REIT - A November To Remember

2023-11-26 09:00:00 ET

Summary

- U.S. equity markets continued their November rally into the Thanksgiving week, while benchmark interest rates held steady around two-month lows as investors weighed easing geopolitical tensions alongside mixed economic data.

- Gaining for a fourth straight week since dipping into "correction territory" at the end of October, the S&P 500 gained another 1.0% this week, while the tech-heavy Nasdaq 100 advanced 0.9%.

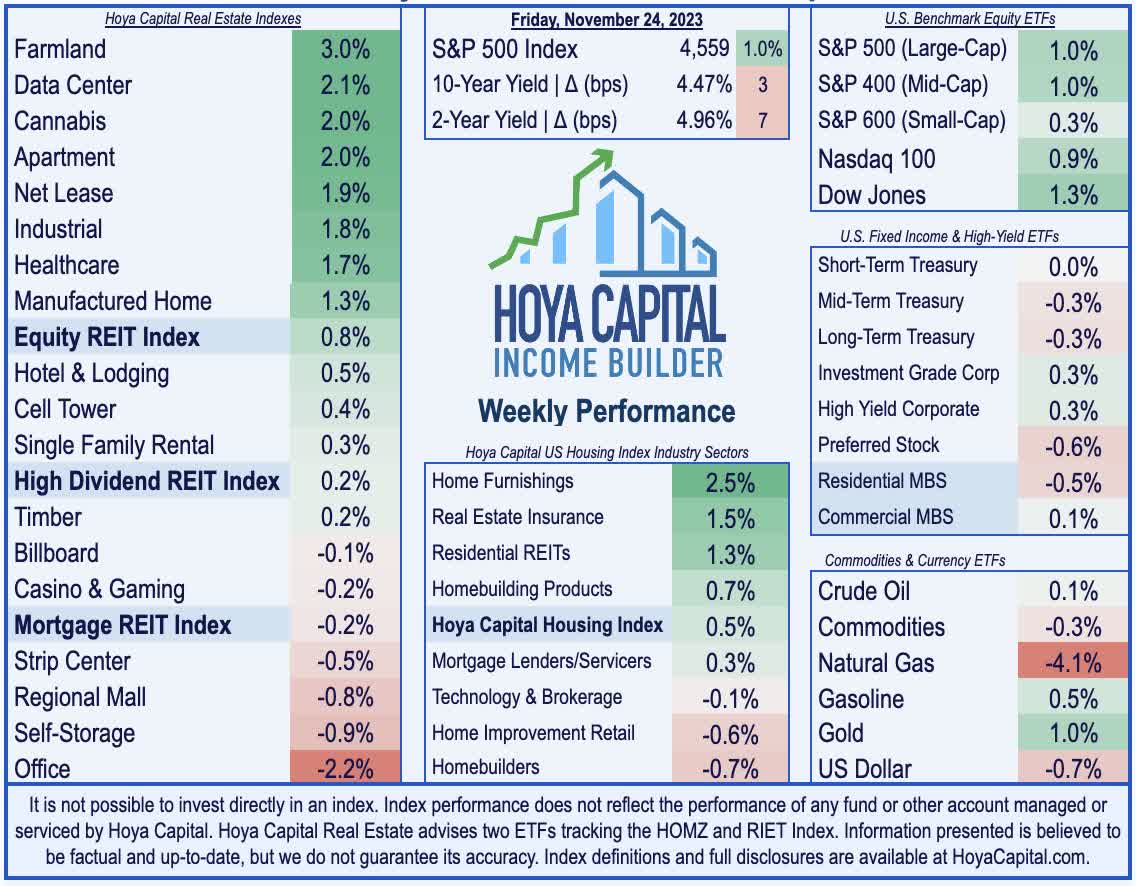

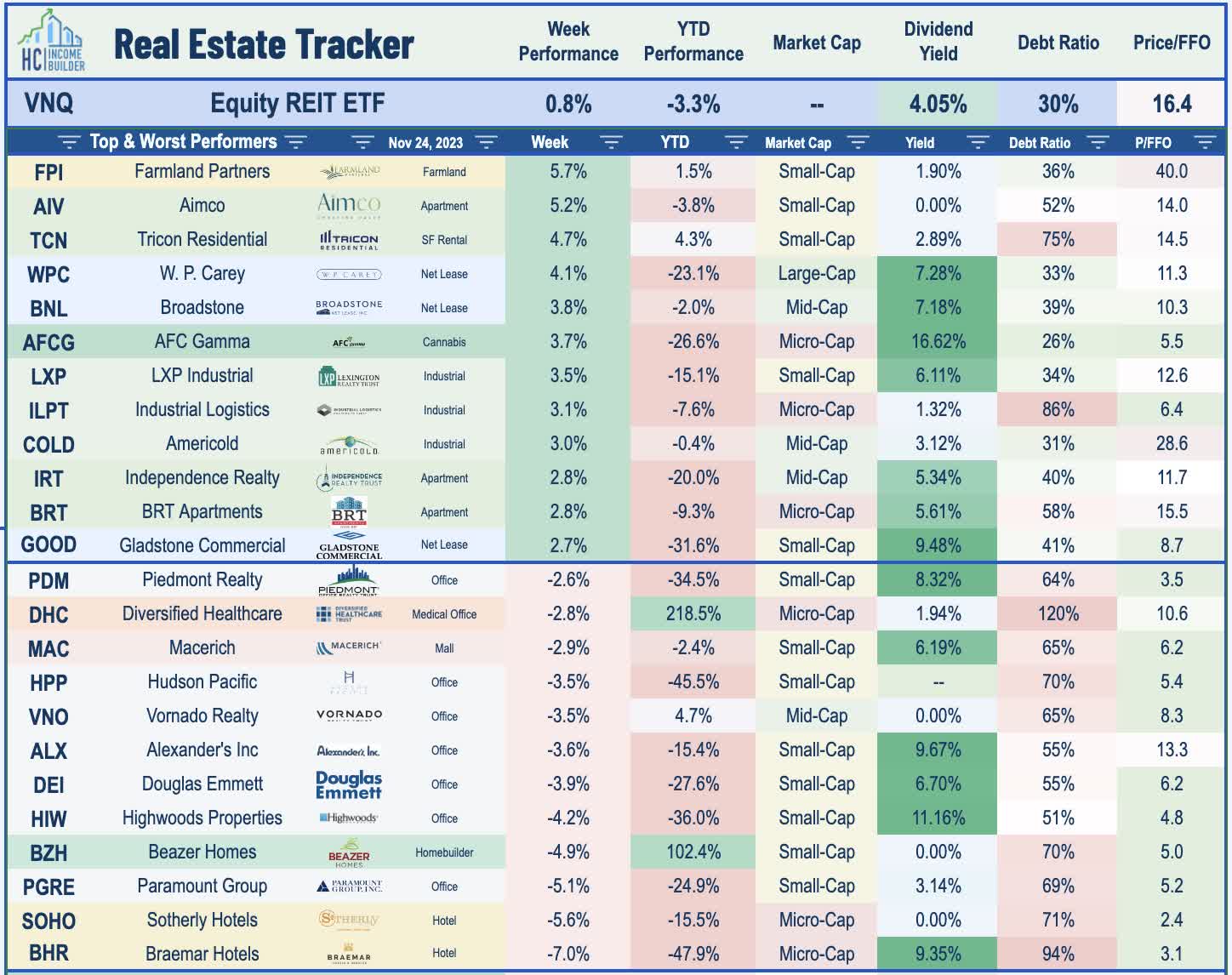

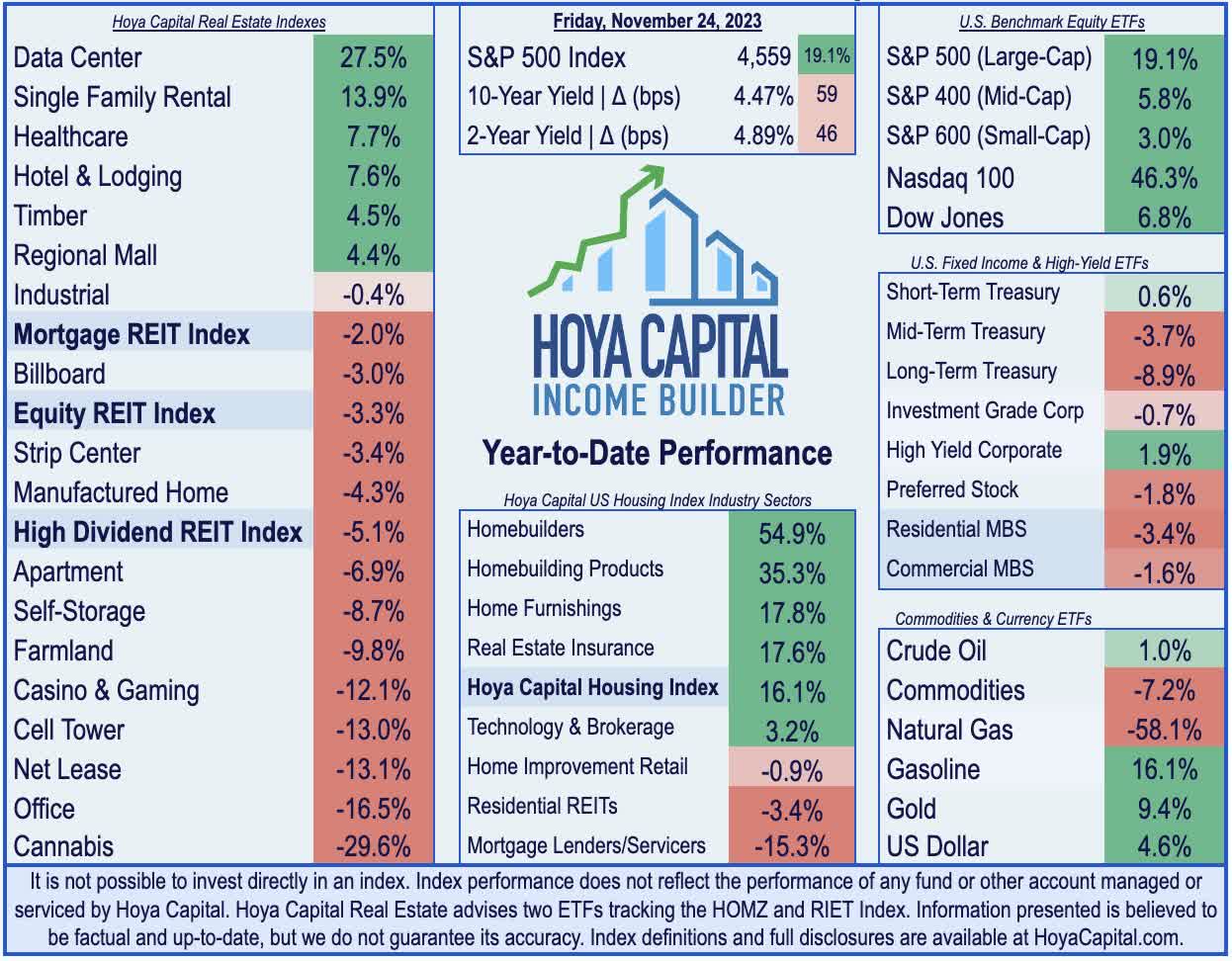

- Following a nearly 5% surge in the prior week, real estate equities also finished modestly higher this week. The Equity REIT Index advanced another 0.8%, but Mortgage REITs slipped 0.2%.

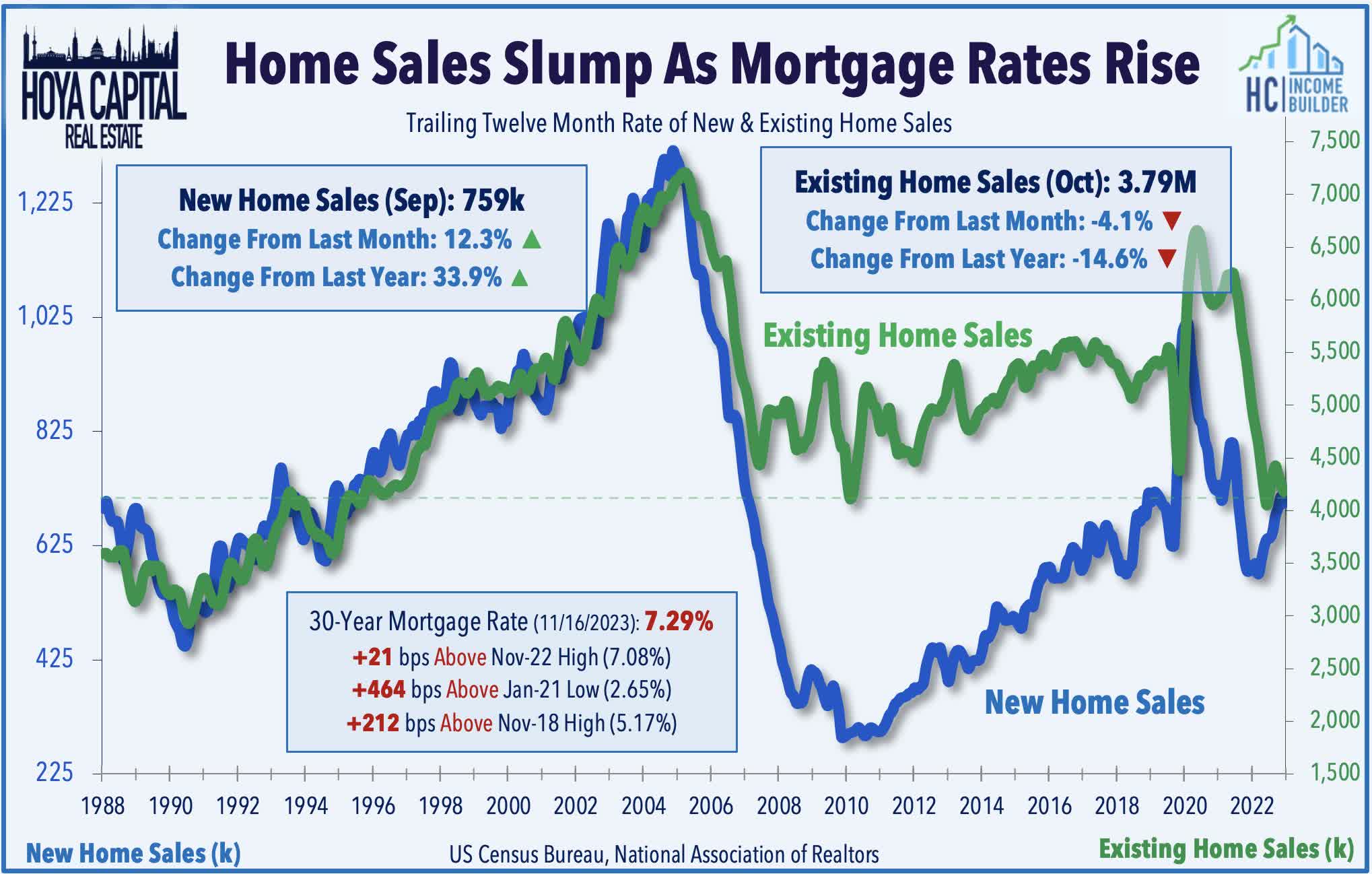

- While the recent pullback in mortgage rates has brightened the outlook for the sluggish housing market, data this week showed the effects of the late summer surge in mortgage rates to above 8%. Existing home sales slid 14.6% from a year earlier in October. Despite the sales slowdown, inventory levels remain well below historic averages.

- Apartment REITs were in focus following a WSJ report that several bidders have emerged in the FDIC's auction process of Signature Bank's $33B real estate loan portfolio following the collapse of the NYC-focused bank in March.

Real Estate Weekly Outlook

{kind=link}

U.S. equity markets continued their November rally into the Thanksgiving week, while benchmark interest rates held steady around two-month lows as investors weighed easing geopolitical tensions alongside a mixed slate of economic data and corporate earnings results. Gaining for a fourth-straight week since dipping into "correction territory" at the end of October, the S&P 500 gained another 1.0% this week, while the tech-heavy Nasdaq 100 advanced 0.9% - climbing to its highest level in nearly two years. Following a nearly 5% surge in the prior week, real estate equities also finished modestly higher this week. The Equity REIT Index advanced another 0.8% this week, with 12-of-18 property sectors in positive territory, while the Mortgage REIT Index slipped 0.2%. Homebuilders were under some pressure this week on data showing that Existing Home Sales dipped to thirteen-year lows, while retail earnings results showed sluggish home improvement trends.

{kind=link}

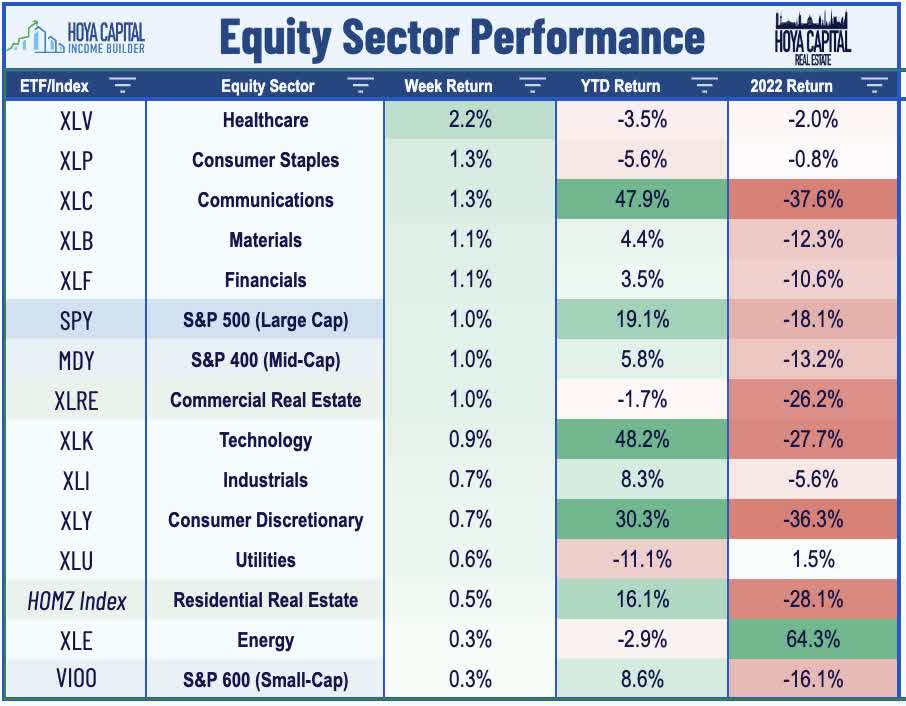

Bond markets were mixed this week, as the 10-Year Treasury Yield edged higher by 3 basis points to close at 4.47% - but still near the lows of its two-month range - while the policy-sensitive 2-Year Treasury Yield advanced 7 basis points to 4.96%. Narrowly snapping a five-week skid, WTI Crude Oil advanced 0.1% on the week to just over $75 per barrel but slid late in the week after OPEC delayed its planned Sunday meeting amid a dispute over production levels. The US Dollar Index posted a third-straight week of losses, while the CBOE VIX Index ( VIX ) - a measure of stock market volatility - dipped to its lowest level since January 2020. All eleven GICS equity sectors finished higher on the week, with Healthcare ( XLV ) and Consumer Staples ( XLP ) stocks leading to the upside, but retail stocks were among the laggards during the critical 'Black Friday' week following disappointing results from "big box" retailers Kohl's ( KSS ) and Best Buy ( BBY ) along with mall-based retailers Nordstrom ( JWN ) and Urban Outfitters ( URBN ).

{kind=link}

Real Estate Economic Data

Below, we recap the most important macroeconomic data points over this past week affecting the residential and commercial real estate marketplace.

{kind=link}

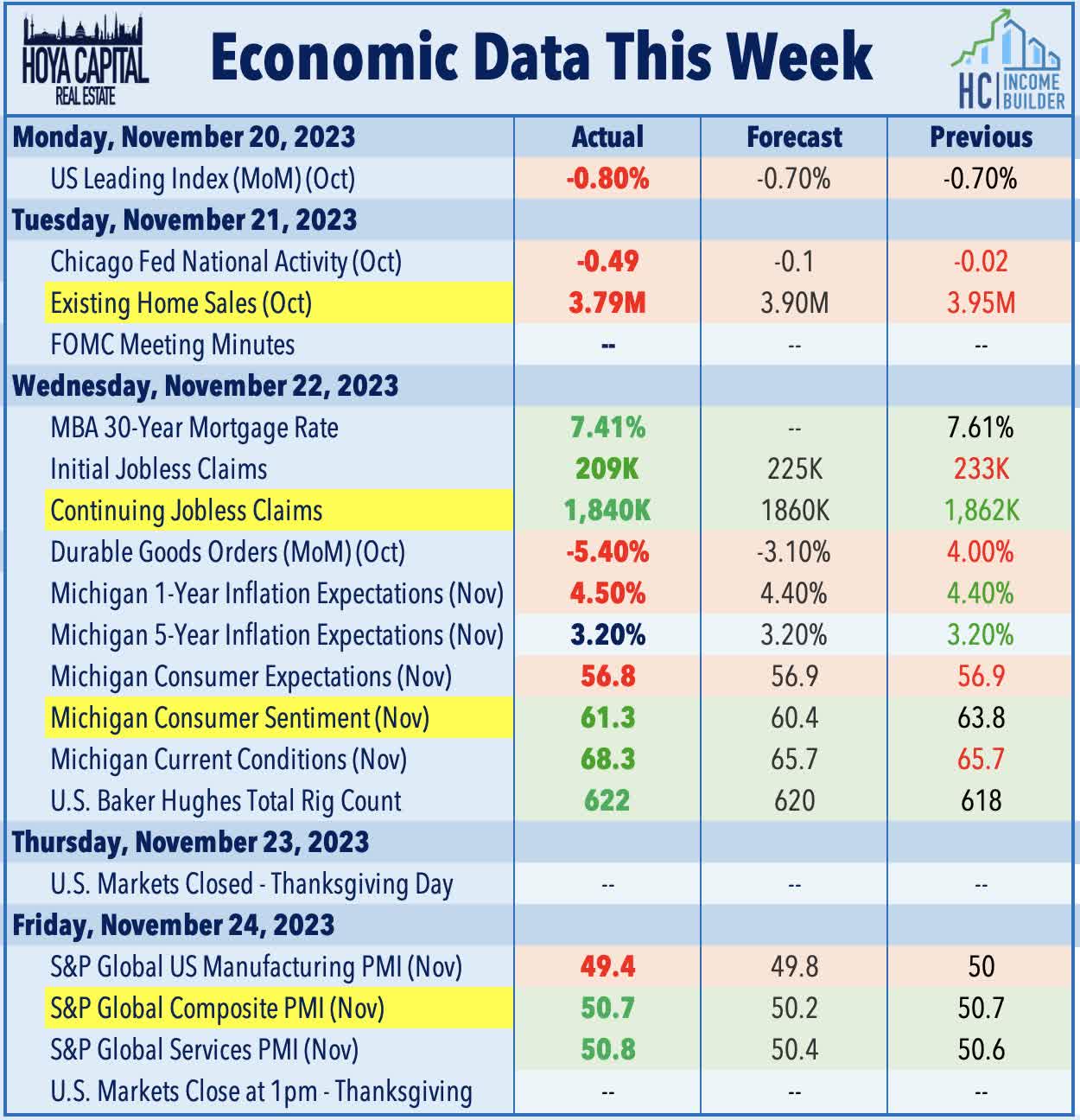

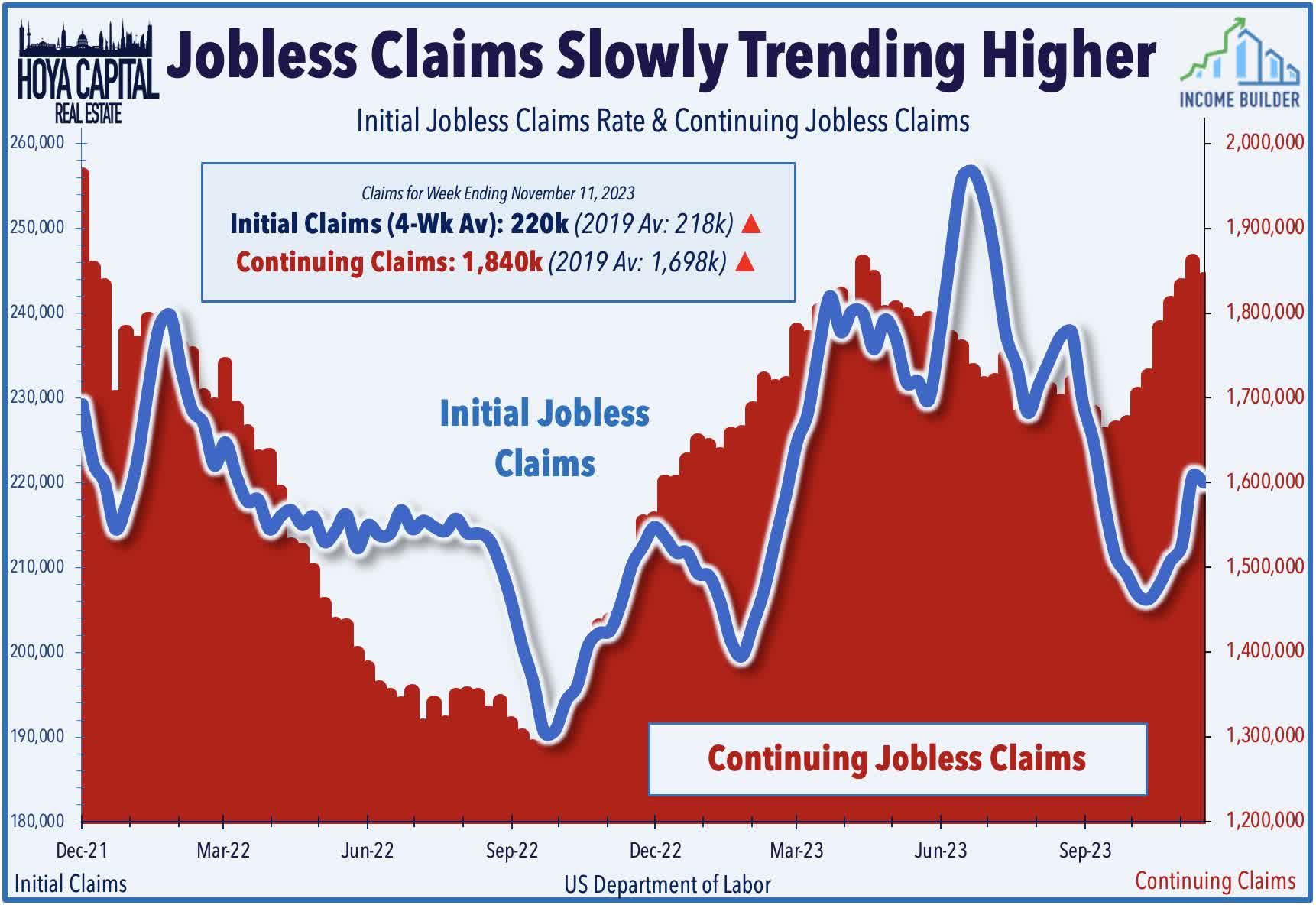

Following several weeks of soft employment data, weekly Jobless Claims data this week was stronger than expected, showing that initial jobless claims fell by the most since June while continuing claims declined for the first time in two months. Weekly claims data tends to be choppy around the holiday season, however, and it's notable that on an unadjusted basis, initial claims climbed to the highest since July, while unadjusted continuing claims rose by the most in four months. Consumer sentiment data was also slightly stronger-than-expected on the headline reading - edging up to 61.3 from 60.4 in early November - but the report showed an uptick in consumer inflation expectations and a more pessimistic view of future conditions. Manufacturing data was notably weaker-than-expected, showing that durable goods orders dipped -5.4% from last month - worse than the -3.1% expected - and was higher by just 0.3% from last year, which was the weakest since August 2020.

{kind=link}

While the recent pullback in mortgage rates has brightened the outlook for the sluggish housing market, data this week showed the effects of the late-summer surge in mortgage rates to above 8%. Existing-home sales slid 14.6% from a year earlier in October to a seasonally adjusted annual rate of 3.79 million - weaker than expected and marking the second slowest month for home sales since 1995, eclipsed only by one month - August 2010 - at the depths of the GFC-induced slowdown. Per Freddie Mac, the average quoted 30-Year Fixed Rate mortgage declined to 7.29% this week, down 50 basis points from the recent peaks near 8% in late October. New Home Sales data earlier this month showed that the largest single-family homebuilders have been able to cope with multi-decade-high mortgage rates by leveraging their platform's scale and relatively healthy balance sheet to offer more attractive financing options than what's currently available for prospective homebuyers in the traditional existing home sales market. Of note, New Home Sales represented 15% of total home sales in October, the highest since 2003.

{kind=link}

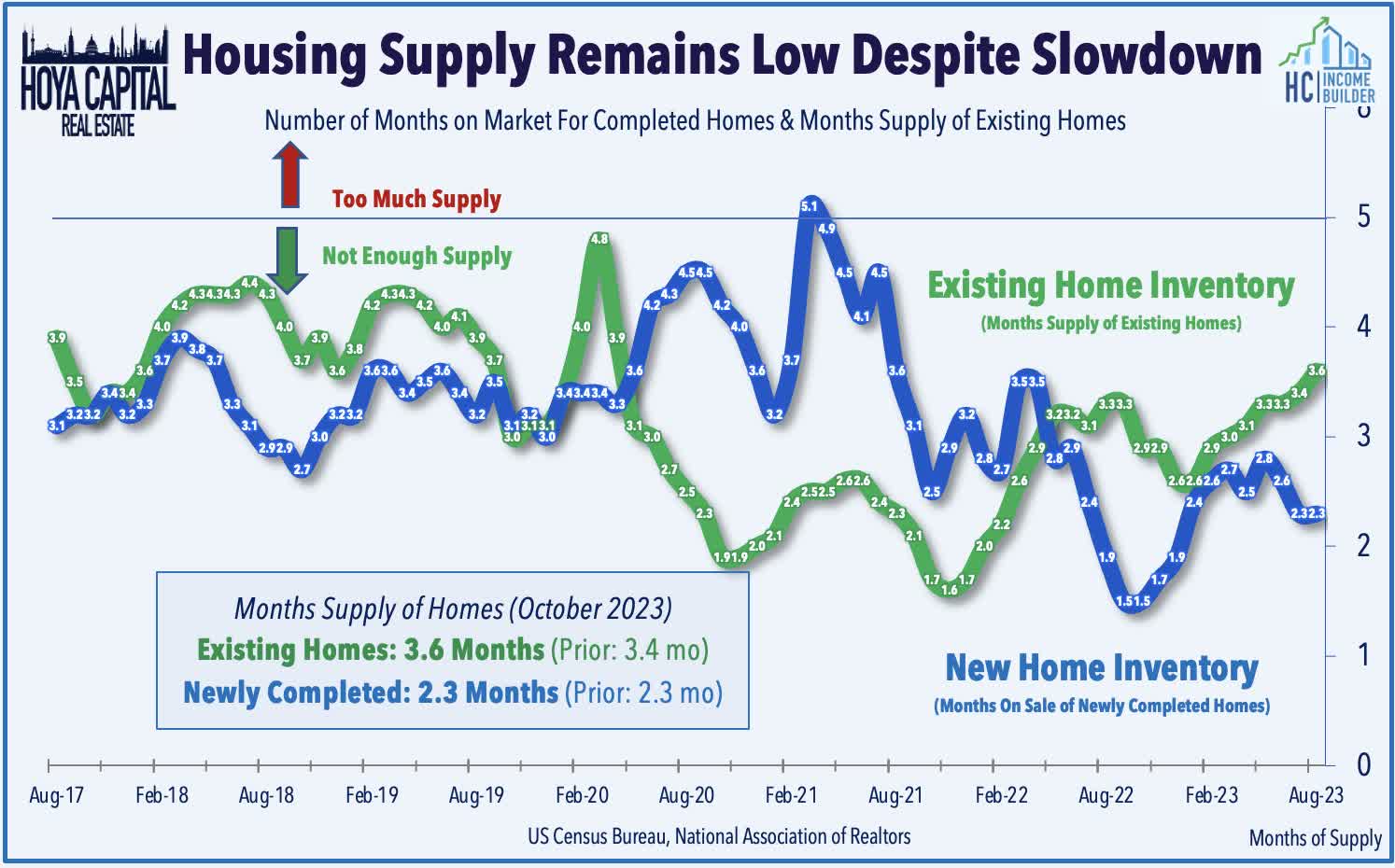

Despite the sales slowdown, inventory levels remain well below historic averages, which has kept a floor on home values and helped to sustain some base level of demand for new home construction in the face of the substantial interest rate headwinds. Total housing inventory was down 5.7% from one year ago, while unsold inventory sits at a 3.6-month supply at the current sales pace - well below the historical average of roughly 6 months. Even with the sluggish overall sales pace, the median existing-home sales price climbed 3.4% from one year ago to $391,800 – the fourth consecutive month of year-over-year price increases. Supply levels of new construction homes remain even lower on a historical basis, with newly completed homes being sold within 2.4 months of listing in the latest report - well below the pre-pandemic average of roughly 3.5 months.

{kind=link}

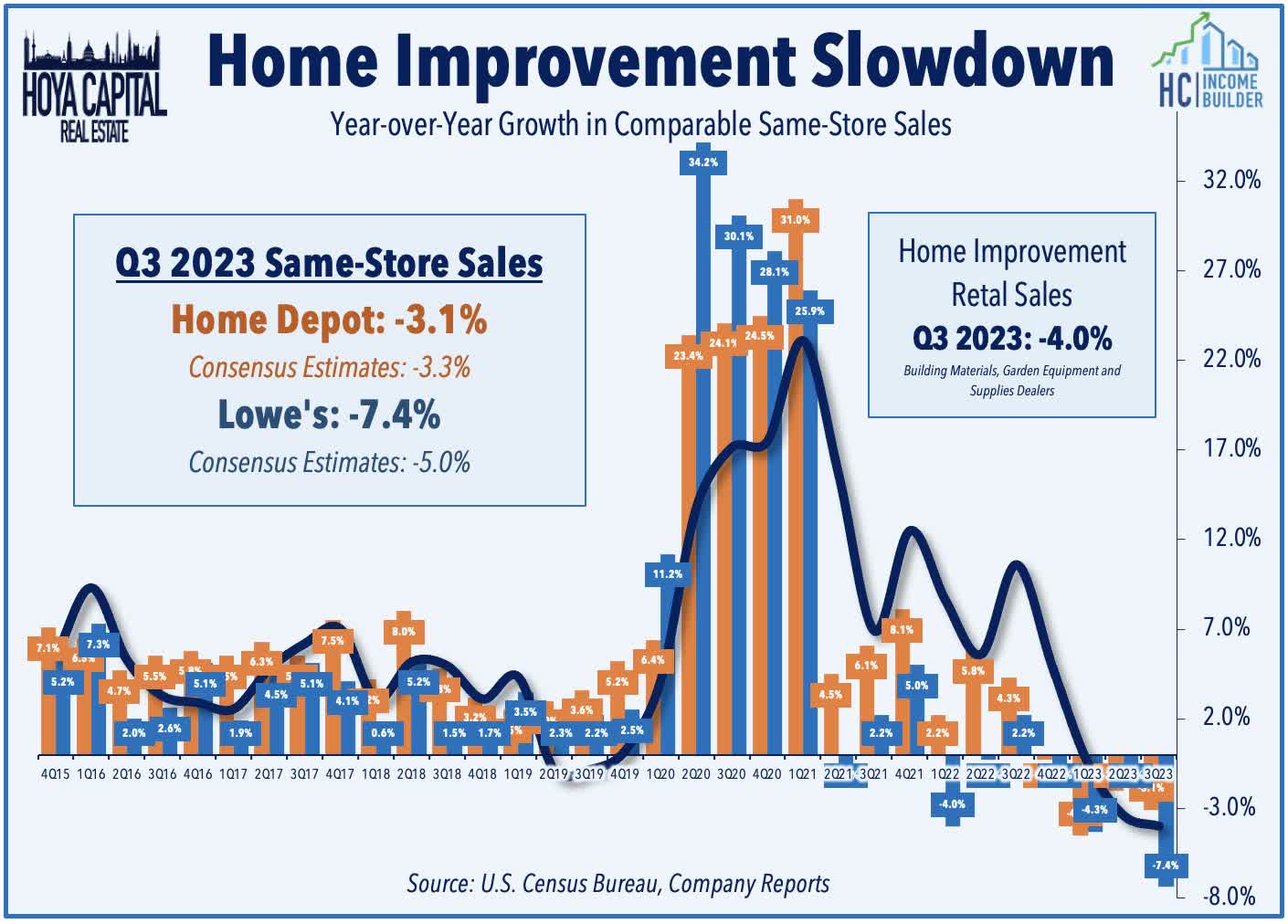

Home improvement spending - which tends to track home sales patterns - has remained similarly sluggish in recent months. Lowe's Companies ( LOW ) - the second-largest U.S. home improvement retailer behind Home Depot ( HD ) reported that it has felt a “greater-than-expected pullback” by customers on discretionary projects and big-ticket purchases. Lowe's reported that its comparable sales dipped -7.4% during the quarter - below consensus estimates and worse than the -3.0% decline reported by Home Depot earlier this month - citing weakness in do-it-yourself ("DIY") trends. Lowe's now expects its full-year comparable sales to be down by -5% - a 200 basis point reduction from its prior guidance of -3%. Lowe's noted that DIY customers drive 75% of its revenue, while the broader market mix is roughly 50% DIY and 50% Professional. Retail Sales data last week from the BLS showed that spending at Home Improvement stores is lower by -5.6% from last year, while spending in the Furniture and Furnishings category is down 11.8%.

{kind=link}

Equity REIT Week In Review

Best & Worst Performance This Week Across the REIT Sector

{kind=link}

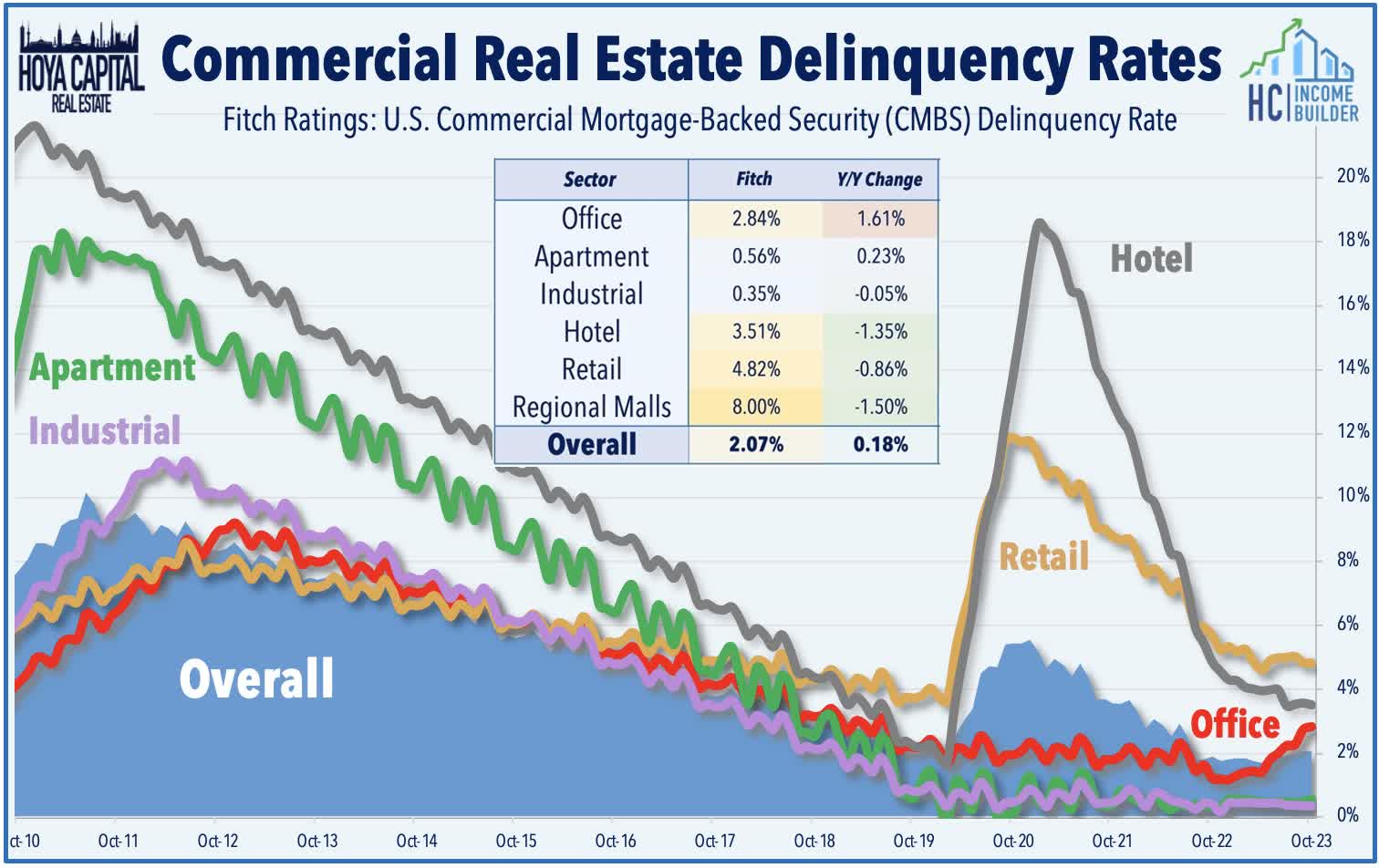

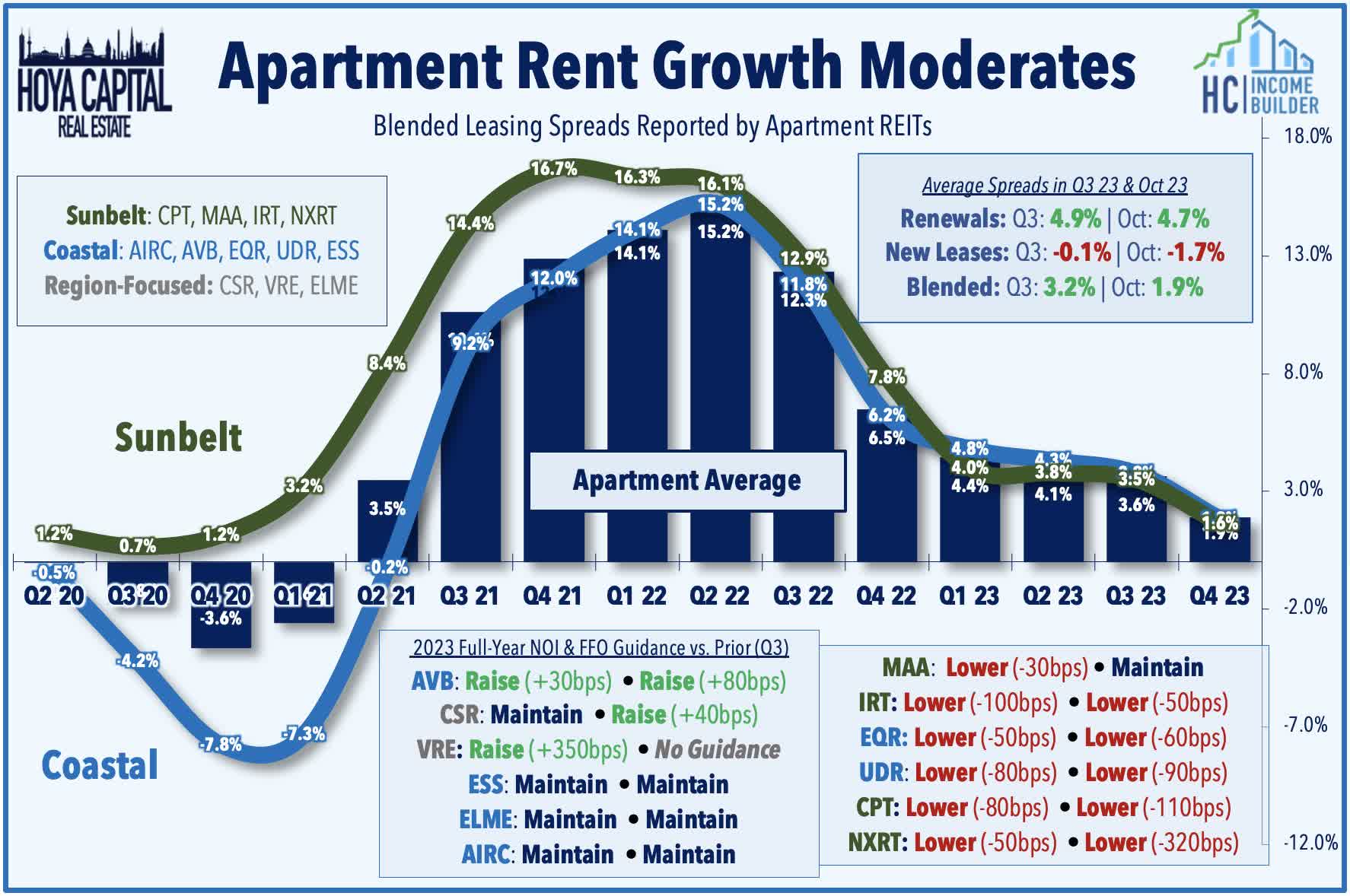

Apartment : On an otherwise quiet week of newsflow across the real estate space, apartment REITs were in focus following a WSJ report that several bidders have emerged in the FDIC's auction process of Signature Bank's $33B real estate loan portfolio following the collapse of the NYC-focused bank in March. In particular focus was the roughly $15B pool of rent-controlled NYC apartment units, which have seen significant value impairment since the passage of legislation in 2019, which made it more difficult for rent-controlled building owners to convert units to market-rate, during which time expense growth inflation has substantially outpaced these units' maximum potential revenue growth. WSJ notes that this loan pool is reportedly selling to Related Fund Management for 70% of the loan's face value, while the FDIC will retain a 95% stake in the portfolio. A number of bidders have emerged for the pool of non-rent-controlled properties - with Blackstone ( BX ) reportedly viewed as the frontrunner - a portfolio that includes a mix of office, industrial, retail, and traditional residential loans. While the narrative on commercial real estate credit is as downbeat as ever, actual loan defaults on CRE loans remain historically low, and the uptick over the past year is almost entirely attributable to office assets. Multifamily is the only other sector that has seen an increase in default rates, with many of these defaults coming from "mom and pop" property owners who financed assets with floating-rate bank debt.

{kind=link}

This week, we published REITworld Recap: Challenges & Opportunities In 2024. Hoya Capital CIO David Auerbach attended the 2023 NAREIT REITworld conference in Los Angeles last week, and had the opportunity to meet with several dozen REIT management teams. With some bullish optimism following the CPI print along with Treasury Yields trending back below 4.5%, the conference was abuzz as many stocks traded in the green throughout the event - a long-awaited rebound following many months of persistent downward pressure. Of note, we saw some revival of the long-dormant "animal spirits" on the external growth front. While we've seen plenty of intra-sector M&A this year via REIT-to-REIT mergers, there was a shared consensus in our meetings that public REITs are poised to reach into the private markets in 2024, utilizing their substantial competitive advantage with both cost of capital and - more importantly - access to capital if macroeconomic conditions do indeed trend towards a "softish" landing. Below, we note some of the highlights from these NAREIT management discussions.

{kind=link}

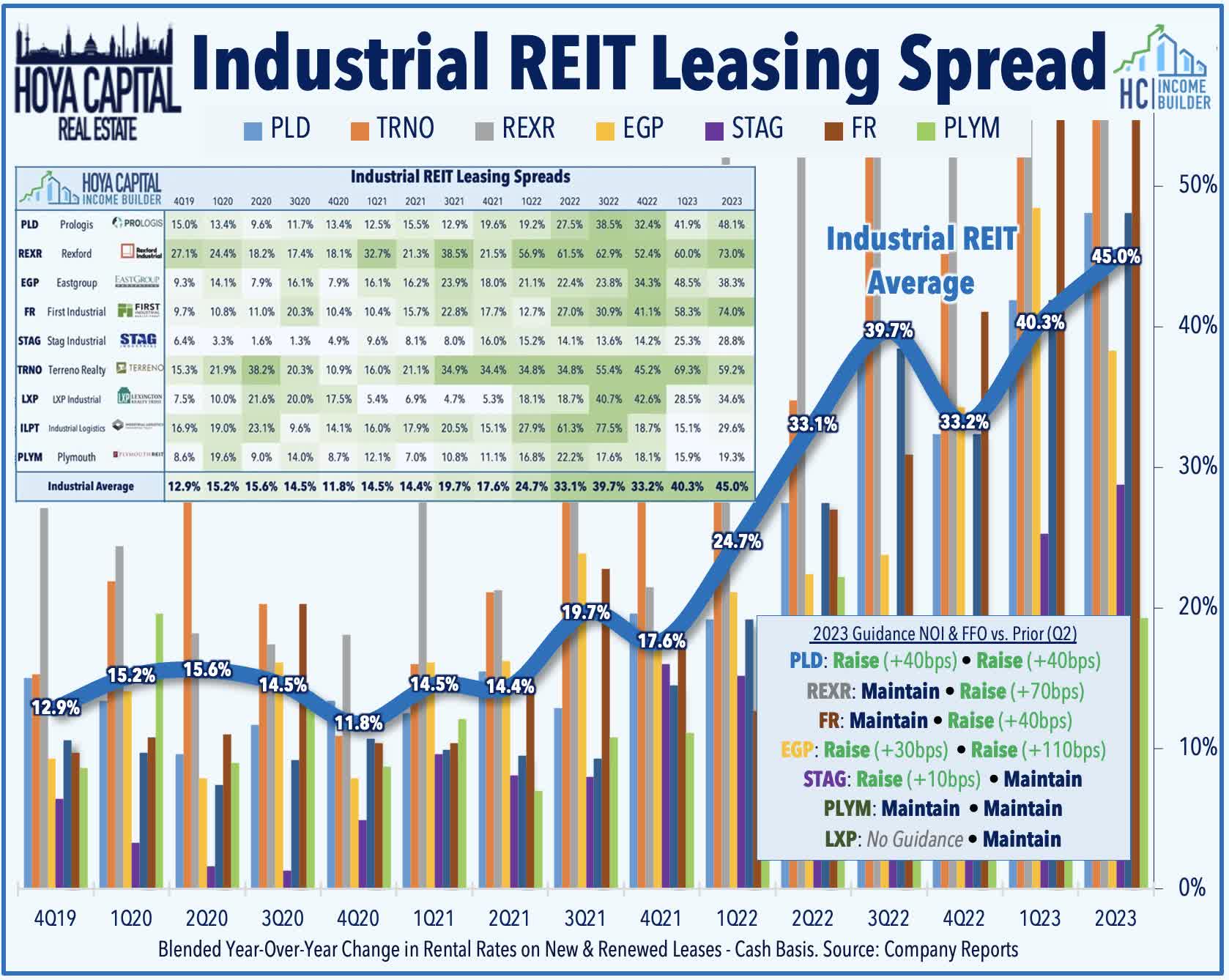

Industrial: Updates on the state of logistics demand were a key focus, given the continued softening evident across the manufacturing and transportation sectors. EastGroup Properties ( EGP ) noted that bulk industrial is slowing while their multi-tenant properties continue to outperform. EGP highlighted their acquisition strategy, with one-offs providing a meaningful driver of growth. They highlighted strong rental growth in El Paso, San Diego and Phoenix and spent time highlighting Tesla in Austin, along with the need for its suppliers to have industrial space near the Tesla property. STAG Industrial ( STAG ) noted that supply/demand is healthy, but occupancy may tick lower in 2024 due to lead time to backfill spaces along with increased supply and it should pick up in ’25. They anticipate 25-30% leasing spreads and note that South Dallas, Indianapolis, and Columbus are “struggling” due to big box size. Terreno Realty ( TRNO ) noted that market rents are “flattish” and that LA remains the weakest market. They noted that 2024 will be the year of opportunity and differentiation” as their strategy continues to be owning the end of the supply chain as opposed to the beginning or middle.”

{kind=link}

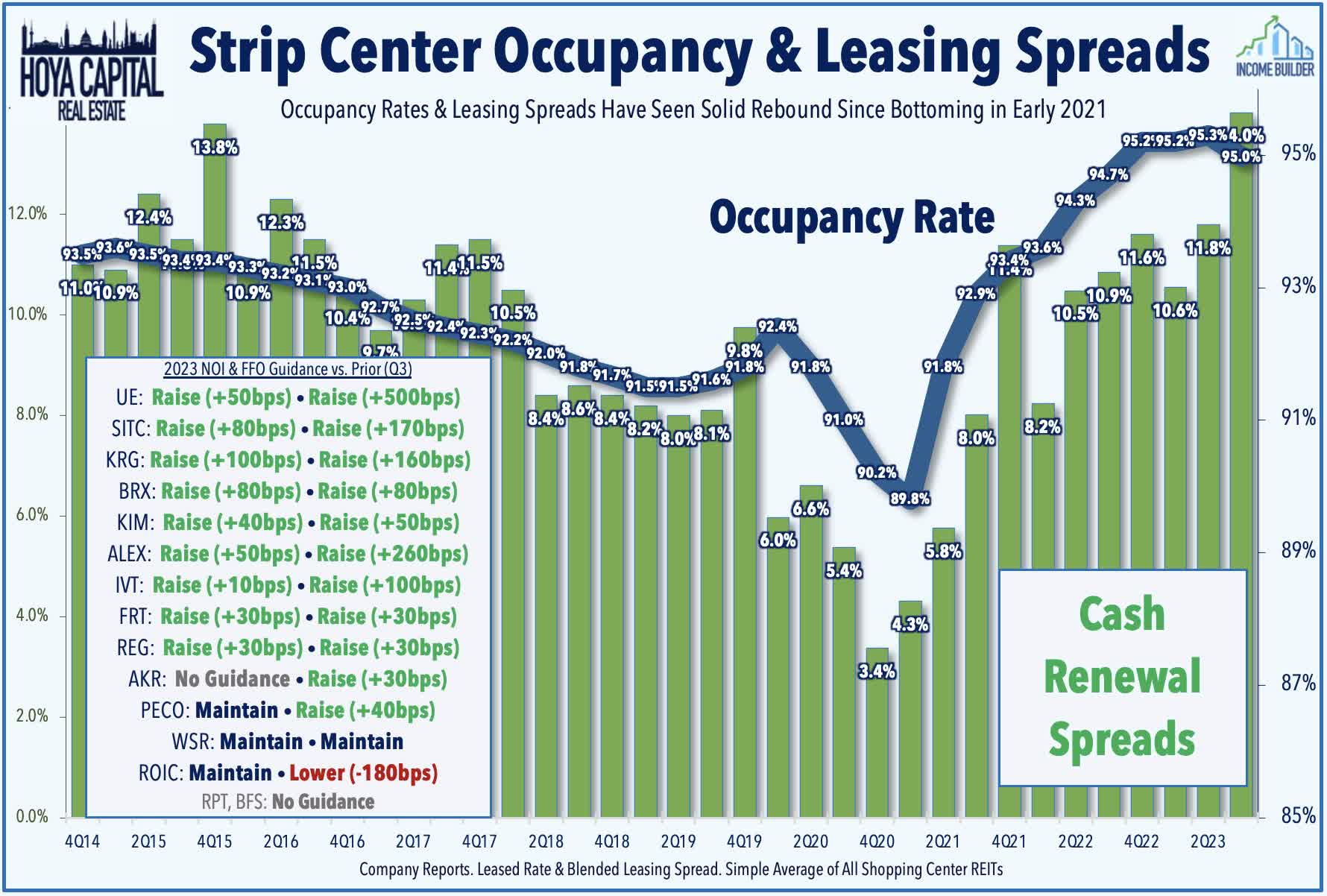

Strip Center : We met with a pair of strip center REITs as well. Kimco Realty ( KIM ) talked about its rent escalators in place along with leasing spreads and noted that they have room to run with small shop tenants as the overall portfolio is only 90 bps below its pre-pandemic occupancy rate. They spent time highlighting the synergies in its pending merger with RPT Realty ( RPT ) along with the integration of the Weingarten portfolio. They also noted that they will be selling the remaining shares in Albertsons (14.2 million shares) next year. Federal Realty ( FRT ) noted its annual dividend increases and its strategy of being in "first ring" suburbs in 9 strategic high-barrier markets as they create value over the long-term through its development pipeline. FRT discussed progress in re-leasing its vacated Bed Bath & Beyond space, and echoed commentary from other strip center REITs that the effect of the Bed Bath bankruptcy will be a net positive for same-store NOI and FFO in 2024 given the double-digit rent spreads achieved on this vacated space.

{kind=link}

Apartment : Updates from residential REITs were status-quo, with a shared sentiment that rent growth headwinds will persist through mid-2024. Mid-America Apartment ( MAA ) highlighted their "building blocks" towards 2024 earnings growth and sees tailwinds ahead beginning in 2025/2026. MAA noted that its "close to the bottom" regarding downward pressure on rent growth. Apartment Income ( AIRC ) stated that it's focusing on tenant retention, noting that its renewals are "20% more profitable" than its new leases. AIRC highlighted its sector-leading tenant retention ratio along with the credit score of its underlying tenants. Centerspace ( CSR ) noted that revenue growth in 2024 is anticipated to be “tough” but believes that tertiary markets should outperform in 2024. Manufactured Housing REIT UMH Properties ( UMH ) spent time focusing on its rental rate increases and delivering over 1000 new homes with 3000 vacant sites currently in its portfolio. They are trying to find acquisition opportunities on properties with 30-60% occupancy and commented on their NOI growth outlook in the future.

{kind=link}

Casino & Net Lease : We also joined Mizuho's analysts for dinner with VICI Properties ( VICI ), who highlighted their busy year expanding their relationship with Canyon Ranch along with their recent sale-leaseback transaction on 38 bowing entertainment centers with Bowlero Corp. as management expects “to execute on more non-gaming equity investments, though will still make up a relatively small part of the overall tenant roster.” Gaming and Leisure Properties ( GLPI ) talked about their "risk thoughtfulness" and their margin of safety, noting that their recent at-the-market secondary equity issuance activity was necessitated by its development pipeline. We chatted with the management teams of CTO Realty Growth ( CTO ) and Alpine Income ( PINE ), who commented on opportunities in structured finance since they aren’t seeing distressed opportunities and highlighted their debt stack with no debt maturities coming due until 2026. We visited with Realty Income ( O ), who spent time highlighting their merger with Spirit Realty ( SRC ) along with talking about the Digital Realty ( DLR ) joint venture and noting that it's looking internationally for other opportunities.

{kind=link}

Additional Headlines from The Daily REITBeat:

- CTO Realty ( CTO ) closed on its $18.2M sale of a 129,600 SF shopping center in Henderson, NV at an exit cap rate of 7.4%.

- Apple Hospitality ( APLE ) completed the acquisition of the 192-room Embassy Suites in Salt Lake City for $36.8M, or $191k per key.

- S&P affirmed Services Properties Trust's ( SVC ) “B+” issuer credit rating, and revised its outlook to Stable from Negative.

- Fitch Ratings affirmed Omega Healthcare's ( OHI ) credit ratings including its “BBB-” Issuer rating, and revised its outlook to Stable from Negative.

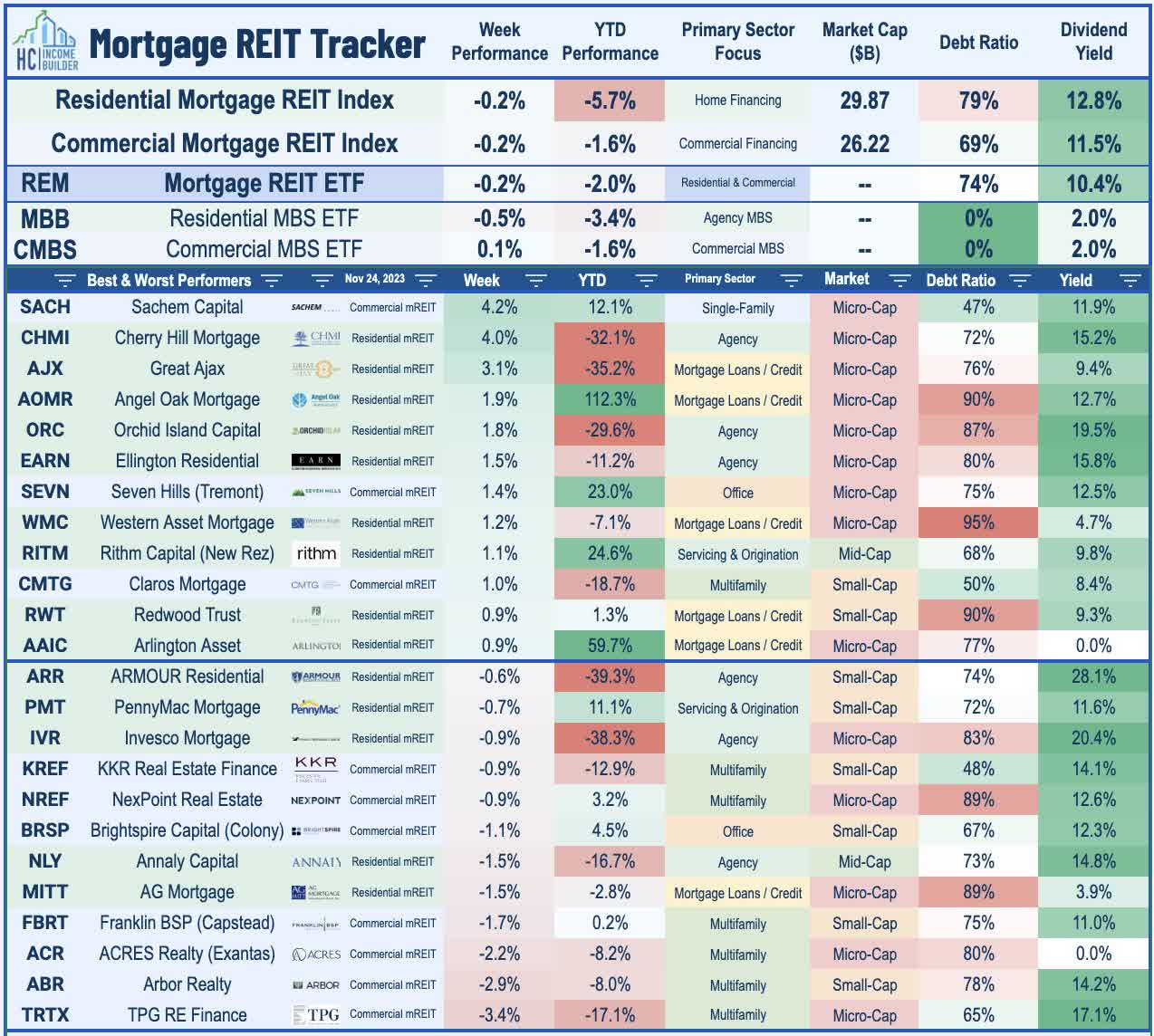

Mortgage REIT Week In Review

Mortgage REITs were little changed on a quiet holiday week of newsflow, with the iShares Mortgage REIT ETF ( REM ) slipping 0.2%. Over the past month, however, mortgage REITs have rebounded by over 15% and are again outperforming their equity REIT peers for the year. AG Mortgage ( MITT ) and Western Asset Mortgage ( WMC ) - which plan to close on their merger next month - each announced a second interim dividend this week to reflect the roughly one-month delay in their closing date from November 9th to its new expected closing date of December 6th. Several small-cap mREITs led the gains this week, including Sachem Capital ( SACH ) and Cherry Hill ( CHMI ). On the downside this week, multifamily lender Arbor Realty ( ABR ) remained under pressure from the short report from Viceroy Research last week.

{kind=link}

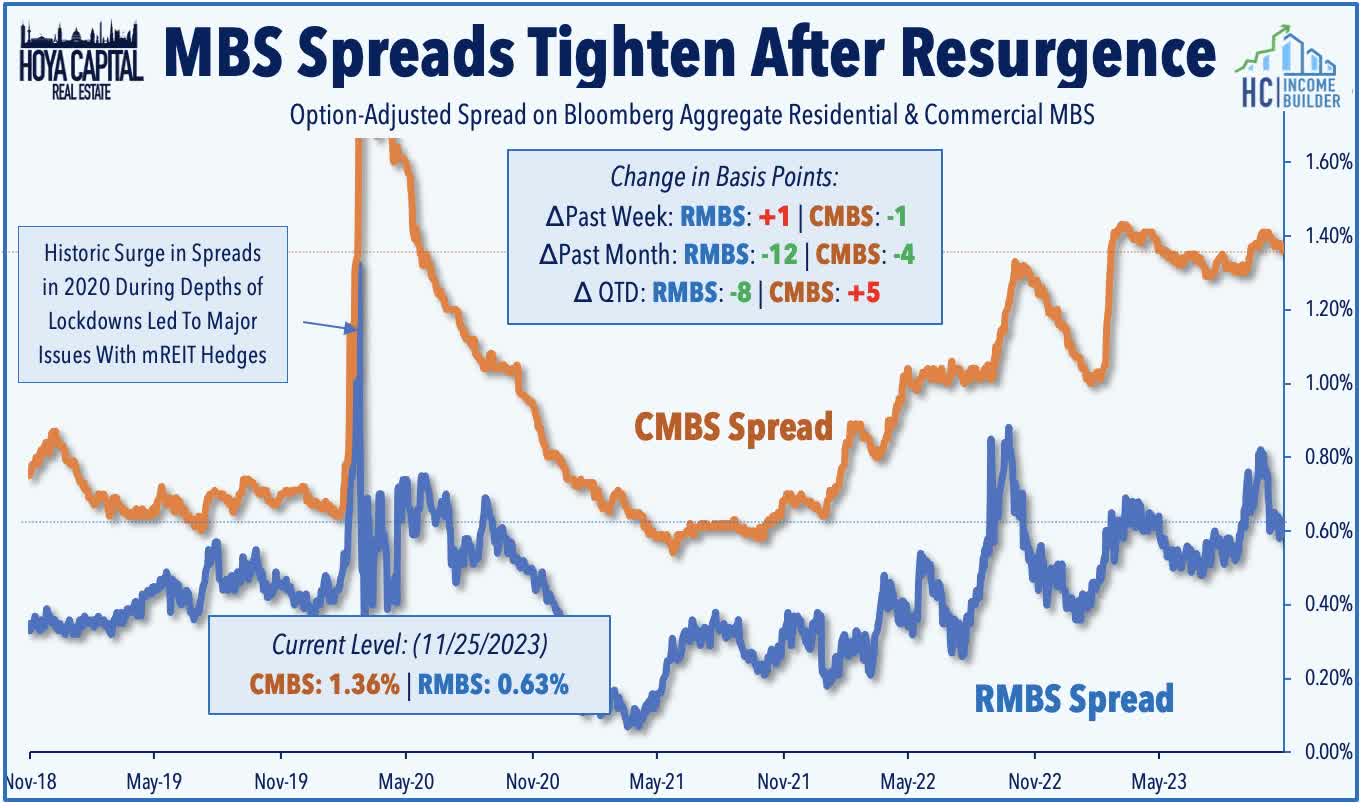

In our Earnings Recap , we noted that the (now largely reversed) surge in interest rates and MBS spread-widening wreaked havoc on residential mortgage REITs during the third quarter, resulting in a significant deterioration in book values for mREITs focused on government-backed ("agency") residential MBS. Agency-focused mREITs reported an average decline in Book Value Per Share ("BVPS") of 13.1% during the quarter, but credit-focused mREITs reported more muted declines in BVPS, averaging around 5%. On the commercial mREIT side, the movement in BVPS was far more muted, with an average decline of about 1% in the third quarter. Residential MBS spreads have compressed by 8 basis points since the start of Q4, while Commercial MBS spreads have widened by about 5 basis points.

{kind=link}

2023 Performance Recap & 2022 Review

With just five weeks left in 2023, the Equity REIT Index is now lower by 3.3% on a price return basis for the year (0.3% on a total return basis), while the Mortgage REIT Index is lower by 2.0% (+7.7% on a total return basis). This compares with the 19.1% gain on the S&P 500 and the 5.8% gain for the S&P Mid-Cap 400 . Within the real estate sector, six property sectors are in positive territory on the year, led by Data Center, Single-Family Rental, and Healthcare REITs, while Office and Net Lease REITs have lagged on the downside. At 4.47%, the 10-Year Treasury Yield has climbed 59 basis points since the start of the year - up sharply from its 2023 intra-day lows of 3.26% in April - but down from peaks above 5.0% in mid-October. Following the worst year for bonds in decades, the Bloomberg US Bond Index is slightly higher this year, producing total returns of 0.5% thus far. WTI Crude Oil - perhaps the most important "swing" inflation input - is higher by 1.0% this year, while Natural Gas is lower by over 55% this year.

{kind=link}

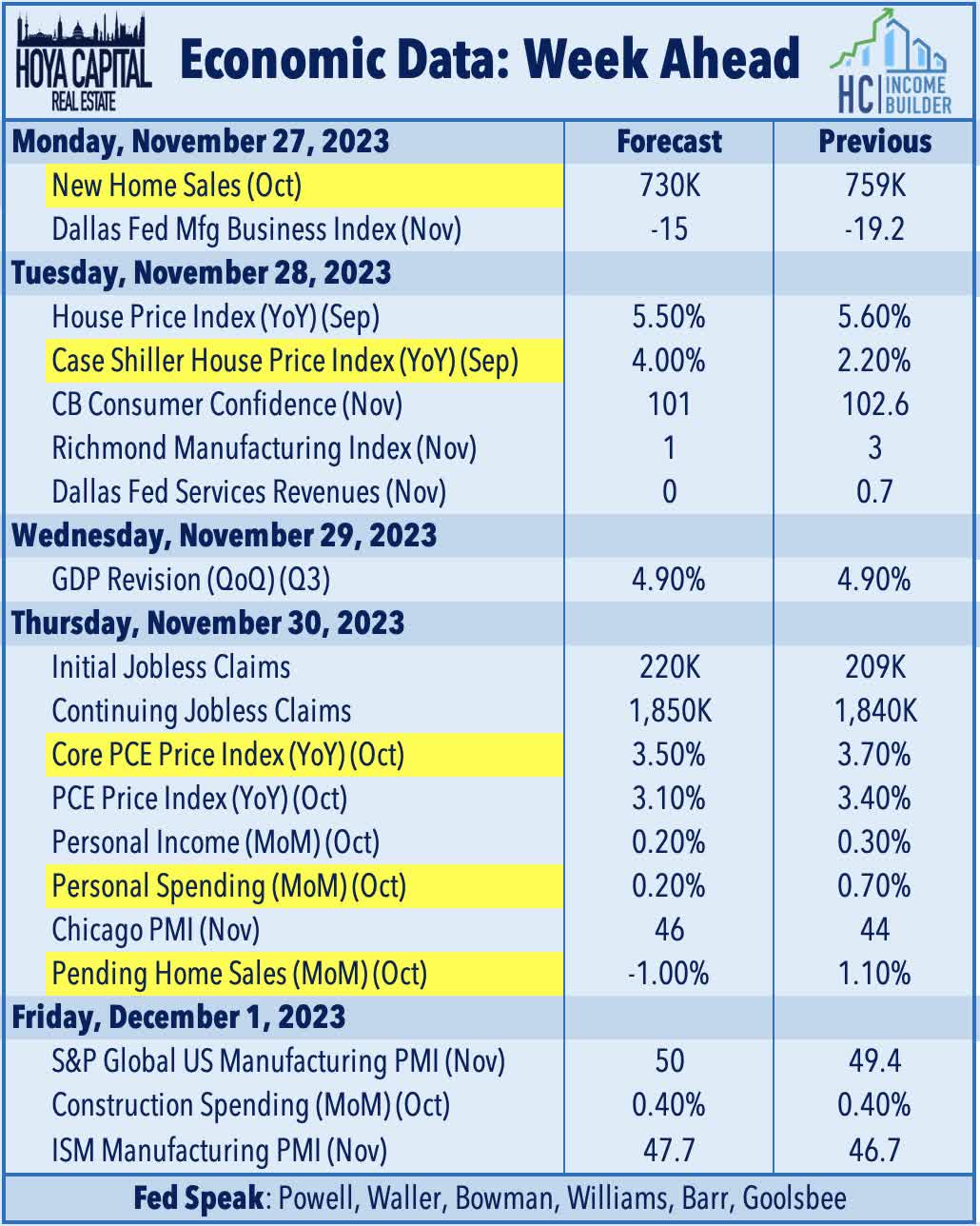

Economic Calendar In The Week Ahead

The economic calendar heats up again in the week ahead following the Thanksgiving recess. The most closely-watched report of the week comes on Thursday with the PCE Price Index - the Fed's preferred gauge of inflation - which is expected to show a year-over-year increase of 3.5% - down from the 3.7% increase last month and down sharply from the 7.0% rate seen a year ago. We'll also get our second look at third-quarter Gross Domestic Product, which showed an expansion of 4.9% in its initial reading - confirming the surprising reacceleration in economic activity seen during the late summer months. The Atlanta Fed's GDPNow estimates that Q4 GDP is trending at 2.1%, which would result in full-year GDP growth of roughly 2% - down from 4.4% in the prior year. The state of the U.S. housing market also remains in focus in the week ahead, with New Home Sales data on Monday and Pending Home Sales on Thursday. The housing industry had briefly emerged from a rate-driven recession from mid-2021 through early-2022 before facing renewed pressure from higher rates in late summer and into early Autumn. The largest single-family homebuilders have, so far, been able to cope with multi-decade-high mortgage rates by leveraging their platform's scale to offer more attractive financing options than what's currently available for prospective homebuyers in the traditional existing home sales market. We'll also be watching the Case Shiller Home Price Index report on Tuesday, Jobless Claims data on Thursday, Construction Spending data on Friday, and a flurry of PMI data throughout the week.

{kind=link}

For an in-depth analysis of all real estate sectors, check out all of our quarterly reports: Apartments , Homebuilders , Manufactured Housing , Student Housing , Single-Family Rentals , Cell Towers , Casinos , Industrial , Data Center , Malls, Healthcare , Net Lease , Shopping Centers , Hotels , Billboards , Office , Farmland , Storage , Timber , Mortgage , and Cannabis.

Disclosure : Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index . Index definitions and a complete list of holdings are available on our website.

{kind=link}

For further details see:

A November To Remember