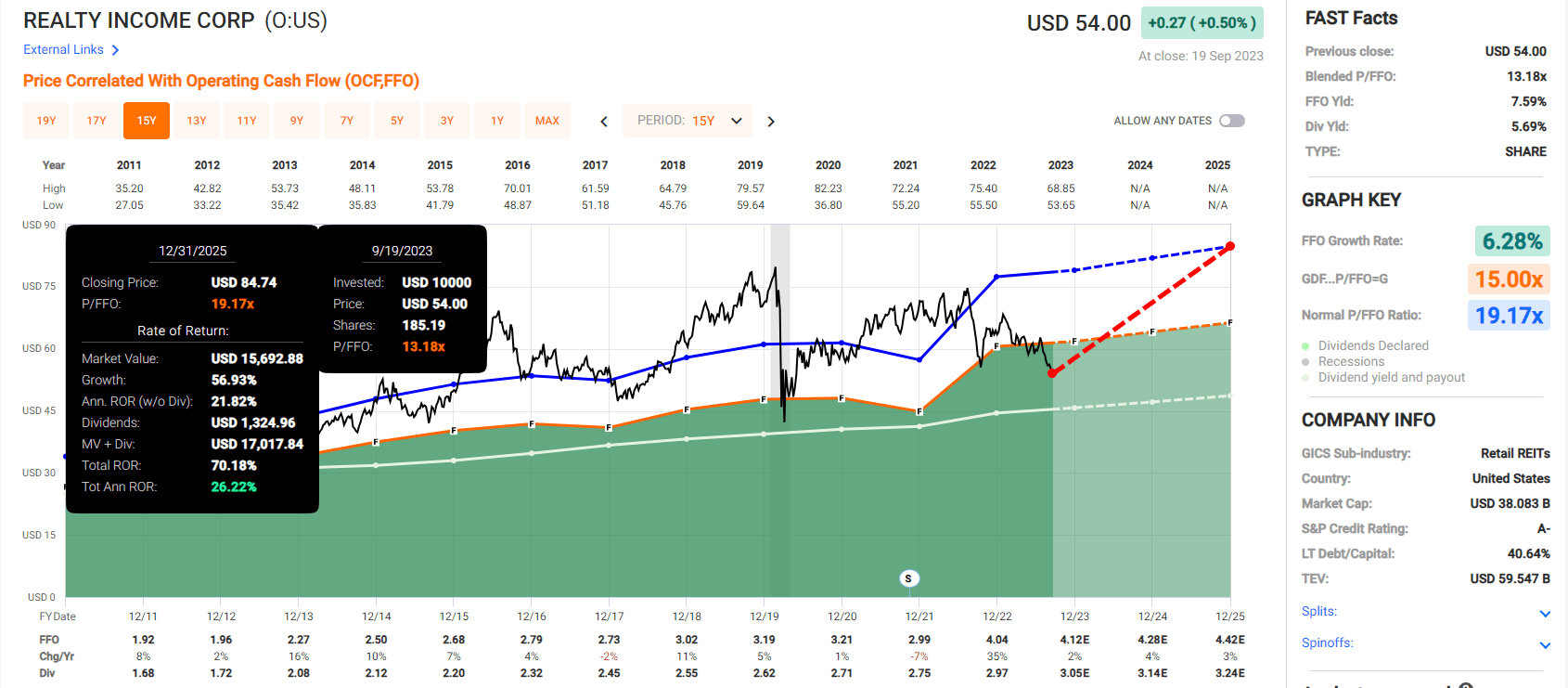

- Realty Income ( O )

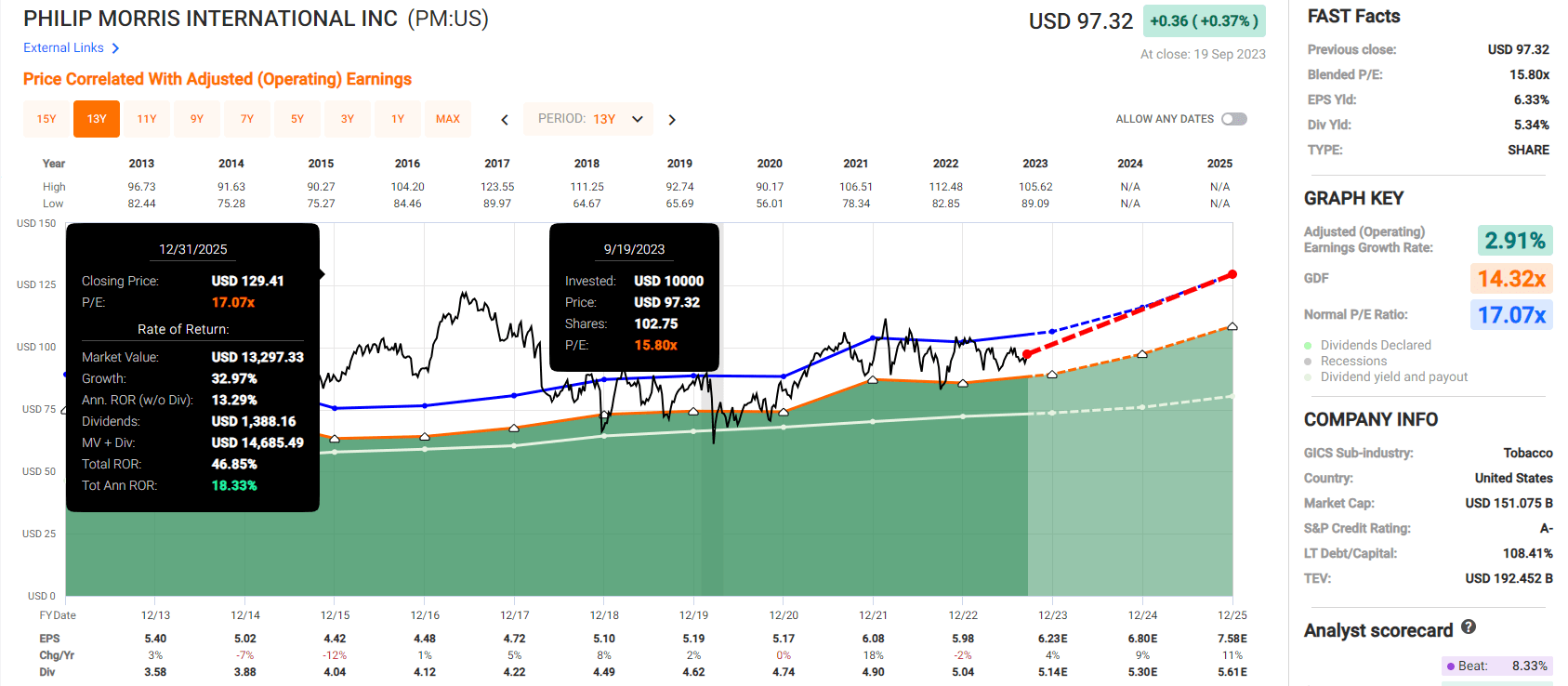

- Philip Morris International ( PM )

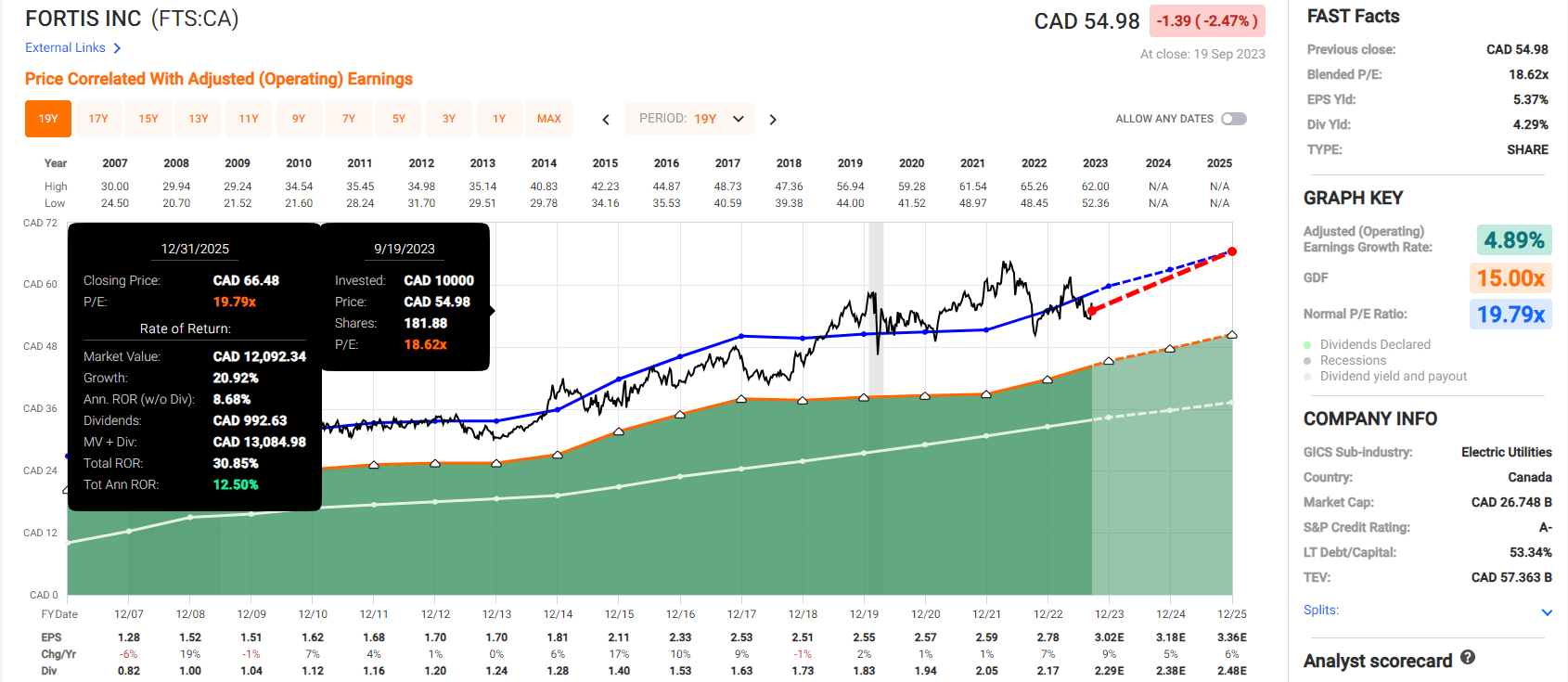

- Fortis ( FTS )

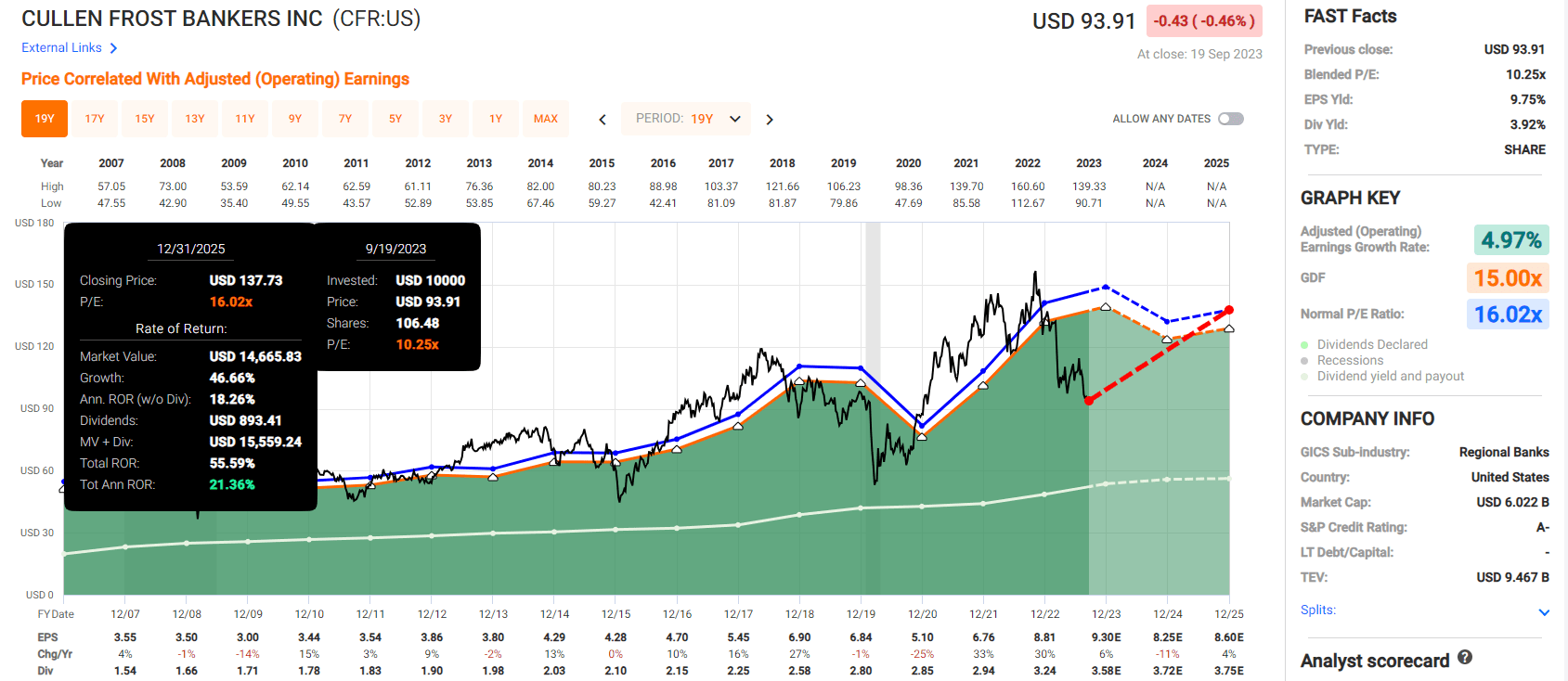

- Cullen/Frost Bankers ( CFR ).

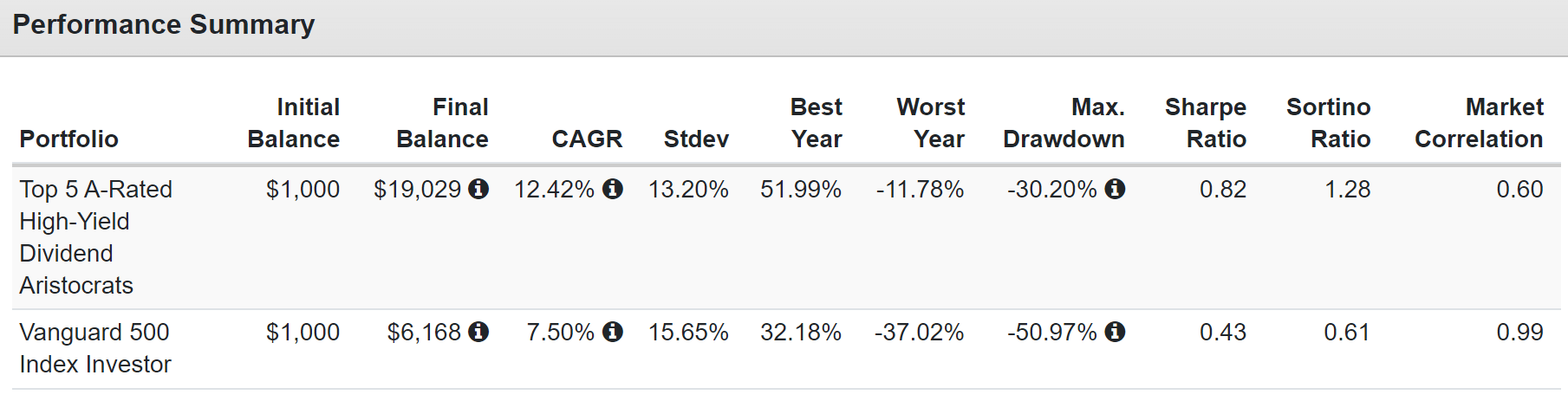

Fundamental Summary

- Yield: 5.2%

- dividend safety: 85% (1.75% risk of a cut)

- overall quality: 86% 13/13 Ultra SWAN

- average credit rating: A- stable (2.5% 30-year bankruptcy risk)

- average dividend growth streak: 36 years (since 1987)

- growth consensus: 6.2%

- LT total return potential consensus: 11.4%

- valuation: 20% discount

- DK rating: potential strong buy

- 10-year valuation boost: 2.3% per year

- 10-year consensus total return potential: 5.2% yield + 6.2% growth + 2.3% valuation boost = 13.7% CAGR vs 8.7% S&P 500

- 10-year consensus total return potential: 261% vs 130% S&P 500.

How does 3X the S&P 500's yield today and twice the 10-year total return potential sound? In an A-rated dividend aristocrat package?

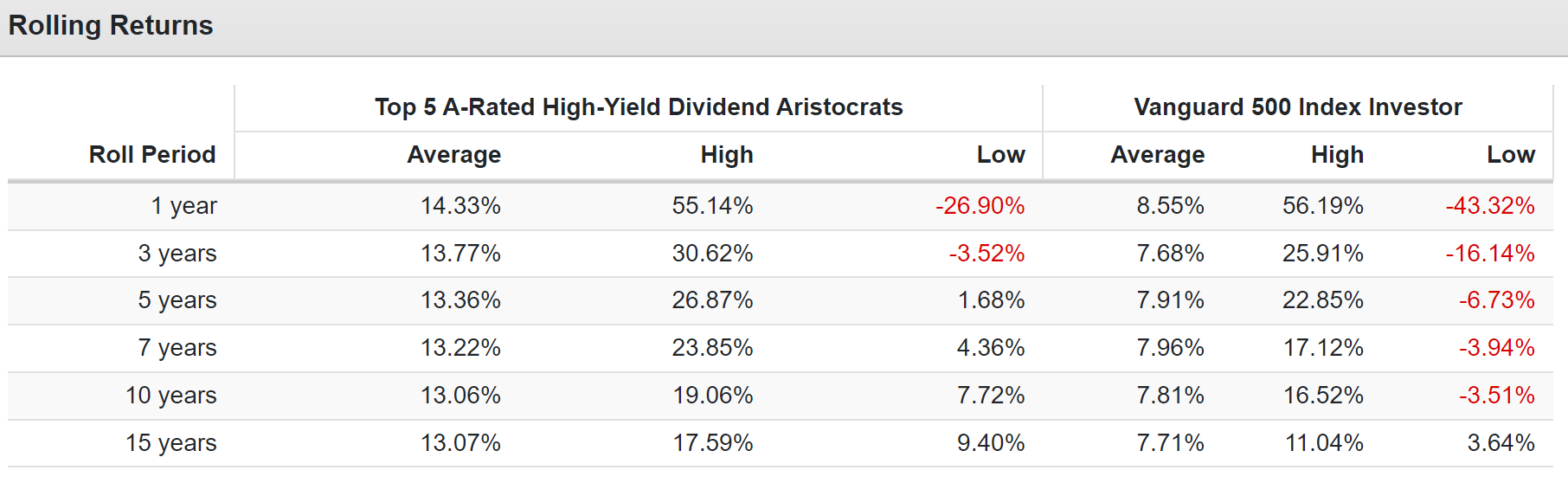

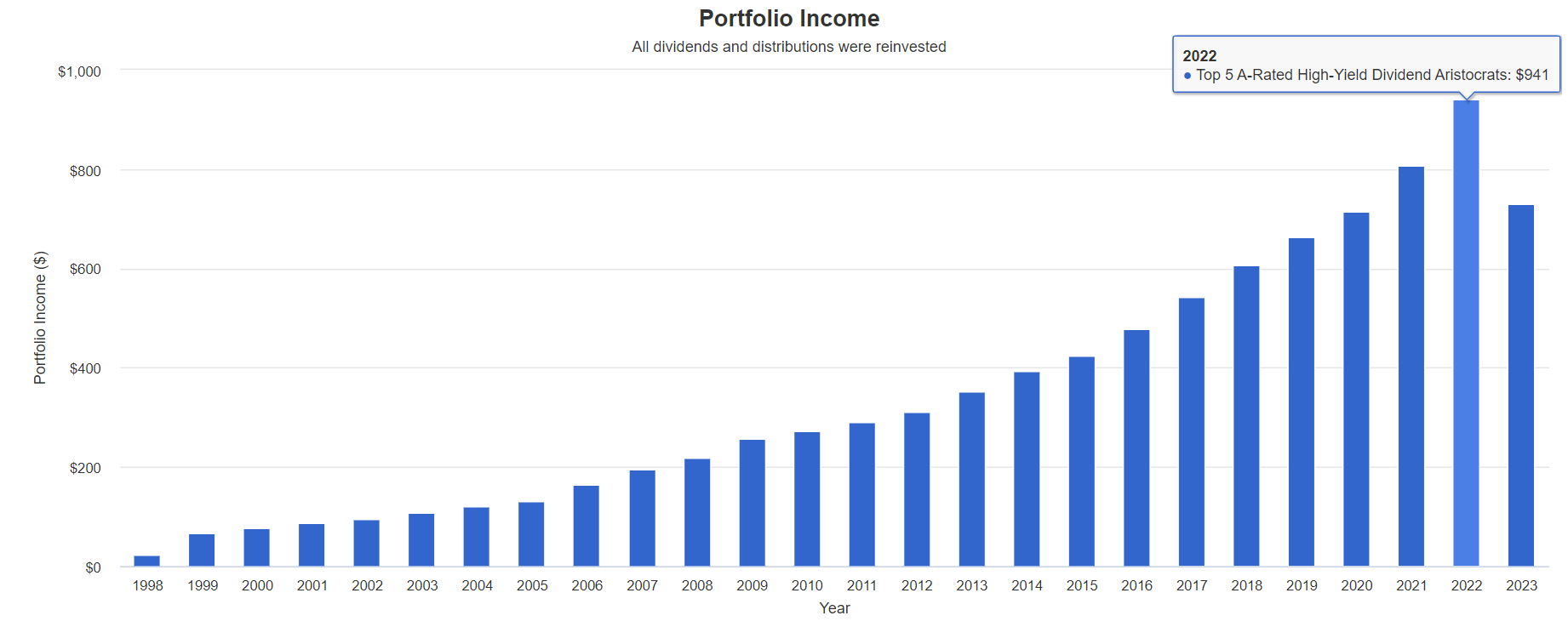

Historical Returns Since 1998

(Source: Portfolio Visualizer Premium) (Source: Portfolio Visualizer Premium) (Source: Portfolio Visualizer Premium)

{kind=link}

{kind=link}

{kind=link}

12.2% annual dividend growth for 23 years.

- 6.7% yield in 1999 (tech bubble value bear market)

- 94.1% yield on cost in 2022

- 50% inflation-adjusted yield on cost.

2025 Consensus Total Return Potential

- if and only if these companies grow as analysts expect

- and return to historical market-determined fair value

- these are the returns you will make including dividends

Enterprise Products Partners

{kind=link}

Realty Income

{kind=link}

Philip Morris International

{kind=link}

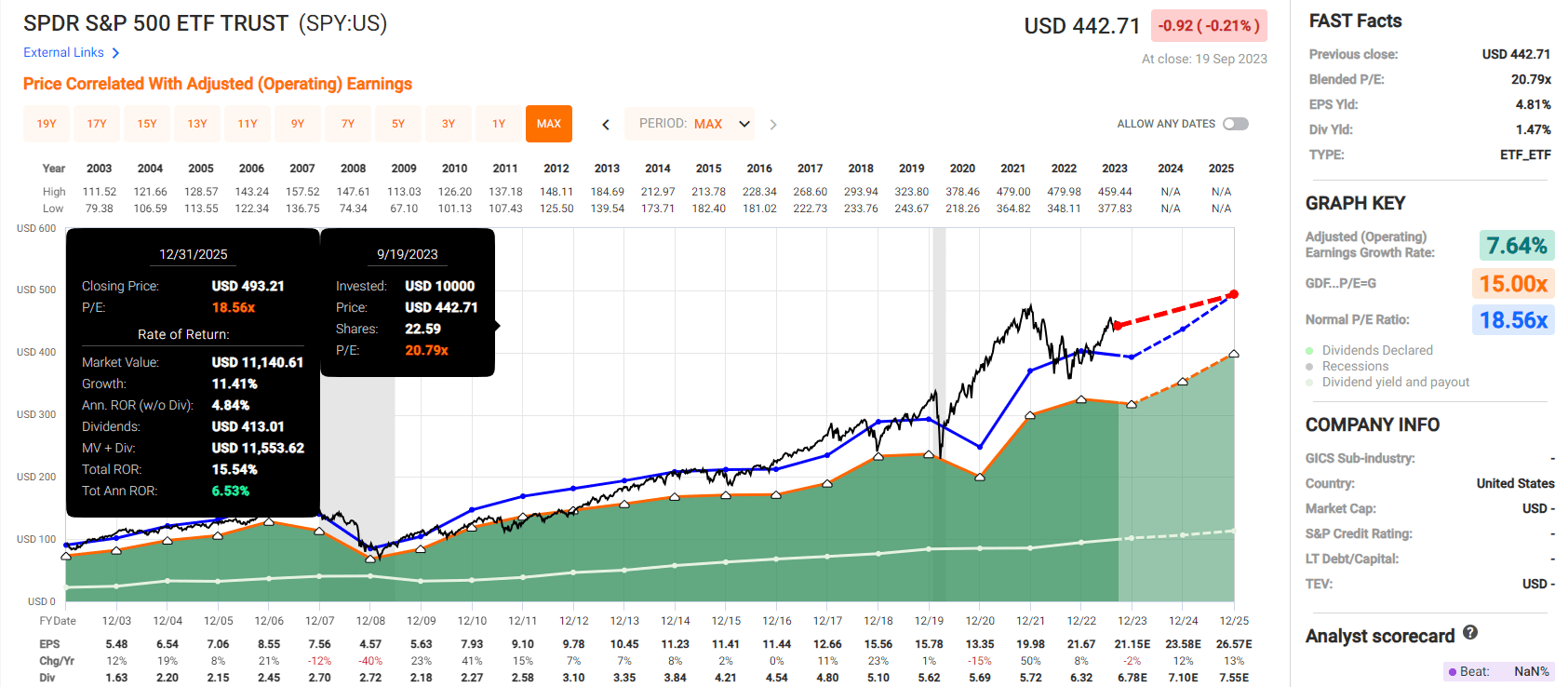

Fortis

{kind=link}

Cullen/Frost Bankers

{kind=link}

S&P 500

{kind=link}

S&P 500: 6% annual and 15% total return potential through 2025.

5 A-rated High-Yield Aristocrats: 21% annual and 55% total return potential through 2025.

3.7X better total return potential than S&P 500 with 3X the much safer yield.

Bottom Line: The 5 Best High-Yield A-Rated Dividend Aristocrat Buys

The Fed being behind the curve isn't actually outrageous.

A paper by three New Zealanders that’s forthcoming in the Journal of Money, Credit and Banking taps into results from the Gallup World Poll from 2005 to 2019, covering 1.5 million people in 141 nations. The poll includes questions about how people feel about their lives and their current situations...

People are nine to 13 times as likely to report sadness or physical pain in the short term when there’s been a one-percentage-point increase in the unemployment rate as when there’s been a one-percentage-point increase in the inflation rate. Similarly, an increase in unemployment is about six times as potent as an increase in inflation in lowering people’s self-assessments when they were asked a longer-term question about how they feel about their lives on a scale of zero to 10." - NYT (emphasis added).

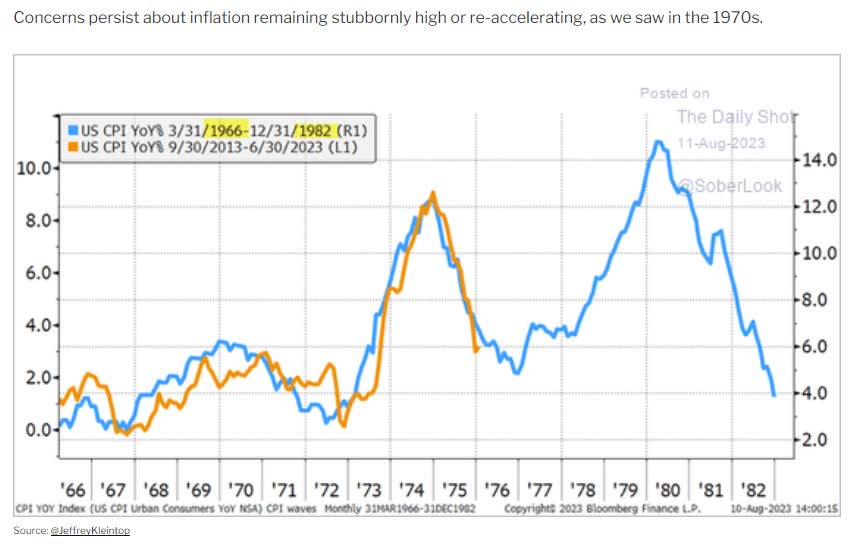

Morally speaking, as long as we aren't headed for another 1970s style wage-price spiral, avoiding recession is more important than getting inflation back to 2%.

After all, the purpose of government policy, or anything we do in our lives, is to maximize well being while minimizing harm.

It's easy to forget that the Fed's decisions have important consequences that affect billions of people around the world.

So I am not mad or outraged at the Fed for not hiking more aggressively. Yes, the math says the Fed should be at 7% to 8% right now, but life is more than just math, it's people.

But the fact is that if the Fed fails to beat inflation then long-term rates are likely to go a bit higher or potentially much higher.

Smart long-term investing means being able to sleep well at night, whether rates are at 0.5% or 5%.

Whether Europe is at peace or at war.

Whether relations with China are hot or cold.

Whether or not the government is shutdown or functioning normally.

Life is complicated, the world is messy, but EPD, O, PM, FTS, and CFR are A-rated high-yield aristocrats you can safely buy today, and trust to handle whatever is coming in the next few weeks, years, and decades.

For further details see:

5% Yielding Dividend Aristocrat Bargains You Don't Want To Miss