ACTV - A Soft February Jobs Report Or Cold CPI Can Set Up The Next Rally In Stocks

2023-03-09 02:17:04 ET

Summary

- The market appears too aggressive expecting a 50-basis-point rate hike at the next Fed meeting.

- A "soft" payroll report or slowdown in the CPI update could be bullish for stocks by resetting monetary policy expectations.

- We highlight the themes to watch over the next few weeks.

Fed Chairman Jerome Powell's latest semi-annual testimony to congress drove a renewed round of market volatility. The quotes from the event that stood out are that the economy has been "stronger than expected" and that the disinflationary process was "not unfolding smoothly". This setup opens the door for further rate hikes including the possibility of a faster 50 basis point increase at the next FOMC later this month.

The S&P 500 ( SPX ) sold off by about 1.5% on the day and is down on the week. In many ways, there wasn't necessarily any new insight from the event, which rehashed recent indicators going back to the exceptional labor market trends and the monthly surprise higher in the January CPI.

Nevertheless, stock market bears and doom-and-gloomers are seeing a signal for the start of a "big crash lower". This is the same group that has been running in circles attempting to explain away the recent market strength, still waiting for a new cycle low. Keep in mind that SPX is up more than 12% from its 2022 bottom and higher compared to levels last May and June, nearly 9 months ago.

In our view, it's too early to close the door on a 25 basis point hike for the March meeting, and an expectation for stocks to sell off further is far from certain. There are many moving parts here, but our message is that the underlying bullish momentum in the stock market remains in place and we believe there is more upside to the S&P 500 going forward.

The main event this month is still to come starting with the February payrolls report on Friday, March 10th followed by the February CPI update. Simply put, the potential for a "soft" jobs number or cooler inflation trend can work to reset the narrative into the upcoming Fed Meeting.

We see a good chance of those two indicators surprising to the downside. In this scenario, stocks could get a boost higher as interest rate forecasts to roll back with a confirmation of the disinflationary process and evidence the Fed's policy strategy is working.

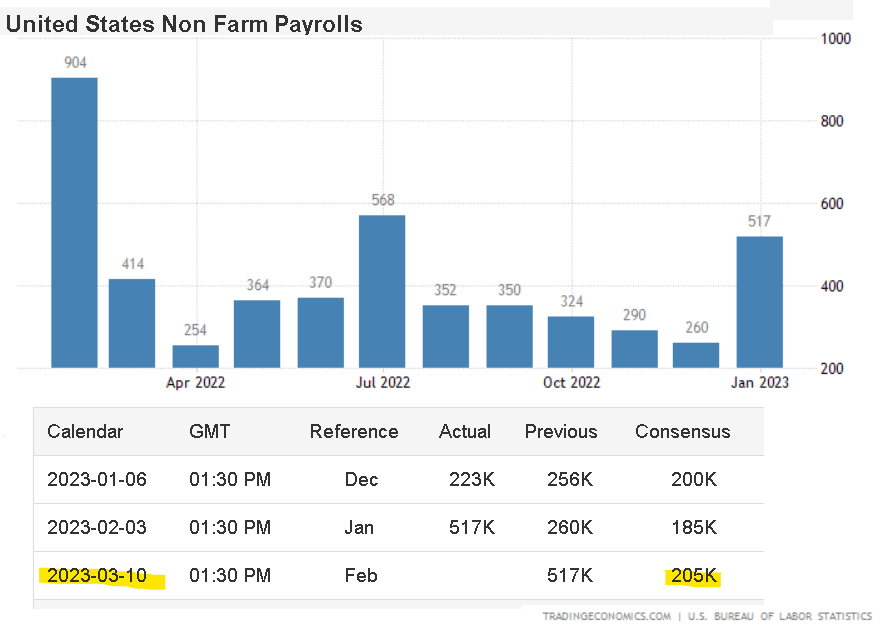

February Payrolls Report Preview

The problem stock market bears are facing is the challenge of reconciling a view that inflation is re-accelerating while also predicting economic conditions to collapse.

That juxtaposition comes into play with the upcoming payrolls report where signs job gains are slowing would undermine the view that the labor market is still too hot as a core inflation driver.

Looking back at the January report, the U.S. added 512k jobs in what was seen as a "blowout" number. Beyond seasonal adjustments and solid trends from industries like leisure and hospitality, the surprise was that the data failed to capture reports of widespread layoffs in tech and business services.

So when we look at the current estimate for 205k job gains in the upcoming February data, it's fair to hold an ounce of skepticism. We have some room for a lower number considering the forecasts from economics have failed to hit the target on many fronts.

One dynamic that could be on the table is a time lag with companies pulling back on hiring plans into the new year that gets reflected in February but missed in January. The wage growth component will also be closely looked at. By all indications, companies are cutting back on bonuses and salary increases which is in contrast to trends from early 2022.

Even at the consensus, it's hard to see why the Fed would take a more aggressively hawkish route from what would be the slowest month of employment gains in over a year. Stock market bears need to be rooting for another scorching non-farm payrolls number to set the alarms off that demand-side inflationary pressures are still a big concern. That's a hard bet to take right now.

{kind=link}

source: tradingeconomics

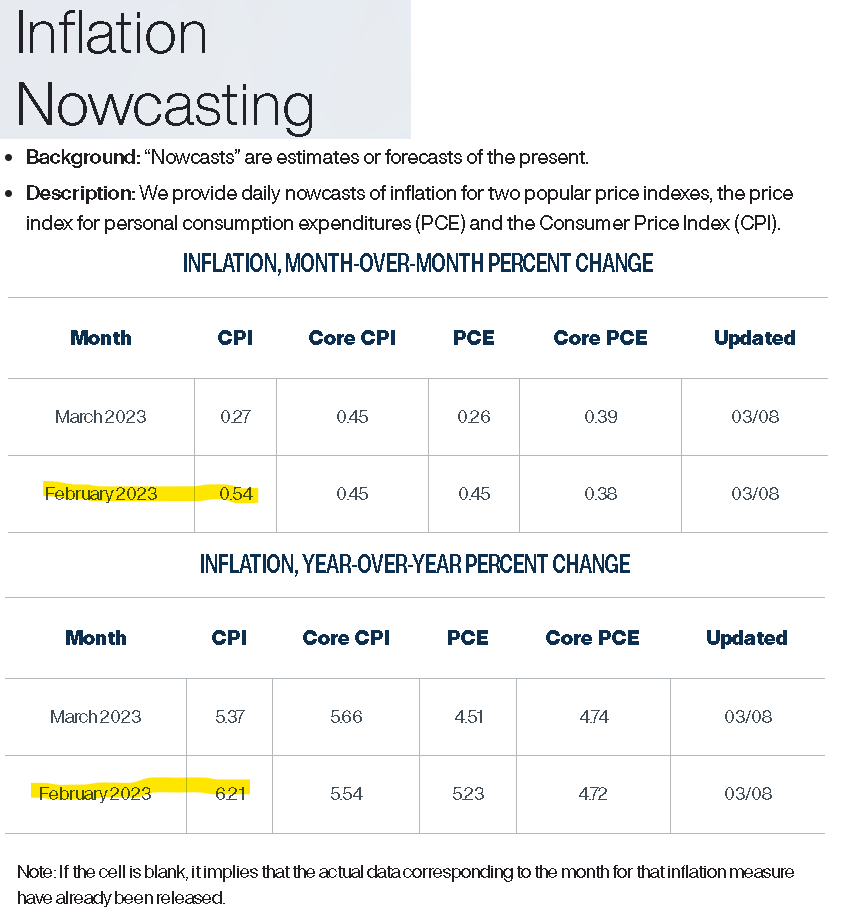

Importance of the February CPI Data

Even more important than the jobs report will likely be the February CPI update on March 14th, ahead of the Fed's March 22nd meeting.

Currently, the data we're looking at from the Cleveland Fed suggests a " Nowcast " for the February CPI to climb by 0.5% m/m, mirroring the trend from January. Favorably, the annual rate should still narrow to 6.2% compared to 6.4% in January. Even more encouraging is the March CPI Nowcast, for next month, which is currently at an annual CPI of 5.4%, nearly 100 basis points lower compared to the January rate, getting into tough comparables from last year.

The setup here is simple. A "cold" or lower-than-expected figure between the headline monthly and annual rate, or core component (excluding food and energy) could indicate that the January blimp higher was simply an anomaly.

{kind=link}

source: Cleveland FED

We sense that the burden of proof for the inflation hawks is to get a "hot" number, which may not be that straightforward. The last time the monthly CPI was above 0.5% was last June. Considering the cumulative effects of higher rates over the period, and the slowdown in major pricing categories, it's a stretch to claim monthly inflation is running hotter today than it did in Q2 2022.

We can go through several commodity charts across energy, agriculture, grains, and metals to demonstrate that the trend was negative during February. Key items like oil and gas are down over the past year and specifically declined during the month. Our call is for core services to start trending lower.

Compared to the 0.5% m/m CPI estimate, a 0.4% figure would make the headlines surrounding the report revolve around the sigh of relief. These types of optics matter when the Fed decides between a 50 basis point or 25 basis point hike at the next FOMC.

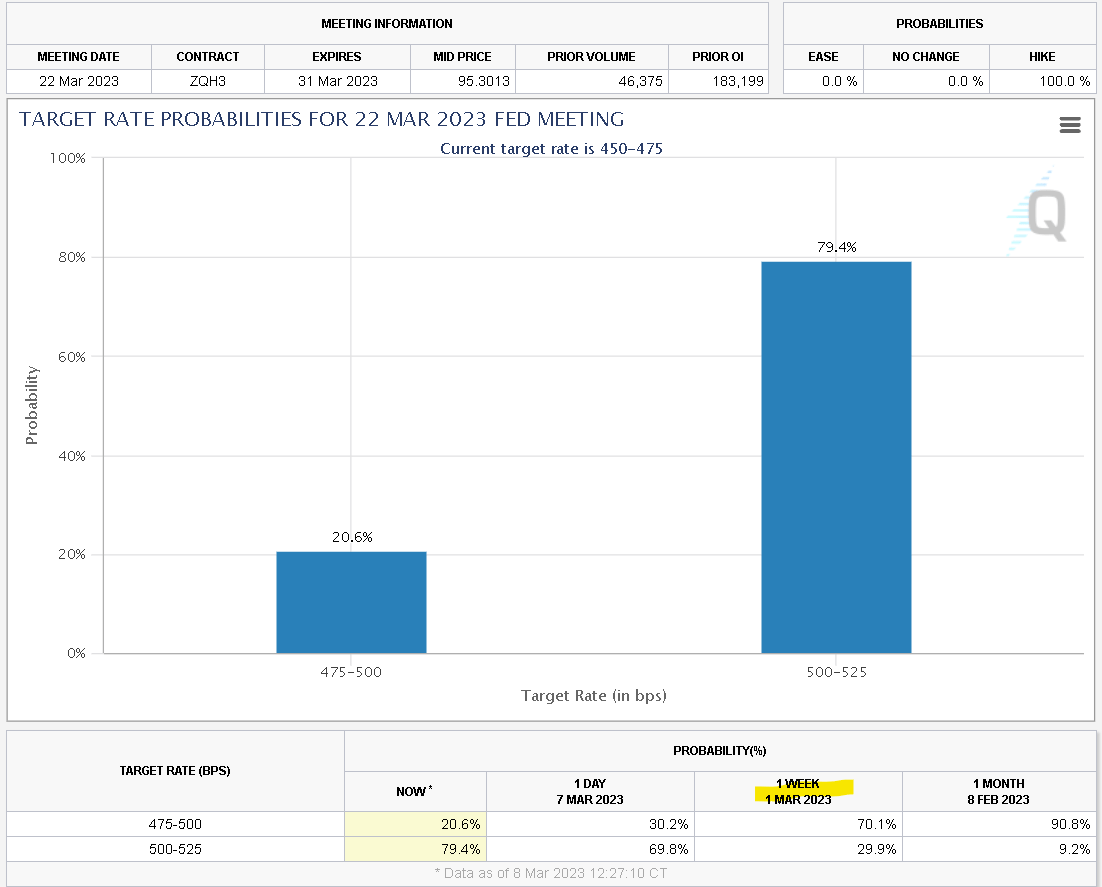

Path for a 25 Basis Point Rate Hike In March

According to the CME " FedWatch Tool " which quantifies the market-implied expectation for the direction of Fed policy, rate futures suggest a 79.4% the Fed will hike by 50 basis points to an upper range in the Fed Funds Rate of 5.25%. This view has shifted from as low as 9.2% last month and 29.9% last week, before Powell's latest round of comments.

Our thinking here is that these current estimates are too aggressive, especially considering the uncertainty around the payrolls and CPI over the next week. We can bring up here that on the second day of testimony, Powell specifically stated no decision on the pace of the rate hikes has been reached yet. This confirms that the Fed is data-dependent and their forecasts are subject to change as new data comes in.

A February payrolls figure under 200k and subdued CPI would help make the case that a 25 basis point hike to 5.0% at the March FOMC still makes sense. In other words, we believe the true probability may be closer to 60/40 on the side of a 25 basis point hike which highlights the opportunity as it relates to the direction in stocks against the cloud of pessimism.

{kind=link}

source: CME

Final Thoughts

The next couple of weeks will be critical to set the stage for the next big move in stocks. Ultimately, the bullish case for the S&P 500 and other broad market equity indexes centers around the "soft landing" scenario. Ideally, we want to see the U.S. and the global economy avert a deep recession while inflation trends lower allowing interest rates to stabilize.

Just getting an annual rate inflation rate of around 4% later this year would still not be at the 2% Fed target, but hardly "out of control". This backdrop would help build confidence toward a stronger growth "recovery" into 2024.

The key monitoring point here that supersedes economic data points comes down to corporate earnings. The ability of major companies to continue managing margins and deliver profitability works as a strong level of support to the market.

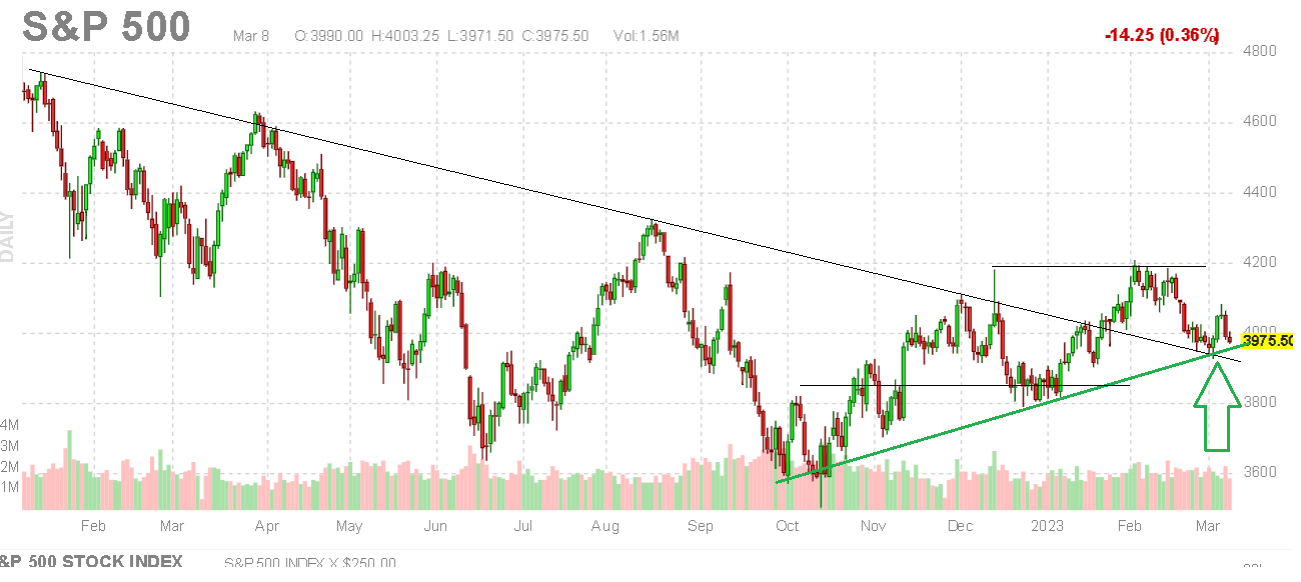

Until those factors materially change, we're maintaining a bullish view on equities. To the upside, the first target here is $4,200 where a breakout could put $4,500 in sight over the next several months. On the downside, it will be important for the market to hold $3850-$3800 as an important area of support.

{kind=link}

source: finviz

For further details see:

A Soft February Jobs Report Or Cold CPI Can Set Up The Next Rally In Stocks