WMB - 8%-Yielding Enbridge: Still An Amazing Buy

2023-12-14 08:05:00 ET

Summary

- Enbridge is a steady and durable energy company with a moat-worthy business model that is unlikely to be disrupted by newcomers.

- The company's recent acquisition of Dominion Energy's natural gas utilities enhances its industry positioning in the U.S. and it's entering the RNG space.

- Enbridge offers a 7.7% forward dividend yield and has a strong track record of dividend increases, making it an attractive investment for income-focused investors.

It pays to invest in businesses that have steady revenue streams and are likely to be around for many generations. In such cases, getting in at a decent valuation and yield are likely the biggest things an investor needs to worry about, as they can be easy to hold onto without too much worry.

Plus, income investors get the benefit of recurring dividends that can be used to fund their lifestyles without having to time the market and sell shares. This helps them to avoid the regret of selling too early and paying the opportunity cost of missing out on future gains. I don't know about you, but I'd like to have my cake and eat it too.

This brings me to Enbridge (ENB), which carries a moat-worthy business model and unlike tech stocks, isn't likely to be disrupted by a newcomer anytime soon. I last covered ENB here back in August, highlighting its opportunities in the energy space and attractive valuation.

Lots have happened since my last piece, including stock market volatility due to interest rates and ENB's announced acquisition of 3 of Dominion Energy's (D) natural gas utilities. ENB's price action since August reflects that, as shown below. Nonetheless, ENB still trades 11% below where it was 12 months ago and offers a 7.7% forward dividend yield. In this piece, I highlight recent developments and discuss why I continue to view it as a solid high-yielding buy, so let's get started!

{kind=link}

Why ENB?

Enbridge is a Canadian company and over its lengthy history has become one of the largest and most important energy companies in North America. While ENB's business revolved primarily around liquids pipelines, it will become better hedged towards natural gas with the closure of its natural gas utility acquisitions (to be completed in latter 2024). As shown below, the post-acquisition ENB's EBITDA will be comprised of 50% liquids and 50% natural gas and renewable power.

Investor Presentation

Hallmarks of ENB's durability include the fact that 98% of its EBITDA comes from cost-of-service or contracted assets and over 95% of its customers have investment grade credit ratings. Plus, 80% of ENB's EBITDA has inflation protections, while just 10% of its debt have floating rate exposure, thereby mitigating near-term interest rate risks.

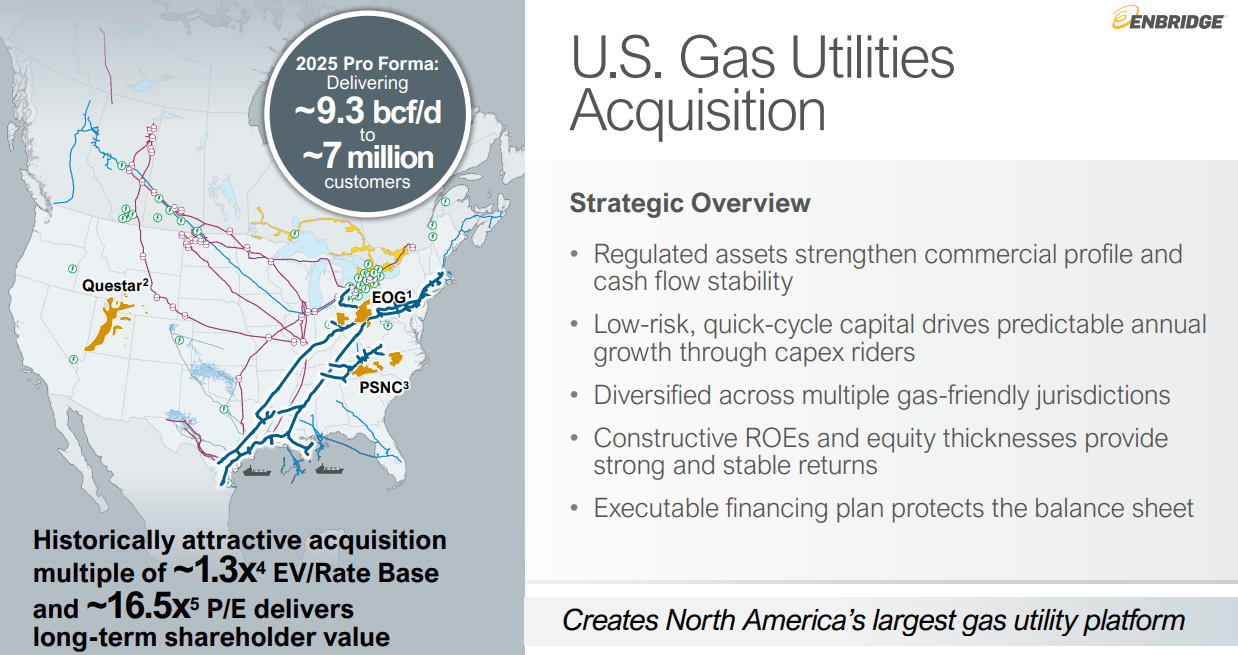

What's perhaps on top of mind for investors is ENB's C$19 billion acquisition of Dominion's 3 natural gas utilities, which greatly enhances ENB's industry positioning in the U.S. It's worth noting that 75% of the funding for the acquisition is already complete, comprising of C$6.2 billion in acquired utility OpCo debt, C$4.6 billion of equity issuance, and C$3.7 billion worth of convertible securities and bonds.

It appears that ENB is already making in-roads on the remaining funding, supported by the announcement this week that fellow Canadian midstream company Pembina Pipeline ( PBA ) will buy ENB's interests in the Alliance, Aux Sable and NRGreen joint ventures for C$3.1 billion, inclusive of C$327 million of EB's assumed debt.

Management expects for the remaining 25% of funding to come from a mix of asset recycling, proceeds from DRIP (dividend reinvestment program) and ATM equity issuances, convertible securities and bonds. Notably, these regulated utility assets help to further drive low risk cash flow stability in constructive and gas-friendly jurisdictions, enabling ENB to reach an estimated 7 million customers by the year 2025, as shown below.

{kind=link}

Meanwhile, ENB has continued to execute well, generating record EBITDA, up 3% YoY, and record DCF (distributable cash flow), up 2% YoY. This was driven by ENB's bread and butter liquids business, which remain highly utilized, transporting just under 3 million barrels per day, a record for Q3 volumes. Gas transmission was slightly lower during the third quarter due to lower ownership interest in DCP Midstream following ENB's transaction with Phillips 66 (PSX) last year, and the renewable business performed in-line with expectations.

Looking forward, ENB holds promise in the RNG (renewable natural gas) space as it recently entered into an agreement to acquire 7 high-quality operating and fully contracted landfill gas to RNG assets in Texas and Arkansas, selling 4.5 Bcf of pipeline quality renewable natural gas each year. The RNG assets are expected to be immediately accretive to ENB's DCF. What makes RNG assets attractive is the minimal required capital investment, since the source of landfill gas doesn't require expensive equipment to mine like that of natural gas. ENB expects for the RNG production number to grow at 3% annually, and has existing long-term full volume off-take agreements with Shell (SHEL) and BP (BP).

This, combined with ENB's other business, is expected to contribute to 5% annual EBITDA growth in the medium term, supporting its 3% to 5% annual dividend growth target. ENB lived up to that guidance by hiking the quarterly dividend rate by 3% to C$0.915 last month. This equates translates to USD $0.68/quarter and a 7.7% forward yield (subject to currency fluctuations) at the current share price of USD $35.48. The total dividend (including preferred shares' dividends) is also well-covered at a 53% payout ratio based on TTM operating cash flow, and ENB would qualify as a dividend aristocrat if it were a part of the S&P 500 ( SPY ) based on 28 consecutive years of dividend increases.

Risks to ENB include its higher leverage than some of its midstream peers, with a debt to EBITDA ratio of 4.5x, sitting higher than the 3x of midstream peer Enterprise Products Partners (EPD). However, ENB does have regulated utility businesses that EPD does not have and carries a respectable BBB+ investment grade credit rating.

A bigger risk is asset integration when it comes to the natural gas utility acquisitions next year. Although management expects to maintain its leverage ratio in the range of 4.5 to 5.0x post-acquisition, a low share price could make ENB more reliant on debt funding, which could cause it to land at the high end of its leverage range. Also higher interest rates could result in higher interest expenses, but that seems less likely now that the Federal Reserve is projecting three quarter-point rate cuts in 2024 as their inflation outlook has improved.

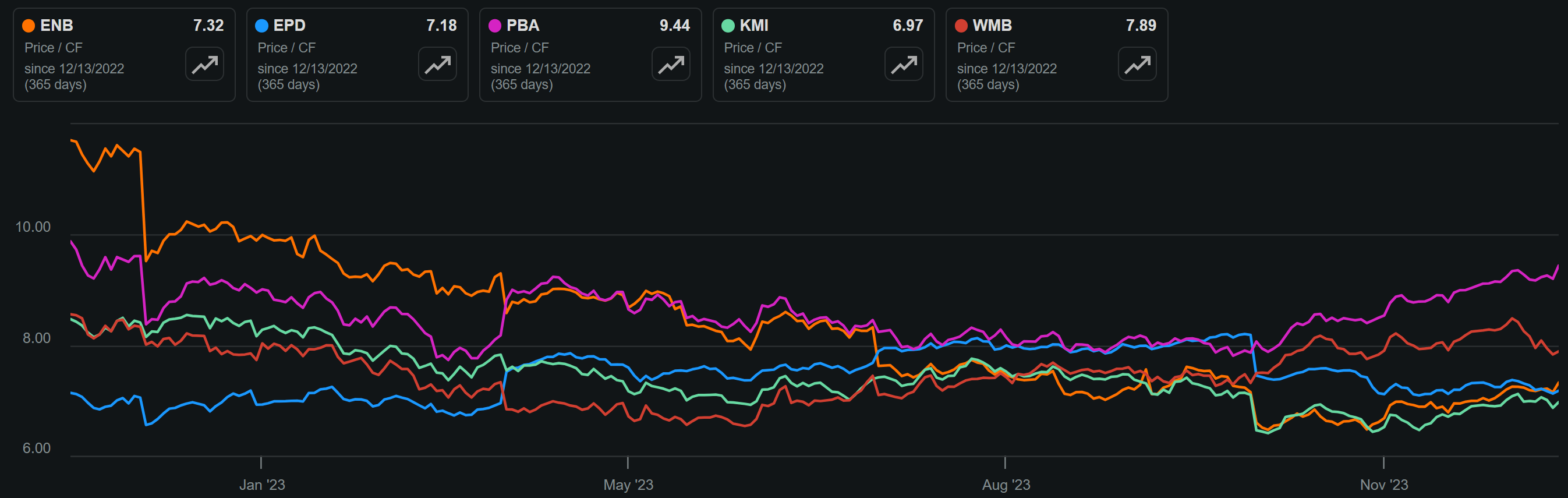

Turning to valuation, I continue to see value in ENB at the current price of $35.48 with a 7.7% forward dividend yield and a price-to-cash flow of 7.3x. As shown below, this puts ENB at the middle of the pack, sitting above the 7.2x of EPD, 7x of Kinder Morgan (KMI), and below the 9.4x of PBA and 7.9x of Williams Companies (WMB), despite ENB's wide asset base.

{kind=link}

Even more conservative income investors may want to consider the Preferred Series P stock ( ENB.PR.P:CA ). This preferred issue current trades at $16.45, representing a 34% discount to its $25 par value. It's also cumulative, which means that any missed payments must be made up unless if ENB files for bankruptcy, which is an unlikely scenario. It also yields 6.7%, which investors may find attractive should interest rates go down next year, as mentioned above.

While this preferred issue is trading past its call date of 3/1/2019, the market does not appear to believe it will be called anytime soon considering the wide discount to par value and elevated interest rates. Plus, this preferred issue has a face yield of just 4%, making it even more unlikely that ENB will call it anytime soon. Lastly, being called in wouldn't be the worst scenario for today's investors, as they would realize an immediate 34% gain!

Investor Takeaway

Enbridge remains one of my top picks in the midstream sector due to its diverse and stable asset base, continued execution, and attractive valuation. It also offers investors a healthy and growing dividend yield, with potential for growth in the future. While there are risks to consider, such as leverage and potential integration issues with upcoming acquisitions, I believe ENB's strong fundamentals make it a solid long-term investment for income-focused investors. And with its recent entry into the RNG space, ENB has positioned itself to take advantage of the growing interest in renewable energy sources. Considering all the above and some additional funding needs to close its natural gas utility acquisitions, I'm downgrading the stock from a 'Strong Buy' to a 'Buy'.

For further details see:

8%-Yielding Enbridge: Still An Amazing Buy