CBRL - A Focus On Menu Pricing At Cracker Barrel Could Be Huge For Investors

2024-01-12 10:52:32 ET

Summary

- Cracker Barrel Old Country Store's stock has fallen over 20% in the past year, but a rebound is possible if management takes corrective action.

- Increasing menu prices is the biggest lever for improving returns, as the company has room to catch up to competitors.

- The company's financials show a need for more dividend coverage, and pricing growth is the solution, in our view.

- We see upside in Cracker Barrel's shares to $100+, and investors get paid a very nice dividend yield of ~6.9% to wait.

By Valuentum Analysts

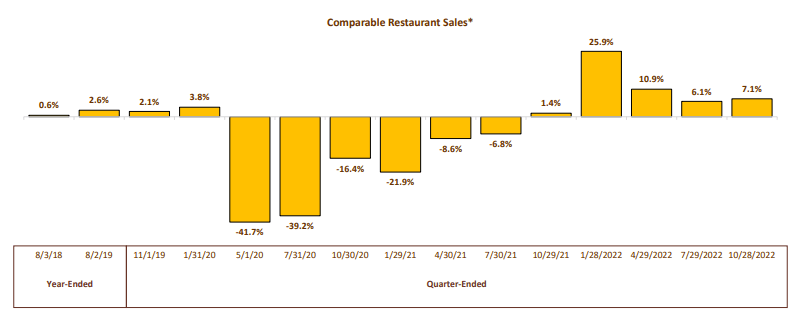

Cracker Barrel Old Country Store ( CBRL ) is a high-dividend paying restaurant that has a concept that is unmatched in the dine-in space, in our view. Not only do customers enjoy a home-away-from-home atmosphere, but guests can shop in their store while they wait--a combination that few, if any, other major restaurant concepts enjoy. Looking over the past several years, comparable store sales at Cracker Barrel faced significant pressure during the COVID-19 pandemic and have since been in recovery mode.

{kind=link}

Comparable store sales at Cracker Barrel have been in recovery mode since the end of the worst of COVID-19. (Cracker Barrel)

The stock, however, has languished in recent periods, with shares falling more than 20% over the past year or so. If management can take corrective action, however, we think this high yielding equity could experience a nice rebound. Cracker Barrel's dividend yield stands at ~6.9% at the time of this writing, a level that indicates some fundamental distress, but if the company can get things back on track, it might make for a very interesting income idea in a well-diversified portfolio.

In this article, let's talk about what we think Cracker Barrel should do to right the ship to drive improved equity returns for investors. Aside from continuing to execute on the expense front, we think the biggest lever that Cracker Barrel has to pull to improve returns is to continue to increase menu prices. From our perspective, the company has a lot of room in this area when compared to the menu prices of other dine-in peers. Cracker Barrel hasn't made enough progress on this front, and it has even taken its foot off the gas a bit when it comes to menu pricing. We think it should bite the bullet and raise menu prices materially.

Latest Quarterly Results

Here's what we wrote about Cracker Barrel on our website regarding its most recent quarterly results:

When Cracker Barrel reported first-quarter fiscal 2024 results for the period ended October 27, the performance wasn’t great. Revenue fell almost 2% on a year-over-year basis, while the firm’s non-GAAP earnings per share came in lower than expectations. Comparable store restaurant sales dropped 0.5%, while comparable store retail sales fell 8.1% in the period. Management is focused on marketing and the guest experience, which is great, but we think the C-suite needs to turn up efforts with respect to pricing to offset headwinds.

Total menu pricing increased 6.8% in the quarter (and management is targeting 4.5%-5% increases in fiscal 2024), but the executive team needs to be more aggressive on this front to catch up to peers that are charging much more for a much less desirable in-restaurant experience. Its average check, for example, is a meager ~$12-$13, which is only a few dollars more than value meals at fast-food restaurants these days.

{kind=link}

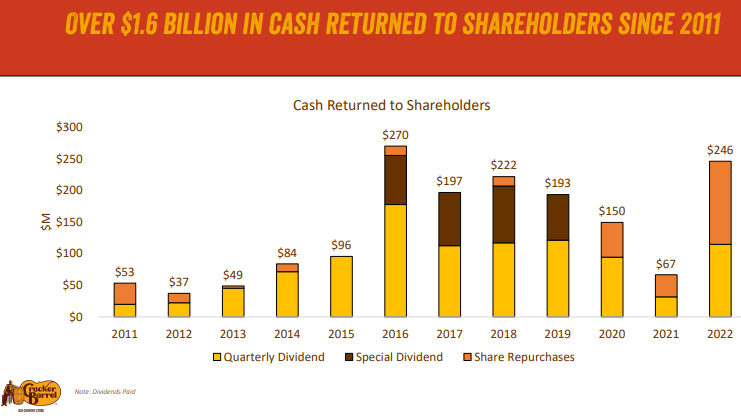

Cracker Barrel remains focused on returning cash to shareholders. (Cracker Barrel)

In its latest quarter, GAAP operating income fell to $11.4 million, or 1.4% of total revenue, dropping by more than half from the year-ago period. Adjusted operating income fell to $19 million, or 2.3% of total revenue, from $30 million in last year’s quarter, or 3.6% of total revenue. We don’t think that the firm’s menu or retail store selections are any less desirable in a post-COVID-19 world, but the firm is having trouble retaining levels of operating income due to higher costs across the board from labor to general administrative and beyond. In its latest earnings release , for fiscal 2024, the executive team is expecting commodity inflation in the low-single digits and hourly wage inflation in the mid-single digits, and these headwinds are being compounded by pressures on restaurant traffic and price-conscious guests reducing their retail purchases.

{kind=link}

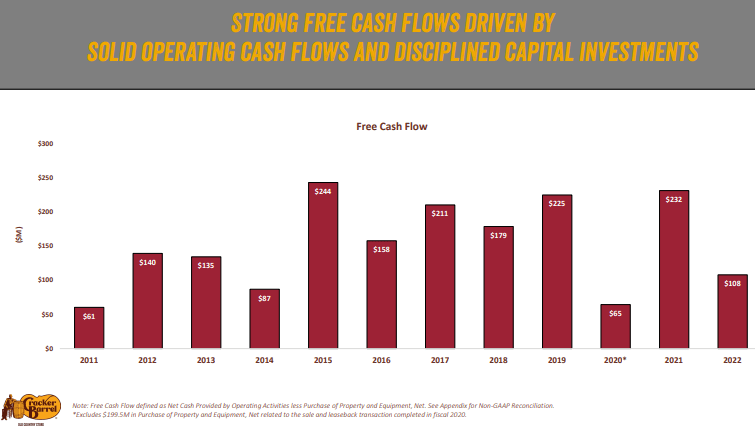

Cracker Barrel has done a good job driving positive free cash flow, despite challenges in its business. (Cracker Barrel)

Over the past couple years, many other restaurants have significantly raised their menu prices due to inflationary pressures, but based on our channel checks, Cracker Barrel has lagged behind in this area. Most of the company's marketing efforts have targeted the value-conscious consumer, too, with the company featuring a $8.99 price point for breakfast and highlighting selections in lunch and dinner that are below $12.

Though it may cause traffic declines to a certain degree, we think Cracker Barrel has a lot of room to raise prices by as much as 30%-50% in the coming years. The pricing lever is a big opportunity for Cracker Barrel, and we think elasticities from pricing actions will be positive for the company. Most visitors enjoy its friendly restaurant atmosphere, and a price point for breakfast at $11.99 and lunch and dinner at $15.99 could be a big needle-mover for the firm.

In particular, we would expect some pushback on the higher pricing from value-conscious customers and some traffic declines, but the higher margins it would gain across its operations should drive a step change in operating income and earnings per share, not to mention that it should help drive significant improvements in operating cash flow and free cash flow with respect to dividend coverage. Management might consider phasing out restaurants that suffer from outsized levels of traffic declines in the event that such large pricing actions are pursued in order to further optimize profitability and cash flow generation for shareholders.

Cracker Barrel barely covers cash dividends paid with free cash flow. (Cracker Barrel)

From our perspective, if Cracker Barrel doesn't put in plans to raise prices materially, its business and stock, for that matter, will likely continue to languish, and in the years ahead, its payout might grow under a greater risk of being cut.

Looking at its financials, Cracker Barrel has a net debt position with material operating lease liabilities, while free cash flow of ~$123.5 million for the twelve months ended July 28, 2023, was only marginally better than the $116 million in dividends it paid over the same period (as shown in the image above).

It needs more wiggle room with respect to dividend coverage, and pricing growth is the answer, in our view. Price falls straight to the bottom line, and Cracker Barrel needs to reset consumer expectations about its offerings. We find that it delivers tremendous value to consumers, and frankly, it is not charging enough.

Valuation

{kind=link}

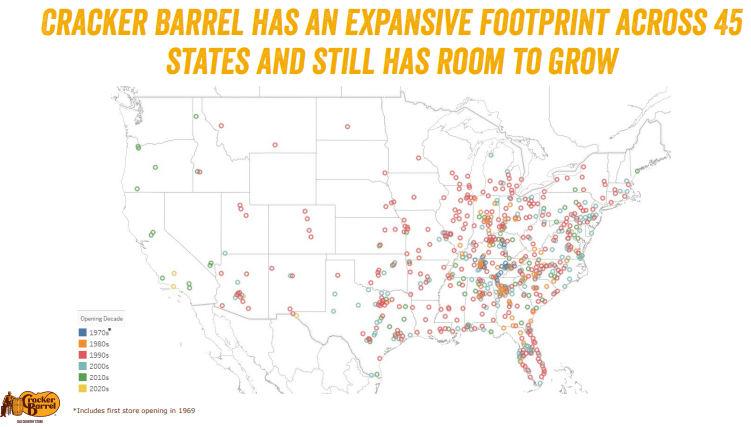

Cracker Barrel’s established restaurant concept has a lot of room to grow. (Cracker Barrel)

Cracker Barrel continues to have long-term unit growth opportunities at its Cracker Barrel and Maple Street stores, and these unique concepts are resonating. This helps to form a solid foundation for our long-term revenue growth assumptions at the company. Its latest quarterly results showed comparable store sales declines at its restaurant, but we think these trends are fixable through pricing actions.

{kind=link}

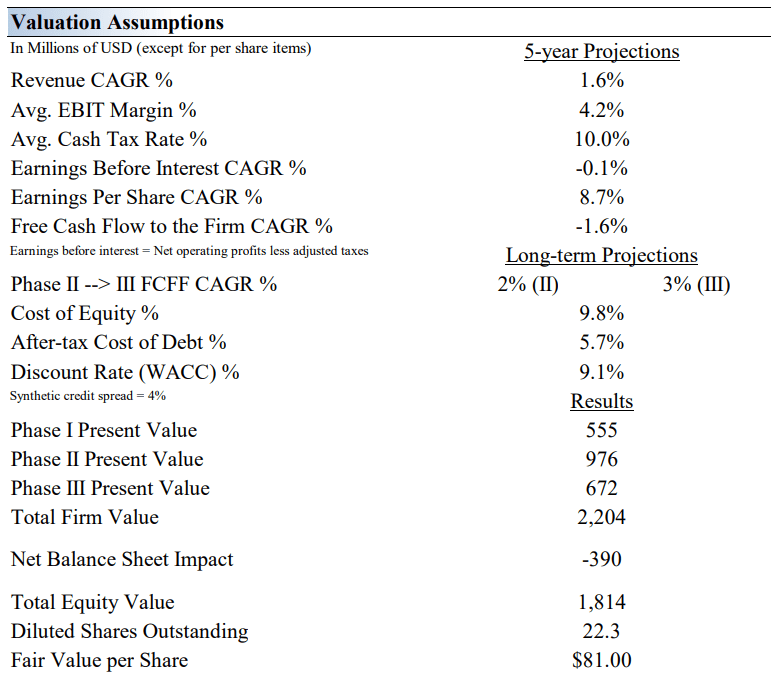

Our summary valuation assumptions of Cracker Barrel. (Valuentum)

As we look at our valuation assumptions above, we're not expecting much at Cracker Barrel over the next five years. We're modeling in modest revenue expansion to the tune of a 1.6% compound annual growth rate over the next five years, and we think earnings before interest will actually be below levels that they are today in five years. This results in an $81 fair value estimate, a level at which Cracker Barrel is still below. These are very conservative assumptions, in our view.

However, as shown in the image below, the high end of our fair value estimate range that we assign to Cracker Barrel stands north of $100 (its shares are trading at ~$75 each). At the moment, Cracker Barrel plans to pursue a cautious approach with respect to pricing for the remainder of its current fiscal year, but we think pricing adjustments represent a huge source of upside for Cracker Barrel over the next few years, a move that would result in a much higher fair value estimate.

The high end of our fair value estimate range of Cracker Barrel stands north of $100 per share. (Valuentum)

Risks

We think the biggest risk for Cracker Barrel is if it stands still. The industry has moved aggressively to raise menu prices, and while Cracker Barrel has taken some action in this area, clearly it hasn't been enough given recent trends in its operating margin. Instead of trying to appeal more to lower-margin, value-conscious customers, Cracker Barrel should instead work to attract higher-margin customers by raising its menu prices. Though such a move may result in traffic declines, to varying degrees across various markets, we think it is a risk worth taking.

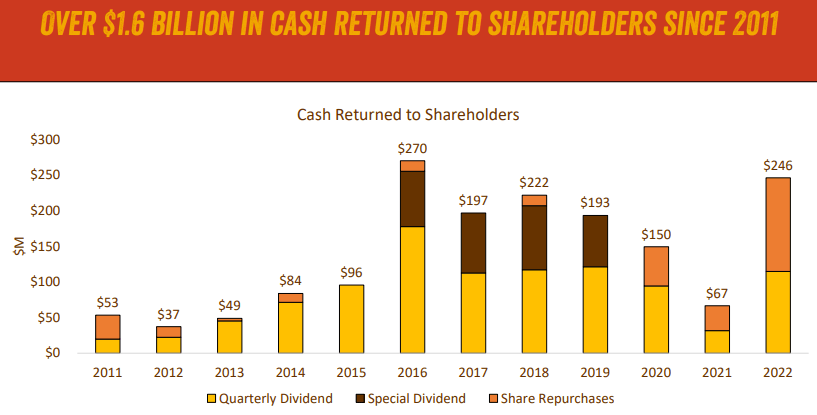

Other risks to our thesis on Cracker Barrel rest on whether it can keep its dividend intact if it does decide to keep going along its existing path without biting the bullet and raising menu prices significantly. Free cash flow barely covers its dividend payout as of the last fiscal year, and any further deterioration in operating cash flow might put the dividend on the chopping block. If that happens, we think many a dividend investor would look elsewhere, a huge disappointment for a company that has done a good job returning cash to shareholders in recent years.

Cracker Barrel has done a good job returning cash to shareholders in the past. (Cracker Barrel)

{kind=link}

Concluding Thoughts

The troubles at Cracker Barrel can be fixed, in our view, but management will likely have to come to the conclusion that any sustainable turnaround will, to a large degree, have to come via higher menu prices. If it doesn't make this move, inflation in the forms of commodity prices and hourly wages will likely continue to weigh on operating performance. Its value-conscious marketing messages just aren't working that great.

The magnitude of Cracker Barrel ~6.9% dividend yield speaks of risk to the payout, as does its free cash flow coverage of its payout, but if the executive team is able to ramp pricing initiatives more aggressively in the coming years, the stock could make for a great income idea with strong capital appreciation potential.

The high end of our fair value estimate range stands at $100+ per share, and Cracker Barrel's stock could get there if management executes a turnaround that we think is readily achievable through menu price expansion.

For further details see:

A Focus On Menu Pricing At Cracker Barrel Could Be Huge For Investors