ACTV - A March Fed Rate Cut Is Becoming Less And Less Likely

2024-01-21 06:45:39 ET

Summary

- Renewed uncertainty regarding the pace and time of 2024 rate cuts by the Fed add to risks for stocks and bonds.

- The odds for a March rate cut have declined to under 50% from as high as 80% earlier this month.

- We expect the Fed to maintain a hawkish tone at the upcoming January FOMC.

After just over two years, the S&P 500 ( SP500 ) has finally posted a new all-time high. A lot has happened over the period with the market climbing over major headwinds including the post-pandemic hangover, supply chain shortages, a short-lived energy crisis, the start of two wars, 40-year high inflation, and the significant rise in interest rates.

The story now is about the otherwise resilient U.S. economy managing to avert a recession while the outlook for cooling inflation has opened the door for Fed rate cuts this year. There's also building optimism that the emergence of artificial intelligence has set off a major new growth driver in tech fueling optimism for a new round of earnings growth.

While the setup for the stock market can be described by some as "good", attention turns to one of the pillars in this bull market run over the last several months. Indeed, there is some new uncertainty regarding the timing and pace of Fed rate cuts following a string of mixed data points.

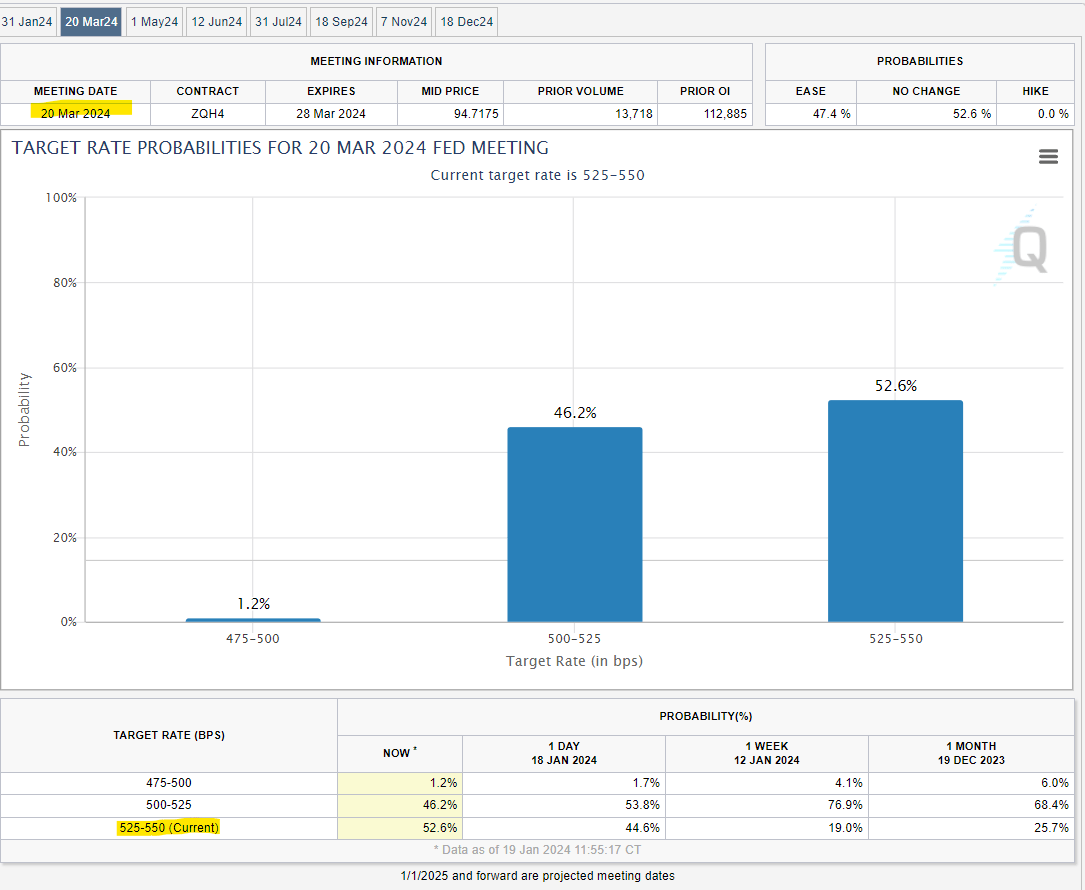

According to the CME FedWatch Tool , which extrapolates a market-implied probability for interest rate policy decisions, the market now sees a less than 50% chance for a March rate cut. This is down from a high of 80% earlier this month, essentially pushing back on the timetable for the elusive Fed pivot.

Ahead of the upcoming FOMC set for later this month on January 31, we believe the odds for a March cut are even lower with several reasons to believe the Fed is likely to maintain a hawkish tone. Ultimately, an environment where interest rates remain higher for longer introduces risks into the market that can translate into rising volatility for stocks and bonds.

{kind=link}

The Challenge of Mixed Data

Historically, the Fed tends to avoid surprises. Outside "emergency meetings", it goes against their mandate to make major policy changes without first clearly signaling their next step in official communications. In terms of 2024 rate cut timing, that hasn't happened yet.

That becomes a problem thinking about the upcoming January FOMC where presumably the group would need to tee up the first March rate cut the market is already thinking about. Ideally, the Fed would come into that meeting with a checklist of data points supporting the initial process of rolling back financial tightening with a messaging that is perceived as dovish.

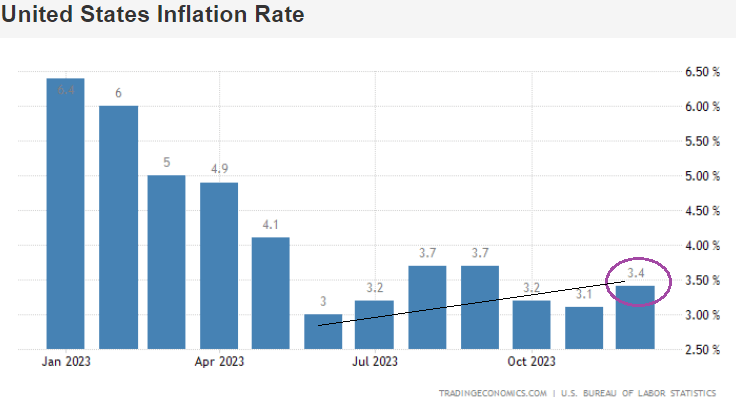

We know the inflation picture has gone in the right direction over the past year, but the current 3.4% headline annual rate from the December CPI isn't great. While down from the cycle peak in 2022 or even 6.4% in January last year, keep in mind that the CPI hit a low of 3.0% in June 2023, so the progress has already been bumpy.

The latest trends in the labor market with ongoing positive job gains as well as consumer spending through retail sales surprisingly strong to start the year work to downplay any urgency that immediate rate cuts are necessary.

Simply put, we just don't think there is enough right now that warrants the Fed at the upcoming FOMC to project confidence inflation will continue to trend lower.

The big risk here is that the disinflation process stalls or inflation even re-accelerates particularly as monetary policy becomes less restrictive into the second half of the year.

The combination of strong consumer sentiment and financial asset prices near record levels has the potential to unanchor inflation expectations to the upside going forward.

{kind=link}

Fed Will Err on The Side of Caution

The other angle we offer here is to think back at the perceived credibility crisis the Fed went through between 2021 and 2022 when it was too late to hike interest rates as inflation exploded higher at the time.

With that episode in mind, a situation where the Fed cuts too early and is later forced to hike again if the CPI rises higher would be disastrous in terms of market confidence and rebuilding its authority.

As analysts, we can dig through the inflation numbers and find categories of the CPI that are encouraging including core-services ex-shelter, or even extrapolate that used car prices have more downside, but that line of thinking hasn't been part of the script for the Fed this cycle for erring on the side of caution.

Going through official policy statements over the past two years, even as it became apparent inflation had peaked and was cooling, the sense is that the group has always been reluctant to highlight the "good" developments with a fear of declaring victory too soon. So while we may be approaching that finish line over the next few months, there's a good case to be made to push back on that timetable.

As we see it playing out, an expectation for the May FOMC to deliver the first cut would both buy the Fed a few more months for the data to evolve with the March Fed meeting setting the stage for the messaging pivot signal instead of January.

What's interesting about the March Fed meeting is that it will come with the updated quarterly package of economic projections which would be the opportunity to set the tone for the rest of the year.

What Happens Next?

We've maintained the position that the market consensus entering 2024 for 6 or more Fed rate cuts was likely too aggressive or overly optimistic. While there is still some uncertainty on that front, the latest trends suggest rates will end up a bit higher than previously expected.

There are many paths the Fed could take with an initial cut either in March, May, or later followed by a "pause" over single or multiple meetings. The Fed could even wait to cut later into the second half but make a bigger first move with a 50 basis point Fed Funds Rate reduction.

In the scenario where the group emerges very dovish at the upcoming January FOMC, the issue there is that the messaging could be perceived as suggesting some insight into an underlying weakness in the economy the group sees that the market is missing. This would create a separate line of challenges.

What we can say with confidence is that the backdrop of mixed data between economic conditions with more uncertainty on the trajectory of inflation sets up the potential for renewed volatility in stocks and bonds.

The good news here is that a stronger-than-expected economy works as a tailwind to the operating environment and earnings outlook for major companies. The question becomes whether that is enough to balance out the consequences of rates staying higher for longer.

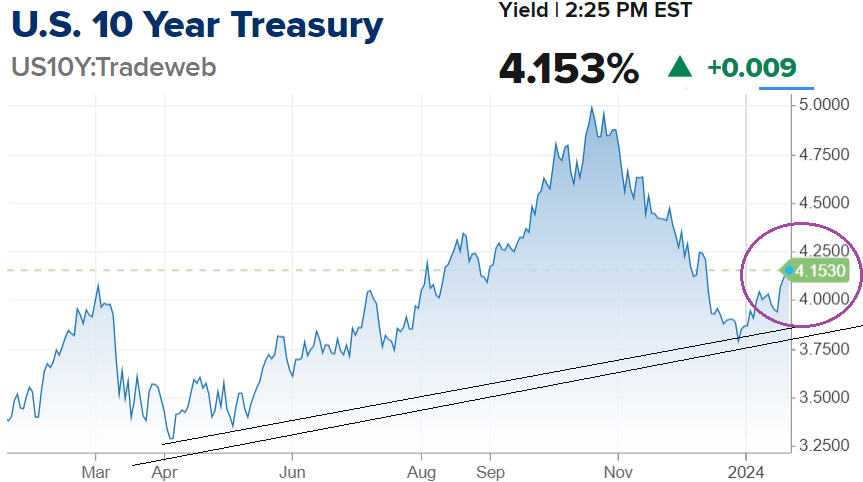

We're already seeing bond yields reverse their gains since the December Fed meeting and that steepening represents just one divergence compared to the strength in equities.

{kind=link}

We sense that some optimism in the stock market and current earnings projections consider an expected boost from interest rates quickly trending lower. If the narrative gets reset, stocks could be repriced lower thinking about the role of a lower equity risk premium.

One concern here is that each additional month that goes by with interest rates at the current level creates an opportunity for something in the financial market or even the real economy to break. We saw some of that with the banking industry turmoil in early 2023.

Attention turns to the health of the consumer with signs of rising credit delinquencies . If the current strength of the economy is unsustainable, the Fed moving to cut rates may not do enough to sufficiently support growth or avert a labor market rolling over.

Final Thoughts

It has become less and less likely that the Fed will begin cutting rates in March. Whether the market finds that a problem remains to be seen, but our take is that risks are high so that a reset of expectations takes place.

In terms of the stock market, the bullish momentum appears very strong, but as is often the case, all it takes is a couple of headlines for sentiment to change quickly. We urge caution and recommend avoiding chasing momentum names at the current level.

For further details see:

A March Fed Rate Cut Is Becoming Less And Less Likely