ACTV - A Sticky CPI Along With Hot Jobs Report May Kill Hopes For Rate Cuts

2023-04-09 06:15:00 ET

Summary

- The jobs report was stronger than expected, and repriced rate hike odds.

- The CPI report is likely to show that inflation is sticky.

- The market will be upset when it finds out there will be a rate hike in May and no rate cuts in 2023.

This week, the focus will shift from the jobs market to inflation, with the CPI report due April 12. The report is expected to have a significant wrinkle, as core CPI is likely to have risen by more than the headline CPI for the first time in a while, providing clear evidence that inflation is sticky.

If the headline CPI meets expectations or misses some, it isn't going to matter; the Fed is still likely to raise rates by 25 bps in May. The odds of a Fed rate hike have increased to 70% from around 50% before the jobs report. Unless there is a significant miss on the CPI, it won't matter; the Fed's goal is to get the Fed's Fund rate above 5% because inflation remains too high.

This development may upset the equity market, as it has already priced in a Fed pause and rate cuts, given the recent rally since mid-March and the strong performance in the technology-heavy and interest rate-sensitive NASDAQ.

Jobs Report Was Stronger Than Expected

The jobs report on the headline non-farm payroll establishment survey was stronger than expected, with 236,000 jobs added, higher than estimates for 230,000. Last month's numbers were also revised upward to 326,000 from 311,000. The household survey saw even bigger beats, with the unemployment rate falling to 3.5% (below estimates for 3.6%) and the labor participation rate rising to a new cycle high of 62.6% from 62.5%. Wage growth continues to increase at a pace inconsistent with a 2% inflation rate.

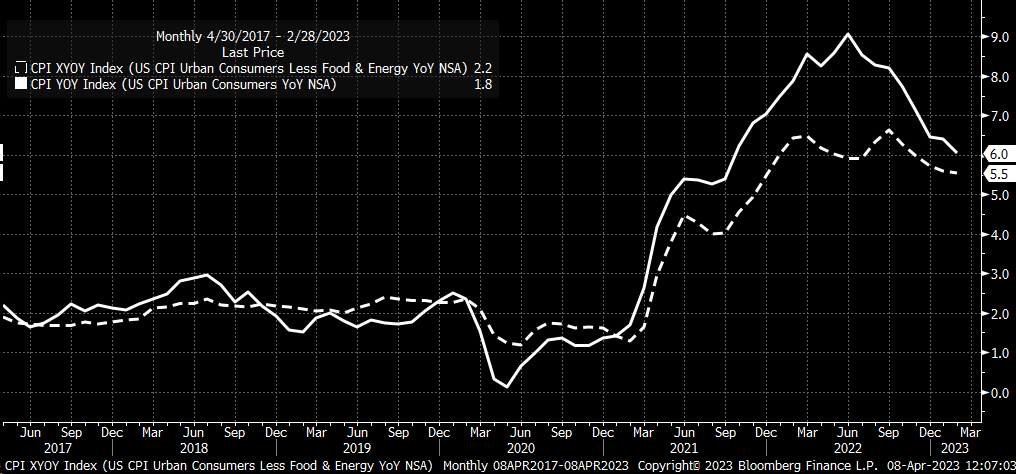

Headline CPI Is Becoming Less Important

For March, CPI is expected to rise by 0.2% month over month and 5.1% year over year, which is slower than the February reading of 0.4% and 6.0%, respectively. Meanwhile, core CPI is expected to rise by 0.4% month over month and 5.6% year over year. In February, core CPI rose by 0.5% and 5.5%. If core CPI rises by 5.6%, it will be the first time since September that it has increased and the first time since the beginning of 2021 that core CPI is rising faster than headline CPI.

{kind=link}

Meanwhile, the Cleveland Fed is projecting core CPI to rise by 5.7%, slightly higher than the analyst median estimate of 5.6%. Unfortunately, we can't rely on inflation swap pricing this time because there is no pricing available for core CPI, only for headline CPI. The swap market suggests that headline CPI will rise by 5.1%, which aligns with analysts' expectations. However, based on those swaps, inflation is expected to increase in April, with year-over-year gains of 5.2%.

{kind=link}

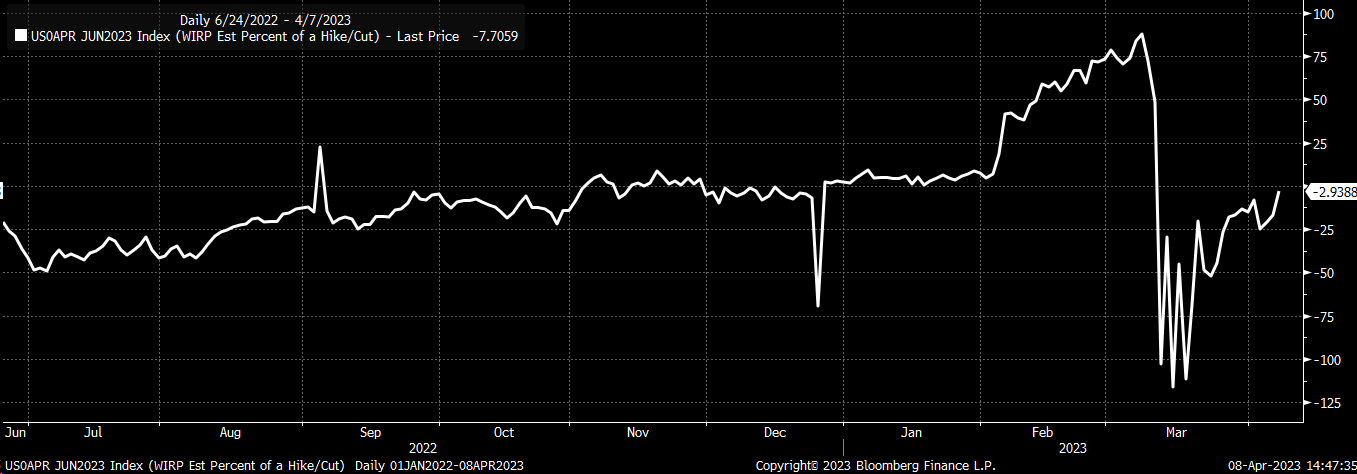

Odds Increase for May Rate Hike

Given the strong March jobs report and the expected sticky core CPI report, the odds of a 25 bps rate hike in May will likely increase further from the current 70% odds for the May meeting. Although a 25 bps rate hike would be much lower than anticipated before the Silicon Valley Bank meltdown, as the stress in the banking system eases, it may give the Fed more room to keep pushing rates higher beyond May.

{kind=link}

The market had been pricing in increasing odds of rate cuts in June. However, following the release of the jobs data, those odds have vanished, and no rate cuts are now expected in June.

{kind=link}

Recent Stock Market Rally Overdone

The recent rally in technology and mega-cap stocks suggests that the equity market has been pricing in rate cuts. If the data continue to support another rate hike in May and the possibility of no rate cuts in 2023, then the recent rally in stocks may be overdone and must be corrected. It's also possible that nominal and real rates could begin to rise again soon.

Furthermore, despite the recent rally, the NASDAQ earnings yields minus the 10-year TIP rate are still very low. This suggests that the NASDAQ remains overvalued compared to real yields, more so than at any other point over the past decade.

{kind=link}

It's not just the NASDAQ that's overvalued compared to bonds. The S&P 500 dividend yield is also very low compared to the 10-year rate, and the spread between the two is trading at its highest level in over a decade.

{kind=link}

The equity market wants the Fed to be done with rate hikes and is betting that rates will begin to fall given the wide spreads and the recent rally in the NASDAQ and the S&P 500. However, the data that the Fed is focused on, such as the jobs data and the inflation data, does not support the Fed's rate-hiking cycle being over or for rate cuts.

Softening Economy

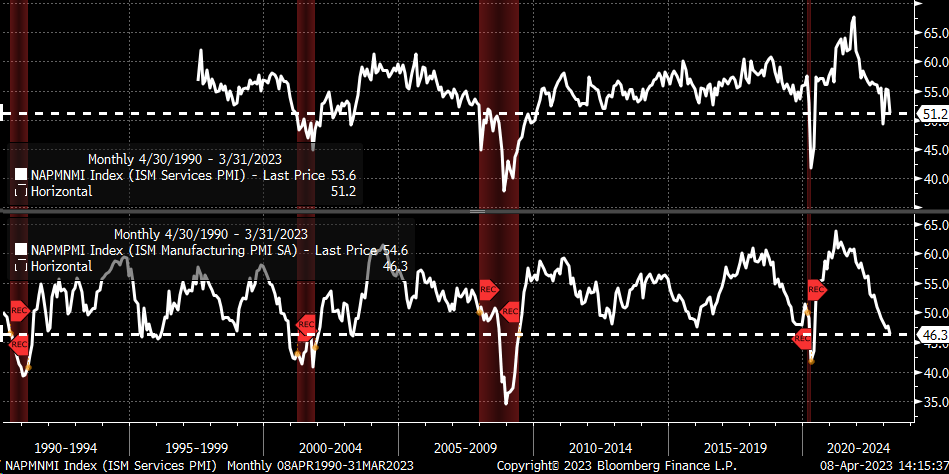

On the other hand, survey data supports that the Fed is done with rate hikes and suggests a substantial economic slowdown is occurring. The ISM manufacturing data fell to 46.3 in March, and levels this low tend to be associated with recessions. Meanwhile, the Services survey showed the index fell to 51.2, close to recession levels.

{kind=link}

In addition, it's now clear that the Fed is not conducting QE as the size of its balance sheet shrinks. This is due to the usage of the Fed's discount window continuing to decline and the pace of banks using the lending facility slowing down materially.

{kind=link}

Over the next couple of days, as the equity market continues to digest the fact that there is no QE and that the Fed is likely to continue to hike rates in May and potentially beyond, that bank stress continues to ease, and no rate cuts. The recent rally in the NASDAQ will need to unwind, and the market will need to voice its opinion that the Fed needs to stop raising rates because the soft data suggest that the economy is slowing dramatically.

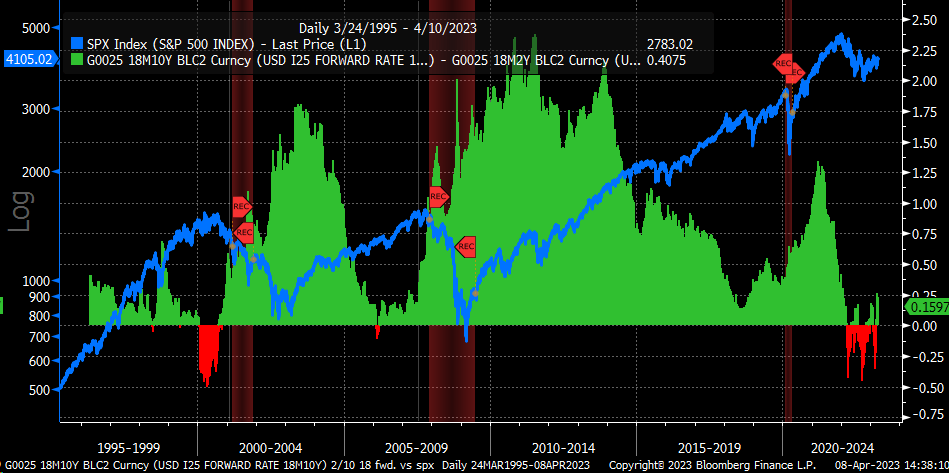

Currently, the 18-month forward 10-2 spread is steepening dramatically, and typically when that spread begins to rise, it is lights out for the equity market.

{kind=link}

Stocks aren't cheap and offer no earnings growth in 2023, while the outlook for 2024 is becoming increasingly shaky.

For further details see:

A Sticky CPI Along With Hot Jobs Report May Kill Hopes For Rate Cuts