SFTBY - A Good Hold: SoftBank Group's Asset Management And Investment Acumen At Play

2023-11-06 20:56:11 ET

Summary

- SoftBank Group is diversifying into various sectors such as e-commerce and internet services through strategic partnerships and investments.

- The IPO of Arm Holdings injected $4.87 billion into SoftBank's financial pool, signaling a financial rebound.

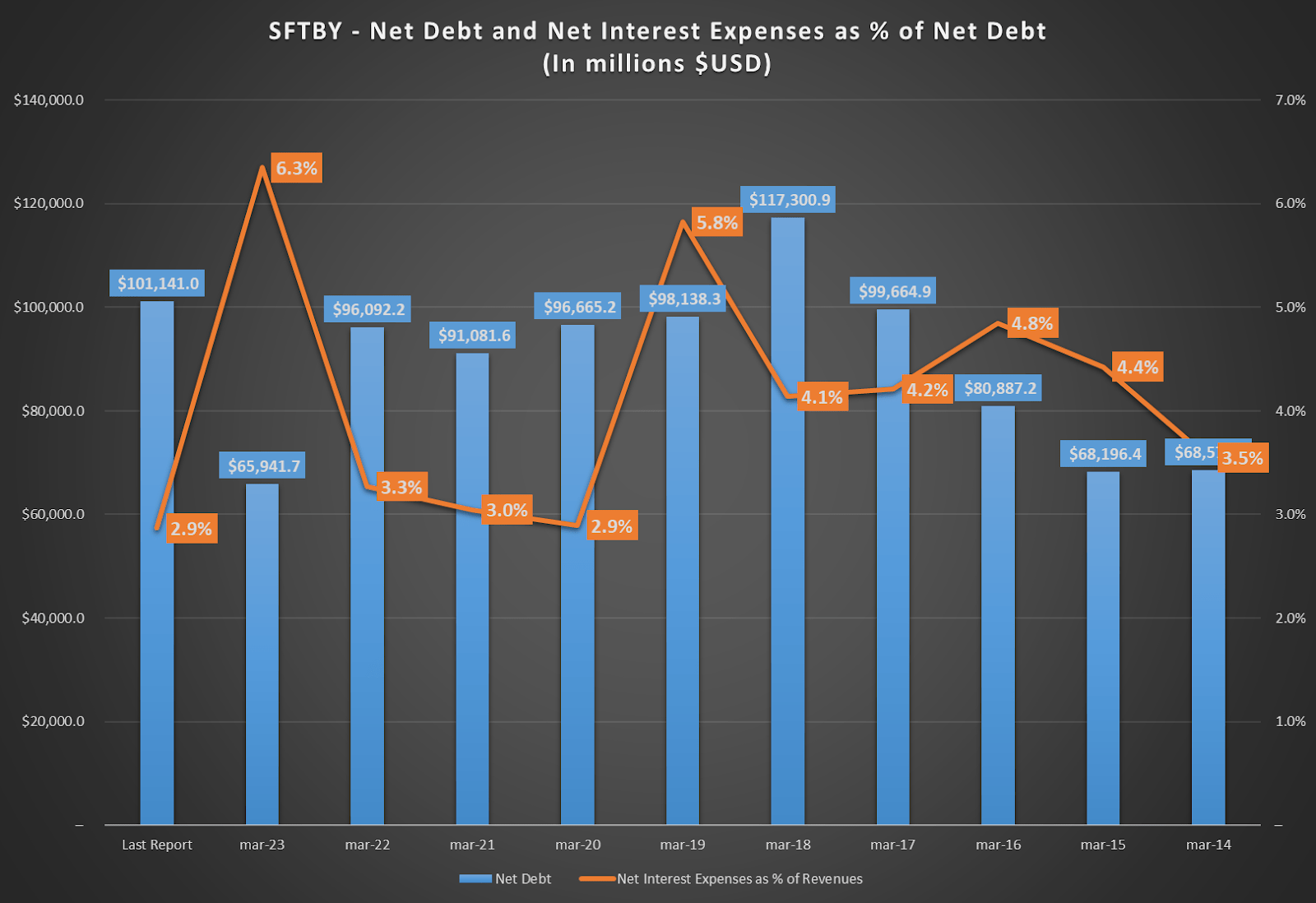

- The Company still grapples with a substantial debt of $151.85 billion, but transitioning to fixed interest rates has brought some relief.

- A P/B ratio of 0.93 suggests a "hold" rating for SoftBank, reflective of its asset-driven value and prudent financial management.

SoftBank Group Corp. ( SFTBY ) is a telecommunications giant diversifying into various sectors such as e-commerce, internet services, and Warehouse-as-a-Service through its venture with Symbotic, fueled by a strong desire for innovation. Noteworthy strategic partnerships, especially with Arm Holdings, have broadened its market footprint. The IPO of Arm injected an impressive $4.87 billion into SFTBY's financial pool, although it also ushered in market and geopolitical challenges. According to the Q1 2023 report, SFTBY displayed a promising net income of $3.17 billion, along with a $1 billion gain from the Vision Fund, pointing towards a financial rebound. However, the company still grapples with a substantial debt of $151.85 billion, although transitioning to fixed interest rates has brought some relief. In evaluating SFTBY's valuation, I believe employing the P/B ratio is a prudent investment approach. The current P/B ratio of 0.93 indicates a "hold" rating for the company.

Business Overview

SoftBank, headquartered in Tokyo, Japan, operates as a multifaceted conglomerate with a broad spectrum of business segments. Its core operations emanate from its Telecommunication Services, offering mobile communications, broadband services, and related solutions to a diverse clientele domestically and internationally. The company's expansive Investment Ventures, notably the SoftBank Vision Funds, delve into venture capital and private equity investments. SFTBY had a strong standing in technology-related ventures. At the same time, its ventures into e-commerce, internet services, and a recent foray into Warehouse-as-a-Service with Symbotic highlight its drive towards automation and AI integration in supply chain systems.

Furthermore, Pocketalk, SFTBY, and 1NCE have partnered to broaden global language translation initiatives. Pocketalk provides real-time translation tech for individual travelers and global organizations. SFTBY collaborates with Pocketalk to offer translation solutions to Japanese enterprise customers, exploring AI, IoT, and 5G for digital growth. 1NCE contributes its IoT connectivity, enhancing Pocketalk's devices for mobile communication in Wi-Fi-scarce areas. This partnership seeks to boost digitalization and global connectivity, helping overcome language barriers and foster international communication. Pocketalk aims to secure a Nasdaq listing within the upcoming two years, targeting a valuation of $1 billion.

Source: Earnings Investor Briefing for Q1 2023.

SFTBY's size and overall situation can be gauged not only from its diverse business ventures but also from its significant stakes in various telecom and tech entities. In my opinion, the company's multifaceted business model, coupled with strategic investments and alliances, places it in a vantage point to capitalize on emerging market trends.

SoftBank's Stake in ARM's IPO

In 2016, SFTBY acquired Arm Holdings and later increased its stake in anticipation of Arm's planned IPO . The relationship between Arm and SFTBY hints at a symbiotic potential, where a successful Arm IPO augurs well for SFTBY's market capitalization and investor confidence. In September, Arm Holdings' ( ARM ) IPO was priced at the highest point of its advertised range, resulting in a valuation of almost $60 billion . On September 13, Arm priced shares at the upper end of its expected range. The next day, the stock first traded at $56.10 and ended at $63.59. From this IPO, SFTBY obtained $4.87 billion while retaining a significant majority stake of 90.6% in Arm.

Arm Holdings is known for its innovative licensing model in the semiconductor and software design sector. The licensing model of Arm is distinctive, fostering a vast ecosystem of developers and facilitating companies eager to develop products based on Arm's designs. This model propels its technological imprint across various devices and markets, including the IoT and automotive electronics. The cornerstone of Arm's allure is its RISC (Reduced Instruction Set Computing) architecture, which epitomizes its dedication to power efficiency and high performance, setting it apart from the CISC (Complex Instruction Set Computing) architectures of its rivals.

In my view, the financial symbiosis between Softbank and ARM post-IPO has created a lucrative venture for Softbank, with a substantial portion of ARM's net income , which stands at $671 million, directly contributing to Softbank's coffers, through its 90.6% stake. However, this large stake also exposes Softbank to certain market risks. The burgeoning competition from RISC-V architecture, with its cost-effective, open-source nature, might appeal to cost-sensitive markets, potentially eroding ARM's dominant market position in the smartphone chip and energy-efficient semiconductor sectors. Moreover, the geopolitical and operational entanglements surrounding ARM's former subsidiary, Arm China, add a layer of risk. Any turmoil in China could have a cascading negative effect on ARM's, and by extension, Softbank's financial standing. The significant share of ARM's net income in Softbank's overall net income, which is $11.64 billion over the TTM, highlights ARM's role in Softbank's financial health. It's clear that while the ARM IPO has indeed been a financial boon for Softbank, the associated market and geopolitical risks warrant a vigilant strategic outlook to ensure sustained profitability and mitigate potential adverse impacts.

Source: Earnings Investor Briefing for Q1 2023.

In the Q1 financial report for the quarter ending on June 30, 2023, SoftBank Group's CFO, Yoshimitsu Goto, disclosed a net income of $3.17 billion primarily attributed to foreign exchange fluctuations, yet highlighted the improvement in financial metrics such as Net Asset Value and Loan-to-Value ratio. A significant revelation was the Vision Fund's $1 billion gain on investments, signaling a financial turnaround following six difficult quarters. The report emphasized a revived investment focus on the AI and logistics sectors with significant investments in Symbiotic, Berkshire Grey, and TELEXISTENCE. Goto reaffirmed SFTBY's financial strategy of retaining stability while capitalizing on investment opportunities.

Furthermore, SFTBY's evolving investment strategies are accentuated by a shift from merely an investor to an operator, especially in the semiconductors and robotics sectors. The investment focus favored AI-centric companies like Tractable and Spanned Logistics due to growth and AI integration in these sectors, as opposed to sector-specific investments. The investment strategy is leaning toward companies centered around AI technology due to the growth potential and the integration of AI in these fields. This strategy is more about targeting companies based on technological innovation, specifically in AI, across different sectors.

A Complex Yet Simple Valuation

From a valuation perspective, it's SFTBY's intrinsic worth is intricately linked to its insightful investment strategies and a substantial asset portfolio. In this sense, it's worth noting that the stake increment by Masayoshi Son in 2022 signals a strong internal belief in SFTBY's upward trajectory. This sentiment could resonate with prospective investors.

Nevertheless, it's worth noting SFTBY's substantial debt load of $151.85 billion . So, the company's strategic shift from floating to fixed interest rates is a laudable move that enhances its financial adaptability in the face of market uncertainties. This transition acts as a financial bulwark, safeguarding SFTBY against the vagaries of fluctuating interest rates, which, in my view, is pivotal for a company with such a hefty debt obligation. The fixed interest rates engender a more predictable interest expense , pegged at $4.03 billion for the TTM figures, which is a significant factor from a valuation perspective. By curbing the potential financial strain from escalating interest rates, SFTBY not only ensures a steady interest expense but also potentially augments its financial stability.

Source: Seeking Alpha plus author's elaboration.

{kind=link}

However, the cornerstone of SFTBY's valuation lies in its diverse asset portfolio and strategic investment ventures. The stellar success of Arm Holdings' IPO , with a valuation of $54.5 billion and a financial infusion of $4.87 billion, epitomizes SFTBY's investment acumen. This venture not only magnified the asset value but also furnished vital liquidity for future strategic forays, outlining a proactive stance toward asset consolidation and value augmentation. The pre-IPO acquisition of a 25% stake from Vision Fund further accentuates the strategic significance of Arm within SFTBY's asset echelon. In my view, these elements collectively propel SFTBY's valuation, rendering SFTBY a potentially lucrative venture for investors with a penchant for a diversified and strategically managed asset portfolio. The crux of SFTBY's valuation hinges on its adept asset management and strategic investment activities, with the successful IPO of Arm Holdings being particularly emblematic of SFTBY's strategy.

In my view, valuing SFTBY using a DCF methodology presents a nuanced endeavor owing to the firm's multi-faceted nature and substantial revenue decline from $86.7 billion in 2019 to $45.4 billion in TTM figures. The company's hefty debt load of $151.85 billion might inflate the WACC, thus potentially lowering the intrinsic valuation derived from DCF. However, the strategic shift from floating to fixed interest rates showcases prudent financial management, which could ameliorate some risk factors in the WACC calculation. Significantly, SFTBY's diverse investment ventures and asset portfolio, illustrated by the lucrative IPO of Arm Holdings that furnished $4.87 billion, along with a valuation boost to $54.5 billion, heralds a potential offset to the revenue decline concerns. This, coupled with the Vision Fund's $1 billion gain on investments, underscores the firm's adept asset management and strategic investment acumen, which could potentially augment its intrinsic value.

Source: YCharts.

Nevertheless, SoftBank's valuation, akin to that of Berkshire Hathaway (BRK.A), can be understood via the P/B ratio due to its holding company structure encompassing a variety of assets. This resemblance provides a solid basis for utilizing the P/B ratio to compare SoftBank's market valuation with its book value. SFTBK's P/B ratio has historically fluctuated between 0.64 to 2.38 since 2018, reflecting market sentiment. However, SFTBK currently trades at a P/B ratio of 0.93. This, coupled with the company's strategic decision to fix interest rates and the implication of moving towards a more stable capital structure, favors using the straightforward P/B ratio. Overall, these factors support a "hold" rating for SoftBank.

{kind=link}

The simplicity of this valuation method appeals to a broad range of investors, similar to the straightforward valuation approach favored by Berkshire Hathaway. Key investments in companies like Alibaba, Arm Holdings, and Vision Fund highlight SoftBank's asset-driven value, effectively represented by the P/B ratio. While a DCF analysis might offer more detailed insights, the P/B ratio's ease of use makes it a notably relevant valuation tool for SoftBank's complex asset portfolio, thus validating the selected valuation method and my resulting "hold" rating.

Looking Forward

Currently, SoftBank is expected to report earnings on November 9, 2023 . Concretely, I think investors should be eager to see if the company can uphold its net income from the previous term, which was $3.17 billion, and if it can continue to profit from its Vision Fund, noted for a $1 billion gain earlier after the ARM IPO. A critical aspect of this report will be how SoftBank manages its substantial debt of $151.85 billion, especially after its decision to fix its interest rates-a true test of its fiscal management.

Naturally, SFTBY's ventures in e-commerce and internet services will shed light on its ability to adjust to the dynamic market, so it's definitely worth monitoring to see if they're making new substantial investments after the ARM IPO, which could become future value drivers for the stock. Strategic alliances, such as the one with ARM Holdings, and forays into new sectors like Warehouse-as-a-Service are pivotal to SoftBank's market influence and revenue generation and will thus be under close watch.

Furthermore, the Fed is potentially near the end of its tightening cycle, and other economic variables are key considerations for SoftBank's investment tactics and overall market stance. The company's P/B ratio stood at 0.93 at the time of this writing, hinting at a conservative "hold" recommendation until more data is available. So, the forthcoming report could potentially change this ratio into a more undervalued range, making it a more attractive investment. Thus, overall, the next report will reflect SFTBY's strategic vision and its agility in navigating the markets as they seem to turn a corner due to the Fed's monetary policy.

Conclusion

SoftBank is evolving from a telecommunications behemoth into a multifaceted investment dynamo, branching out into realms such as e-commerce, internet services, and Warehouse-as-a-Service. A notable milestone in this transformation was the acquisition of Arm Holdings, which, coupled with a successful IPO, injected $4.87 billion into SoftBank's coffers. Moreover, financial highlights from Q1 2023 include a net income of $3.17 billion, juxtaposed against a substantial debt of $151.85 billion. However, a silver lining emerges with the Vision Fund posting a gain of $1 billion. Still, SoftBank's prudent decision to transition to fixed interest rates to cushion against interest rate risks. Overall, a P/B ratio of 0.93 nudges toward a "hold" rating for SoftBank. This tempered endorsement hinges on robust assets and astute investments, coupled with a relatively fairly valued stock.

For further details see:

A Good Hold: SoftBank Group's Asset Management And Investment Acumen At Play